This research report has been funded by Blockdaemon. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Blockdaemon. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

The Institutional Staking Landscape

Key Takeaways

- Institutional staking has rapidly matured into a sophisticated global market, catalyzed by Ethereum’s Proof-of-Stake transition and greater regulatory clarity, particularly in the US.

- Institutional staking providers emphasize secure, non-custodial solutions with robust compliance frameworks, differentiating themselves through service quality, risk management, and regulatory alignment.

- DeFi-Native and liquid staking solutions offer enhanced liquidity, composability, and MEV optimization, increasingly attracting yield-sensitive institutional investors. Institutional providers offer comprehensive liquid staking infrastructure across multiple networks, while providers are integrating sophisticated reward optimization strategies, including preconfirmation services and MEV extraction capabilities to deliver superior institutional yields.

- 'Earn' programs are emerging as hybrid products that combine traditional staking with DeFi protocols to maximize institutional yield opportunities. Leading providers utilize API integrations with leading DeFi protocols, as well as combining staking rewards with additional layers through partnerships with protocols and automatic allocation of institutional capital across staking and DeFi opportunities to maximize risk-adjusted returns.

- ReStaking represents an emerging frontier, enabling institutions to simultaneously earn rewards across multiple networks or applications, though it introduces complex risk management requirements and heightened slashing vulnerabilities. Institutional providers are integrating platforms, offering enhanced yields while requiring sophisticated risk assessment frameworks.

Introduction

Institutional staking providers specialize in offering secure, compliant, and scalable solutions for organizations, asset managers, and individuals who wish to stake large volumes of digital assets. Staking-as-a-Service Providers (SaaSPs) act as intermediaries, running blockchain nodes and managing the technical complexities of staking on behalf of clients, often providing custody, reporting, and yield optimization features across a broad range of assets and networks.

While early adopters were primarily retail users and crypto-native funds, the past three years have seen an influx of institutional players, drawn by the potential for predictable yield, low operational friction, and growing onchain governance influence. Notably, our January 2025 survey of institutional investors conducted by EY Parthenon and Coinbase found that among respondents planning to or already engaging with DeFi products, 38% indicated interest in staking, second only to derivatives and perpetual products. Today, institutional staking spans a wide range of providers, each with distinct risk and operational profiles, as well as differentiated regulatory and technical considerations.

Market Growth and Institutional Adoption

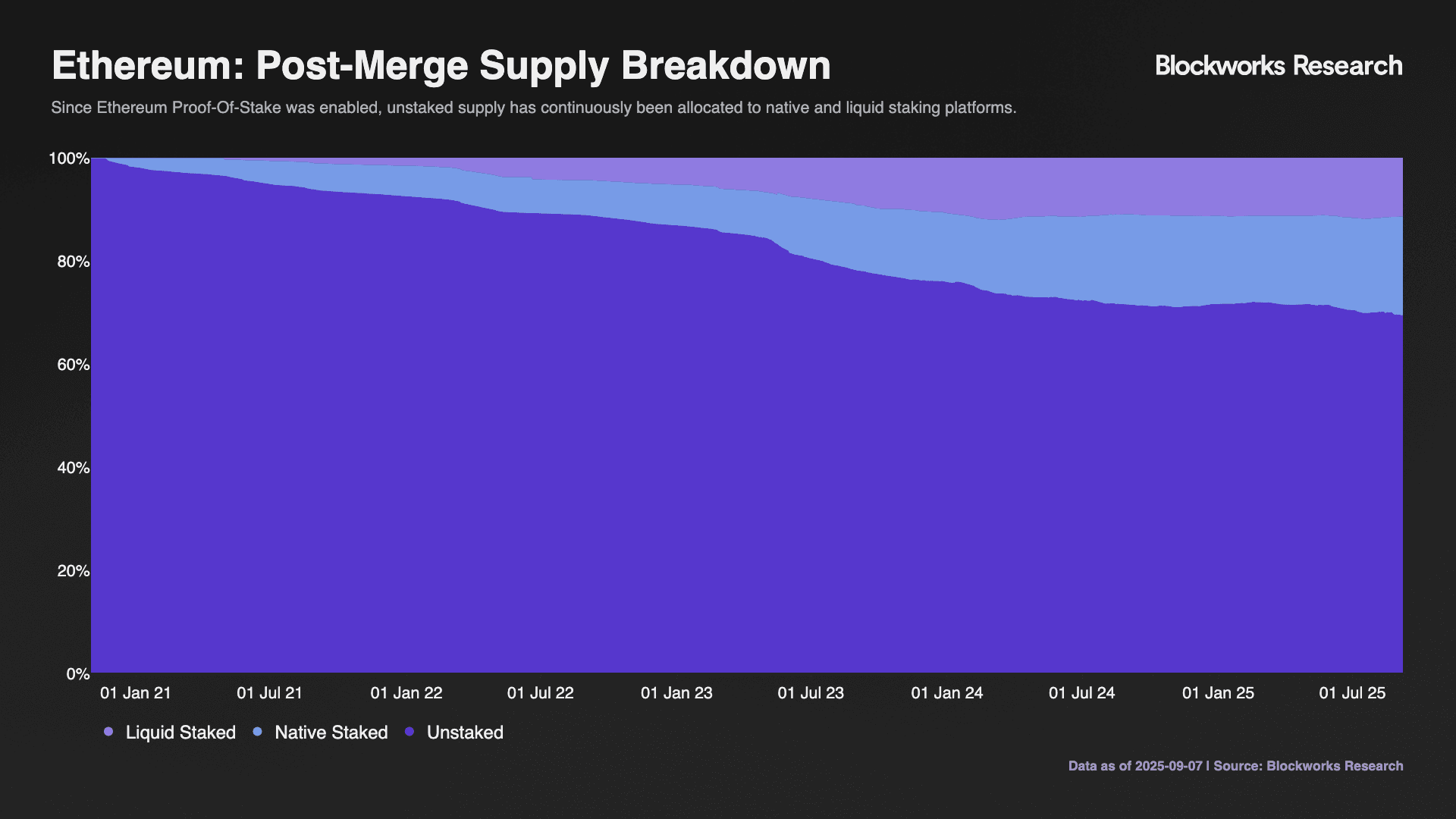

Staking has become a fundamental part of blockchain network design, operation and participation, with Ethereum’s Merge to Proof-of-Stake in 2022 marking a significant growth catalyst. While networks like Solana, Polkadot, Cardano, Near, and Celo had already implemented staking mechanisms, Ethereum's transition increased the relevance of staking across the industry. The ability to withdraw staked ETH, enabled in 2023, unlocked new participation, quelling concerns around illiquidity and risk. As staking matured, providers introduced features aligned with institutional requirements like SLAs, slashing insurance, multi-network support, and regulatory compliance. The Ethereum Pectra Fork, deployed to mainnet in May 2025, introduced a dramatic change to validator economics through EIP-7251, which increases the maximum staking cap per validator from 32 ETH to 2,048 ETH. This change allows large institutional validators to consolidate their operations significantly, reducing infrastructure complexity and operational overhead by managing fewer validator nodes while staking the same total amount of ETH. Additionally, institutional validators are increasingly focusing on client diversity as a critical risk management strategy, with leading staking providers actively distributing their validator operations across multiple Ethereum client implementations to enhance network resilience and reduce correlated failure risks. These enhancements, combined with increasing clarity from US regulatory bodies around non-custodial staking models, have set the stage for rapid institutional growth.

We are seeing a notable rise in institutional participation in staking, with hedge funds, venture funds, and an emerging set of traditional financial institutions staking holdings to earn yield. As of late 2024, a Blockworks Research survey found nearly 70% of institutional token holders were staking their ETH as a way to earn steady, predictable yields on long-term crypto holdings in a low-rate macro environment.

