This research report has been funded by Morpho. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Morpho. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

Morpho: Evolving into Permissionless Lending Infrastructure

Key Takeaways

- Morpho introduces “aggregated” lending architecture that enables permissionless market creation and modular vault curation, while also shifting risk management away from slow-moving DAO consensus and instead towards vault curators with pertinent expertise.

- Growth of deposits has been incredibly strong, having reached $1 billion total deposits in under 5 months and up to $4 billion today. Pioneered the curator model and risk curators have quickly adopted Morpho Vaults; competing lending protocols have introduced similar modular/aggregated lending designs in tow.

- Ecosystem expansion and product integrations are focal points of the growth strategy going forward. Spark, Moonwell, and others have begun to create revenue-generating vault offerings that directly improve product experience for their users.

Challenges of Monolithic Lending

Morpho emerged in 2022, initially developing Morpho Optimizers as an innovative optimization layer to enhance the capital efficiency of existing lending platforms like Aave and Compound. By creating a peer-to-peer layer atop these protocols, Morpho introduced a mechanism that directly matched lenders and borrowers, thereby improving interest rates while maintaining the underlying protocols' liquidity and risk parameters. Morpho Optimizers’ unique design ensured users could benefit from two potential rate structures: in the worst case, they received the standard APY of the underlying pool, and when successfully matched, they accessed an improved peer-to-peer rate. This approach guaranteed that users always received an interest rate equal to or better than the original protocol's offering. However, the growth potential of Morpho Optimizers were ultimately constrained by the limitations of existing lending pool designs.

The existing DAO-based lending protocols face significant challenges in risk management that fundamentally limit their effectiveness in rapidly evolving, permissionless markets. These protocols struggle with the immense complexity of managing risk parameters, in some cases needing to monitor and update over 500 parameters in near real-time, with complexity increasing exponentially as more markets and features are introduced. The inherent structural weakness of DAOs lies in their governance model, where token holders—who are typically not risk management experts—are responsible for critical decisions, often deferring to external consultants and approving proposals with minimal scrutiny. This approach introduces substantial risks, including potential conflicts of interest between risk management firms, token holders, and end users, while simultaneously creating a consensus mechanism that significantly slows down critical risk adjustment processes. Recognizing these fundamental limitations, Morpho strategically pivoted to develop a novel, trustless lending primitive designed to address these systemic inefficiencies and provide a more scalable, efficient approach to decentralized lending infrastructure.

