This research report has been funded by Kast. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Kast. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

The Neobank Landscape

Key Takeaways

- Neobanks are no longer defined by features, they are defined by who owns the user’s primary financial relationship. Banking apps, brokerages, exchanges, and superapps are converging toward the same goal: becoming the main interface through which users save, spend, earn, and move money.

- The strongest neobank economics come from credit and balance-sheet monetization, not payments alone. Interchange and payment fees are useful entry wedges, but the most mature and durable models compound through lending, net interest income, and broader financial cross-sell.

- Stablecoin-first neobanks have the clearest structural edge in emerging markets and cross-border use cases. Their advantage is not just better UX, but globally portable dollar access, higher potential yield, and cheaper international money movement in markets where traditional banking is weakest.

- The long-term moat is shifting from licenses and front-end UX toward data, infrastructure, and execution control. Winners will be the platforms that combine strong distribution with proprietary behavioral data, robust fiat/onchain infrastructure and, eventually, the ability to underwrite credit and support agent-driven financial activity safely.

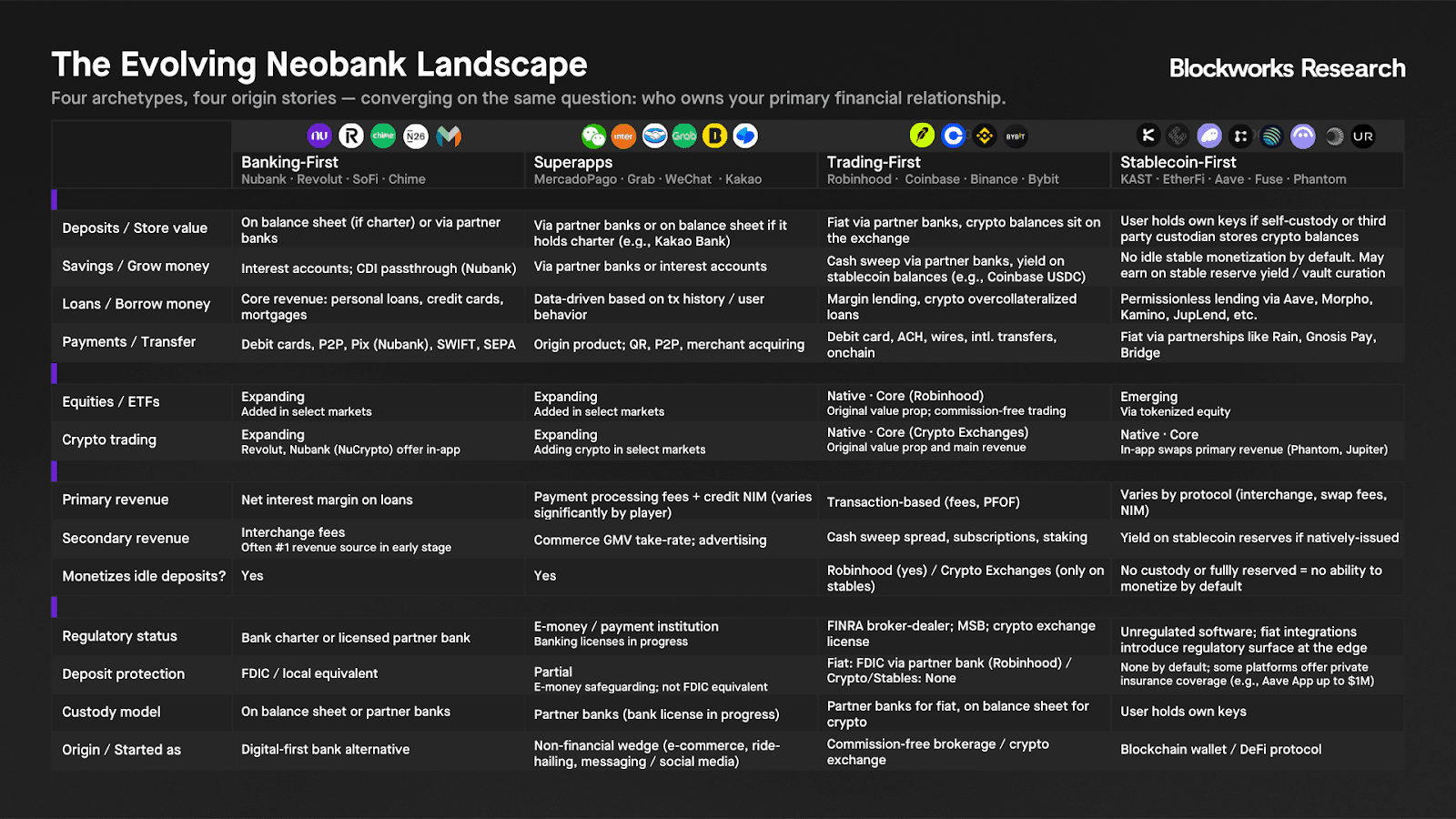

The Evolving Neobank Landscape

Ask ten investors what a neobank is, and you'll get roughly the same answer: digital-first, mobile-only, bank-like functions. Ask ten consumers which app they actually run their financial life through, and the answers get a lot more interesting. First-generation neobanks added investing, brokerages added banking features, and crypto exchanges added cards and yield on stablecoin balances. The lines are blurring, and rather than define a neobank by a feature set, it's increasingly useful to ask: do users treat this app as their primary relationship with money?

The convergence story is path-dependent. In the US and Europe, where banking penetration was already high, neobanks emerged as a bank-switch pitch: legacy infrastructure wrapped in better software. In Latin America and Southeast Asia, where it wasn't, fintech arrived through multiple paths: cards-first neobanks like Nubank, but also commerce-first platforms like MercadoPago and Grab that embedded finance into products people already used daily. That second path has no real equivalent in the US or Europe, and the same structural conditions that enabled it are where stablecoin-first neobanks are most likely to find product-market fit first.

This report groups the neobank landscape into three origin-based archetypes, analyzes the moats and unit economics of each, and draws lessons for how stablecoin-first neobanks may evolve:

- Banking-first: started with the depositor relationship. A better bank account as the wedge. Nubank, Revolut, N26, Chime.

- Commerce- and social-embedded superapps: started with a non-financial daily utility (commerce, mobility, messaging) and embedded finance into an existing user relationship. MercadoPago, Grab, Kakao, WeChat.

- Trading-first: started with the investor relationship rather than the depositor relationship and used it as a cross-sell surface into banking, payments, and credit. Robinhood, Coinbase, Binance.

The stablecoin-first model is structurally different from the first three, yet all four ultimately compete for the same customer relationship. The moats that made each archetype durable are the lens through which to understand the fourth: what ‘stablecoin neobanks’ need to replicate, and where they have a structural edge instead. One of the clearest early examples of this emerging category is KAST, which is examined later in the report as a case study in stablecoin-native financial infrastructure.

Banking-First Neobanks

Banking-first neobanks enter with core checking-like functionality, establish a primary relationship with cards and payment transfers, and layer higher take-rate products once deposit scale and underwriting data are established.

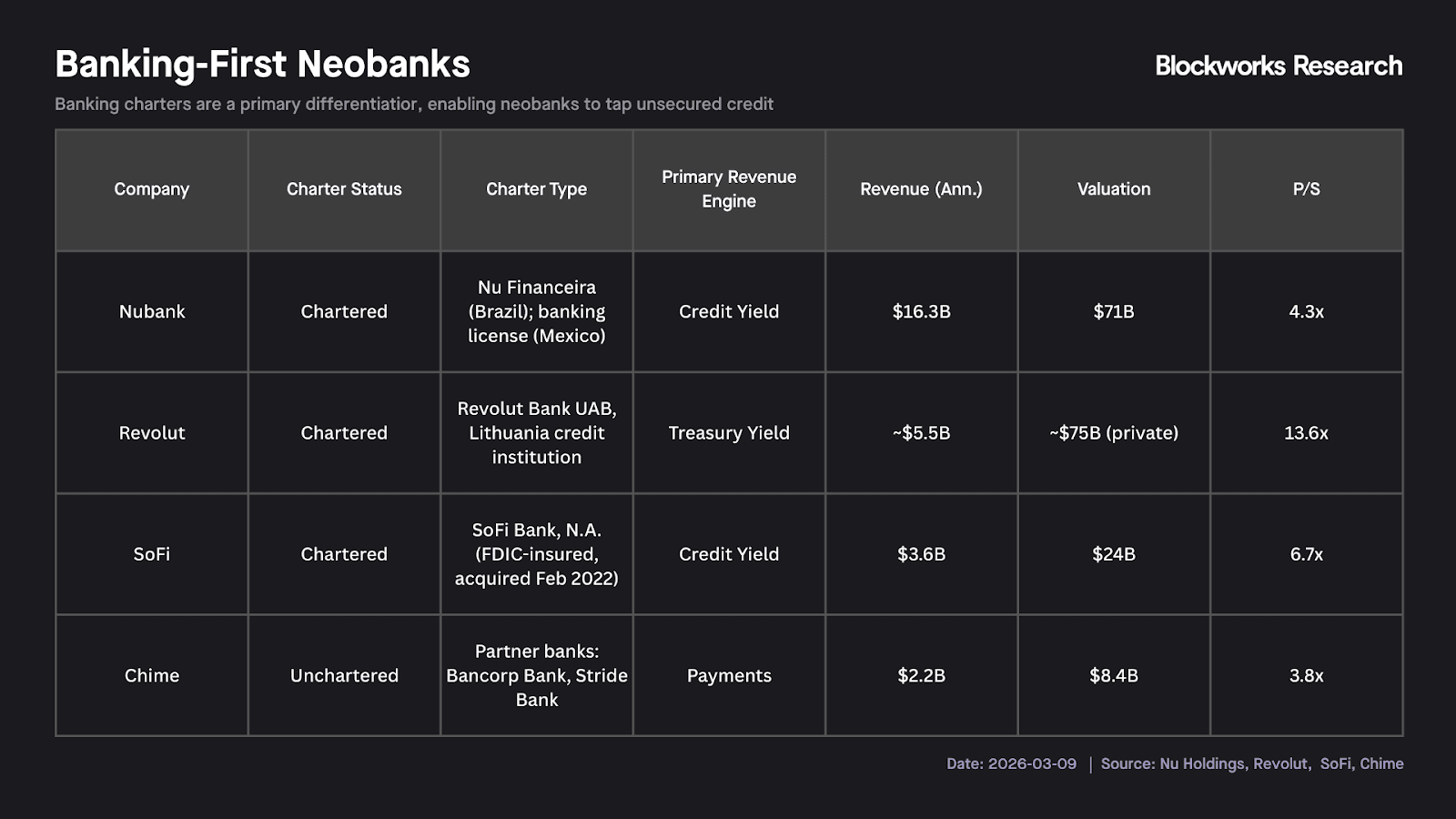

The archetype splits on regulatory structure: In the US and Europe, SoFi and Revolut, respectively, hold banking licenses and extend credit directly from their own balance sheets; Nubank operates through regulated entities in Brazil and Mexico with similar balance-sheet functions; Chime, which operates exclusively within the US, relies entirely on partner banks — it does not directly hold customer deposits, and without a charter, it cannot fund a lending book at deposit rates or extend credit directly from its own balance sheet.

Revenue within this cohort sequences across five streams: interchange, interest income, subscriptions, FX, and trading. The charter/unchartered divide determines how far along that sequence a platform can travel, and the mix each platform has reached reveals more about its maturity than any single headline number.

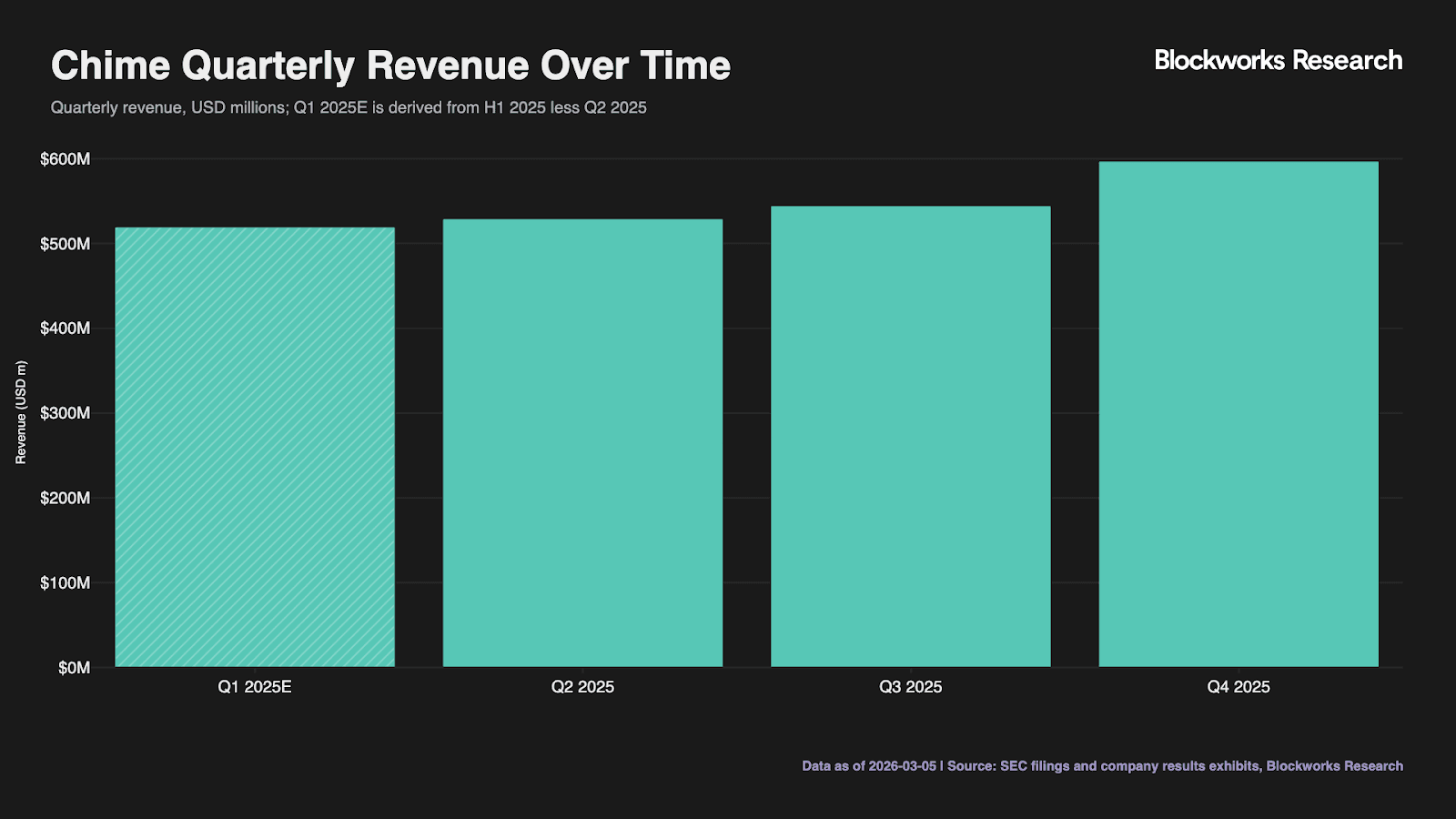

Chime illustrates the interchange-first stage: $2.2B in FY2025 revenue, 71% from payments take-rate, with platform-related revenue growing but not yet reshaping the mix. Without a charter, Chime cannot fund a lending book at deposit rates, so interest income remains a secondary engine.