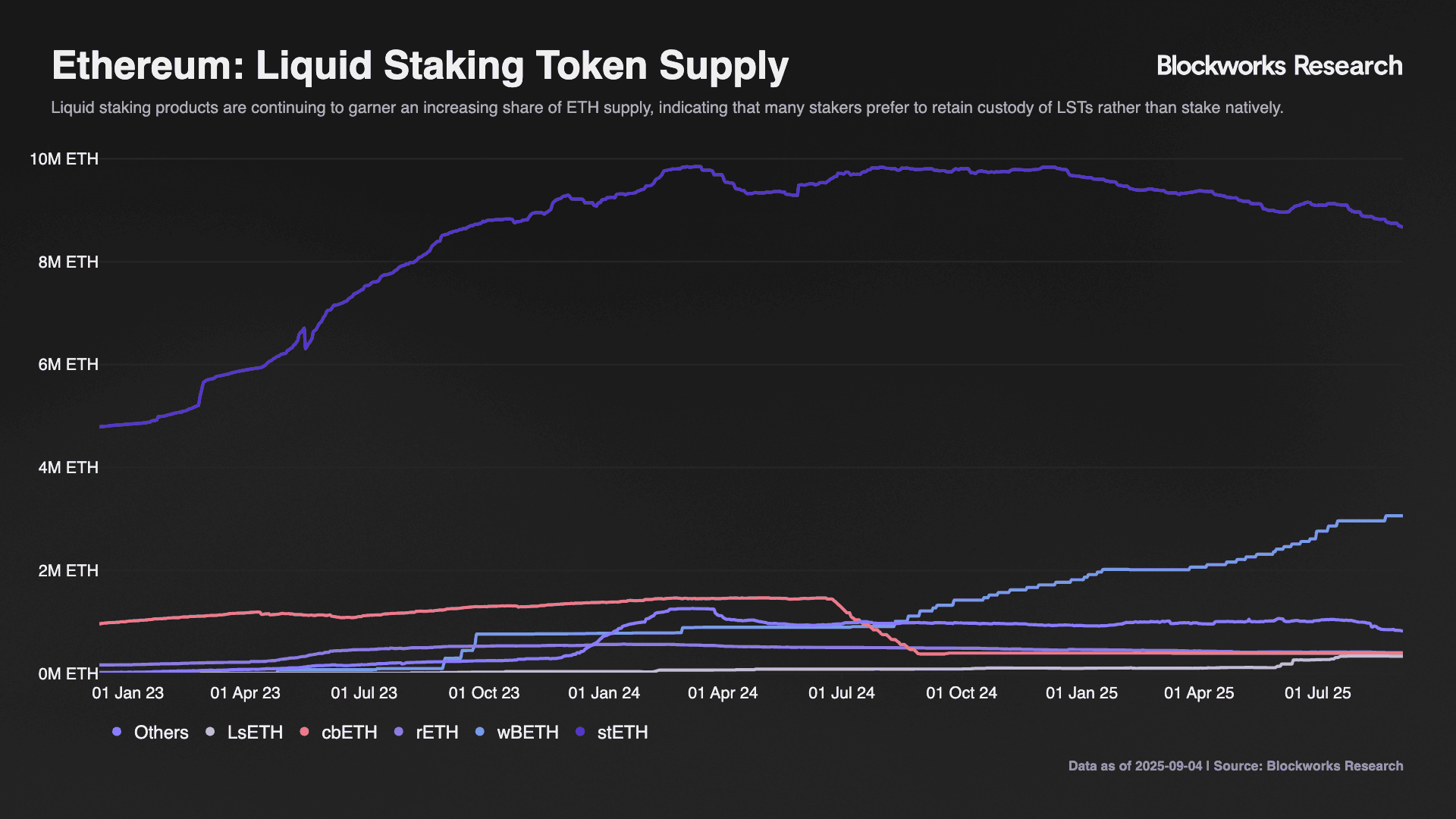

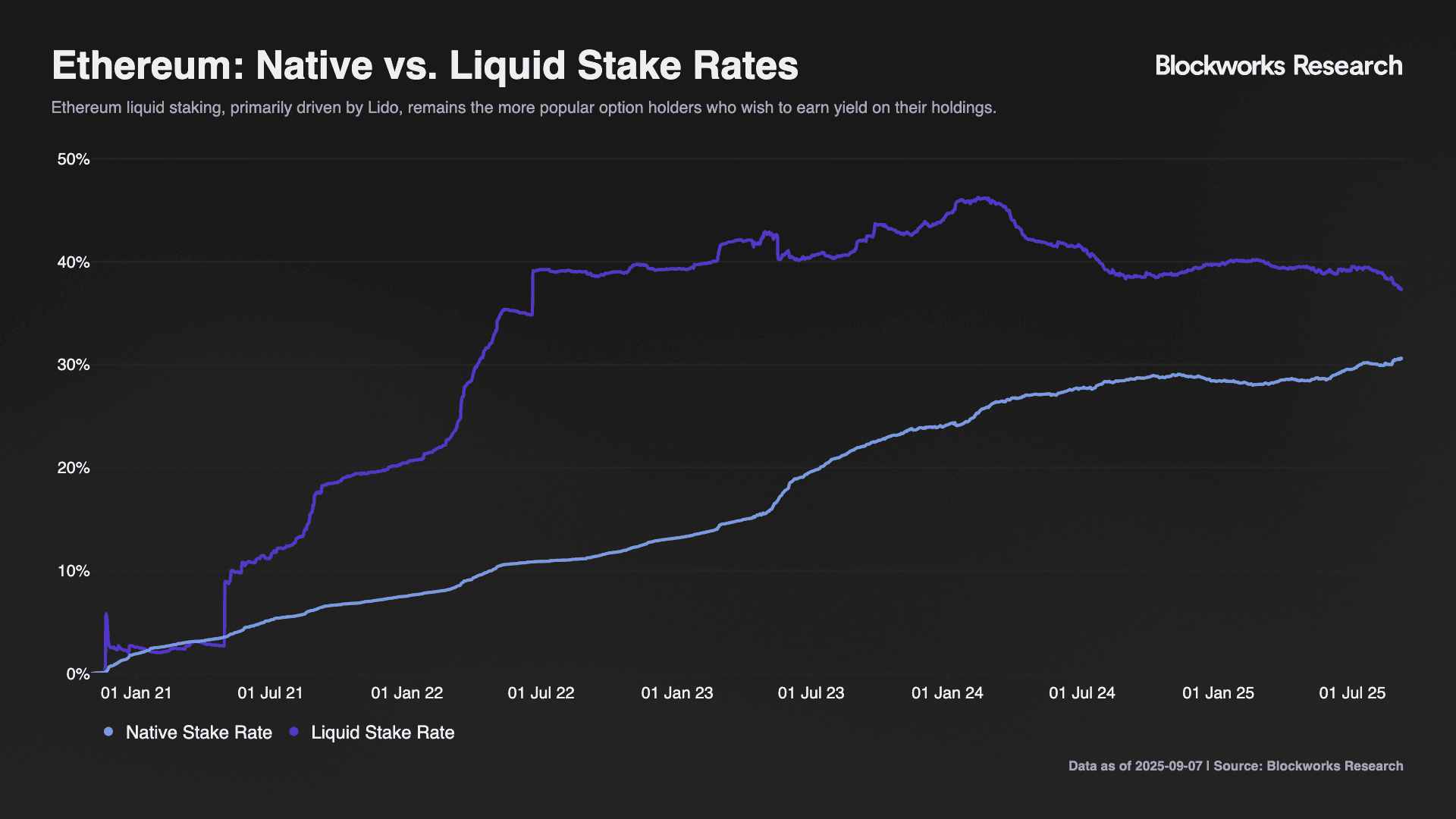

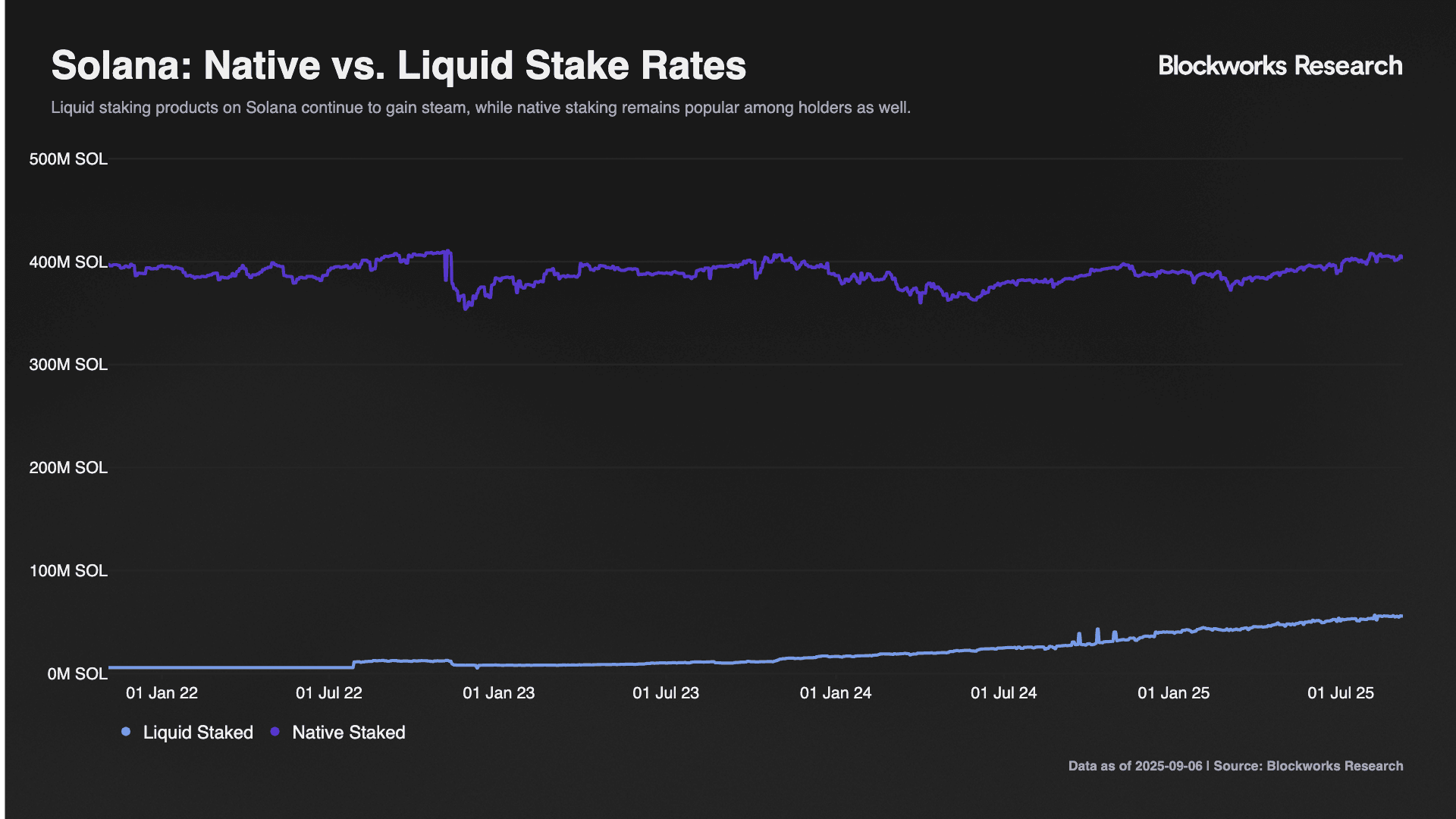

Liquid staking protocols have also exploded in popularity, allowing users to stake while maintaining liquidity via derivative tokens. Lido remains the largest staking provider, currently accounting for ~24% of all staked ETH, highlighting that many stakers value decentralization and liquidity. Looking ahead, Lido's proposed V3 upgrade introduces modular stVaults that will enable customizable staking setups for institutions and complex investment strategies, potentially launching as early as Q3 2025. Additionally, a flourishing liquid staking ecosystem has emerged on Solana over the past 18 months, pioneered by Marinade Finance, expanded upon by dozens of independent providers and aggregators such as Sanctum.

Staking Primitives

The staking landscape has evolved significantly, diversifying into distinct segments catering to specific user groups, risk profiles, and liquidity requirements. These segments can broadly be categorized as Exchanges, Institutional Providers, and DeFi-Native solutions, including Liquid Staking and ReStaking.

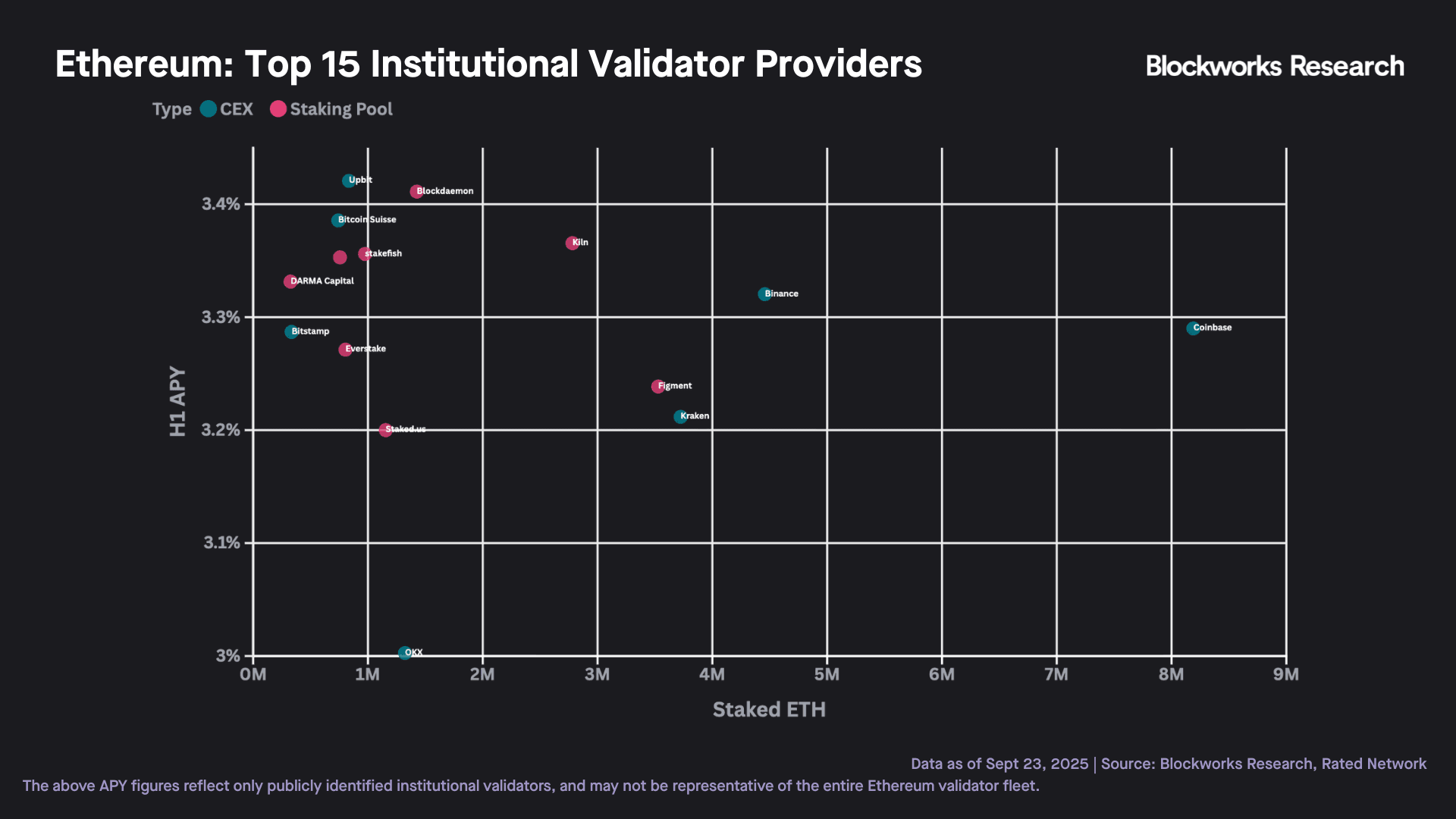

Exchanges remain highly prominent, focusing on both retail and institutional participants. Retail staking is largely dominated by centralized platforms like Coinbase, Binance, and Kraken, which offer custodial services designed around ease-of-use, streamlined interfaces, and comprehensive customer support. Coinbase and Binance exemplify this market positioning, managing a combined ~20% of all staked ETH, highlighting market acceptance despite inherent reliance on platform security. Institutional exchanges and custodians, including Hex Trust, Anchorage Digital, and