A New Lending Primitive

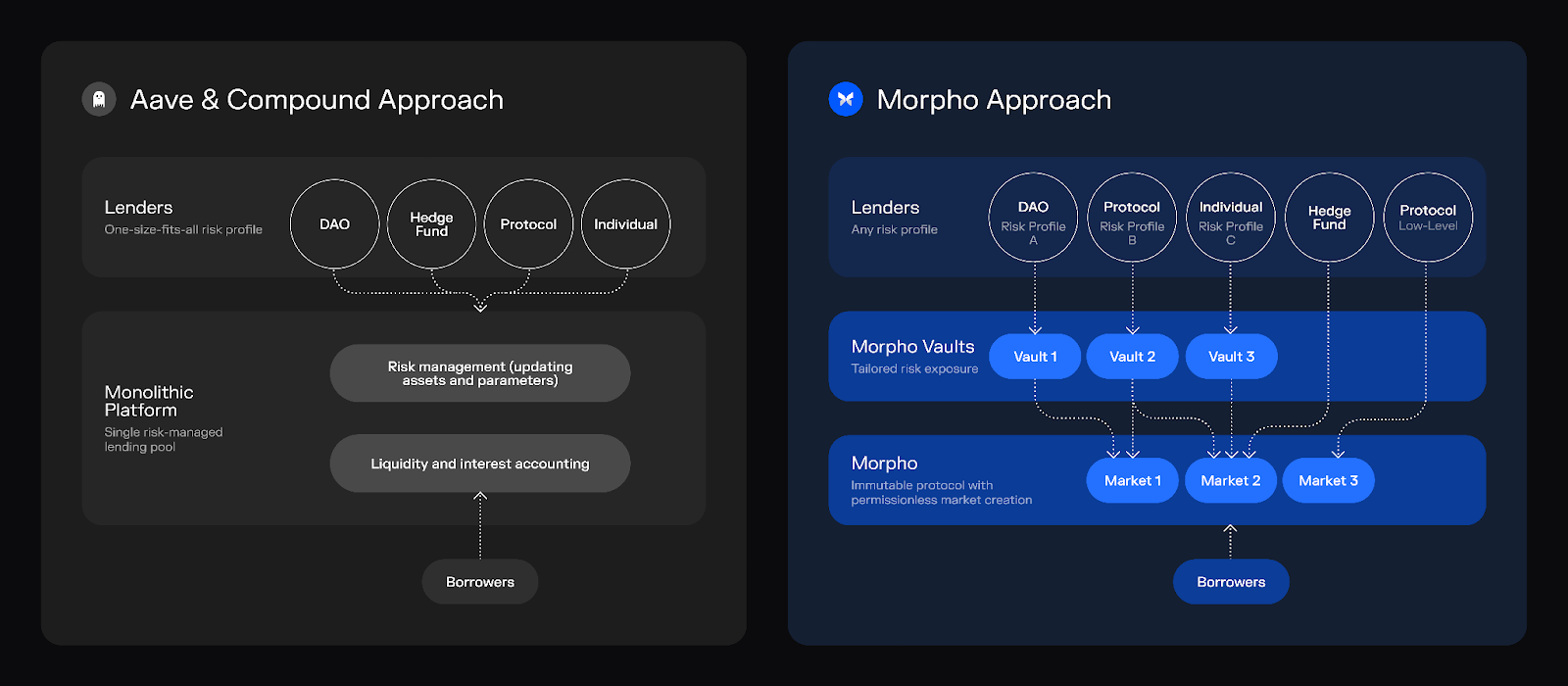

The search for an entirely new lending primitive led to the creation of the Morpho protocol (previously Morpho Blue). The Morpho protocol is a trustless lending primitive with permissionless market creation. Unlike the monolithic approaches of existing platforms like Aave or Compound, which feature unified lending pools and centralized risk management, Morpho introduces an innovative "aggregated" design that allows for modular market creation while maintaining a shared core lending market primitive.

The protocol enables users to deploy minimal, isolated lending markets by specifying parameters such as loan and collateral assets, liquidation loan-to-value (LLTV) ratios, and oracles; LLTV and interest rate model (IRM) options are defined via whitelisting through Morpho Governance. This architectural approach provides several key advantages: the protocol remains immutable, Morpho Governance cannot interfere with deployed markets, and risk managers can design pools with optimized rates and higher LLTVs without complex multi-asset risk considerations that affect all users of the protocol. By facilitating permissionless market creation with isolated pools, Morpho significantly expands the potential scale and diversity of lending use cases, offering a more granular and adaptable approach that addresses many limitations of existing lending protocols.

Monolithic lending vs. Morpho’s aggregated lending approach | Source: Morpho

Modular Lending Vaults

Building upon the foundational Morpho protocol lending layer, Morpho Vaults were designed to offer users a sophisticated and flexible approach to passive liquidity provision. Each vault, designed to support a single loan asset, allows Vault Curators to allocate deposits across multiple Morpho markets while maintaining full liquidity and transparency, enabling withdrawals at any time and providing visibility into the vault's current state.

The protocol introduces a nuanced vault management model where anyone can create and own a vault, with the ability to assign critical operational roles including a Curator (who sets market bounds and supply caps with a mandatory 24-hour to one-week timelock), a Guardian (with power to revoke pending actions), and Allocators (responsible for continuous market rebalancing to optimize yield). Critically, these vaults operate independently of Morpho protocol governance, allowing vault owners to set their own performance fees while maintaining a noncustodial structure that empowers risk protocols and experts to serve users directly—a more scalable and user-aligned business model that represents a significant evolution from traditional DAO-based consulting approaches. This design not only provides flexibility for users to engage with lending markets according to their individual risk appetites but also creates a more dynamic and scalable business model for Morpho.