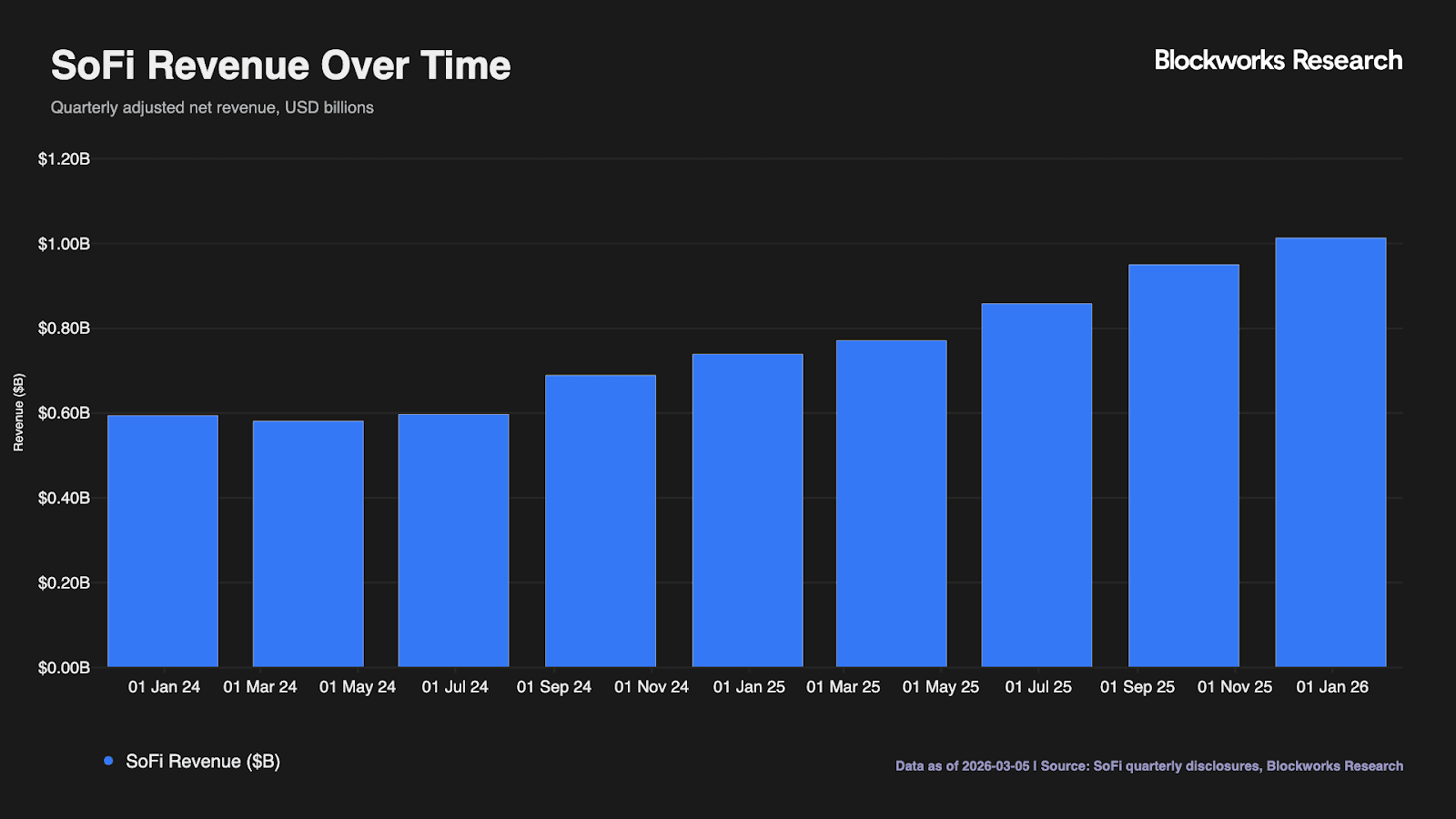

SoFi illustrates what the charter unlocks: deposits cost 181 bps less than warehouse facilities in Q4 2025, implying ~$680M in annualized interest expense savings, with net interest margin at 5.72% and lending segment net revenue at $486.5M.

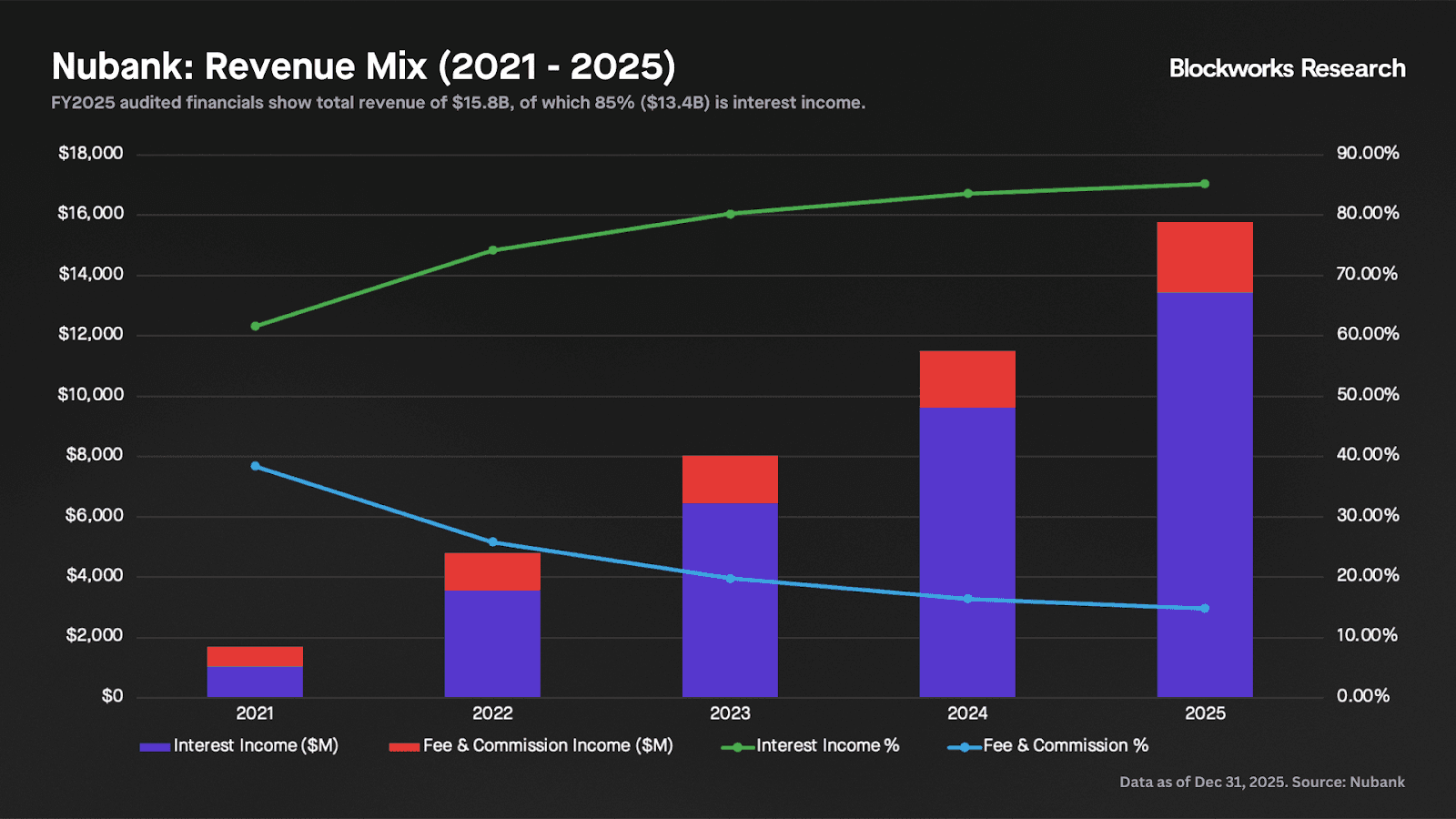

Nubank represents the credit yield engine at scale and the clearest proof that the lending book, not interchange, is what defines a mature neobank. FY2025 audited financials show total revenue of $15.8B, of which 85% ($13.4B) is interest income, with credit card interest contributing $4.6B and loan interest $4.8B. That 85% figure reflects a deliberate trajectory: in 2021, when Nubank was still primarily a card issuer, interest income was 62% of revenue. As the lending book scaled, that share grew to 74% in 2022, 80% in 2023, and 84% in 2024.

Fee income, predominantly interchange, grew nearly 4x in absolute terms over the same period but fell from 38% to 15% of the mix, not because fees shrank, but because credit yield compounded faster. The unit economics that underpin this are striking: monthly revenue per active customer reached $15 in Q4 2025 against a cost-to-serve of $0.80, a nearly 19x return that no traditional bank with physical branches can replicate.

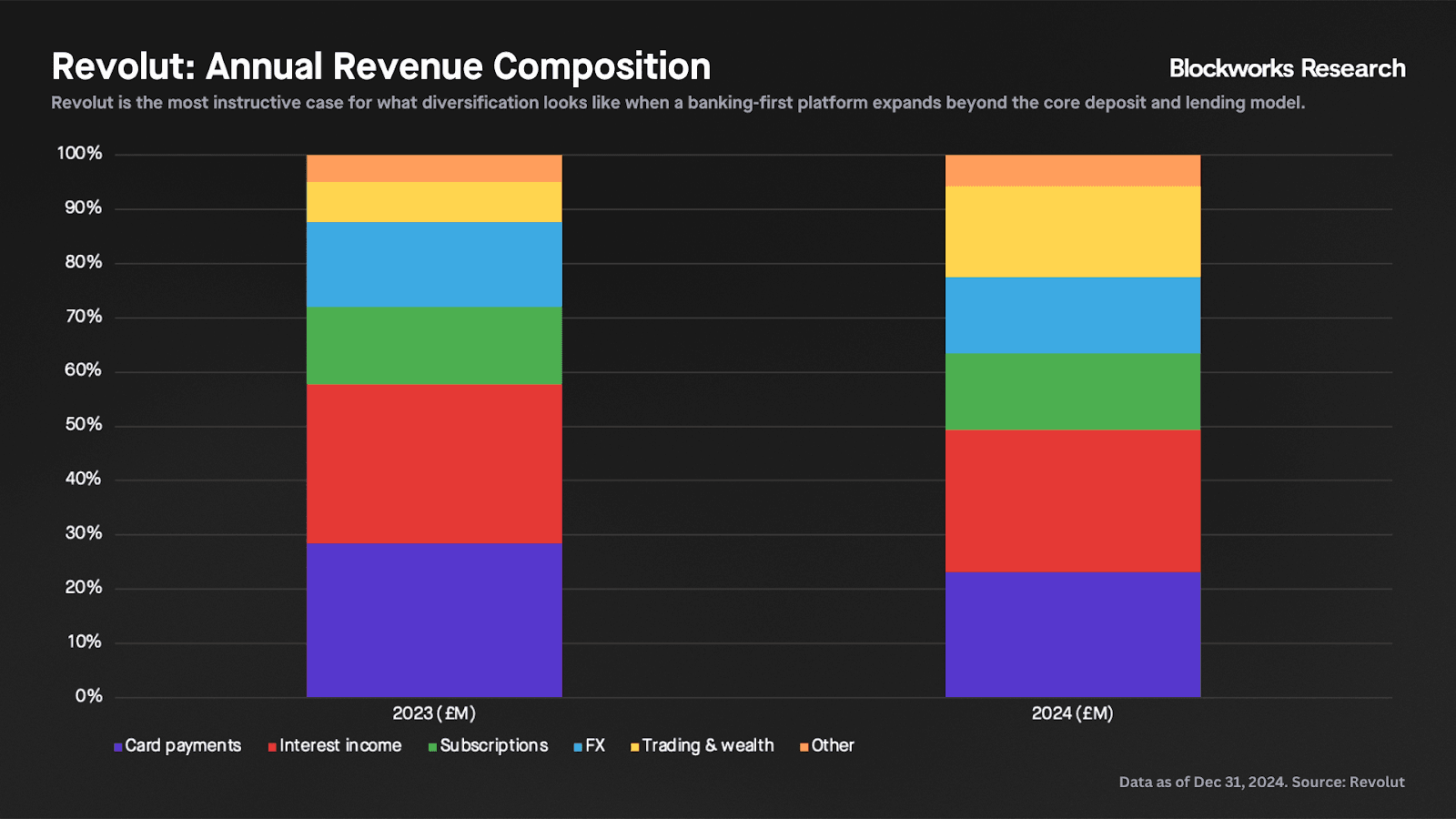

Finally, Revolut is the most instructive case for what diversification looks like when a banking-first platform expands beyond the core deposit and lending model. Its 2024 annual report shows £3.1B in total revenue across five streams: interchange at £694M, interest income at £790M, subscriptions at £423M, FX at £422M, and trading and wealth at £506M (the last driven primarily by crypto trading activity and up 298% YoY). No single line makes up more than 30% of total revenue.

That revenue mix looks less like a bank and more like a diversified financial platform, which is precisely the convergence thesis playing out from the inside. The contrast with Nubank is instructive: Nubank has gone deep on one engine (credit yield) while Revolut has gone wide across five.

Both are winning, but they represent different theories of what the primary financial relationship looks like at scale. The caveat on Revolut is that trading revenue is cyclical. The 298% wealth growth in 2024 was partly a bull market effect, so the diversification is real, but not all of it is durable across cycles.

Path Dependency: Charters, not Stablecoins

The central advantage of the chartered neobank model is not the savings rate or the card product. It is unsecured lending. The same regulatory stack that unlocks deposit-rate funding and direct credit extension also limits how aggressively a platform can make stablecoins central to the deposit relationship. The pattern is consistent across the cohort. Revolut, the most crypto-forward of the group, has not introduced yield on stablecoin balances; its February 2026 FCA sandbox trial for a proprietary stablecoin is payments infrastructure, not a savings product. Nubank's USDC rewards program frames stablecoins as an extension of existing card relationships.

SoFi is the most instructive case: as the only nationally chartered US neobank in this group, it had more regulatory latitude than most to put stablecoins at the center of the deposit relationship, but it didn't. SoFiUSD, launched in December 2025, is a settlement rail. Its March 2026 Mastercard partnership routes it through card clearing infrastructure, but none of that touches the savings or lending relationship. A chartered bank chose the payments lane deliberately, because the lending book is where the economics are. In all three cases, stablecoins are extending into the edges of the product while the charter-protected lending book remains the core business.

That containment is stable for now, but it rests on a specific market condition: onchain yields are currently uncompetitive. Aave v3 USDC has recently traded at 2-3%, below SoFi's 3.3% savings APY and Revolut Ultra's 4.25%. But onchain yields are compressed by the current market environment; during periods of elevated DeFi activity, Aave USDC has reached 8-10% and Ethena's funding-rate-driven yields have run well above that. In any case, routing FDIC-insured deposits into those venues is structurally incompatible with capital requirements.

The chartered neobank moat is durable as long as the primary financial relationship stays anchored to credit. A competitor unconstrained by charter overhead can offer structurally higher dollar yields and lower cross-border costs simultaneously. Argentina, where Nubank has no meaningful presence and primary demand is dollar-denominated savings rather than consumer credit, is the most acute expression of that exposure. In such markets, the charter is overhead, not moat.