Copper, integrate staking solutions directly into secure custody frameworks, tailored specifically for institutional demands with an emphasis on compliance, rigorous governance participation, and detailed reporting. Additionally, some institutional staking services operate on a non-custodial basis, where specialized staking providers manage the validator operations while funds remain under the control of institutional custodians or smart contracts. For institutions that already rely on trusted custodians for asset storage, this is an attractive onramp to staking with minimal operational effort.

More recently, traditional brokerage platforms have begun layering in native staking experiences. For example, Robinhood’s August 2024 launch of a self-custodial Solana wallet and its subsequent roll-out of 5% APY Solana staking in Europe demonstrate how legacy finance firms are leveraging simple, high-yield protocols to extend blockchain service upside to their existing user base. This strategy accelerated significantly with Robinhood's July 2025 launch of ETH and SOL staking in the US market, featuring an unprecedented $1 minimum stake requirement that dramatically lowers barriers to entry for retail participants. This approach aligns Robinhood with other major platforms, but lacks transparency regarding its validator sources, leaving open the possibility of in-house management or undisclosed partnerships. Meanwhile, Coinbase has doubled down on integrated institutional offerings, combining brokerage, custody, fiat-crypto ramps, stablecoins, staking, and tokenization under one roof, and continues to forge high-profile alliances like its staking collaboration with BlackRock, underlining how turnkey solutions are now table stakes for large asset managers.

