Hyperliquid: Weekend Price Discovery in 24/7 Markets

Key Takeaways

-

During the four focal crude weekends, Hyperliquid provided continuous off-hours crude price discovery while benchmark futures were closed. In the first shock weekend, CL began repricing at 06:14 UTC, ahead of official strike confirmation while CME remained closed, and by the final pre-open had already bridged roughly 44% of the eventual $7.72 reopen gap. The second shock weekend showed the same pattern at much greater scale: notional rose 21.8x, from $14 million to $305.6 million, while median quoted spreads held near 4.13 bps, as Hyperliquid repriced crude to its +5% weekend ceiling of $95.8 ahead of the benchmark reopen at $106. On both shock weekends, crude finished pressed into the upper weekend bound, so the effective ceiling on further adjustment was the platform’s bounding-band.

-

Crude oil is not the only asset moving 24/7 on Hyperliquid. Across a broader panel of 199 symbol-weekend observations, TradeXYZ’s HIP-3 final pre-open price was closer to the eventual TradFi reopen than Friday’s close in 78.4% of cases, reducing median reopen error from 92.8 to 38.4 basis points and mean absolute reopen error by 51.8%. Directional agreement was 89.9%, and the relationship between Hyperliquid’s implied move and the realized reopen move remained strong, with a slope of 0.816 and an R² of 0.785.