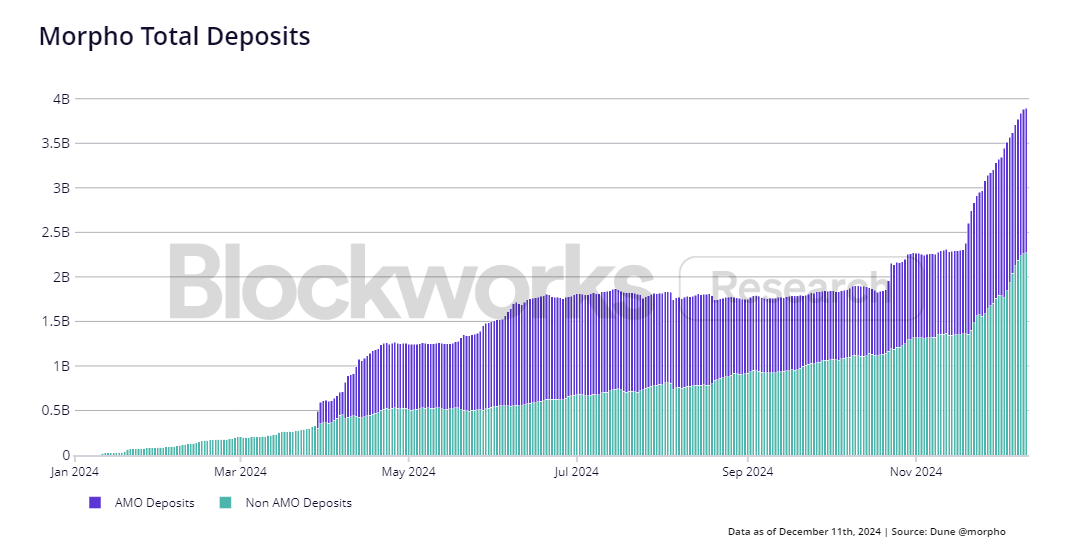

The growth of Morpho has been incredibly strong, with total deposits on the platform reaching nearly $4 Billion in under a year. Algorithmic Market Operations (AMOs), typically used by stablecoins like DAI or FRAX to manage stability, account for roughly half of the deposit volume today and have seen several brief, sharp increases, while non-AMO deposits have been on a steady upward trend since the beginning of the year.