Dedicated Institutional Providers, distinct from exchanges, primarily offer specialized, non-custodial staking infrastructure services. These providers, including Blockdaemon, Figment, and P2P.org, emphasize technical excellence, reward optimization, and comprehensive client reporting, catering specifically to the risk and compliance standards required by institutional clients. Offerings from these providers typically span multiple blockchain networks and facilitate active governance participation, making them attractive to institutions seeking secure, high-performance staking without direct custody risks.

White-label Providers occupy a crucial niche in the staking ecosystem, catering primarily to businesses seeking turnkey staking solutions. These providers offer infrastructure and technical expertise that allows clients, such as exchanges, wallets, and custodians, to seamlessly offer staking services without developing their own staking infrastructure. Leading providers in this segment operate on B2B2C models, delivering staking capabilities behind the scenes for prominent platforms across the industry. Multiple established operators provide white-label solutions with various institutional partners, running validators for their staking offerings. Major industry participants, including exchanges, custody providers, and protocol platforms, frequently utilize these infrastructure services, demonstrating the extensive market penetration of white-label solutions. This enables institutions to effortlessly incorporate staking functionality into their offerings while ensuring comprehensive institutional compliance, detailed reporting, and governance standards. Consequently, white-label providers play a pivotal role in democratizing staking, significantly expanding access while maintaining a high level of institutional trust and operational efficiency.

DeFi Native providers include Liquid Staking Tokens (LSTs) and the emerging practice of ReStaking. Liquid staking providers like Lido, Rocket Pool, and Ether.fi issue tokenized staking assets that combine yield generation with enhanced liquidity and interoperability across DeFi platforms. While appealing due to their liquidity and capital efficiency, these solutions present concerns related to smart contract vulnerabilities and operational transparency, causing some institutional hesitation. ReStaking presents an innovative approach that allows users to leverage a single staked asset across multiple networks or applications simultaneously. This strategy enhances capital efficiency and potential yields, attracting institutions looking to maximize returns and asset utility. However, ReStaking introduces complex risks, including heightened vulnerability to slashing, increased protocol dependencies, and significant risk management complexities.

The staking ecosystem comprises interconnected yet distinct service providers, each catering uniquely to varied investor requirements, risk appetites, and compliance expectations. Understanding these nuanced distinctions remains critical for effectively navigating the evolving and increasingly sophisticated staking market.

Competitive Dynamics

Within the institutional staking provider sector, competition is intensifying as staking grows. Many providers support overlapping sets of networks, so they vie to win the same large token holders as clients. This leads to competition on commission rates, which are compressing for basic staking services. Providers typically charge in the range of 5-10% of rewards as fees, but institutions sometimes negotiate lower rates due to volume and newer entrants sometimes undercut on fees to attract clients from incumbents.

Institutional Decision Framework: When evaluating staking providers, institutions must balance three critical factors in their selection process. Security considerations encompass infrastructure redundancy, validator key management practices, slashing protection mechanisms, and geographic distribution of nodes to mitigate systemic risks. Reliability factors include historical uptime performance, disaster recovery capabilities, monitoring systems, and the provider's track record during network upgrades or emergencies. Reward optimization involves comparing not just commission rates, but also the provider's ability to maximize MEV opportunities, participate in governance decisions that benefit token holders, and offer value-added services like automatic compounding or DeFi yield enhancement strategies. Institutions typically establish weighted scoring systems across these dimensions, with security often taking priority over marginal reward differences, particularly for fiduciary-bound entities like pension funds or insurance companies.

Service Differentiation: One provider might distinguish itself with a superior user dashboard and analytics, while another prides itself on governance support. Some offer value-adds like reward reinvestment via automatic compounding, MEV reward maximization, or research on network upgrades to keep clients informed. Advanced providers are also differentiating through sophisticated reward optimization strategies, including preconfirmation services and liquid staking solutions that allow institutions to maintain liquidity while earning staking rewards. For example, Blockdaemon offers comprehensive liquid staking infrastructure across multiple networks, including Ethereum and Kusama, providing institutional clients with compliance-focused solutions that include KYC/AML requirements, seamless minting and redemption capabilities, and enterprise-grade node operator services."

Earn Stack Offerings: Institutional "Earn" programs such as Blockdaemon’s Earn Stack, and Kiln’s Earn program are emerging as sophisticated hybrid products that layer traditional staking rewards with DeFi protocol integrations through comprehensive API suites, enabling automated capital allocation across lending platforms, liquidity pools, and yield farming opportunities while maintaining enterprise-grade compliance standards. These programs utilize yield aggregators that continuously optimize capital deployment by analyzing onchain liquidity signals and offchain macroeconomic indicators, automatically rebalancing portfolios across multiple protocols to maximize risk-adjusted returns within client-defined risk parameters. The resulting infrastructure provides institutions with turnkey access to complex DeFi strategies, including liquidity mining, automated compounding, and cross-protocol arbitrage opportunities, all delivered through white-labeled dashboards with institutional-grade reporting and custody integration.

Collaboration Amidst Competition: It’s not uncommon for one provider to delegate to another in certain cases for load balancing or if they decide to focus on fewer networks. We also see consortiums where multiple institutional validators jointly secure a network.

Geographical and Regulatory Positioning: Some competition comes down to jurisdiction. Many institutions may choose to stake assets with a provider licensed in their country or region. Providers are working to expand geographically, but local presence and licenses can be a differentiator. As regulations formalize, we might see certain providers becoming dominant in specific regions due to compliance credentials. OFAC compliance has become a particularly critical differentiator, as institutional clients increasingly require providers to demonstrate robust sanctions screening and compliance frameworks.

Scale vs. Niche: Larger providers compete on being able to handle very large stakes with proven infrastructure, while smaller niche providers compete by being more flexible and offering customized solutions such as reporting integrations and unique financial products. When evaluating providers, institutions must carefully compare offerings, considering factors such as protocol width (the breadth of supported networks), infrastructure security measures, and the provider's track record across different market conditions.

Rewards vs. Security Trade-offs: A key competitive dimension involves the balance between maximizing rewards and maintaining security. Some providers focus on aggressive reward optimization through timing games and sophisticated MEV extraction, while others prioritize validator security and network stability. Institutions must weigh whether higher potential returns justify increased operational risks. For example, on Solana, validators can maximize rewards by running multiple nodes and employing MEV strategies through programs like Jito, but this increases exposure to hardware failure and increases operator complexity compared to conservative validators that prioritize consistent uptime and proven infrastructure. Recent analysis from Blockdaemon demonstrates how aggressive MEV tactics like timing games and sandwich attacks, while potentially boosting short-term profits, can harm long-term network health and user experience. Their research shows that validators engaging in block production delays or vote timing manipulation may undermine network stability, particularly on high-throughput networks like Solana where even minor disruptions can significantly impact performance.

Compliance vs. Protocol Rewards: Providers increasingly compete on how they navigate the tension between regulatory compliance and reward maximization. Some offer compliant staking options that may sacrifice certain yield opportunities (such as sandwiching transactions or participating in timing-sensitive MEV strategies) to ensure full regulatory adherence, while others provide tiered services allowing clients to choose their risk-reward profile.

Multi-Provider Risk Management: Some institutions are adopting multi-provider strategies to hedge against operational risks and avoid concentration in any single validator. This approach allows institutions to diversify across different provider strengths, using one for compliance-focused staking, another for yield optimization, and a third for specific protocol expertise. While this creates additional operational complexity, it reduces counterparty risk and ensures continuity if any single provider experiences technical issues or regulatory challenges.

Financialization: There is also an emerging trend in offering hedging products for staking yields. Twinstake’s collaboration to execute the first ETH staking yield swap is an example where a staking provider adds value by enabling risk management for stakers. Such financial innovation could become another battleground, where providers that can integrate staking with hedging, lending, or liquidity solutions might attract more sophisticated institutional capital.