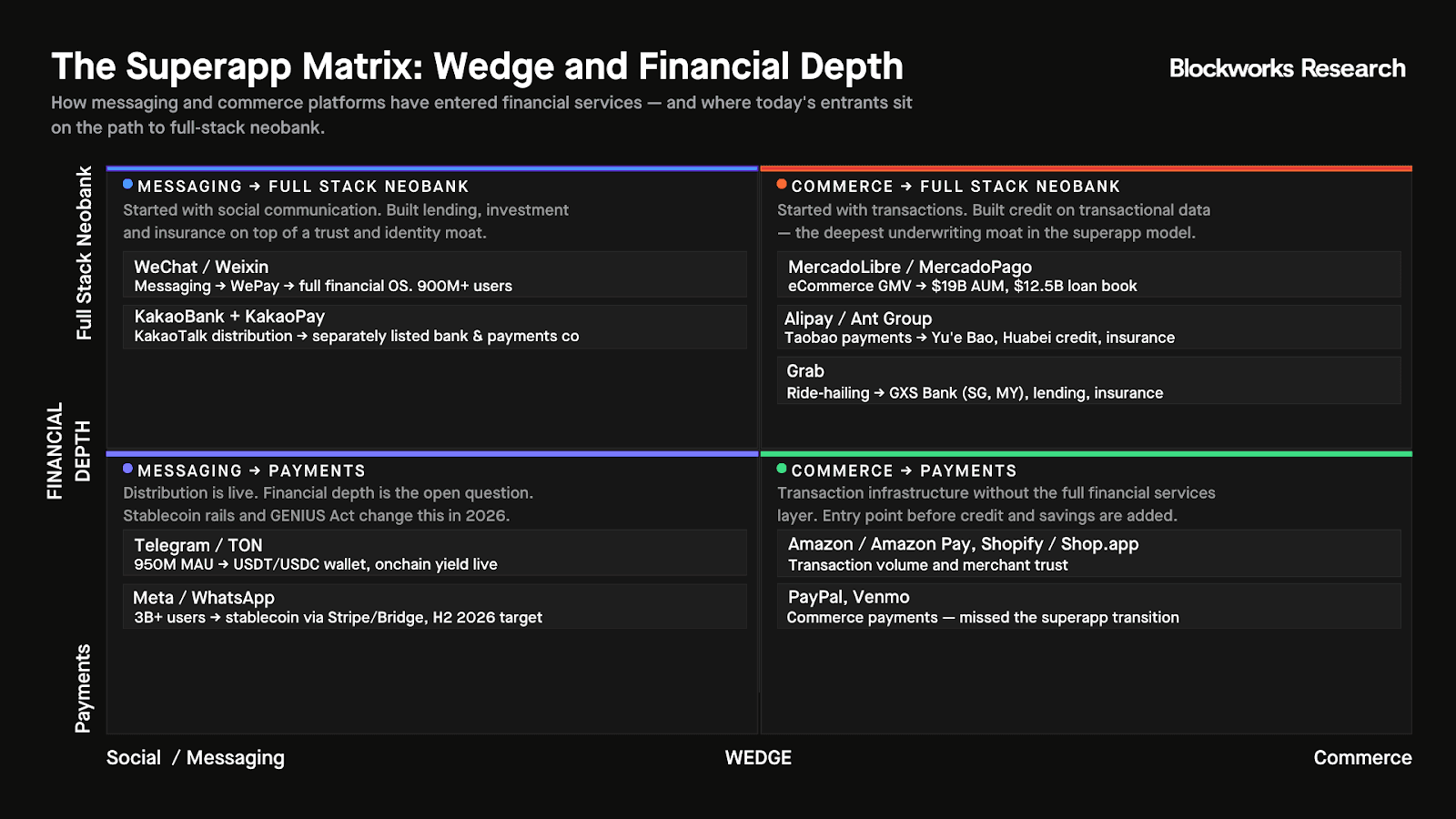

Superapps

The superapp archetype splits into two distinct models, with different moats, different data assets, and different paths to financial depth.

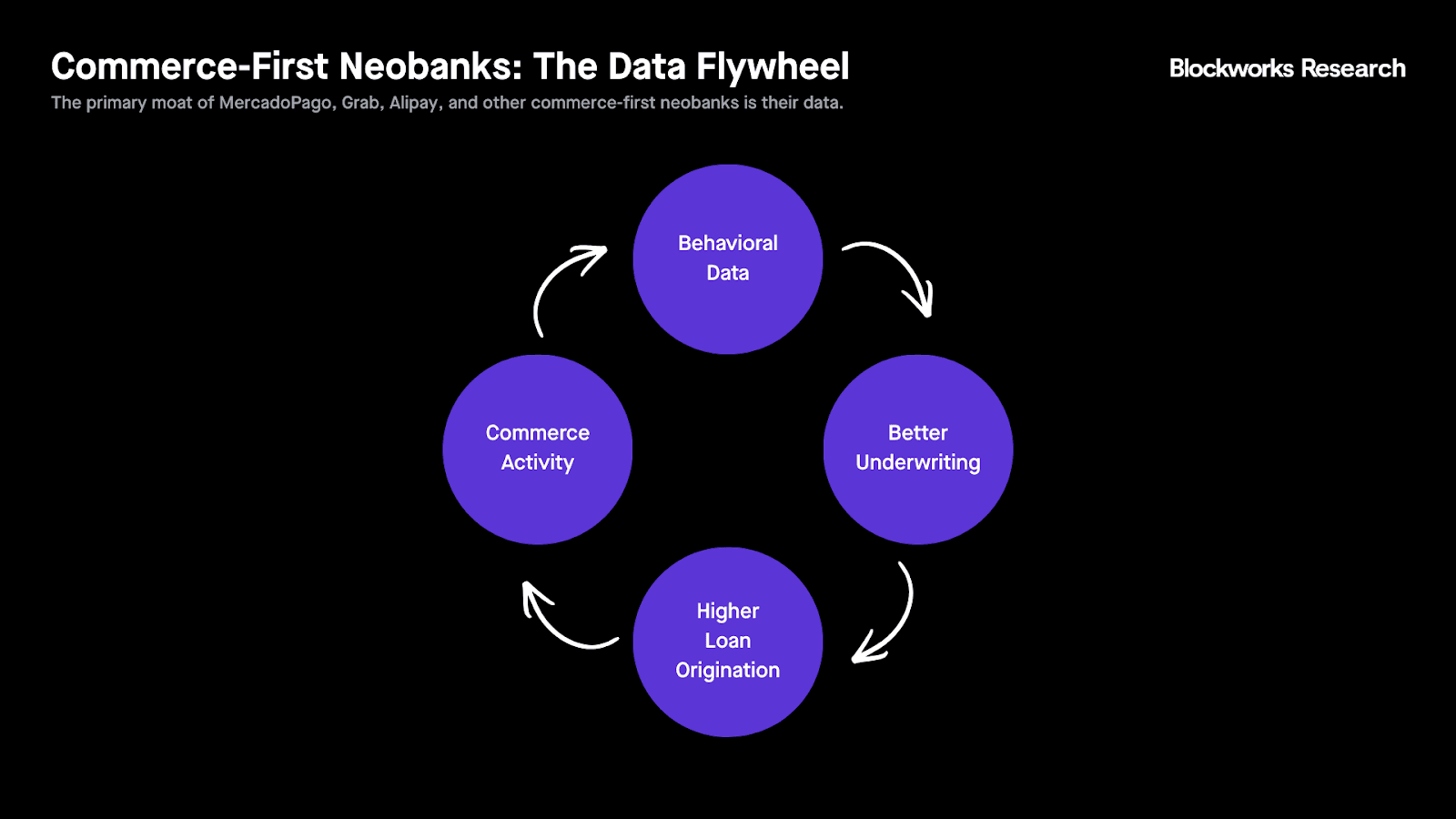

The first is commerce-embedded finance. These companies didn't set out to build a neobank. They set out to solve a different problem entirely: how do you get people to transact on a marketplace, book a ride, or order food when most of them don't have a bank account? The financial services came later, almost as a byproduct of solving that first problem, but the years of transactional data that accumulated became the moat.

The second is messaging-embedded finance. The moat isn't data but distribution. WhatsApp, WeChat and Telegram each have over a billion monthly active users, making customer acquisition cost effectively zero. The gap between that distribution advantage and actual financial depth is where the story gets complicated: WeChat crossed it; WhatsApp and Telegram haven't, partly by choice, partly because both have faced regulatory friction that WeChat never had to navigate at the same scale.

Commerce-Embedded Neobanks

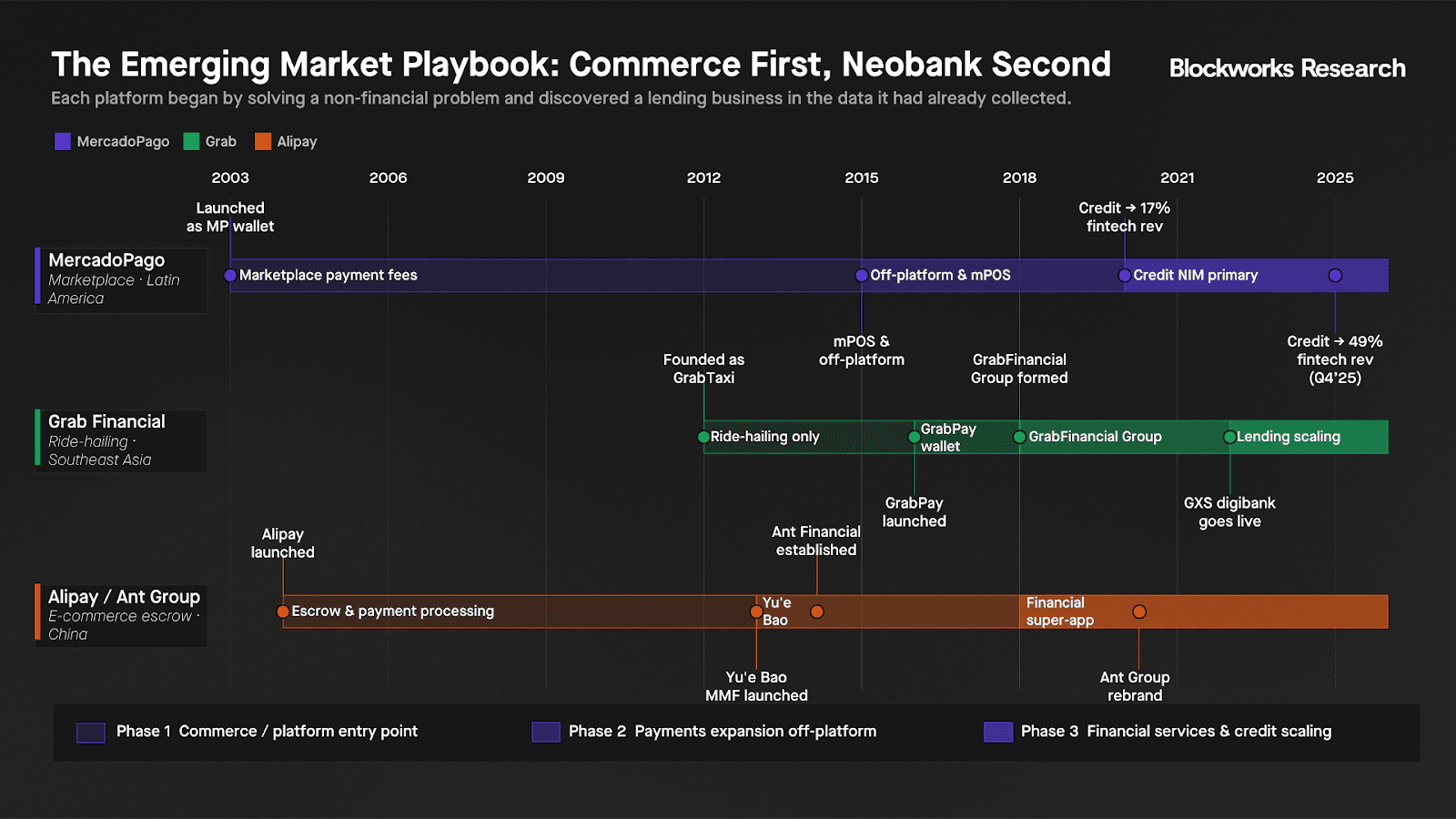

Mercado Pago launched in 2003 to solve a marketplace problem: hundreds of millions of potential buyers across Latin America who couldn't complete a transaction because they lacked a bank account or credit card. Mercado Pago offered a digital wallet that could be loaded with cash at physical locations, enabling the unbanked to participate in e-commerce for the first time.

The same logic applies to Grab and Alipay, with different entry points. Grab started as a ride-hailing app solving a safety and reliability problem in Southeast Asian cities. Alipay started as an escrow service solving a trust problem on Taobao, where buyers wouldn't pay sellers they'd never met. In each case, the financial infrastructure was built to serve the core product, not the other way around. The financial relationship followed the commerce relationship, and by the time these platforms started offering credit, savings, and investment products, they already had years of behavioral data that no bank or neobank could replicate.

The monetization arc: from processing fees to credit NIM

The revenue evolution of commerce-embedded finance follows a predictable arc, and Mercado Pago is the most instructive case study because it is the furthest along.

Phase 1: Marketplace payment fees. Mercado Pago's original revenue was a simple take-rate on transactions flowing through the MercadoLibre marketplace, generally around 8% per transaction. Revenue scaled with GMV. This phase lasted roughly from 2003 to 2015.

Phase 2: Off-platform payment processing. In 2015, Mercado Pago began offering mPOS devices to small and medium merchants outside the marketplace. The addressable market expanded dramatically — from MercadoLibre's own GMV to the entire informal and formal retail economy across Latin America. Payment processing fees remained the core revenue driver, but the business was no longer a captive feature of the marketplace.

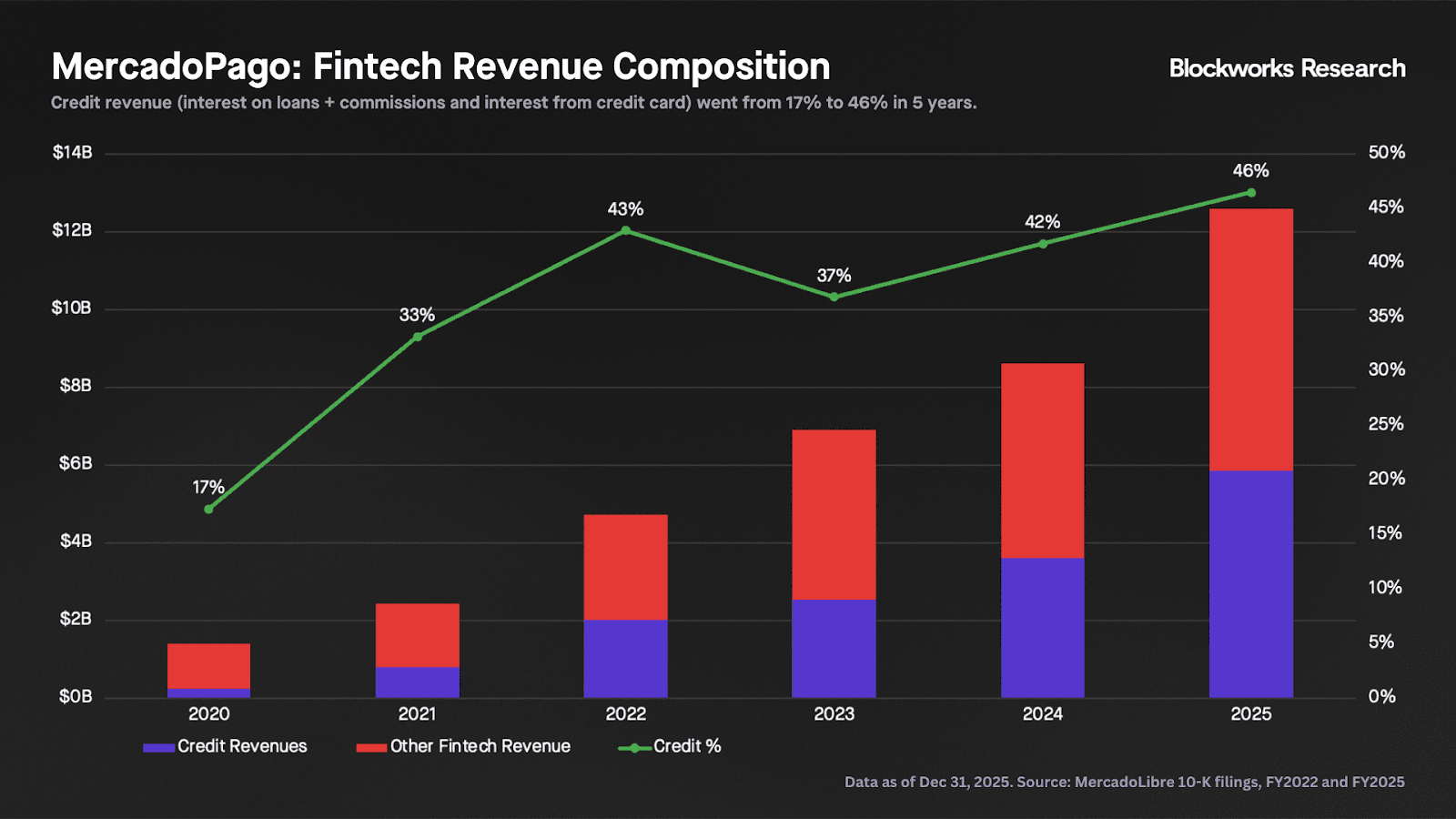

Phase 3: Credit as primary revenue. Credit revenues grew from $246 million in 2020 to $5.9 billion in 2025, a 24x increase in five years, and from 17% to 47% of Mercado Pago's total fintech revenue over that period. Net interest margin on loans to merchants and consumers is now the primary revenue driver, not payment processing fees. Mercado Pago has, in effect, become a lender that happened to start as a payments platform — mirroring Nubank's trajectory almost exactly, with the key difference being the entry point.