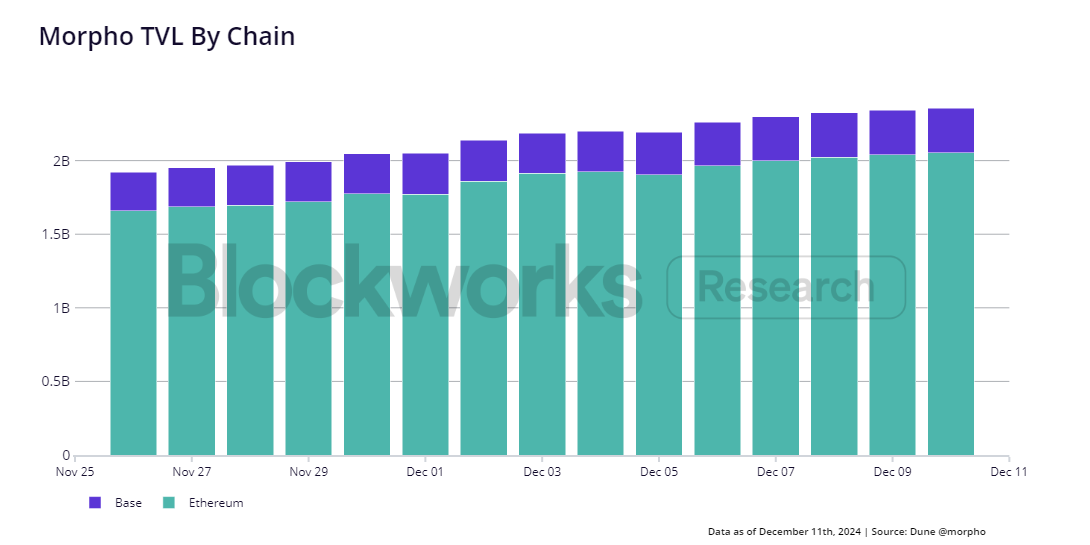

Morpho is currently live on both Ethereum mainnet and Base with nearly 90% of TVL coming from the mainnet deployment. This relationship is not surprising given the ETH L1’s general stickiness of capital and dominance of total DeFi TVL over the past few years even as more transactionally active chains, such as Solana and Base, have begun to gain traction.

DAO Governance

Morpho's governance model is deliberately designed to be minimal and strategic, focusing primarily on providing core infrastructure features for the lending primitive rather than engaging in extensive market management. The key responsibilities of governance are limited to introducing new loan-to-value (LLTV) thresholds and interest rate models that can be selected when creating markets. Although a fee switch exists within the Morpho markets protocol—currently disabled—it represents a potential future revenue mechanism that could allow the DAO to earn a percentage of interest generated across markets. The recent enablement of on-chain governance and MORPHO token transferability on November 21st marks a significant milestone, with current DAO discussions predominantly centered on growth strategies, including token reward structures and grant programs. As with other prominent DAOs, the future trajectory of Morpho's governance will be critically dependent on its ability to effectively balance growth initiatives, potential revenue capture, and judicious management of its treasury resources.

Risk Curator Adoption

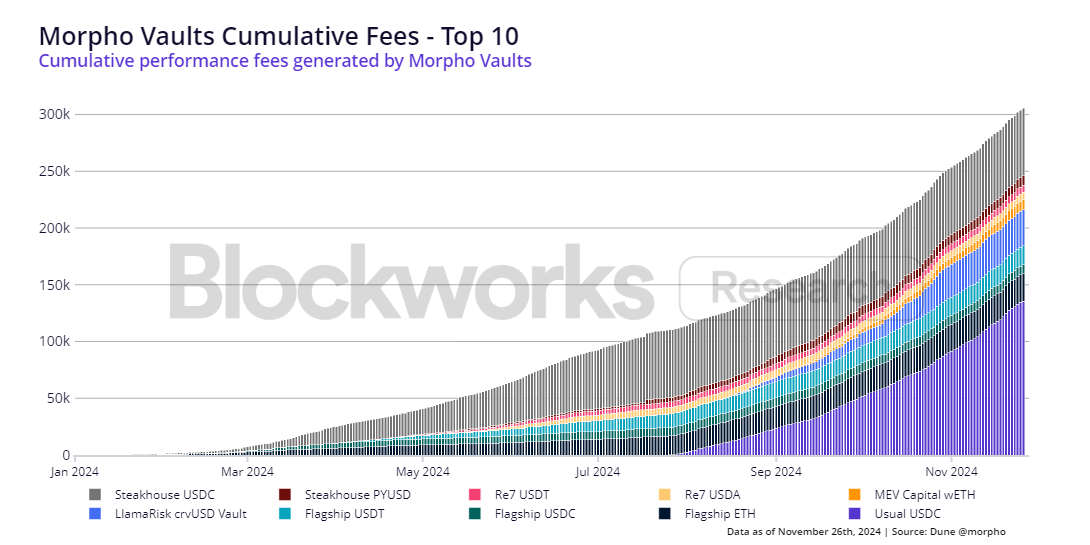

Morpho Vaults have been designed with risk management experts in mind, and prominent DeFi risk advisory teams, such as Gauntlet and Steakhouse, and investment firms with a focus on DeFi risk management, like MEV Capital and RE7 Labs, have quickly flocked to the platform and begun to design various vaults. In general, many of these teams have put together an array of vaults across a variety of assets.