Market Leadership Definition: Being a top node operator in today's competitive landscape requires excellence across multiple dimensions beyond just technical competence. Leading providers must demonstrate consistent operational excellence through proven uptime records, sophisticated infrastructure with geographic redundancy, and robust security protocols including advanced key management and slashing protection. They differentiate through comprehensive service offerings that span multiple networks, provide enterprise-grade reporting and analytics, and offer innovative financial products like liquid staking and yield optimization. Top operators also maintain strong regulatory positioning with appropriate licenses and compliance frameworks, while building trusted relationships with institutional clients through transparent communication, responsive support, and proven performance during market stress periods. The most successful providers combine technical expertise with business acumen, positioning themselves as strategic partners rather than just service providers.

We also see cloud providers and node-as-a-service companies such as Allnodes, Chainstack, and QuickNode moving into the institutional staking arena, though some of these currently focus more on retail or developer APIs than bespoke institutional offerings. These providers compete on uptime, security, network breadth, and client service. Many offer integrations with custodians, allowing for seamless staking through secure interfaces.

Ethereum Staking Landscape

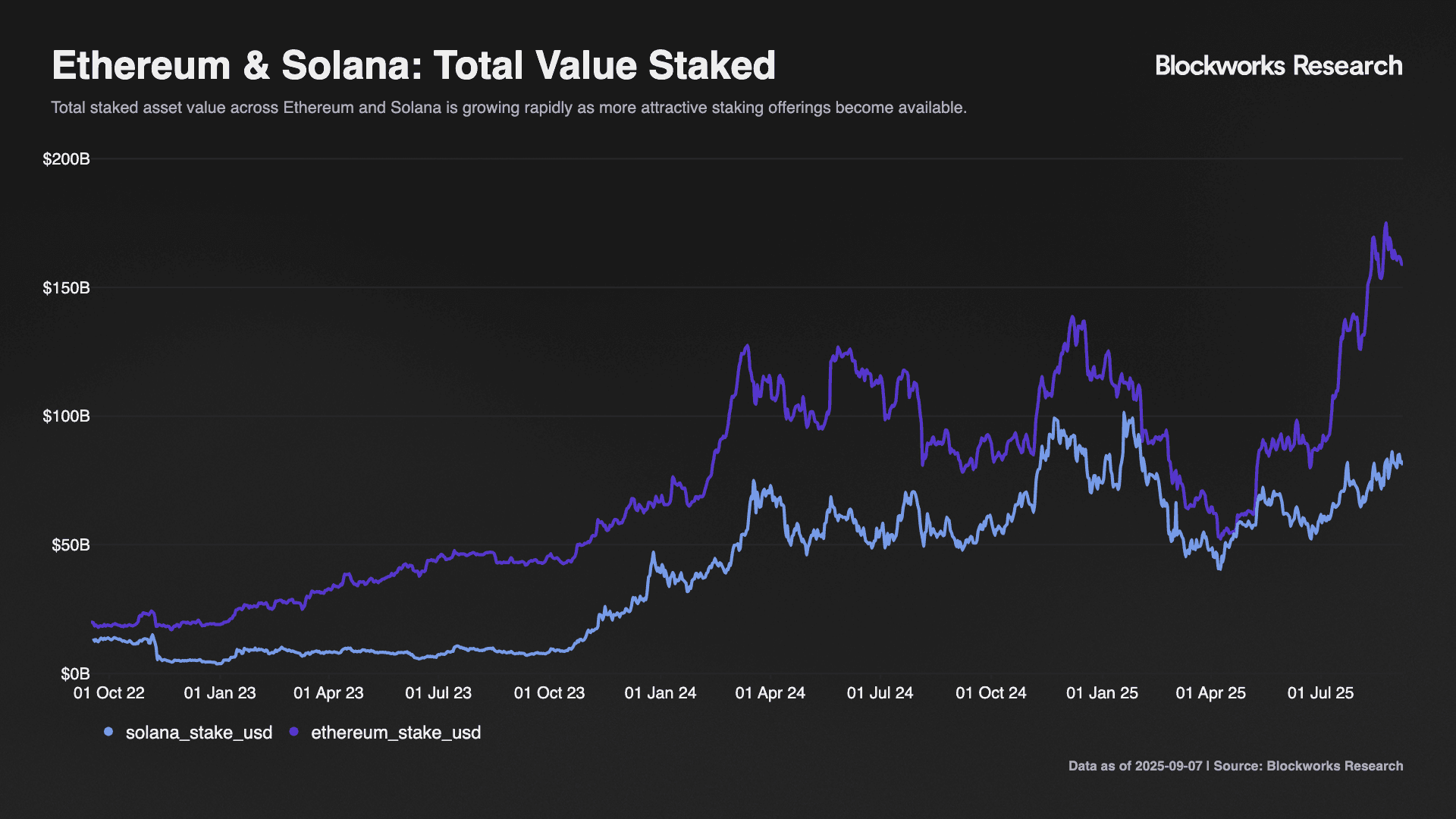

Ethereum's transition to Proof-of-Stake has fundamentally reshaped the institutional staking landscape, creating unprecedented opportunities for sophisticated capital deployment and yield generation. Currently, over 30% of Ethereum's total supply is staked, representing >$169B in secured value and demonstrating the maturation of institutional participation in network consensus mechanisms.

The institutional appetite for optimized staking strategies has manifested in record-breaking validator exit activity, with Ethereum's unstaking queue reaching ~750K ETH in late 2025, and wait times extending to ~13 days. This unprecedented volume is primarily driven by sophisticated repositioning rather than network abandonment. Key drivers include the unwinding of leveraged ETH strategies (particularly stETH loops on platforms like Aave as borrowing costs increased), arbitrage opportunities arising from slight stETH/ETH depegging, profit-taking following ETH's substantial August 2025 rally, and strategic preparation for emerging opportunities, including ETH staking ETFs.

This validator exit phenomenon reflects institutional sophistication in capital management, with large holders actively optimizing their staking positions based on evolving market conditions, regulatory developments, and emerging yield opportunities. This dynamic behavior contrasts sharply with earlier retail-dominated staking patterns, where exits were primarily driven by risk aversion rather than strategic reallocation.

Notably, the top three LSTs, Lido (285K ETH), Ether.fi (134K ETH) and Coinbase (113K ETH), accounted for the majority of unstaking activity, with Lido's queue reaching all-time highs. This exit activity largely reflects validators and institutions repositioning to participate in restaking protocols, capitalize on arbitrage opportunities, and optimize their staking strategies for evolving market conditions.

Lido's dominance in the unstaking queue highlights potential concentration risks that regulatory bodies and network participants continue to monitor. The protocol's planned V3 upgrade, introducing modular stVaults for customizable institutional staking setups, represents a strategic response to growing institutional demands for tailored risk management and compliance features.

Institutional staking infrastructure providers such as Blockdaemon have begun integrating platforms such as EigenLayer and Symbiotic, signaling restaking's strategic importance as a future-oriented institutional staking solution. These restaking integrations can significantly boost institutional returns, with platforms like EigenLayer offering up to 8% yields compared to standard ETH staking, while Symbiotic's multi-asset approach enables additional rewards by securing multiple networks simultaneously without requiring additional collateral.

Looking ahead, the potential approval of Ethereum staking ETFs could dramatically expand institutional access, while continued improvements in liquid staking infrastructure and restaking protocols promise to enhance capital efficiency for sophisticated institutional participants. The Ethereum staking landscape represents a mature, liquid, and institutionally accessible market that continues evolving to meet the complex requirements of professional asset managers and fiduciary-bound entities.