-

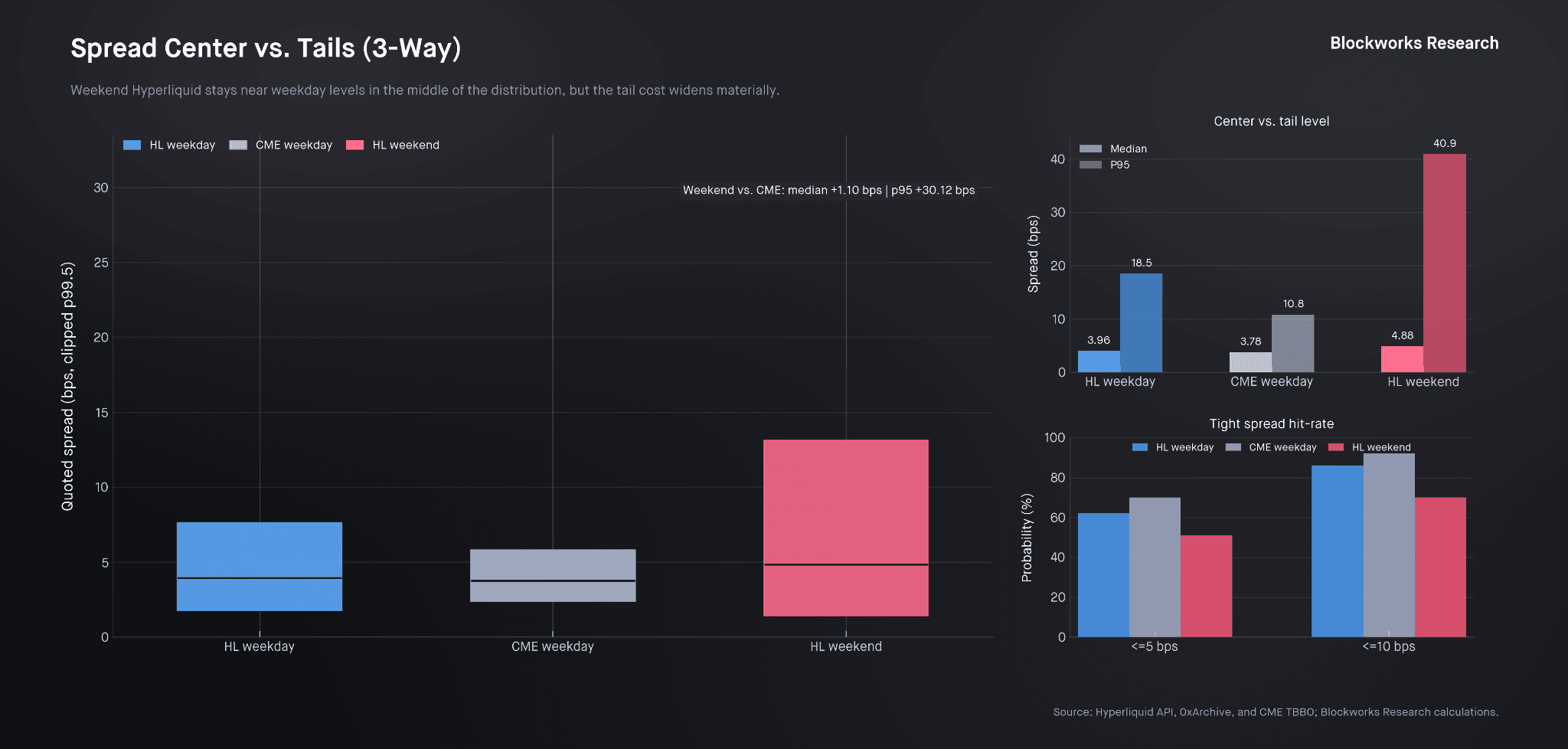

Weekend market quality is functionally resilient in the macro core. Median spreads widen only modestly (3.96 bps to 4.88 bps), while tail execution degrades sharply — 95th percentile spreads more than double (18.5 bps to 40.9 bps) and displayed depth collapses to 33.9% of weekday levels. In high-volume macro markets (CL, XYZ100, EUR, SILVER, GOLD), flow concentration offsets these frictions: 89.7% of trades execute within 10 bps of mid versus 77.7% on weekdays, with notional-weighted slippage improving to 13.05 bps from 16.69 bps.

Bounding bands protect system stability at the cost of price discovery in tail events. TradeXYZ static bands cap weekend manipulation (median exceedance rate: 0% across 40 assets), but in macro shocks CL was pinned at the +5% limit for extended periods both weekends, deferring material adjustment into the reopen window. Bounding Bands v2 enables stepwise discovery: once the oracle reaches 90% of a bound, the reference re-anchors and a new ±5% window opens, allowing unrestricted price discovery.

Introduction

The 2026 Strait of Hormuz conflict triggered the largest oil supply disruption on record, with 14 million barrels per day removed from global markets, more than double the 5.7 mb/d loss during the 2019 Abqaiq-Khurais attack and nearly triple the disruption associated with the 1979 Iranian Revolution. Crude became the market’s primary barometer because the shock initially constrained transport, loading, and export capacity rather than simply destroying upstream production.

With physical delivery uncertain and the duration of the disruption unknown, market participants turned to futures markets to hedge and rebalance exposure. Brent and WTI rallied more than 36% and 39%, respectively, briefly trading above $119 per barrel. ICE Brent alone traded roughly 4.8 million futures and options contracts on March 1, equivalent to approximately 4.8 billion barrel-equivalents, roughly 240 days of normal Hormuz throughput and several hundred paper barrels for every physical barrel removed from the market.

Once CME crude futures closed for the weekend, however, that hedging flow lost access to its main benchmark venue just as the conflict entered its most acute phase. Participants who still needed to cover exposure or adjust positions were forced to wait for a crowded and uncertain Sunday reopen. Hyperliquid remained open throughout the closure window, becoming the only continuously available venue in which real-time oil-linked repricing could continue while traditional futures infrastructure was offline.