On Ethereum mainnet, and looking at Gauntlet as an example, they have created vaults for WETH, Bitcoin assets such as WBTC and cbBTC, and several USD stablecoins including USDC and USDT, among others. For some key assets, USDC for example, Gauntlet has begun to create multiple vaults with varied risk profiles. The Gauntlet USDC Prime and Gauntlet USDC Core vaults are an example of this: the ‘Prime’ vault has a stated goal to optimize for risk-adjusted yield across “large market cap and high liquidity collateral markets” with WBTC, cbBTC, and wstETH making up the collateral mix and a current base rate of 9.06% APY, while the ‘Core’ vault is targeting a higher level of risk and incorporates a wide variety of higher yielding collateral assets such as USD0++, sUSDe, MKR, tBTC, etc., with a base rate of 13.3%.

Gauntlet has outlined the key components of their methodology for risk management and vault curation on Morpho. In terms of individual vault composition, they assert that market allocation is the dominant factor in their modeling. Allocations are influenced by risk factors including DEX liquidity, volatility, slippage, audits, and oracles. Naturally, vault allocation targets are constantly shifting as markets are always changing, and risk curators must continuously optimize for an appropriate risk-adjusted yield in line with a given vault’s goals.

Despite a high number of liquid vaults for the same supply assets (e.g. USDC, WETH), it does not appear that the market has yet converged on any standard performance fee rates for vaults. Gauntlet’s vault fees currently span 0, 5, and 10%, several of Steakhouse’s largest vaults currently have fees set to 0, while RE7 Labs has their Re7 WETH vault charging 20% of earned yield. It appears that supply growth may be a short term goal for some - Steakhouse’s USDC vault for example was initially the highest fee earning vault for several months until around August. Around that same time, supply in the Steakhouse USDC vault began to flatline and drop off, indicating that dropping fees to 0 may have been motivated by the desire for continued supply growth.

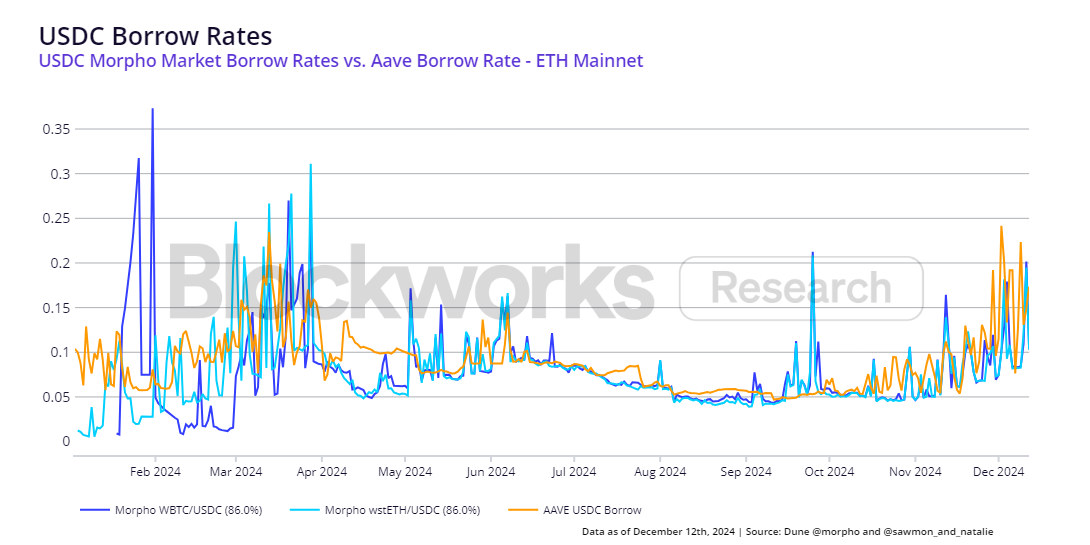

Below we compare average borrow and lend rates for some key assets across Morpho and Aave markets on Ethereum. Due to the variety of isolated markets on Morpho, we compare the borrow rates of the largest Morpho Markets with blue-chip collateral assets to the borrow rates available on Aave. For USDC, we find that these largest markets tend to track quite closely with the available borrow rates on Aave, only with a slightly higher apparent degree of volatility.