Solana Staking Landscape

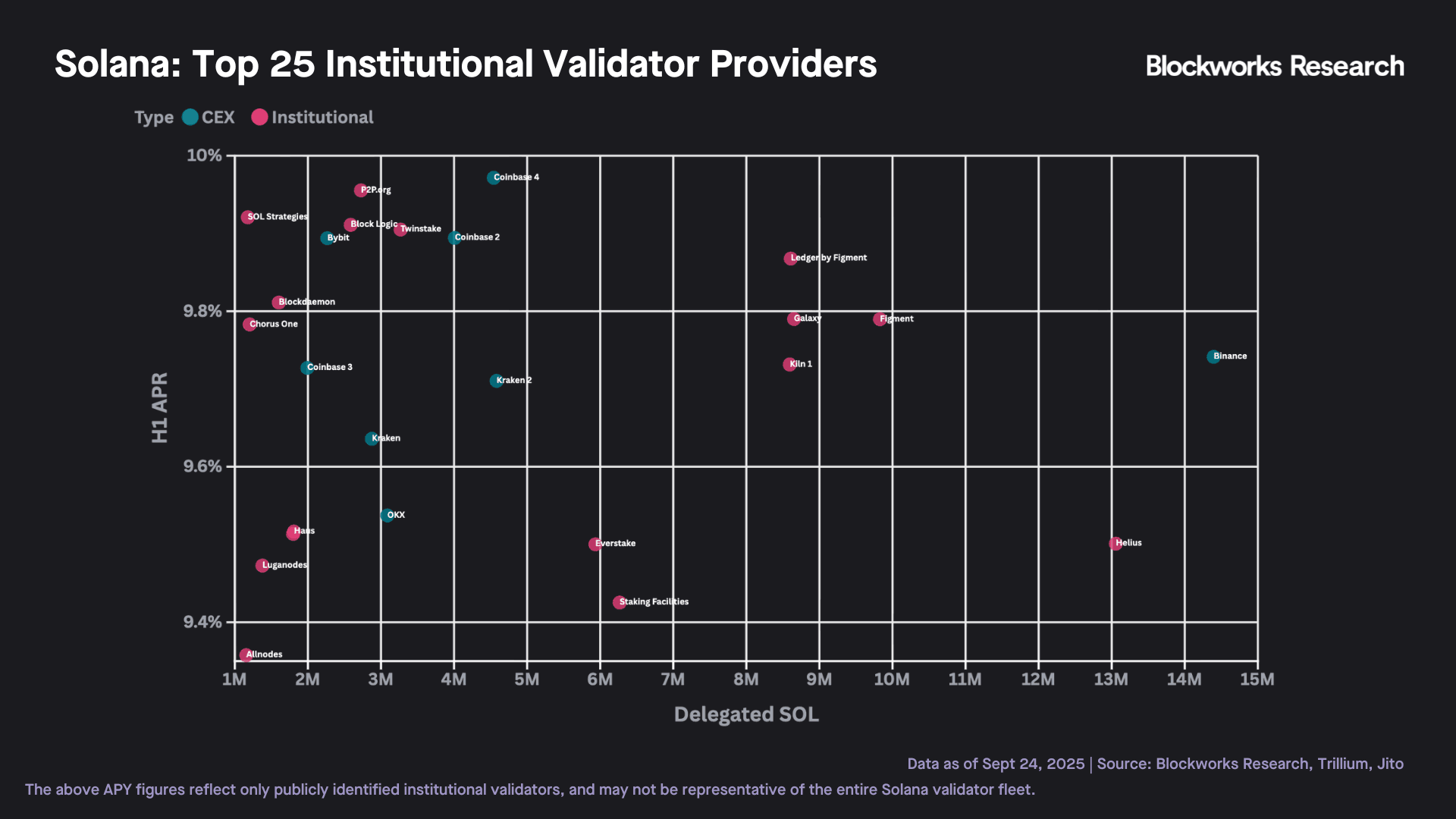

Solana has emerged as one of the leading blockchains for institutional staking, driven by high-performance architecture, low fees, and a rapidly growing ecosystem. Institutional staking on Solana has experienced exponential growth since early 2023, fueled by increased network stability, regulatory clarity, and attractive staking yields that align with institutional risk and return profiles. The network's infrastructure has undergone significant improvements, with skip rates dropping dramatically from 15% in 2021 to just 0.3% in 2025, while block times have improved from 640ms to 400ms, making Solana increasingly attractive for institutional validators seeking reliable performance. However, some validators continue to engage in latency manipulation strategies by intentionally delaying block production to boost rewards by up to 3% annually, which can push block times beyond the 400ms target and reduce overall network performance, prompting protocol-level responses like Timely Vote Credits and exclusion mechanisms.

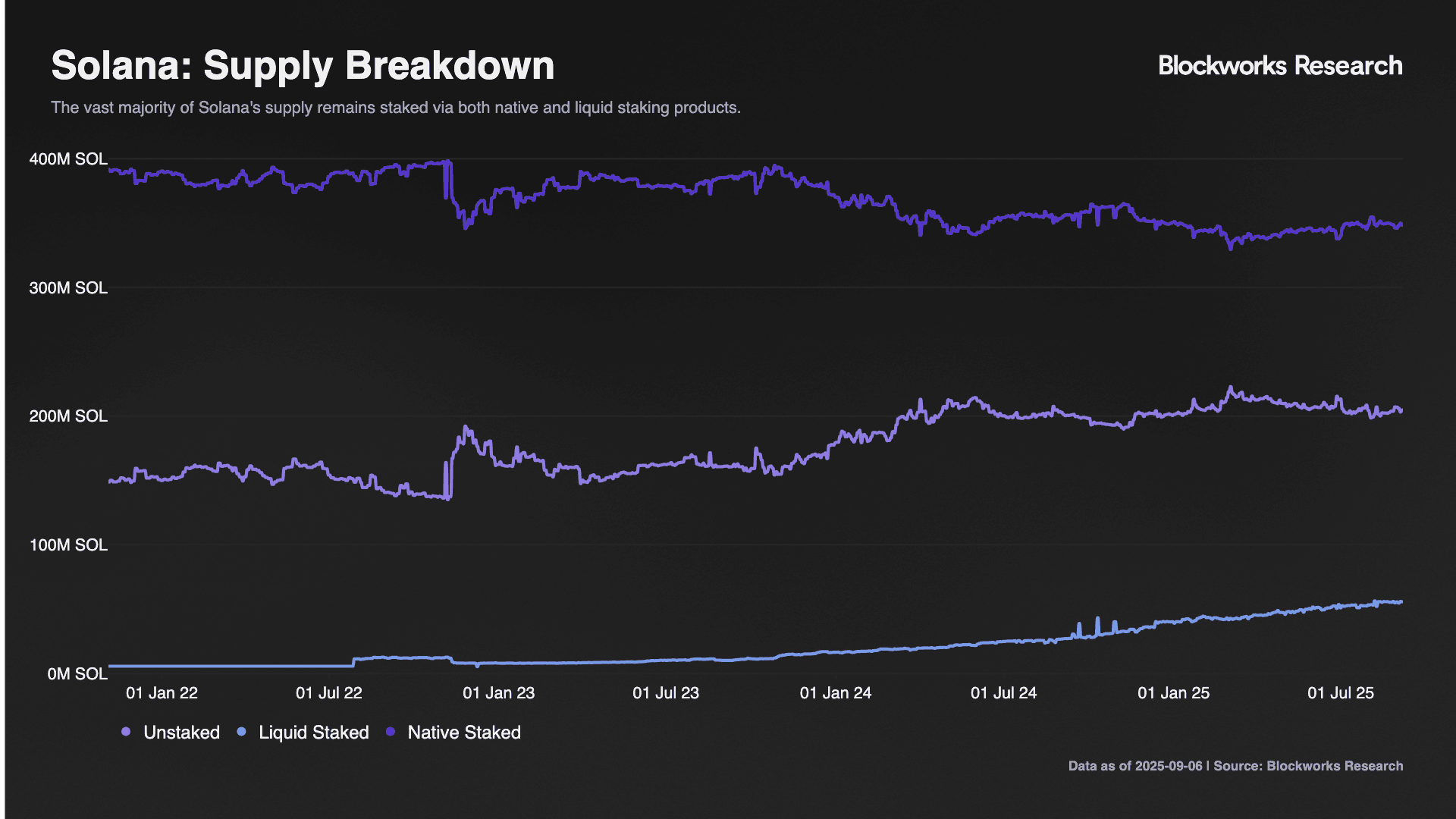

Currently, ~66% of Solana's total supply is actively staked, representing ~$97B in value. Institutional players, including crypto-native hedge funds, asset managers, and traditional financial institutions, increasingly view Solana staking as a strategic opportunity to gain predictable returns and influence network governance.

Leading institutional staking providers on Solana include Blockdaemon, Figment, Chorus One, and Stakefish. Providers such as Figment and Chorus One differentiate by offering extensive governance advisory services, helping institutions actively participate in Solana’s evolving ecosystem decisions. The competition among providers has prompted innovation in staking features, such as enhanced analytics dashboards, sophisticated reward optimization strategies, and proactive governance engagement. Many validators, including major providers like Figment and Blockdaemon, are integrating Jito Labs' Block Assembly Marketplace upgrade, positioning the provider to offer additional rewards opportunities through Plugin revenue sharing.