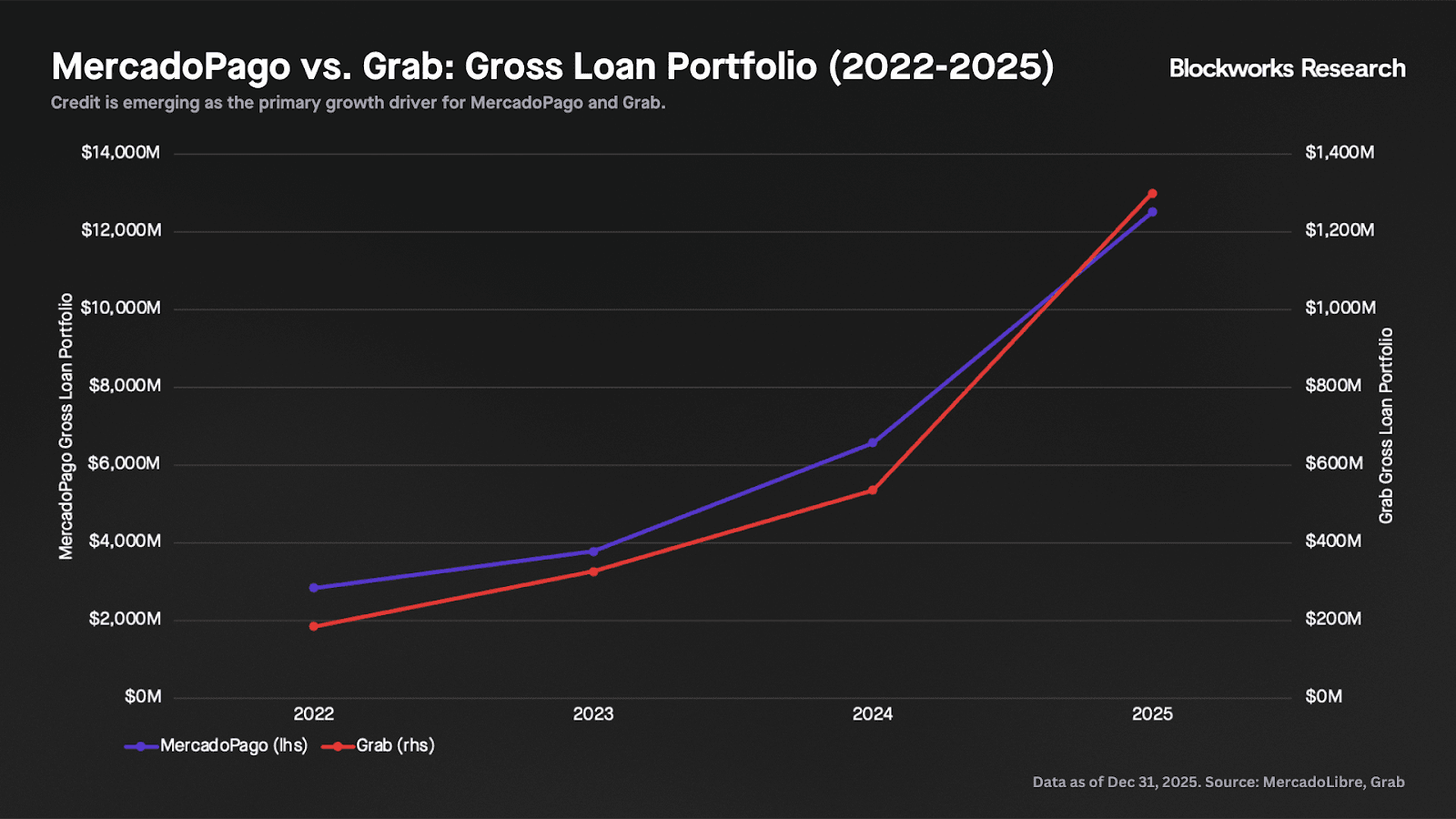

Grab is earlier in the same evolution, expanding from a commerce platform into a full-stack neobank. Financial services revenue was $348 million for full year 2025, growing 38% year-over-year, with lending as the primary growth driver. Grab's loan portfolio grew from $185 million in 2022 to $1.3 billion at the end of 2025; Mercado Pago's grew from $2.8 billion to $12.5 billion over the same period. The data moat is building, credit is starting to scale, and the trajectory is the same.

The data moat

The commerce-embedded moat is not the financial product. Any neobank can offer a credit card. The moat is the data that makes the underwriting better than anyone else's. MercadoLibre's credit-scoring model uses thousands of behavioral variables derived from marketplace activity: purchase history, selling behavior, payment patterns, logistics interactions, and even the categories of goods bought and sold. This is not credit bureau data or bank transaction data. It is a granular, lengthy record of how a person or business participates in the economy, captured years before any lending relationship began. The practical result is that Mercado Pago can extend credit to people and businesses that traditional banks and pure-play neobanks would decline or price punitively — not because it is taking more risk, but because it has better information.

The conditions that produced these platforms were specific to their geographies: high unbanked populations, high smartphone penetration, distrust of incumbent financial institutions, and regulatory environments more permissive of commerce companies owning financial services. The US and Europe lacked most of these conditions, which is why no equivalent emerged there and why the playbook is most relevant for crypto-native entrants targeting markets the existing system has left behind.

Where stablecoins fit

Both Mercado Pago and Grab have launched stablecoins, but early results suggest that launching one is easier than getting users to adopt it. Mercado Pago launched Meli Dólar (MUSD) in Brazil in August 2024, a USD-pegged stablecoin tradable within the app at no fee, since expanded to Chile and Mexico, with MUSD available as cashback for Meli+ subscribers. Despite a base of 78 million monthly active users, MUSD has a circulating market cap of $65 million, less than 0.4% of Mercado Pago's $19B in AUM. Its closed-loop design limits utility by intention, but also limits scale.

Grab's approach is more infrastructure-oriented. In November 2025, it signed an agreement with StraitsX to build a stablecoin-based settlement layer across its eight-market footprint, with a proof of concept already live: a three-way arrangement with StraitsX and Ant International lets tourists using Alipay+ apps pay at GrabPay merchants in Singapore with immediate SGD settlement via the XSGD stablecoin. Grab is using stablecoins for the most obvious use case: cost efficiency in cross-border settlement.

Similar to banking-first players, the gap neither player has explored is yield, which is an opening for crypto-native neobanks to compete directly on yield in markets where legacy fintech infrastructure cannot match it.

Messaging-Embedded Finance

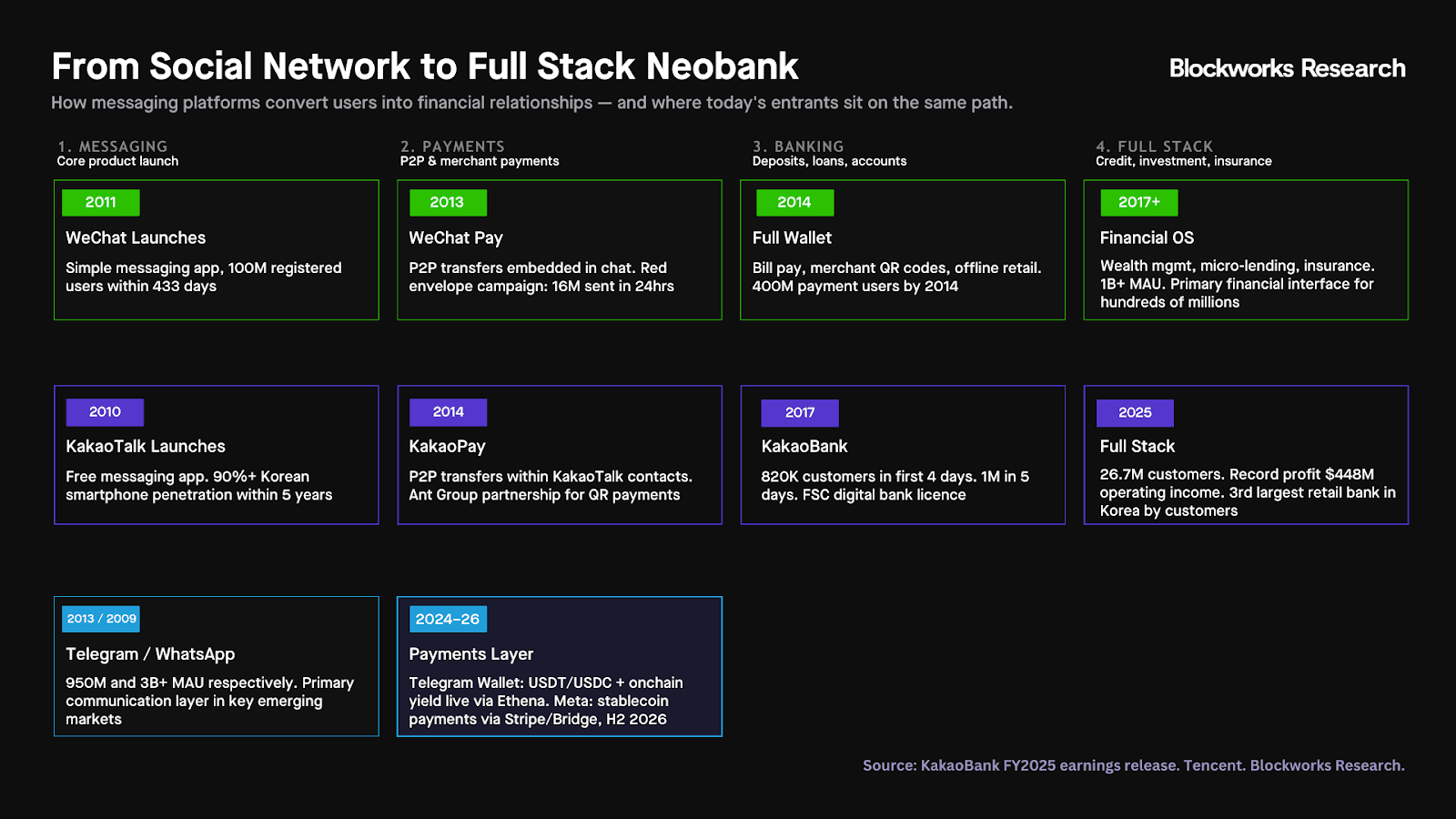

WeChat is the canonical model. By the time Tencent launched WeChat Pay in 2013, WeChat was already the primary communication layer for over 600 million Chinese users. Peer-to-peer transfers, the viral Hongbao red packet feature, and wealth management through Yu’e Bao all rode on top of an existing social graph, with near-zero marginal customer acquisition cost. Hongbao in particular helped normalize digital payments by embedding them in a familiar, culturally resonant behavior. Conversion happened fast because the trust relationship already existed.

Kakao ran the same playbook in Korea with more regulatory friction and still succeeded. KakaoBank launched in 2017, acquired 1 million customers in its first five days, and today has nearly 27 million customers as a separately listed entity and the third-largest retail bank in Korea by customer count. The sequencing in both cases was the same: messaging first, payments second, and full neobank stack third.

The next wave is already taking shape under more favorable structural conditions. Telegram has roughly 1 billion monthly active users and a live crypto wallet with a yield product via Ethena, though with very little traction. Meta is integrating stablecoin payments across its apps targeting H2 2026. Meta is making this move in a markedly different regulatory environment from the one that killed Libra in 2019 and wound down Diem in 2022. WhatsApp Pay is live in Brazil and India but has not achieved a dominant payments position in either market. Whether the current US regulatory environment is finally the catalyst for Meta to become a serious payments player (and from there, a full-stack neobank) is the open question the next two years will answer.