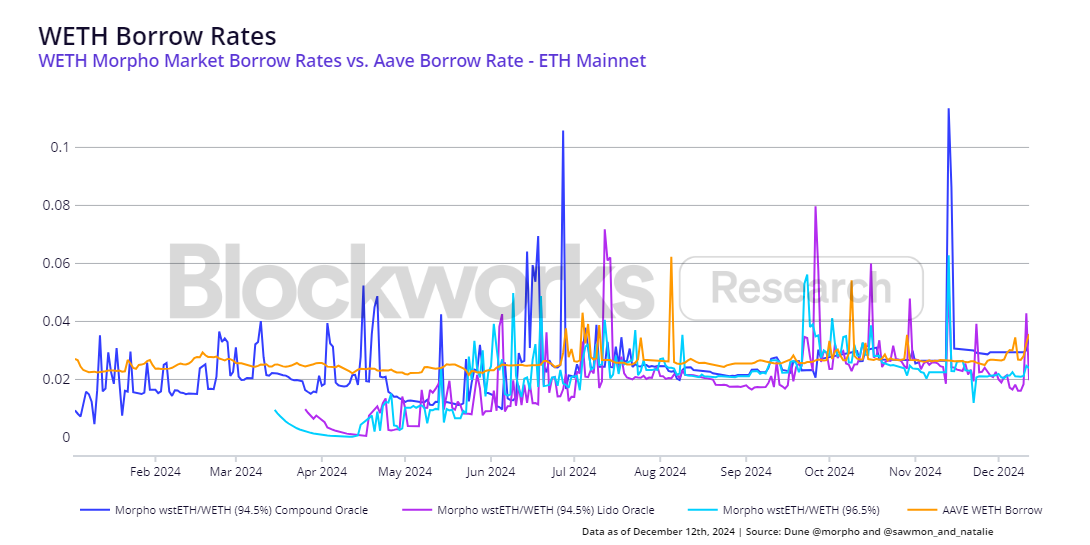

We find the same general trend for the WETH markets as well. Given the collateral assets explored here (WBTC, wstETH) also make up a significant portion of Aave collateral (roughly $9B of $17.8B total supply), it does not come as a surprise that borrow rates for these particular markets would end up fairly similar. In the case of individual Morpho Markets, their volatility and relative rates should naturally evolve as perceived risk of the individual collateral assets change - whereas for Aave this type of effect from a single asset should be muted due to the unified lending pool design.