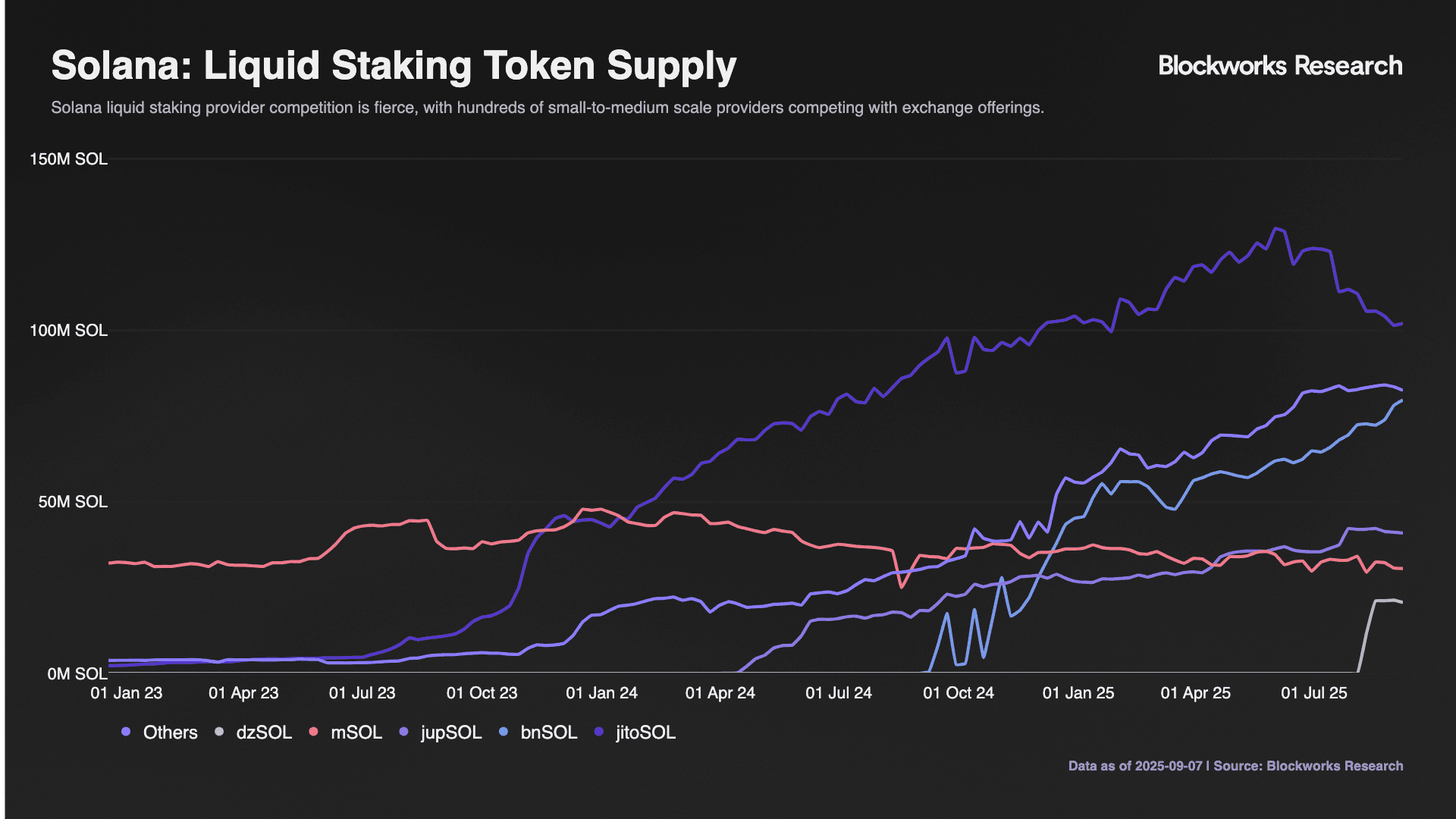

Solana’s liquid staking landscape has seen rapid maturation, currently accounting for >13% of staked SOL. Institutions favor the LST approach due to increased capital efficiency and seamless integration with Solana’s DeFi ecosystem. Jito Labs has uniquely positioned itself by integrating MEV (Maximal Extractable Value) strategies into its widely used validator client. Jito’s staking pools distribute additional MEV-derived rewards to stakers, offering institutions superior yield compared to traditional staking solutions, attracting substantial institutional inflows, particularly from yield-sensitive hedge funds. Fragmetric has emerged as Solana's first native liquid restaking protocol, partnering with Jito to launch fragSOL and addressing LST fragmentation by enabling unified management of multiple liquid staking tokens through its FRAG-22 standard.

The establishment of compliant custody solutions and staking services by regulated providers has further facilitated institutional adoption. Institutions are growing increasingly comfortable holding SOL tokens directly or through regulated financial products, accelerating Solana’s overall adoption trajectory. The network's improved reliability is supported by faster client adoption cycles, with time to supermajority adoption dropping from 250 days to 200 days, and the growing adoption of Frankendancer clients reaching 9% of total stake in July 2025, demonstrating institutional confidence in Solana's evolving infrastructure.

Institutional staking on Solana is set for further growth, driven by continuous innovation, ecosystem expansion, and increasing regulatory clarity, making it a strategically advantageous environment for forward-looking institutions. Additionally, DoubleZero has garnered 16.04% of Solana Mainnet stake on its private fiber network with mainnet launch approaching, indicating continued institutional infrastructure investment in the ecosystem. However, institutions must now factor in emerging slashing risks as Solana transitions from its historical "social slashing" model to programmatic enforcement. The upcoming activation of SIMD-0204: Slashable Event Verification introduces automated onchain penalties for validator misbehavior, initially targeting duplicate block production violations. While slashing events are expected to be rare, as demonstrated by other PoS networks like Ethereum, where less than 0.05% of validators have been slashed, institutional stakers should evaluate slashing insurance options and validator diversification strategies. The proposed penalty structure includes a tolerance buffer below the Nakamoto Coefficient line (~1% of stake), meaning minor infractions by small validators won't trigger slashing, but correlated failures among larger operators could face significant penalties, incentivizing institutions to distribute stake across diverse, high-quality validators.

Regulatory Tailwinds

A critical factor for institutional staking, especially in the US, is the regulatory climate. In early 2023, uncertainty peaked when the SEC cracked down on certain exchange-based staking programs (Kraken, for example, was fined and forced to halt its US staking service, citing securities law concerns). This uncertainty drove some US provider interest in offshore or non-custodial solutions. However, recent developments signal improving clarity in the US, providing tailwinds for many institutional staking providers to return to or open subsidiaries in the US market.

SEC Staking Guidance and ETF Developments: In a much-anticipated move, the SEC's Division of Corporation Finance issued guidance on May 29, 2025 clarifying that "not all staking is a securities offering," drawing a firm line between direct protocol staking versus certain "staking-as-a-service" models where users retain control of their assets and keys versus programs involving third-party custody, pooling, or guaranteed yields. This guidance is a clear positive signal for institution-focused providers offering non-custodial infrastructure where the institution delegates stake without giving up ownership of tokens. This regulatory clarity proved pivotal for August 2025 developments, as liquid staking tokens, particularly JitoSOL, became the cornerstone of Solana ETF proposals from seven major asset managers, including Grayscale, VanEck, Fidelity, and Bitwise. Following additional SEC guidance in early August stating that liquid staking tokens like JitoSOL and Lido are not considered securities, these firms amended their S-1 filings to incorporate comprehensive frameworks for in-kind creation and redemption processes, staking reward distribution mechanisms, and liquidity management protocols, with JitoSOL emerging as the preferred solution due to its fast liquidity and alignment with T+1 settlement requirements. Anchorage Digital now provides full mint and redemption support for JitoSOL, while Jito Labs continues active lobbying efforts with the SEC. With the primary regulatory hurdles around staking integration substantially addressed through the liquid staking token model, market observers anticipate potential SEC decisions on these Solana ETF applications by late August or September 2025. With the primary regulatory hurdles around staking integration substantially addressed through the liquid staking token model, the SEC has delayed final decisions on Solana ETF applications to October 16, 2025, the maximum review period allowed by law. No approvals have been granted thus far, though market observers maintain high expectations for potential approval at the final deadline. Operationally, Anchorage Digital's full minting and redemption support for JitoSOL has strengthened the infrastructure foundation, while Jito Labs and other industry players continue their active lobbying efforts with the SEC.