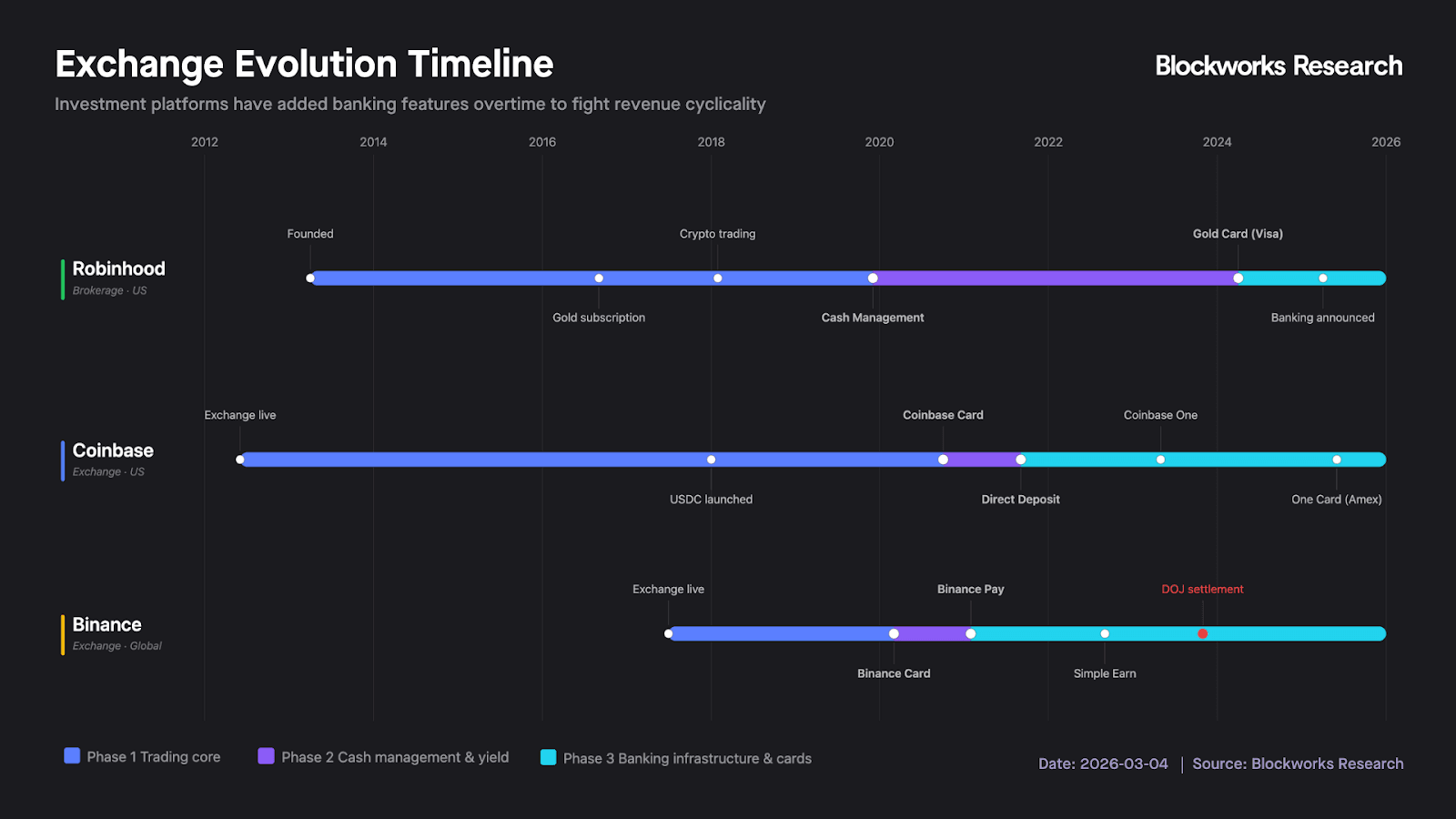

Trading-First Platforms

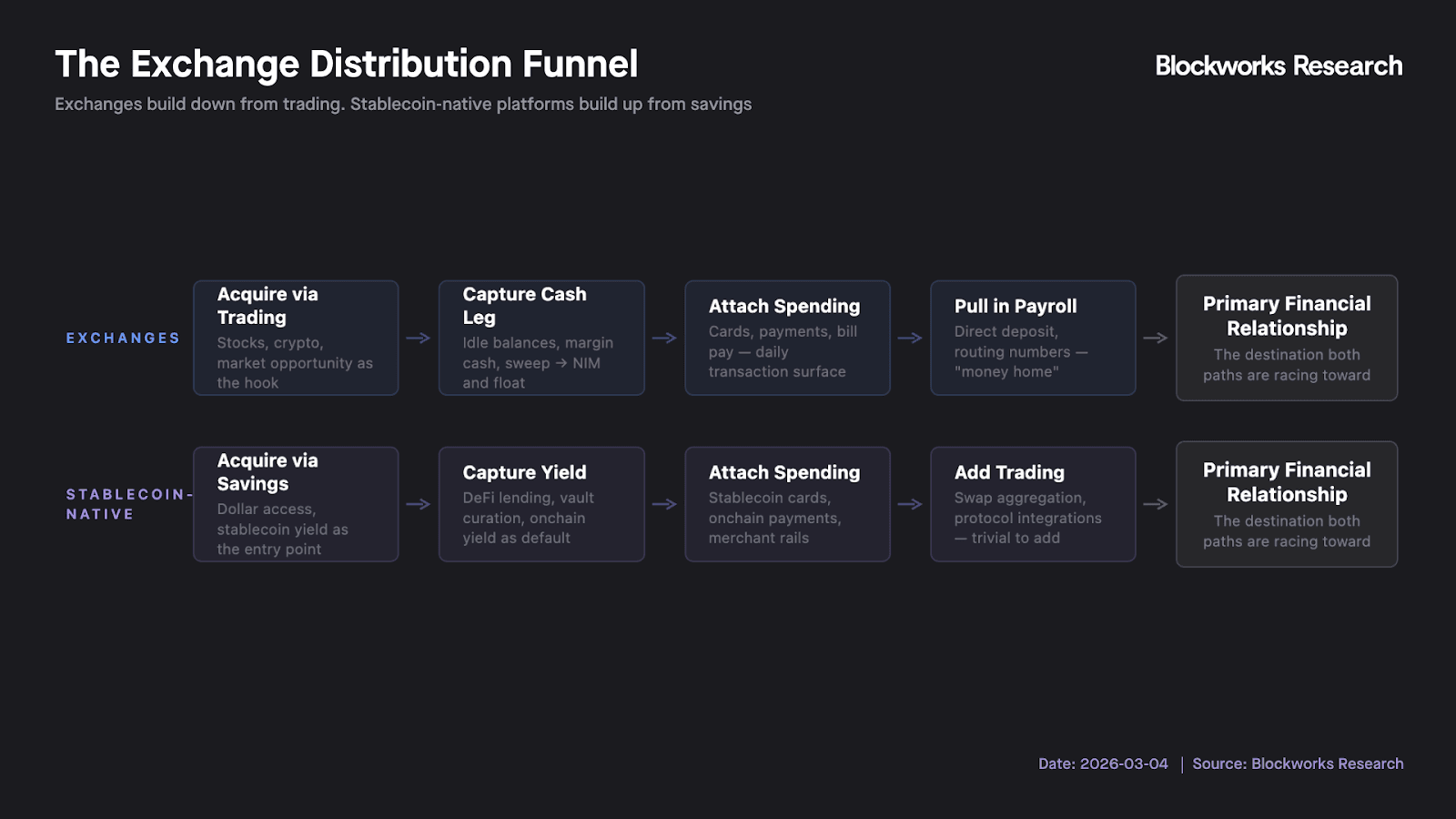

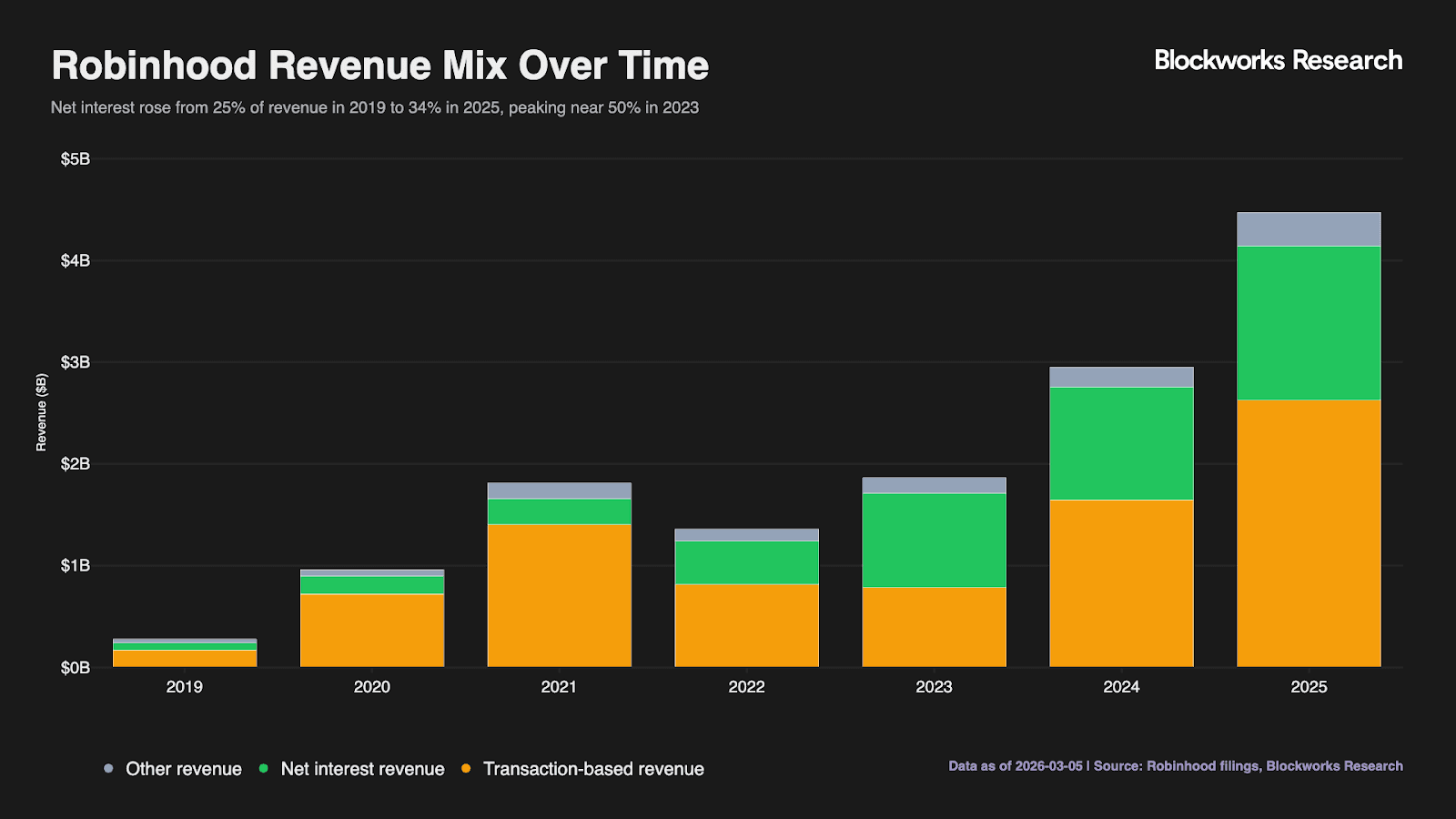

Trading-first platforms began with trading as the primary user value proposition and expanded into neobanking-adjacent products over time. Three revenue streams define the model. Transaction-based revenue is the original engine and the primary source of cyclicality. Net interest revenue monetizes idle cash and margin balances in a bank-like way, making the business sensitive to the rate regime but partially decoupling it from daily trading activity. Subscription revenue, the smallest lever today, monetizes features such as enhanced margin, analytics, and higher yields, and in a mature portfolio should be the least correlated with trading volumes of the three.

The cyclicality problem is structural. Coinbase's annual revenue fell from $7.84B in 2021 to $3.19B in 2022. The banking layer each platform is building is the explicit attempt to generate revenue that does not require a bull market. In this regard, the funnel that gets users there follows a consistent sequence: acquire via trading, capture the default cash leg, attach spending, pull in recurring inflows, and move up the take-rate stack into credit, lending, and subscriptions.

The question is not whether the funnel works but whether each platform controls enough of the underlying economics to make it durable. Two platforms have gone the furthest in answering that question, and they are doing it from opposite ends: Robinhood from the TradFi side, and Coinbase from the crypto-native side.

Robinhood: The Trading-First Superapp

Robinhood is the most complete expression of the trading-first to superapp thesis. It started as a zero-commission brokerage built to democratize stock trading and is becoming the primary financial relationship for a generation of retail investors. The brokerage is the on-ramp, and every product that follows cross-sells into an existing trusted relationship. The logic is the same as WeChat and Kakao, but arriving from the TradFi side rather than messaging or commerce.

The asset and deposit data make the case. Total platform assets grew nearly 70% year-over-year to $324B in 2025. Net deposits were a record $68B, representing 35% growth, with eight consecutive quarters above $10B. These numbers describe a primary banking relationship, not a trading app. Over 40% of total assets now sit across ETFs, advisory, retirement, and cash, the long-term sticky side of the balance sheet. Robinhood has been receiving positive net transfers from all major brokerage competitors for eight straight quarters.

The banking rollout is the proof of concept. Robinhood Banking launched to initial customers in late 2025, and the early results are striking: 25,000 funded customers have brought in over $400M in balances, and over 50% have enrolled in direct deposit. Direct deposit is the definition of primary banking relationship in consumer finance: it is where your paycheck lands, which determines where you spend, save, and borrow. Achieving a 50% attach rate this early in the product lifecycle, before broad rollout, suggests genuine product-market fit rather than promotional behavior.

The product breadth tells the superapp story. Robinhood now has 11 businesses above $100M in annualized revenue. Options at ~26% of total revenue is its largest single product line. Prediction markets reached a $300M+ run rate in their first full year, the fastest-growing business in the company's history. The Gold Card has scaled 5x in 2025 to 600,000 cardholders with $10B in annualized spend, targeting over 1 million cardholders by the end of 2026. Gold subscribers reached 4.2M, up 58% year-over-year. Full-year 2025 revenues were $4.5B, up 52%, representing more than 3x growth over three years.

Coming products, including Robinhood Social, private markets via Robinhood Ventures, the Robinhood Chain L2, and AI-powered advisory via Cortex, extend the cross-sell surface further. Each new product is not a standalone bet but an addition to a platform where the customer relationship already exists.

The market has already begun repricing the story: Robinhood's market cap (~$69B) currently exceeds Coinbase's (~$52B), a relationship that has persisted since mid-2025, reflecting investor recognition that a diversified, compounding platform commands a different multiple than a cyclical exchange, even as both have sold off from their 2025 peaks.

Coinbase: Owning the Stablecoin Layer

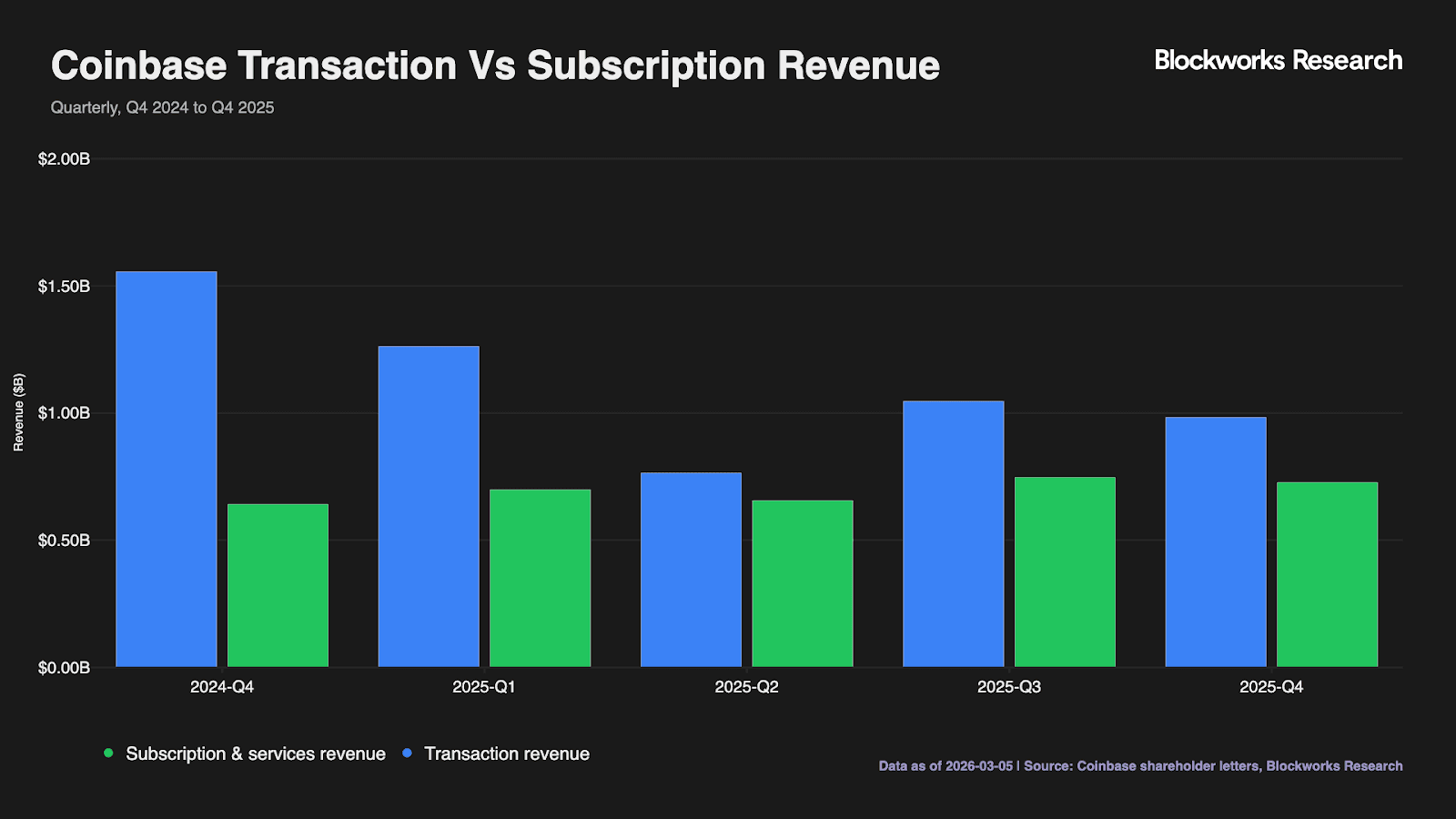

Coinbase is building toward the same destination from the opposite direction: crypto-native infrastructure outward. Its neobank layer is less visible than Robinhood's but more structurally embedded at the cash layer. In contrast to Robinhood, whose sweep economics run through partner banks, Coinbase receives 100% of reserve income on USDC held on its platform and 50% of Circle's residual revenue on off-platform USDC.