Weekend One: First Shock Repricing

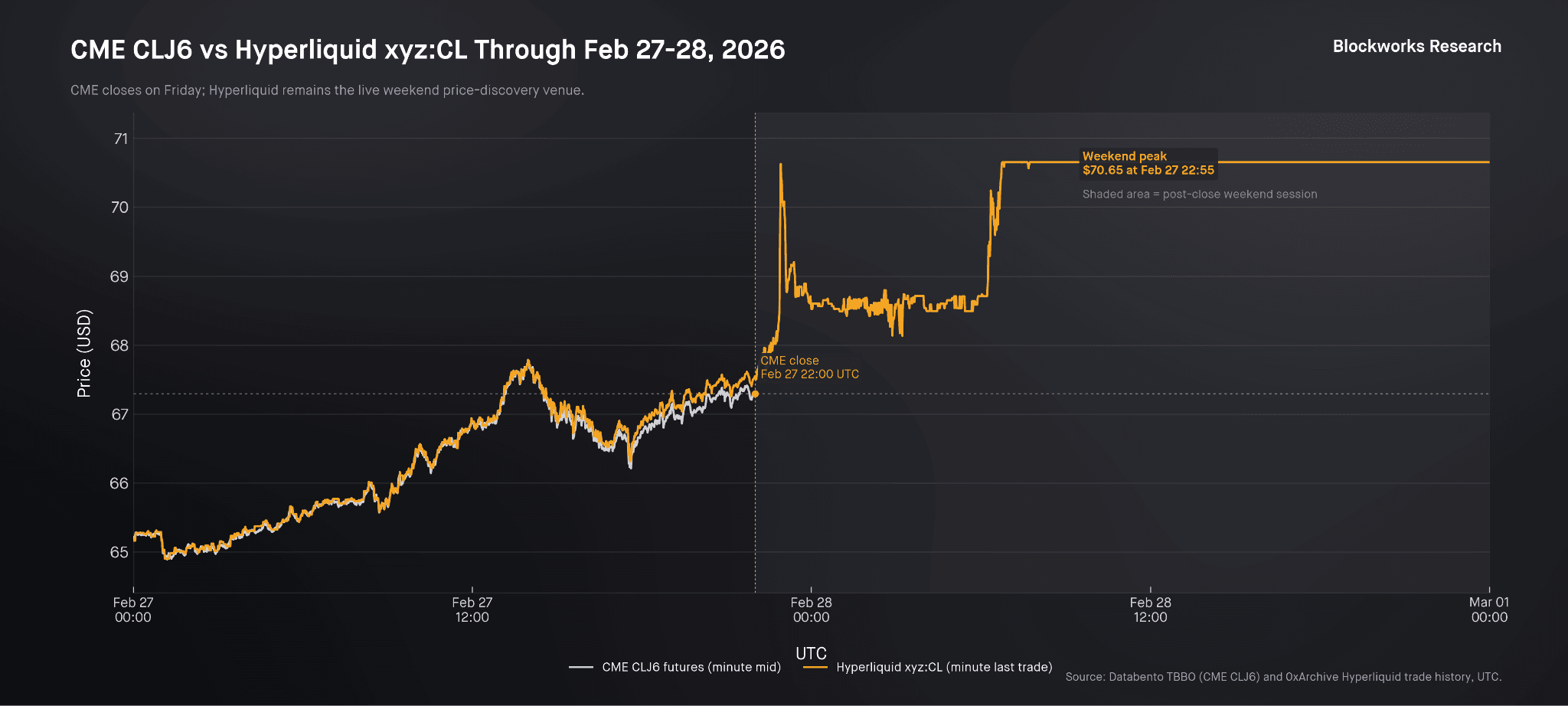

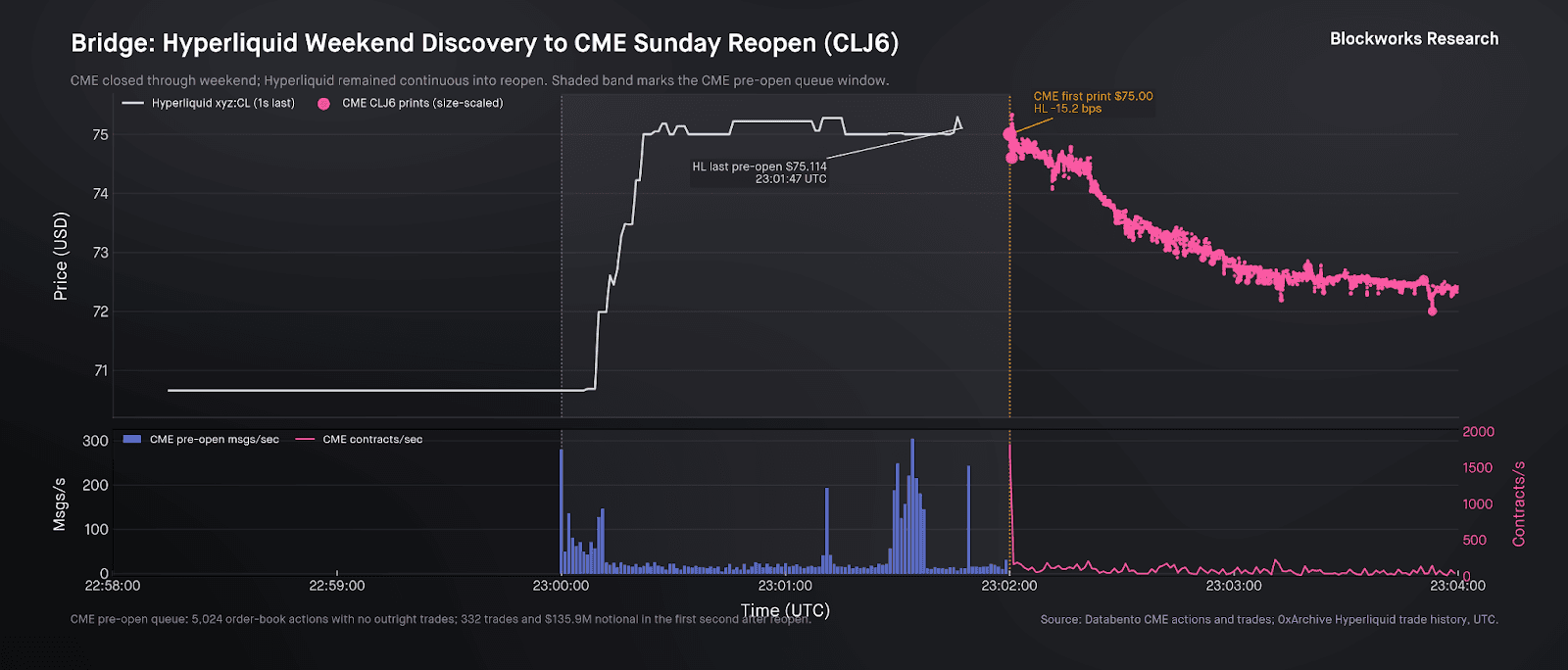

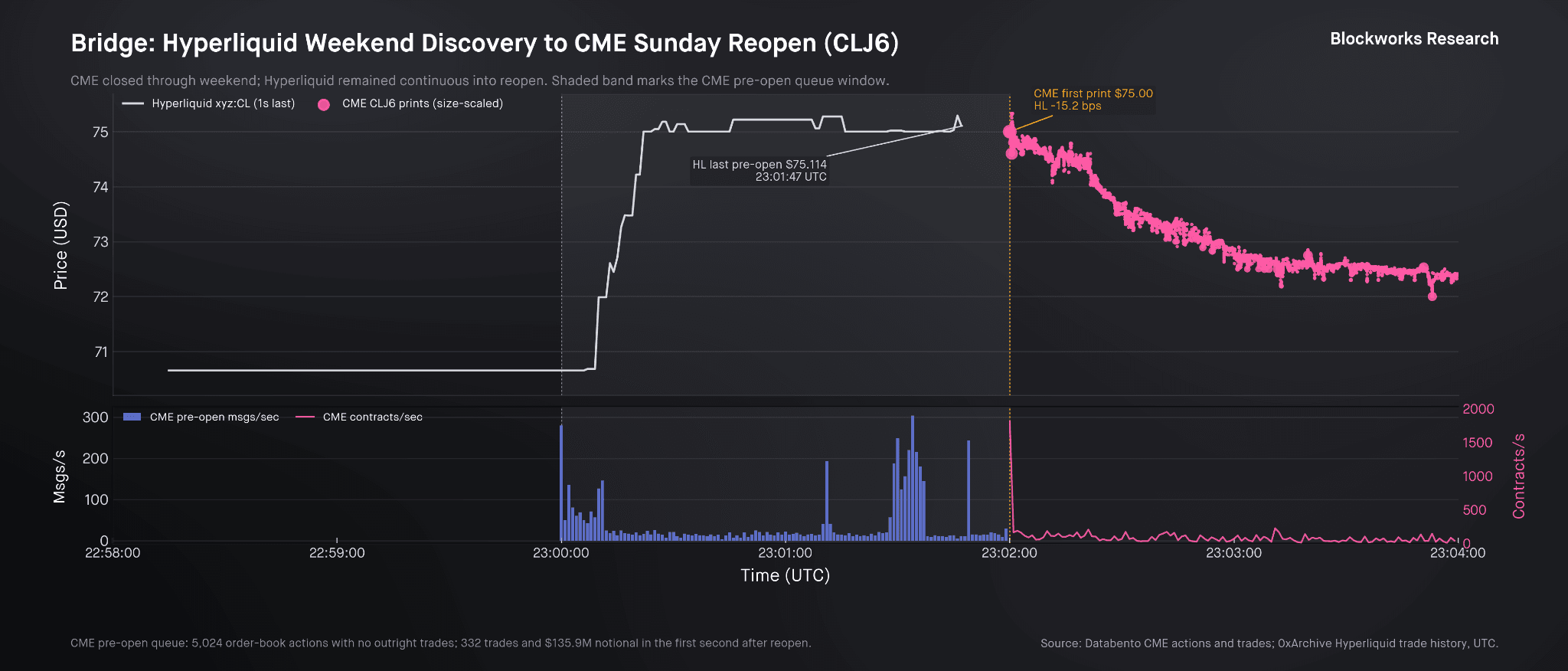

Weekend One (Feb. 27) began with an already elevated CL price, as crude had carried a meaningful geopolitical risk premium into Friday’s close amid deteriorating diplomacy and rising skepticism around a negotiated outcome. The main shock, however, had not yet been fully priced. That changed early Saturday, when public reports of strikes on Iran began to hit while CME crude futures were already closed. Reuters first reported Israel’s pre-emptive attack at 06:29 UTC, and other real-time proxies for information arrival moved sharply in the same window. With benchmark crude futures shut, Hyperliquid became the only continuously open venue through which oil-linked risk could reprice in real time.