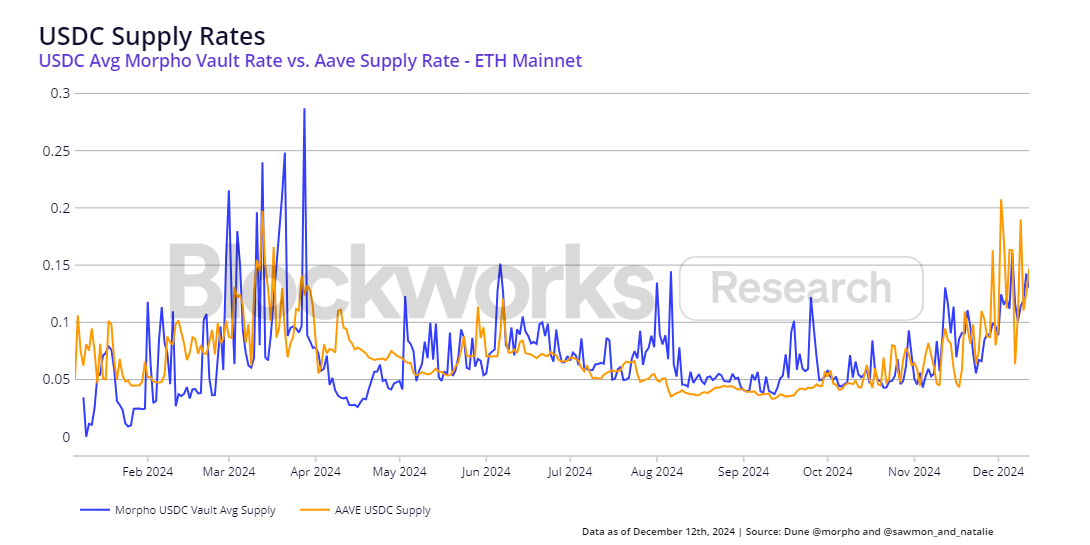

On the supply side, we compare instead the average supply rates provided across Morpho Vaults relative to their Aave counterparts for a given asset. In this case, average vault supply rates relative to the Aave supply rate for USDC have generally tended to stay within the same ballpark outside of a few brief periods of rate divergence.

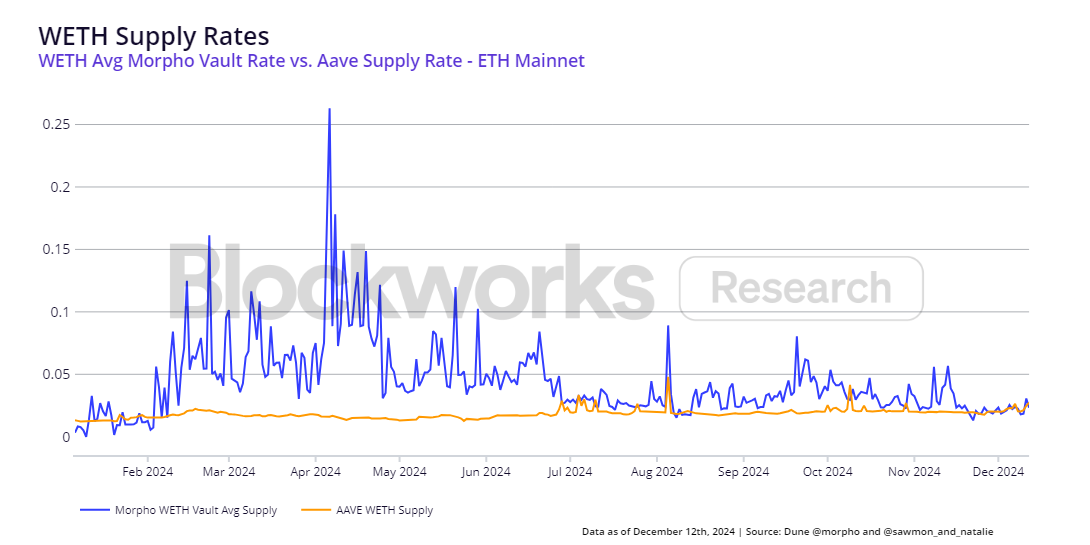

WETH Vaults, on the other hand, have on average offered significantly higher supply rates than that of Aave up until recently. This appears to be largely driven by two vaults - Gauntlet WETH Core and Re7 WETH - which from February to July were offering significantly elevated supply rates, as much as 4 to 5 times higher at their peak, relative to the other WETH Vault offerings which have generally tracked closely with the Aave supply rate.

These higher rates were likely driven by allocations to higher risk collateral assets. This becomes clearer when comparing the Gauntlet WETH Core and Gauntlet WETH Prime vault collateral allocations. The Gauntlet WETH Prime vault, the supply rate of which has generally tracked the Aave WETH supply rate, is today largely allocated to blue-chip collateral such as wstETH and WBTC. The Gauntlet WETH Core vault, which historically has seen hugely elevated supply rates relative to other WETH vaults and markets, has whitelisted a long list of collateral assets and its current allocation spans a variety of liquid staking and restaking assets including: rsETH, ezETH, weETH, ETH+, among others. This variation in vault supply rates and relative risk showcases the value of the Morpho Vault product which enables both Vault Curators and Depositors to make explicit risk-adjusted tradeoffs in terms of how vaults are designed and in choosing where to deposit assets.