In 2025, stablecoin revenue totaled $1.35B, representing 19% of total Coinbase revenue. When transaction revenue fell 37% year-over-year in Q4'25, subscription and services revenue grew 13.5% to $727.4M. This divergence is evidence that the revenue mix is actively decoupling from crypto market conditions as USDC adoption scales.

The consumer banking surface sits on top of this: USDC rewards at 3.5% for Coinbase One subscribers, up to 4% bitcoin back on the Coinbase One Card, and direct deposit through the Base app that converts incoming USD to USDC 1:1 via Bridge. That last detail is architecturally significant: the default cash position is onchain, not swept to a partner bank, which means Coinbase owns the economics of idle cash rather than passing them to a third party.

The institutional layer is deepening in parallel. The Deribit acquisition, which closed in August 2025 for approximately $2.9B, brought the leading crypto options venue onto Coinbase's infrastructure, with $185B in monthly volume and $60B in open interest as of July 2025. Combined with ~$246B in assets under custody, over 80% share of US crypto ETF custody, and CaaS partnerships with PNC and JPMorgan, this divergence evidences Coinbase's efforts to diversify revenue streams and mitigate the cyclicality of crypto markets.

Finally, Base can become an increasingly meaningful revenue tailwind at the infrastructure layer as more value moves onchain.

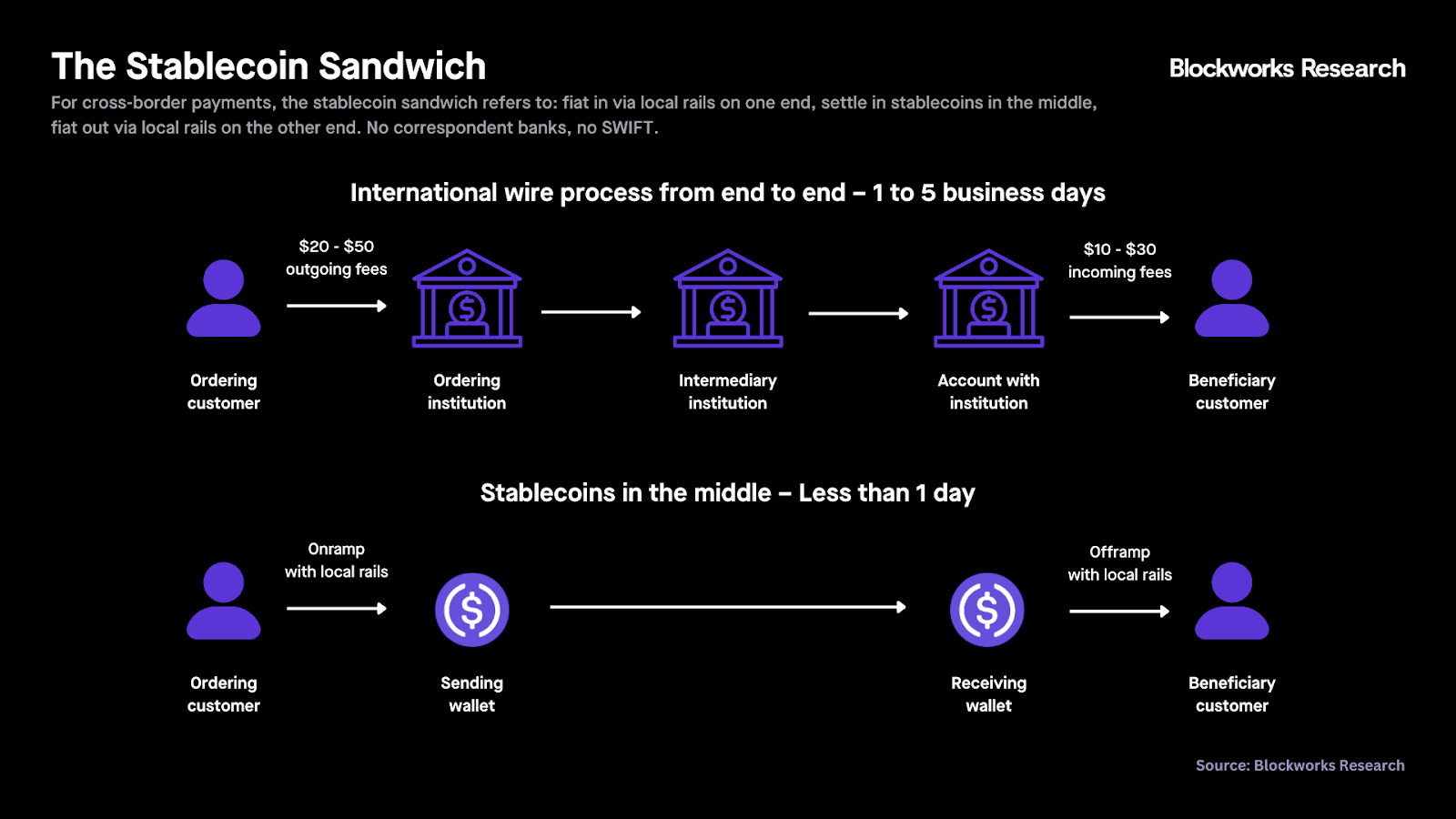

Binance, Bybit, Bitso: The Stablecoin Sandwich

Binance's version of the neobank build operates across a different regulatory context and geographic footprint entirely, and the mechanism that makes it work is structurally distinct from either Robinhood or Coinbase. In high-inflation emerging markets like Argentina and Turkey, the primary user need is not yield-seeking or trading convenience. It is dollar access. Binance pioneered informal dollar access through P2P trading at spot rates, effectively becoming a remittance and dollar-savings layer as a byproduct of being an excellent crypto venue.

The mechanism is what the fintech industry calls the stablecoin sandwich: onramp via local rails, use stablecoins as the middle leg, and offramp via local rails. The economics compress traditional remittance fees dramatically. Bitso processed $6.5B in US-Mexico remittances in 2024, representing over 10% market share of the $64.7B corridor.

On its part, Binance's 300M+ registered users and card infrastructure across Brazil, Colombia, Peru, and parts of the CIS region represent a distribution footprint US-regulated platforms cannot match. Although the model remains under sustained regulatory pressure following the 2023 DOJ settlement, it is still the most widely used crypto exchange globally. In Argentina, people exchange USDT to pesos daily in local “cuevas” using Binance. Bitso and ByBit represent the forward expression of the same playbook with less regulatory baggage.

The CLARITY Act

Stablecoin integration is the critical fork in the road for trading-first platforms, and the CLARITY Act is the legislative gatekeeper. The bill remains stalled in the Senate after Coinbase withdrew support in January 2026, objecting to provisions pushed by traditional banks that would restrict third-party platforms from offering yield on stablecoins. Banks argue such rewards risk pulling deposits out of the traditional system; Coinbase maintains they are essential to innovation and America's crypto leadership. Despite White House mediation and public backing from President Trump, the dispute over USDC yield continues to block passage as of March 2026.

The stakes are clear. Controlling stablecoin reserve economics is the difference between owning the default cash layer and renting it. Coinbase has demonstrated the model works: $1.35B in stablecoin revenue in 2025, compounding independently of trading volumes. A legislative outcome that restricts yield on third-party platforms would directly undermine that engine and push the model back toward partner-dependent sweep economics. There is a further timing risk: the Coinbase-Circle revenue sharing agreement is due for renewal in August 2026, and the CLARITY Act's resolution, or lack of it, will set the legislative backdrop against which those renegotiation terms are struck. The offshore model is indifferent to either, which means offshore exchanges like Binance and Bybit may continue to find a wedge through dollar access and yield offerings on top of their core trading functionalities.

Stablecoin Neobanks

Stablecoins: The Go-to-Market Advantage

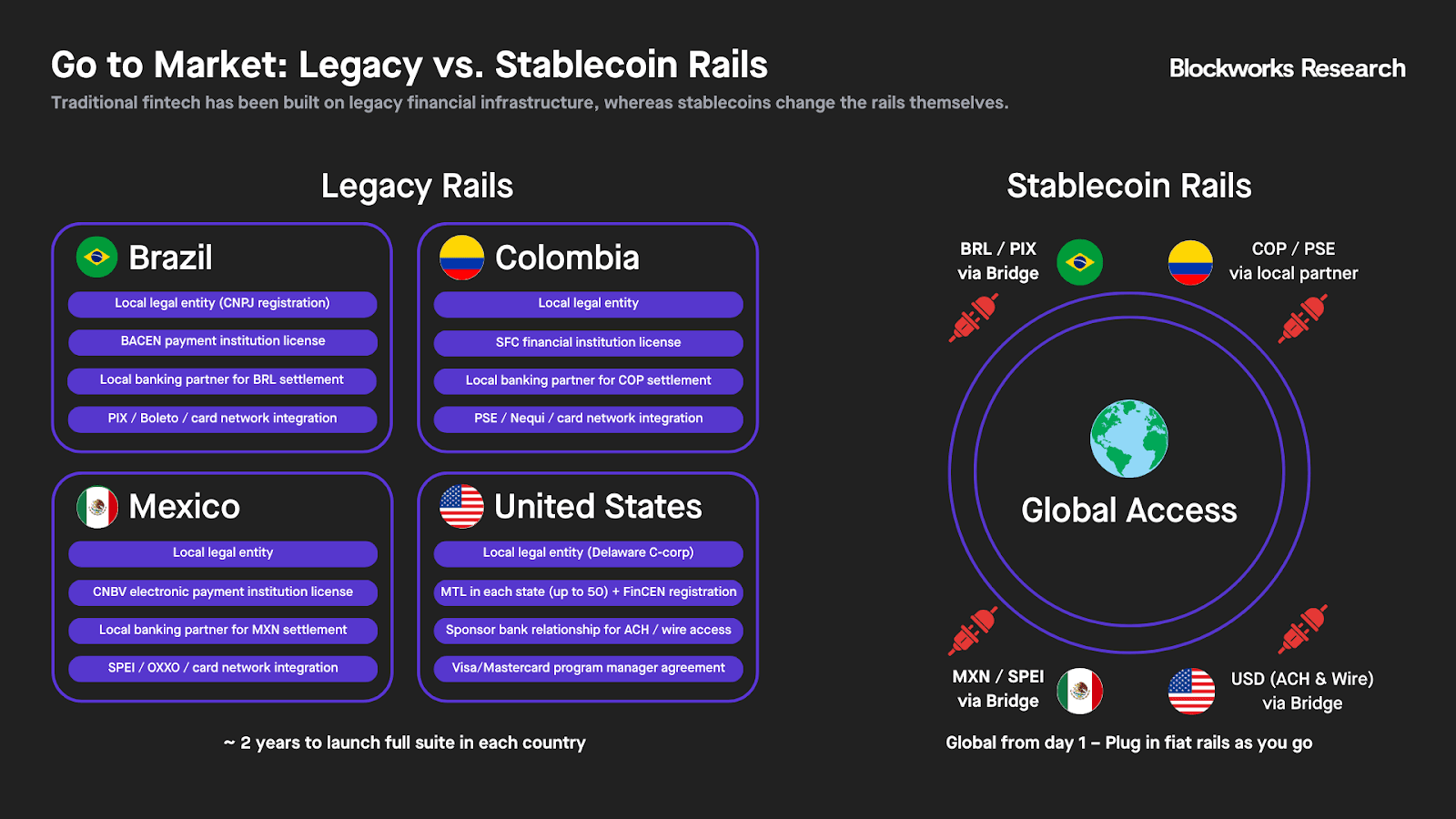

The stablecoin-first model is structurally different from every other archetype in this report. The defining advantage is building on blockchain rails as opposed to wrapping legacy financial rails in better software. Stepan Simkin, co-founder of Squads, puts it plainly: decoupling the account from the bank is what allows you to go global from day one. In practice, this is reflected in the ability to reach internationally distributed users earlier in a platform’s lifecycle, rather than implying uniform market access across jurisdictions. Even though established fintech players like Robinhood, Nubank, and Mercado Pago have the distribution advantage, they are still constrained by legacy rails as the foundation.

That constraint is becoming impossible to ignore. Stripe's 2025 annual letter named KAST alongside Sling Money, DolarApp, and Félix as part of a new cohort building "global financial apps right out of the gate," attributing the shift directly to stablecoins: "The progress is in large part due to stablecoins, whose borderlessness allows fintechs to set up infrastructure that works everywhere."

By contrast, building on legacy rails means that every jurisdiction is like building a new startup. Osvaldo Giménez, CEO of Mercado Pago, explained the constraint: "The way we realize it works is basically pick one of these countries and launch the full suite of products there. And that typically takes a couple of years." By contrast, a stablecoin-first neobank plugs in fiat connectivity via Bridge, Rain, or similar providers where needed, rather than making it the foundation.

Although stablecoin rails enable businesses to reach users across geographies earlier in their lifecycle, most user flows still touch fiat at some point. This is the key bottleneck today: a user receiving a salary, paying rent, or buying groceries still needs to transact in local currency. Adding a vendor like Bridge to solve on- and off-ramps across jurisdictions is exponentially more time- and cost-efficient than launching a new legal entity in each country. A lot of the value continues to accrue at the edges today: on-ramps, off-ramps, and FX conversion. That friction will not disappear entirely, but as more merchants, employers, and platforms move onto stablecoin rails, the surface area where fiat conversion is necessary shrinks.

A downstream implication of broader stablecoin adoption is that payments themselves become a loss leader over the long term. Charging 3% interchange on a transaction that settles instantly on a public blockchain for fractions of a cent is not a sustainable business model. Credit cards will continue to command pricing power through credit, compliance, and guaranteed fraud protection with chargeback rights, but stablecoins will compress margins at the payments layer.

The Landscape

The stablecoin-first neobank landscape is still early enough that most players are serving the same customer: someone already in crypto who wants a better interface for managing and spending onchain assets. That is a real market, but a constrained one. The more interesting question — and the one that determines which players reach meaningful scale — is whether stablecoin-first players can find their wedge outside the existing crypto user base, and in which geographies that wedge is sharpest.

The answer points clearly toward emerging markets. In the US and Europe, the value proposition is blunted by two structural realities: depositors already have dollar exposure (or easy means to do so), and there is no FDIC-equivalent insurance on self-custodied funds, making the risk-adjusted case for switching harder to make to a mainstream user. The wedge flips entirely in regions like Latin America, Southeast Asia, and Africa, where the primary demand is dollar access and dollar yield on top of a better user experience. Offering a user in Argentina or Nigeria a yield-bearing dollar account they actually control, without a local bank intermediary, is a genuinely useful product. The bottleneck remains on- and off-ramps, but that surface area is shrinking.

What connects all players in this landscape is the same sequencing logic: build a trusted relationship around one product, then cross-sell into it. What separates them is how far along that sequence each has traveled and whether the wedge they have chosen can reach beyond the existing crypto user base. One of the clearest case studies of this model is KAST.

KAST: Banking Onchain

KAST is the most funded and fastest-growing stablecoin neobank in this cohort and the clearest attempt to build a fully stablecoin-native financial platform for an internationally distributed user base. Founded in July 2024 by Raagulan Pathy, a former Circle executive in APAC, KAST raised an $80M Series A co-led by QED Investors and Left Lane Capital in March 2026, valuing the company at $600M less than 18 months after launch. The round included participation from Peak XV Partners, HSG, and DST Global Partners.