SEC Chair Atkins on DeFi: Embracing Innovation with Guardrails: At a June 9th, 2025, roundtable, SEC Chair Paul S. Atkins framed decentralized finance as aligned with core American values of economic liberty, private property rights, and innovation, calling blockchain a “peer-to-peer” system redefining ownership and independence of intermediaries. He reiterated that participation in proof‑of‑stake networks, as validators, or via non-custodial staking services, falls outside the scope of federal securities laws, though he emphasized that this clarity stems only from staff guidance, not binding rulemaking. Looking ahead, Atkins said he’s directed SEC staff to draft what he termed an “innovation exemption” or similar regulatory relief to foster DeFi growth, potentially allowing builders and protocols to operate with fewer compliance hurdles, provided intermediaries don’t emerge disguised as decentralized actors. Notably, he underscored that self-custody is a constitutional right “foundational American value” and stressed that developers shouldn’t be held liable solely for the onchain behavior of end-users. His remarks signal a shift from enforcement-first to clarity and guidance, paving the way for rule-based frameworks that balance innovation and investor protection.

Congressional Proposals and State Initiatives: The CLARITY Act passed the US House of Representatives by a bipartisan vote in July 2025, cementing that node operators and validators do not qualify as broker-dealers or investment contract issuers. The bill would hand policing power of the crypto sector to the Commodity Futures Trading Commission and now moves to the Senate, where significant amendments are possible. The Senate Banking Committee has introduced its own discussion draft called the "Responsible Financial Innovation Act of 2025", indicating continued momentum toward accommodating blockchain infrastructure within regulatory frameworks. Meanwhile, jurisdictions like Wyoming and New York have explored bespoke charters or guidance for digital asset custodians and staking services, aiming to attract these activities into a regulated environment.

Institutional Demand for Compliance: US institutional investors have signaled that regulatory clarity is a precondition for their participation in staking. Now, with the SEC explicitly validating direct protocol staking and various agencies recognizing that staking can be done in a compliant manner, these institutions are more comfortable engaging. We are seeing US-based custodians and fintech firms launching staking offerings. For instance, Anchorage Digital, a US federally chartered crypto bank, offers staking for custody clients.

International Regulatory Developments: Global regulatory developments in 2025 have created unprecedented clarity for institutional staking providers across major jurisdictions. The European Union's Markets in Crypto-Assets (MiCA) regulation, which came into full effect on December 30, 2024, has established the world's most comprehensive framework for crypto asset service providers, including specific provisions for staking services and liquid staking tokens, with pan-European passporting rights allowing firms authorized in one member state to operate across all 27 countries. The UK has taken a more targeted approach, removing "qualifying cryptoasset staking" from collective investment scheme regulations in January 2025 and designating it as a standalone regulated activity in April 2025, requiring FCA authorization for firms that pool or delegate customer tokens for staking. In Asia-Pacific, Singapore and Hong Kong continue leading regulatory developments, with Hong Kong's SFC issuing guidance in April 2025 allowing licensed platforms to offer crypto staking under strict conditions, while Singapore has issued over 30 Major Payment Institution licenses tied to stablecoin operations. Australia announced new mandatory licensing requirements for digital asset platforms in March 2025, with the Australian Tax Office treating staking rewards as ordinary income and updated AML/CTF rules taking effect in March 2026. The regulatory clarity has particularly benefited traditional banks, as European banks are planning comprehensive crypto service offerings by 2026, including protocol staking support, where banks can facilitate staking operations and retain portions of generated rewards, while the US rescission of Staff Accounting Bulletin 121 and withdrawal of restrictive federal banking guidance has removed major barriers to bank participation in crypto custody and staking services. These developments create a competitive dynamic where jurisdictions with clear frameworks like the EU, UK, Singapore, and Hong Kong are attracting crypto capital and innovation, while traditional banks can now offer compliant staking services, significantly expanding institutional participation and legitimizing the global staking ecosystem.

In summary, global shifts in regulation are creating a more hospitable environment for staking businesses. Providers can now expand in the US market with greater confidence, and institutions can stake onshore rather than routing through overseas platforms. The result is likely to be increased institutional staking activity in the coming years, benefiting compliant providers.

Risks

Despite positive regulatory developments providing tailwinds, institutions must remain cognizant of the inherent risks associated with staking, which range from regulatory uncertainties to technical vulnerabilities.

Regulatory Changes: Regulatory clarity, while currently improving, remains fluid. Regulatory bodies may introduce new guidelines or shift stances, potentially imposing additional compliance burdens or restricting certain staking models. Institutions should closely monitor ongoing developments, as sudden regulatory shifts could render current operational practices non-compliant or necessitate costly infrastructure adjustments.

Smart Contract and Slashing Risks: Decentralized staking protocols, especially those employing liquid staking and restaking models, inherently carry smart contract risks due to vulnerabilities or exploits that could lead to substantial losses. Furthermore, slashing events, in which validators lose staked assets due to downtime, malicious behavior, or technical issues, pose a significant threat. The September 2025 Kiln API exploit that resulted in $41M in stolen SOL from SwissBorg users demonstrates how security vulnerabilities in staking infrastructure can lead to direct asset loss. Additionally, a September 2025 NPM supply chain attack that targeted crypto wallets through compromised JavaScript packages highlights how infrastructure dependencies can create unexpected attack vectors for staking operations. Institutions must rigorously assess smart contract audits, provider insurance policies, and operator performance metrics to mitigate these risks.

Fee Compression and Profitability: Increasing competition among staking providers is leading to fee compression. Providers competing for institutional clients frequently offer reduced rates, impacting their profitability margins. Continuous downward pressure on fees could lead providers to cut corners in terms of security, governance support, or customer service, inadvertently increasing operational risks for institutions reliant on these services.

Market Concentration and Centralization: A handful of large staking providers dominate significant portions of staked assets, particularly in liquid staking solutions like Lido. Such centralization introduces systemic risks, including reduced resilience against targeted attacks, governance centralization, and increased potential regulatory scrutiny. Diversification across multiple staking providers or leveraging decentralized staking solutions could mitigate some concentration risks.

Counterparty and Custody Risk: Institutions often rely on third-party custodians or staking providers that manage nodes without direct asset custody. While this mitigates some risk, reliance on intermediaries introduces counterparty risk. Failures, security breaches, or mismanagement at the provider or custodian level could jeopardize asset security or yield stability. Thorough vetting and employing provider insurance coverage can reduce these risks.

Liquidity Risks in Liquid Staking: Liquid staking solutions provide tokenized derivatives to maintain liquidity. However, these tokens may face liquidity risks, particularly under stressed market conditions. Reduced liquidity or market volatility could lead to unfavorable pricing, limiting institutions' ability to efficiently enter or exit positions. Institutions should evaluate market depth, trading volumes, and secondary market activity for tokenized staking assets to manage liquidity risk effectively.

ReStaking Complexity and Protocol Dependency: ReStaking, an innovative approach enhancing yield through additional participation in middleware networks, introduces layers of complexity. Institutions employing ReStaking must navigate increased dependencies, potential protocol incompatibilities, and amplified slashing risks. Effective risk management strategies, including rigorous protocol assessment, continuous monitoring, and strong governance participation, are essential to mitigate these complexities.

Addressing these multifaceted risks proactively through diligent monitoring, diversified staking strategies, rigorous provider selection, and comprehensive insurance coverage is critical for institutional stakeholders aiming to sustainably benefit from the evolving staking landscape.

Conclusion

The institutional crypto staking arena is robust and growing, with clear momentum from both a market and regulatory perspective. Global staked asset value is at record levels and climbing, especially as institutions continue to seek yield generation opportunities and networks continue to architect or migrate to Proof-of-Stake. The US market, previously cautious, is opening up due to regulatory clarity following the SEC's May 2025 guidance clarifying that direct protocol staking falls outside securities laws, the bipartisan CLARITY Act passage, and Chair Atkins' pro-innovation stance, presenting new opportunities for providers to operate onshore and for American institutions to participate confidently.

Successful institutional staking programs require partnerships with providers who combine regulatory compliance, operational excellence, and institutional grade security. While fee compression pressures persist industry-wide, institutions increasingly recognize that security, mature tech stack, and comprehensive risk management outweigh cost considerations for large-scale deployments. As the market matures toward stricter institutional standards and potential consolidation, early-moving institutions that partner with proven, global providers will be best positioned to benefit from regulatory clarity while maintaining the security and compliance standards their stakeholders demand.

We see a competitive but collaborative landscape, with a handful of large providers leading on scale, while numerous specialized players carve out niches. As competition drives innovation, institutions stand to benefit from better service, lower fees, and more product options. The coming years will likely see further institutionalization of staking, with stricter standards and possibly consolidation, while the current diversity of players is a sign of a vibrant and maturing sector. Stakeholders drafting strategies in this space should monitor both market share shifts and value propositions of providers to make informed decisions about partners and investments in the staking ecosystem.

This research report has been funded by Blockdaemon Inc.. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Blockdaemon Inc.. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek the advice of a qualified financial advisor before making any investment decisions.