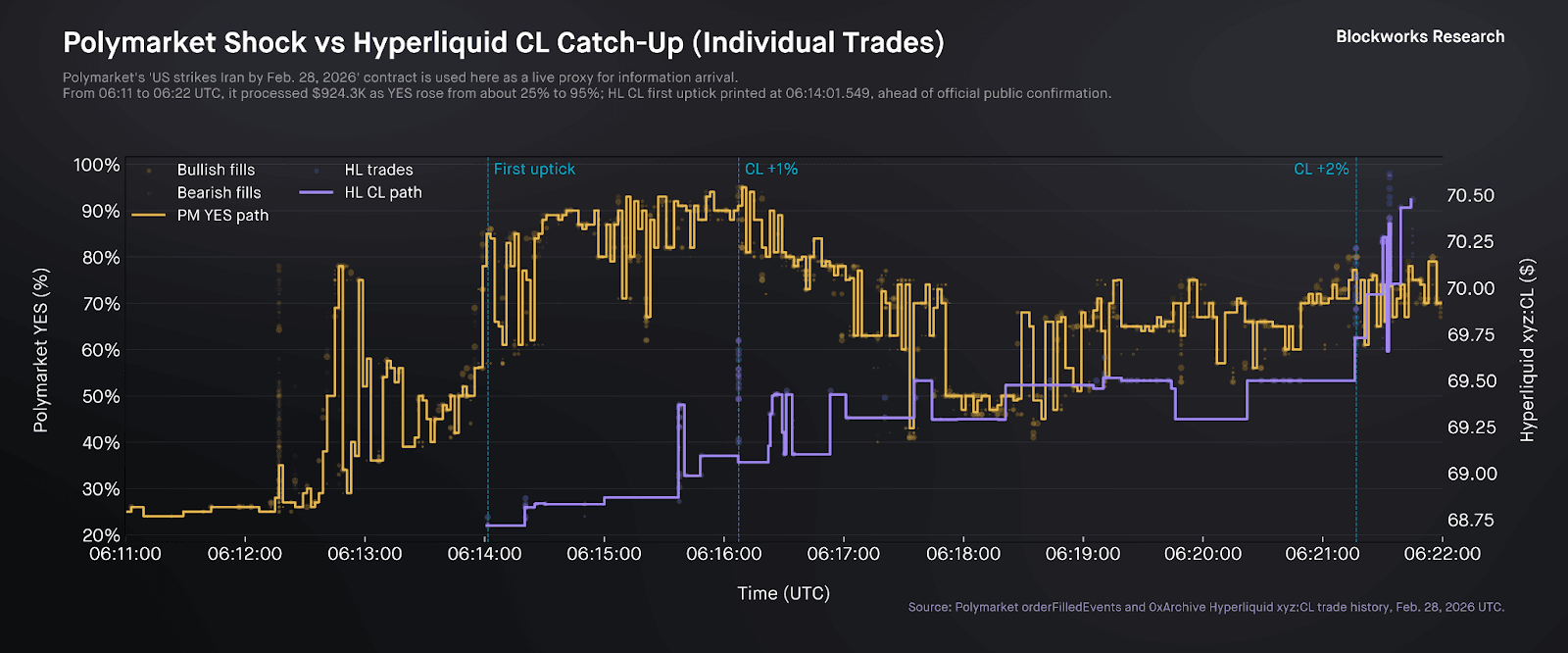

Within minutes of the first information arriving on Polymarket, TradeXYZ had repriced crude oil from its $68.72 baseline to a local high of $70.62, capturing the market's initial shock before traditional venues could even open. Between 06:11 and 06:22 UTC, the prediction market's "US strikes Iran by Feb 28, 2026" contract recorded roughly $924K in notional as the YES price surged from 25% to briefly touch 95%. CL began moving before the first official public confirmation and slightly ahead of the reported 06:15 UTC strike timestamp. By 06:16, the contract had already reached +1%; by 06:21, it crossed +2%, translating raw geopolitical intelligence into live, tradable price discovery while CME remained dark.