Unlike many earlier entrants that focused on a single use case, such as remittances or wallets, KAST is building a full-stack financial platform, aiming to establish a primary financial relationship rather than a point solution.

Raagulan Pathy, KAST’s Founder & CEO, frames the company’s thesis around a broader shift in how financial services are distributed: “Now the system is starting to move to the user. The internet is creating a global, digitally native population that isn’t tied to any one place but still needs access to stable, reliable financial infrastructure.” In practice, stablecoin rails make it possible to deliver dollar-based financial functionality to a globally distributed user base from the outset, rather than requiring users to access financial services through the local banking stack of a single jurisdiction. That matters most for users whose economic lives are increasingly cross-border, but whose access to stable savings, payments, and yield products remains constrained by local banking systems. In Pathy’s words, KAST is “combining traditional financial infrastructure with stablecoins and emerging technologies like AI to serve a global user base that is growing rapidly.” Pathy argues that this globally distributed, digitally native user base could eventually scale into the billions and reshape how a meaningful share of the world accesses financial services.

In terms of traction, KAST now serves over one million users across 170+ countries, processes close to $5B in annualized transaction volume, and is growing users and revenue at 15-20% month-over-month. Revenue has more than doubled since September 2025, and the company is targeting a $100M annual revenue run rate in 2026. If achieved, that would put KAST materially ahead of the scaling timelines seen in earlier fintech leaders such as Revolut, Wise, and Nubank, each of which took roughly five years to reach a comparable revenue scale. Its trajectory also appears at least comparable to, and potentially faster than, more recent high-growth fintech benchmarks such as Ramp. The team has scaled to 300+ employees, drawing from Stripe, Revolut, Airwallex and Circle, among others, bringing deep fintech and payments expertise to a stablecoin-native platform. What makes KAST notable is not just product breadth, but the speed with which a stablecoin-native platform has assembled core financial functions for a geographically distributed user base.

The product stack covers the four functional layers a neobank needs:

- Store: USD-denominated account functionality with ACH and wire capabilities. Of note, KAST offers institutional-grade security through Fireblocks and BitGo custody.

- Earn: Variable yield on stablecoins via risk-adjusted vaults managed by Gauntlet.

- Transfer and off-ramp: Global payouts to 190+ countries; instant and no hidden transfer fees.

- Spend: Visa cards accepted at 150M+ merchants globally, with up to 6% flat cashback.

The Gauntlet vault integration is architecturally notable: rather than offering a static yield product, KAST routes idle stablecoin balances through institutional-grade DeFi vaults with risk-adjusted parameters, giving users access to yield infrastructure typically reserved for sophisticated DeFi participants.

What differentiates KAST's positioning from others in this cohort is its explicit targeting of the cross-border earner: freelancers, remote workers, and founders in markets where the dollar is the preferred unit of account but dollar access is structurally limited. The product is built around that use case: USD-denominated account functionality, multi-currency conversion at checkout across 18+ currencies, and a card infrastructure that works across both crypto and fiat without requiring the user to manage the conversion manually.

Regarding upcoming catalysts, KAST Business is launching in 2026. Businesses already use KAST for payouts, payroll, and cross-border spending. KAST Business will bring these workflows into one dedicated experience designed for global operations. The offering will include global business accounts supporting 15+ currencies, instant payouts in 200+ countries, and customizable team cards, expected in Q3 2026.

KAST is not alone. Several other stablecoin-first neobanks are pursuing the same thesis at earlier stages in their development.

- UR, built on Mantle Network and backed by Bybit's distribution infrastructure, offers virtual Swiss IBAN accounts and a Mastercard debit card; the Bybit alignment provides potential access to its 70 million users, and the product targets Asian non-dollarized markets where dollar access and yield are the primary wedge.

- Plasma One, the consumer product of the Plasma blockchain, runs on a purpose-built stablecoin chain with a Tether relationship and zero-fee USDT transfers; adoption in emerging markets will depend on local distribution.

- Fuse, Squads' consumer app, was built explicitly to test whether a product could feel like a traditional finance app while delivering yield and payments on stablecoin rails. The learnings from building Fuse fed directly into Altitude, Squads' business banking product, which is where the company's consumer ambitions now live.

- Avici converted tokenholders after its MetaDAO ICO into early users to sidestep the cold-start problem; its differentiation bets are privacy architecture and an AI agent for personalized finance, with privacy potentially unlocking enterprise and institutional use cases.

- EtherFi is the clearest example of a DeFi protocol making a credible pivot into stablecoin-first neobanking. With ether.fi Cash, it is building a broad consumer finance stack that lets users save, borrow, and spend against onchain assets without first liquidating them. Its differentiation is the vault-based infrastructure, where collateral remains onchain and can continue working until settlement, making the product feel less like a crypto card and more like a crypto-native primary financial account.

If the defining outcome of this category is the platform that captures the primary financial relationship, it is likely to be the player that combines product breadth, global user distribution, and early scale - rather than one optimized around a single use case.

Trading-First: Jupiter and Phantom

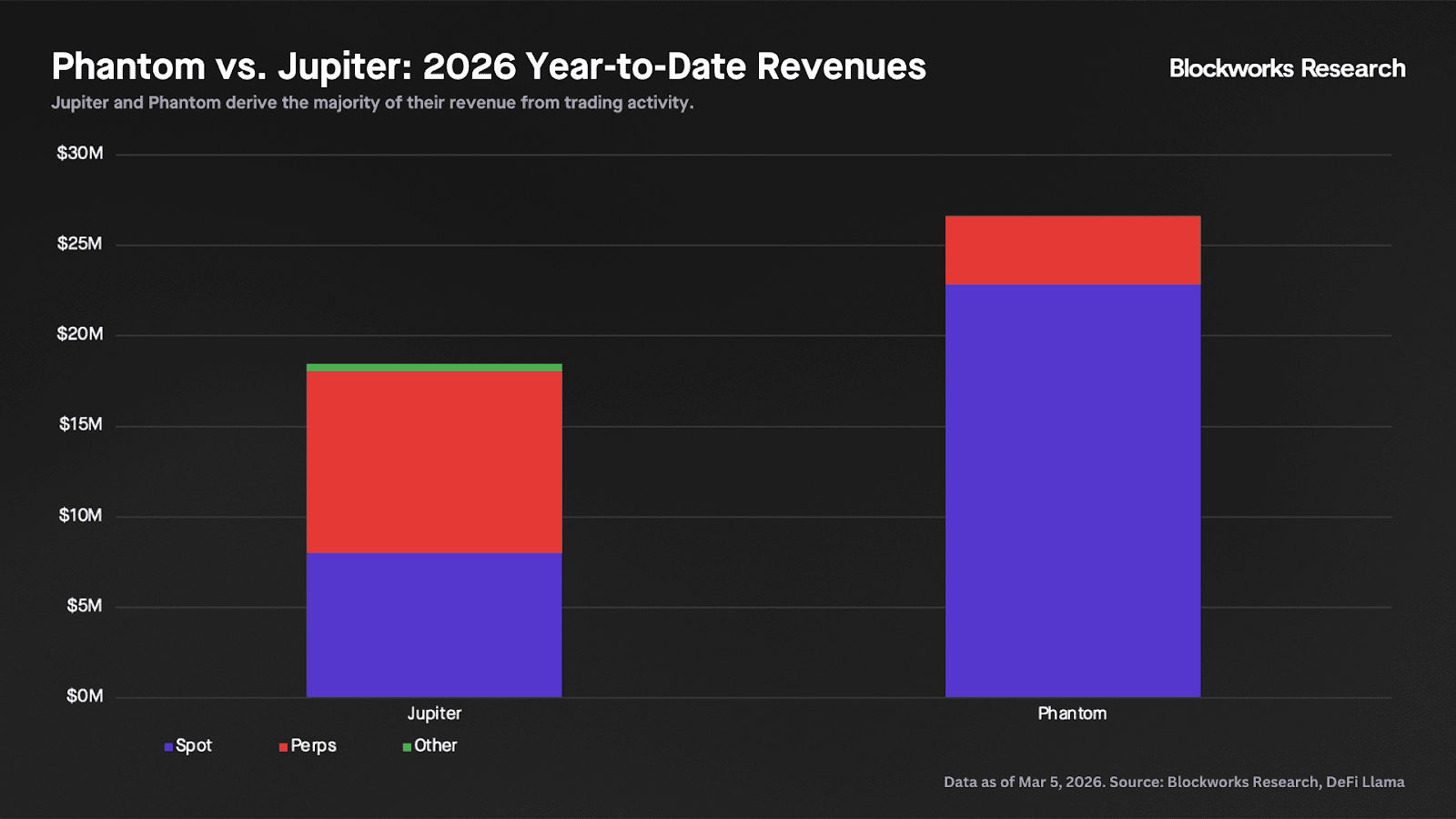

Jupiter and Phantom are best understood as trading-first platforms expanding into neobank territory rather than neobanks that happen to offer trading. Jupiter derives the majority of its revenue from its perps product and DEX aggregator, running at an annualized revenue run rate of $91M on a 30-day trailing basis, with perps accounting for roughly 54% of 2026 year-to-date revenue. Phantom monetizes primarily through in-wallet swap fees on Solana and Hyperliquid builder codes for perps, with spot swaps still accounting for over 80% of revenue and a $119M annualized run rate on the same basis. Both figures exclude revenue from jupUSD and CASH respectively, though neither is likely material at this stage.

What makes both businesses so strong is owning the end user, with both showing meaningful monetization through frontend fees. Jupiter is the go-to venue for trading on Solana, while Phantom had 15 million monthly active users as of February last year — arguably the strongest distribution in consumer crypto.

Both protocols are reinvesting revenues to expand their product suite. Jupiter has shipped JupLend, prediction markets, an ICO platform, a mobile wallet, a debit card, and off-ramp integrations. Phantom has launched CASH (a Bridge-powered stablecoin), added prediction markets via Kalshi integration, a trading terminal, and a card (also powered by Bridge). Both are running the same playbook: use profitable trading revenue to fund neobank expansion, then cross-sell into a user base that is already active and already trusts the interface. The Robinhood parallel is apt: a trading-first business that becomes the default financial app for a generation of users, with each new product cheaper to distribute than the last because the relationship already exists.

The risk in the model is visible in Phantom's swap volume data. Its share of the global embedded swap market fell from roughly 10% at the start of 2025 to under 1% by year-end, eroded by exchange-affiliated wallets offering lower fees and tighter incentives. That compression is undoubtedly why the neobank pivot matters: a platform whose revenue depends entirely on swap fees is exposed to commoditization, while one that has captured the primary financial relationship is not. Phantom and Jupiter are in a race to build that relationship before swap margins compress further.

Of note, Phantom is the most advanced expression of the wallet-to-neobank transition, but it is not alone in running the playbook. MetaMask, Rabby, and Rainbow are following the same path. In our view, Phantom remains the most compelling candidate in this cohort: the product velocity, the 15M monthly active user base, and best-in-class UX put it ahead of peers.

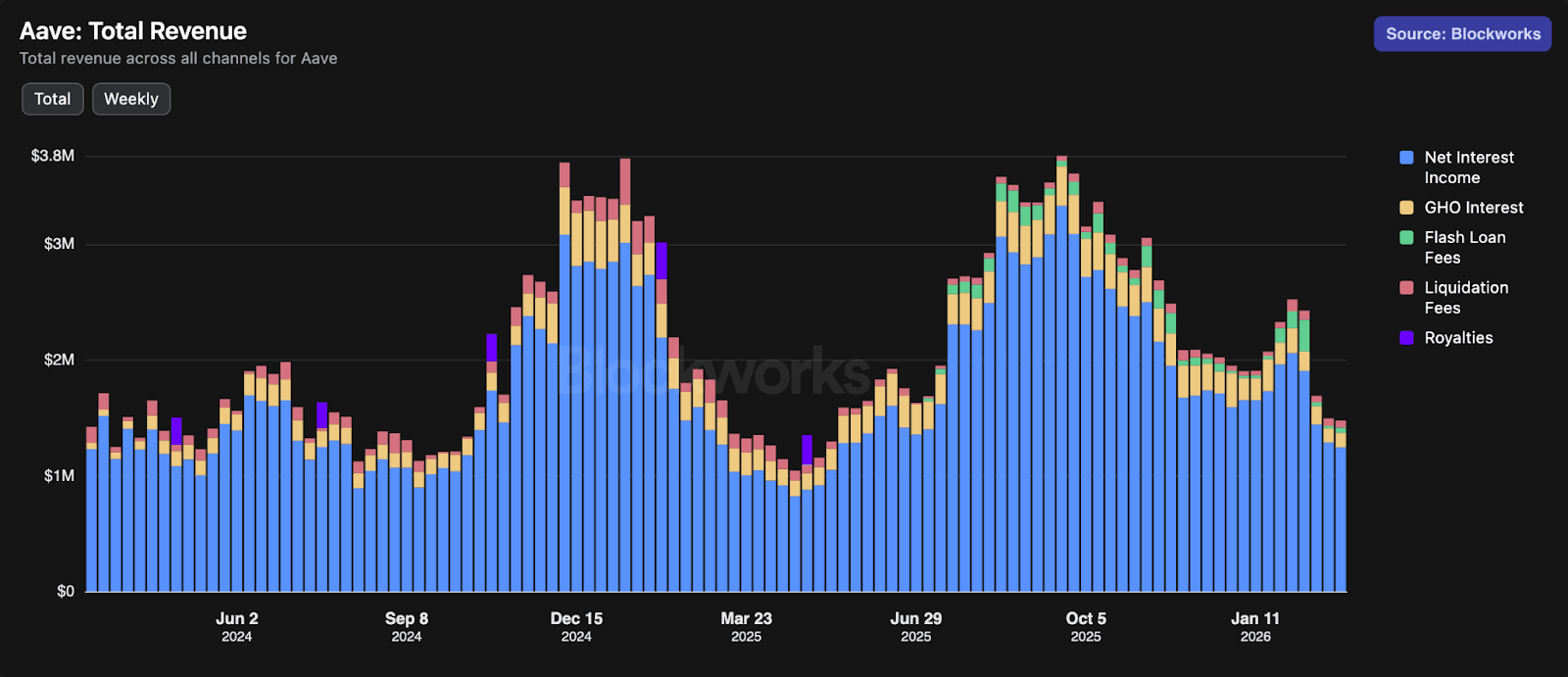

Aave's Push Toward Consumer Finance

Aave is the dominant player in onchain lending, and the upcoming Aave App marks its most deliberate move toward a consumer financial interface. About 85% of Aave's revenue comes from net interest margin on overcollateralized loans, with the remainder split across liquidation fees, flash loan fees, and GHO. The core value proposition of the Aave App is dollar exposure and dollar yield, and the natural target user is in emerging markets where accessing either is structurally difficult. Aave can offer rates that dwarf anything a local bank provides in pesos, rupiah, or naira, without requiring a US bank account or a local financial intermediary.

One detail worth watching is the introduction of insurance-backed account protection up to $1M per account. Self-custody's biggest adoption barrier outside the existing crypto user base has been the perceived risk of holding funds without a safety net equivalent to FDIC insurance. If that objection is credibly addressed, the Aave App has a real shot at acquiring users who would never have considered a self-custodial product otherwise.

The Moat Question

The framing that matters most for this landscape comes from Simkin directly:

"A big mistake everybody seems to be making right now is that the neobank game is copy-paste Revolut's UI and functionality, rebuild it on stablecoins, promise maybe a token for cashback, and then go and compete on distribution. I think this is an incredibly short-sighted way of approaching this. Wherever the moat is, in my understanding, is not somebody who can get the most licenses like it was on Web2. The moat is actually identifying the right hard technical problems and solving them consistently in a way that actually improves the product — credit, privacy, compliance in a way that works for onchain and offchain. When you actually solve all these hard problems, that compounds."