Case Studies

Sky’s (formerly Maker) SparkDAO has deployed its own Morpho vault, strategically allocating DAI to create a unique lending protocol with a simplified development effort. Curated by SparkDAO, this vault is designed to seamlessly allocate DAI liquidity from Sky to Morpho via Spark. The Spark Liquidity Layer (SLL) automates liquidity provision across blockchain networks and DeFi protocols, currently supporting platforms like SparkLend, Aave, and Morpho, and enabling users to earn the Sky Savings Rate of 12.5%. The Spark DAI Morpho vault has emerged as a top-performing revenue generator for Sky, currently managing $750M of the $2.34B liquidity layer and bringing in an APY of around 15% in recent weeks.

Moonwell Finance has also integrated a Morpho Vault product into their existing multichain lending platform. Moonwell are able to easily spin up new products via this Morpho integration, and have thus far created three flagship vaults on Base for ETH, USDC, and EURC, respectively, with support from Block Analitica and B. Protocol for curation and asset allocation. The integration offers a seamless user experience, allowing participants to earn both Moonwell and Morpho rewards directly through the Moonwell platform without the need to interact directly with Morpho. Moonwell is currently incentivizing these vaults with additional $WELL rewards, though even if we exclude this the current rates on the ETH and EURC vaults are more favorable than the regular lending rates for these assets on Base on Moonwell. Lastly, with performance fees set at 15%, Moonwell DAO has an effective means to scale revenues via growth of vault usage. Short term incentivization via $WELL rewards could lead to a sticky base of deposits for continuous revenues, and curation of additional vaults could drive further deposits.

Risks

The potential rapid expansion of Morpho vaults may present a nuanced challenge for the platform, as an introduction of many similar vaults could make it difficult to properly delineate the risk/reward for users, or simply introduce confusion for Morpho front-end users (i.e. 20 USDC vaults with similar yield and collateral assets). Further, the risks of slow-moving consensus to manage risk for large DAO-based lending protocols may be in the process of getting *simplified and automated *thanks to improved oracles and algorithms. On the other hand, long-term adoption of Morpho may skew towards platforms, protocols, and businesses utilizing Morpho markets and vaults on the backend to build their own products. In this scenario, Morpho becomes backend technology that users unknowingly benefit from when interacting with their favorite lending or other application, rather than selecting vaults directly via the front end.

The emerging modular lending vault design employed by Morpho faces potential competitive pressure from other emerging protocols like Euler and Kamino, both of which are adopting similar architectural approaches in their V2 designs. This convergence is also evident in shared curation strategies, with entities like MEV Capital and RE7 Labs actively exploring multiple platforms, signaling a broader industry trend towards more flexible lending infrastructure. Further, traditional lending leaders like Aave could also potentially copycat the modular design in an attempt to redirect capital flows, however the existing relationship might be more nuanced and potentially symbiotic—Morpho markets leveraging existing liquidity pools and assets could paradoxically enhance the overall metrics and profitability of protocols such as Aave. This dynamic suggests that the future of decentralized lending may be characterized less by winner-take-all competition and more by intricate, interconnected ecosystem developments that create value across multiple platforms.

Final Thoughts

Morpho represents an evolution in decentralized lending infrastructure, offering an alternative to monolithic protocols through its aggregated, trustless market design. As the platform navigates potential challenges, such as competitive pressures from other protocols, its strategic approach and high rate of growth suggests a future where lending platforms may increasingly function as interconnected, specialized infrastructure rather than standalone products. The protocol's innovative governance model, combined with its ability to enable risk curators and protocols to create flexible liquidity solutions, positions Morpho as a potentially transformative technology that could reshape how decentralized lending markets operate. Productized integrations, such as those with Sky/SparkDAO and Moonwell, showcase the value of Morpho’s design and further adoption of this nature will be key to the protocol’s long term success.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.