The charter-as-moat argument has commoditized. Bridge, Rain, and their equivalents are spinning up fiat rail connectivity across jurisdictions faster than any individual player can build themselves. The compliance layer is becoming infrastructure. What remains defensible is the data layer: the behavioral data that makes underwriting better than anyone else's. Shopify Capital can underwrite merchant loans at favorable rates because it sees exactly how much revenue those merchants generate through the platform. The same logic produced Mercado Pago's $12.5B loan book: start with the commerce relationship, let the data accumulate, deploy credit when the underwriting is ready.

The same principle applies onchain. Squads sees onchain transaction history, ACH payment patterns, and card spend for every Altitude customer; combining those data sets produces a credit profile no traditional underwriter can replicate. As more businesses and consumers transact onchain, this data becomes an increasingly durable moat.

Credit as the Missing Piece: The Tether Thesis

What is missing from every player in this section is unsecured consumer lending. As discussed in the banking-first section, this is the highest-margin product in retail finance and the one that separates a payments app from a neobank. Every player discussed above offers some version of stablecoin yield, trading, payments, and a debit card. None has cracked consumer credit underwriting at scale.

The problem is not technical but structural: the lack of a credible underwriting framework and regulated capital source. For businesses, the path is clearer. Onchain native businesses with programmatic revenue streams allow a smart contract to guarantee that a portion of revenue flows to loan repayment automatically. For consumers, the data picture is still thin, and legal recourse is limited. Unsecured consumer lending through onchain neobanks is likely still a few years away.

In our view, the most underrated potential entrant in unsecured credit is not coming from any of the players above. On Feb. 25, 2026, Tether Investments announced a $200M strategic investment in Whop, valuing the platform at $1.6B. Whop is a marketplace for digital products with 18.4 million users and approximately $3B in annual creator earnings, growing gross transaction volume at roughly 25% month over month. As part of the deal, Whop will integrate Tether's Wallet Development Kit, making it a self-custodial wallet for its community and explicitly enabling lending and borrowing through DeFi primitives.

The investment is best understood as a distribution acquisition. Tether's CeFi lending book is approximately $16B, entirely institutional and collateralized. It has never done consumer underwriting because it has never had consumer behavioral data. Whop changes that. Transaction history, revenue consistency, audience growth, and churn rates for creator businesses are exactly the kinds of behavioral data that make credit underwriting better. The parallel to Mercado Pago is almost exact: Whop is the marketplace, Tether is the capital, creator storefronts are the merchants. The strategic logic is the same logic that produced Mercado Pago's $12.5B loan book. To be clear, Tether has not announced a lending product and may never extend into unsecured consumer credit, but the foundations have been laid.

Infrastructure Layer

The stablecoin-first landscape described above depends on a layer of infrastructure that most end users will never see. Almost every user flow touches fiat at some point, and that means it touches an on-ramp or off-ramp. The value that accrues to infrastructure players is foundational rather than lateral: the neobanks above are the distribution layer, but the companies below set the price, speed, and compliance cost of the product those neobanks can offer. This is the picks-and-shovels dynamic of the stablecoin era.

This infrastructure splits cleanly into three categories: fiat connectivity, stablecoin issuance, and yield.

Fiat Connectivity

Bridge is the primary player here. Its Orchestration APIs enable businesses to move funds across the globe in minutes and offer virtual USD, EUR, GBP, MXN, and BRL accounts for consumers and businesses globally. The product suite covers the full stack of what a neobank needs to plug in fiat: on-ramps and off-ramps, cross-border transfers, FX conversion, card issuance, and wallet creation. The distribution advantage compounds through the Stripe acquisition: Stripe's existing merchant relationships and card infrastructure become Bridge's go-to-market. Fuse, Phantom's CASH, and Native Market's USDH are already built on Bridge rails.

Rain raised $250M in a Series C led by ICONIQ at a $1.95B valuation. Rain's end-to-end payments platform allows companies to launch compliant Visa stablecoin cards, currently facilitating over $3B in annualized transactions for over 200 partners. Rain holds Visa Principal Member status, meaning it can issue Visa cards directly without a bank intermediary. Its acquisitions of Fern and Uptop in late 2025 suggest it is building toward a more complete infrastructure offering rather than remaining a pure card-issuance layer.

Gnosis Pay offers a self-custodial Visa debit card. Funds remain onchain in a Safe smart account until the moment of settlement, meaning users never relinquish custody to spend. The card processed $131M in volume in 2025 and is targeting $1B in 2026, with a permissionless white-label API now open to developers and a North America and APAC expansion underway. The broader Gnosis 3.0 stack, which bundles Safe smart accounts, CoW Swap, and Gnosis Business alongside Gnosis Pay, positions it as infrastructure for self-custodial consumer finance rather than just a card product.

Mesh closed a $75M Series C led by Dragonfly Capital at a $1B valuation in January 2026. Its SmartFunding technology enables consumers to pay with any asset they hold while merchants receive instant settlement in their preferred stablecoin or local currency.

Squads deserves mention here in its infrastructure capacity thanks to Altitude, its business banking product. Altitude offers global business accounts with USD and EUR local bank details, stablecoin and traditional bank payment rails, zero-fee on/off ramps, and a full CFO stack including bill pay, corporate cards, and accounting exports.

Stablecoin Issuance

Every platform of sufficient scale is issuing or planning to issue its own stablecoin. Jupiter has jupUSD, Phantom has CASH, EtherFi has CASH, and Aave has GHO. The economics are straightforward: rather than letting Circle or Tether capture the reserve yield on dollars held in the platform, issuers capture it themselves. Bridge's Open Issuance platform provides the necessary infrastructure for this, with full customization on reserve allocation, blockchain support, and reward structure, while maintaining interoperability across all Bridge-issued stablecoins.

Yield Integrations

The most underappreciated infrastructure category in this stack is yield delivery. As more neobanks offer savings or earn products, the question of where that yield comes from and how it gets integrated becomes critical.

In our view, an interesting dynamic in yield infrastructure is not the API aggregators like Yield.xyz but the yield-bearing asset issuers going to neobanks directly. Maple Finance has explicitly flagged that demand for dollar-denominated yields extends well beyond DeFi and that fintechs, neobanks, and CeFi platforms represent an expansion target for syrupUSDC and syrupUSDT. The team said its first exchange-earn program is imminent and that it aims to sign three fintech partners by the end of Q1 2026. While fintech integrations can be slower to close given heavier compliance requirements, they could be a meaningful demand driver, with Maple projecting $500M-$1B of fintech-sourced capital by year-end.

Yield-bearing asset issuers are running the same playbook as stablecoin infrastructure providers, but one layer up. Bridge convinced neobanks that building your own fiat rails was unnecessary when you could plug into theirs. Maple is making the equivalent case for yield: building your own lending book is unnecessary when you can plug into institutional-grade overcollateralized yield through a single integration. The neobanks in this report will likely be the distribution layer; the question is if they will embed external sources of yield or build the lending book themselves.

Agentic Finance

The neobank competition described in this report has so far played out on familiar terms: distribution, data, and the primary financial relationship. Agentic finance changes the terms.

AI will matter for neobanks in two phases. The first is operational: lower servicing costs, faster support, and better fraud triage. The second is strategic: agents that do not just assist users, but move money on their behalf. The second matters more. Over time, the key competitive question is not which platform adds the most AI features, but which can safely support delegated finance through clear permissions, monitoring, and liability.

The near-term impact is operating leverage. Klarna said its AI assistant handled 2.3M conversations in its first month while cutting resolution times dramatically. Chime has described similar gains, with fraud losses down 29% since 2022. These benefits are real, but they are unlikely to be a durable moat. AI at the support layer is better understood as margin support than competitive differentiation.

The harder problem starts when agents become actors rather than tools. Existing neobank systems were built for human transaction behavior: payroll, bill pay, card spend, and occasional transfers. Agent activity can look very different. A wallet making hundreds of small payments per day may be normal for software, but it triggers fraud and AML systems designed around human behavior. In an interview with Bridge’s Ben O’Neill, he noted that a pattern of many small-dollar agent transactions could potentially flag existing compliance systems even if the underlying activity were entirely legitimate. Agent accounts will need to be evaluated under fundamentally different criteria than human ones, since their transaction cadence, size distribution, and frequency have no analog in the patterns today's controls were built around.

The core distinction is enforcement. Onchain systems can impose transaction limits directly at the execution layer through scoped keys or smart contracts. Bank API models rely on middleware and internal controls layered on top. Simkin described this as "pairing probabilistic intelligence with deterministic execution": you give an agent a key scoped to specific addresses and thresholds, and the network's validators enforce those constraints at the transaction level.

His example was a rebalancing agent that sweeps idle cash into a yield-bearing treasury account. The worst-case failure is money moving to the wrong internal account, not an unauthorized external transfer. That guardrail is native to onchain execution and difficult to replicate through bank API wrappers. By contrast, Simkin noted that traditional fintech agent features today are largely "glorified autofills" — they assist a human workflow rather than operating autonomously within enforceable bounds. Incumbent networks are responding: Visa introduced its Trusted Agent Protocol in October 2025, and Mastercard launched Agent Pay in April 2025, both aimed at becoming the trust and authorization layer for agent-driven commerce.

Economics Will Move Toward the Platform of Record

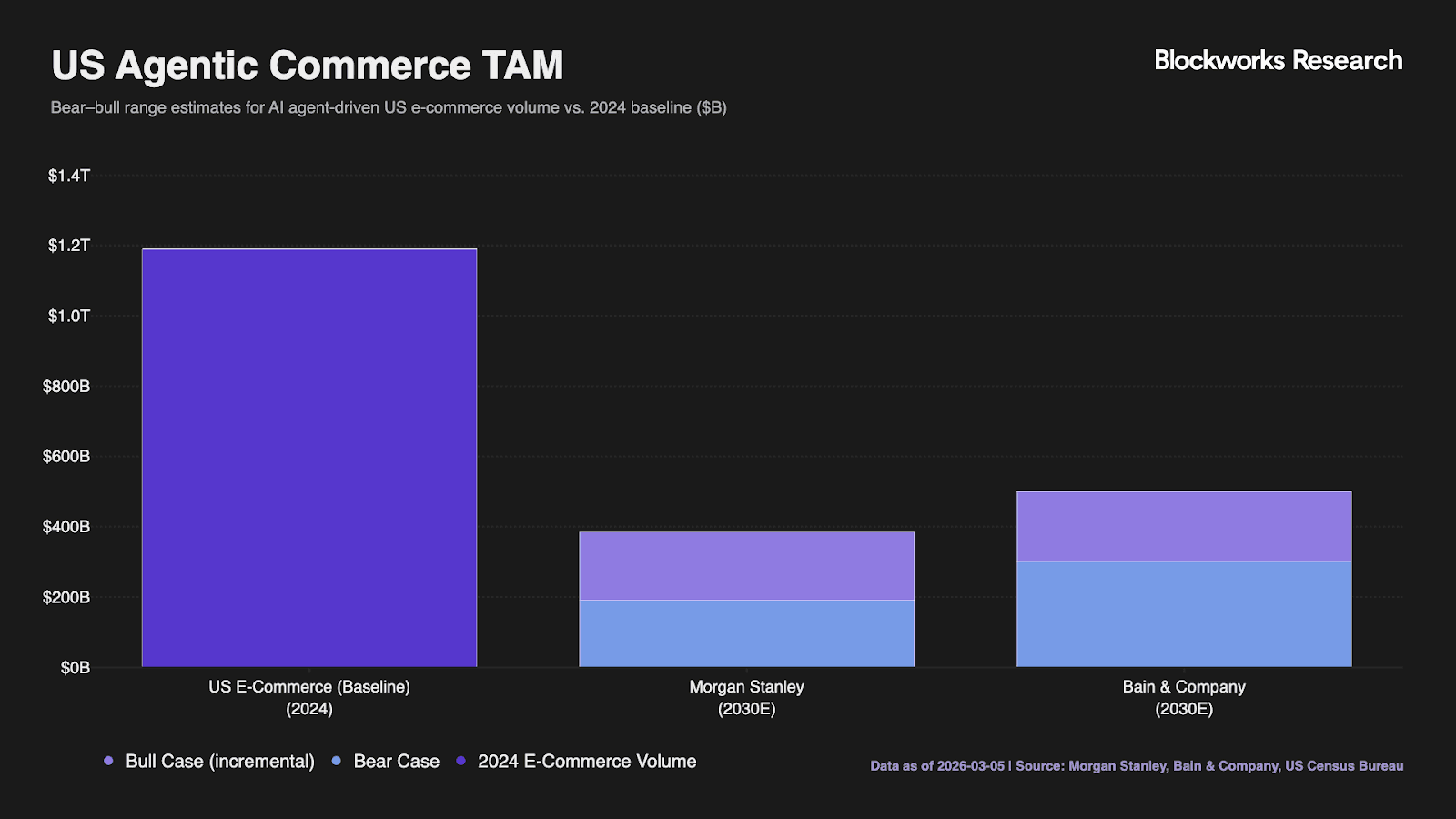

The important position for neobanks is the platform of record: the layer where identity, permissions, liquidity, and dispute resolution sit. Agent-driven commerce could be meaningful. Bain estimates $300B-$500B of US e-commerce by 2030, roughly 15-25% of the market. The winner is less likely to be the cheapest rail and more likely to be the platform that governs what the agent is allowed to do.

Interchange-heavy models are the most exposed, because agents can route spend toward lower-cost rails. There are early signs the revenue model is already shifting: Simkin pointed out that Ramp recently introduced SaaS pricing alongside interchange, a move he attributed to agent workflows enabling outcome-based charging rather than per-swipe economics.

Chartered lenders are better insulated because their core economics come from credit, not payments. Commerce-embedded platforms face a different risk: if agents intermediate checkout, underwriting-relevant behavioral data may stop accruing to the platform.

Onchain models are the most naturally aligned with agentic finance architecturally, but still lack mainstream distribution. O'Neill argued that distribution remains the fundamental moat: volume surfaces edge cases, edge cases harden the product, and product reliability compounds over time. The platforms best positioned are those that can orchestrate across fiat rails, onchain settlement, and compliance in a single layer — and that have the distribution to compound their way through the hard problems that only emerge at scale.

Final Thoughts

Each archetype leaves a lesson. Banking-first proved that trust compounds slowly. Stablecoin-first neobanks face a harder version without insured deposits in the US and Europe, which points toward emerging markets first. Commerce-embedded superapps showed that data is the moat: as more value moves onchain, that data becomes available to stablecoin-first platforms, unlocking unsecured lending they don't offer today and meaningfully upgrading their economics. Trading-first platforms showed that the trading relationship is a natural cross-sell surface: users who trust a platform with their investments are easier to convert on banking, credit, and payments.

The central question for stablecoin-first neobanks is expansion beyond the crypto-native base. Platforms like KAST suggest that cross-border earners may be one of the earliest and clearest wedges for that expansion. Yield is the strongest near-term wedge, particularly in emerging markets. The deeper unlock is how quickly transactional value moves onchain at sufficient scale to make unsecured lending viable. That's the product that would close the gap with incumbents and the one furthest from being solved.

Infrastructure providers like Bridge win regardless of which neobank captures the primary relationship. Agentic finance adds urgency: as agents begin moving money autonomously, the execution layer that can enforce permissions natively has an advantage that API-based models dependent on bank accounts will struggle to replicate. Whether stablecoin-first neobanks reach the required scale before incumbents close the gap is the open question.

This research report has been funded by Kast. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Radworks. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek the advice of a qualified financial advisor before making any investment decisions.