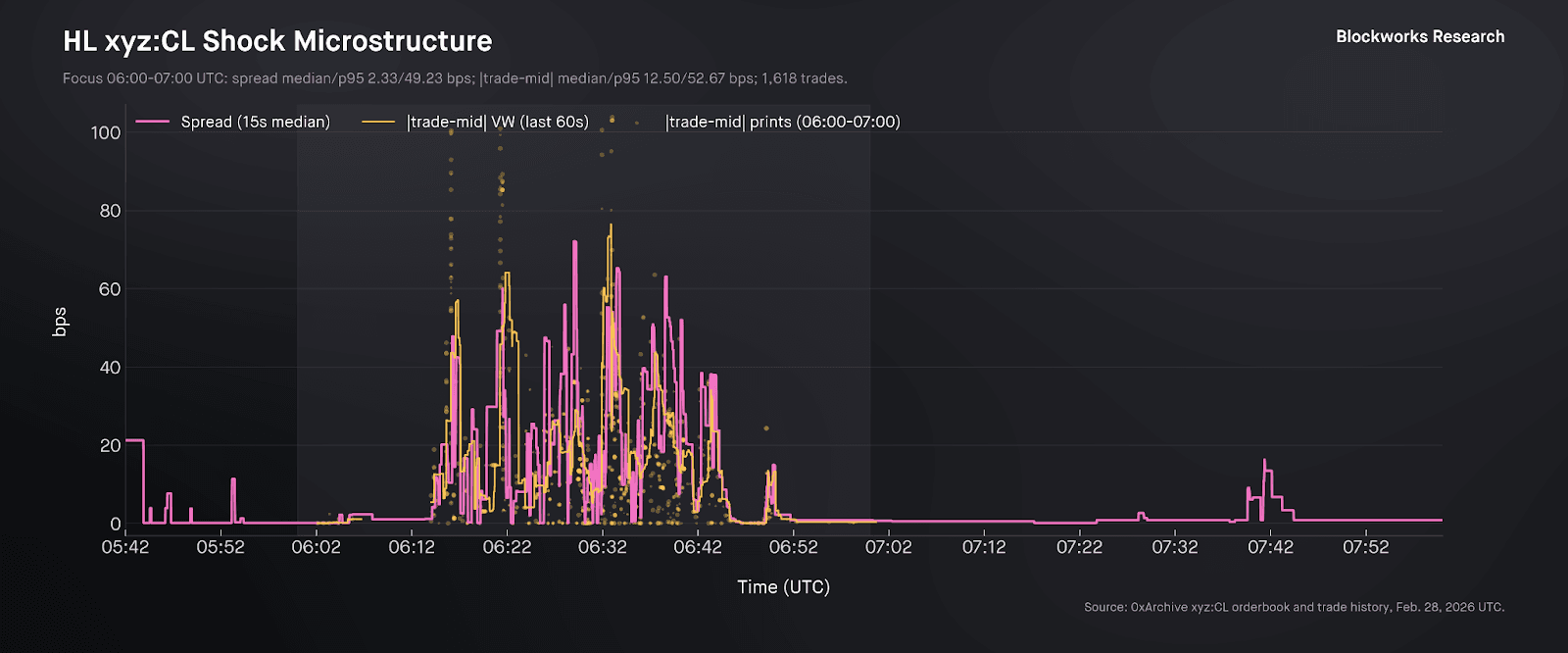

That repricing came with acute microstructure stress. In the pre-move window from 06:11 to 06:14 UTC, median spread was 1.02 basis points, median top-of-book depth was $8.75K, and median depth within ±10 basis points was $65K.

During the initial catch-up from 06:14 to 06:16 UTC, median spread widened to 13.88 basis points, with a 95th percentile of 47.8 basis points, while top-of-book depth fell to $6.44K and depth within ±10 basis points collapsed to just $256.

In the subsequent acceleration phase from 06:16 to 06:22 UTC, median spread widened further to 24 basis points, top-of-book depth fell to $3.52K, and depth within ±10 basis points was effectively zero, with trade-to-mid slippage rising to 14.26 basis points in the catch-up phase and 20.8 basis points in the acceleration phase, while 95th percentile slippage approached 89 basis points in both windows

Even under those conditions, trading continued aggressively because Hyperliquid remained the only continuously open venue through which the shock could be expressed. After the initial repricing, CL stayed pinned near the upper weekend level around $70.65, with bid depth rebuilding beneath the market as buy-side demand accumulated under a capped discovery regime.

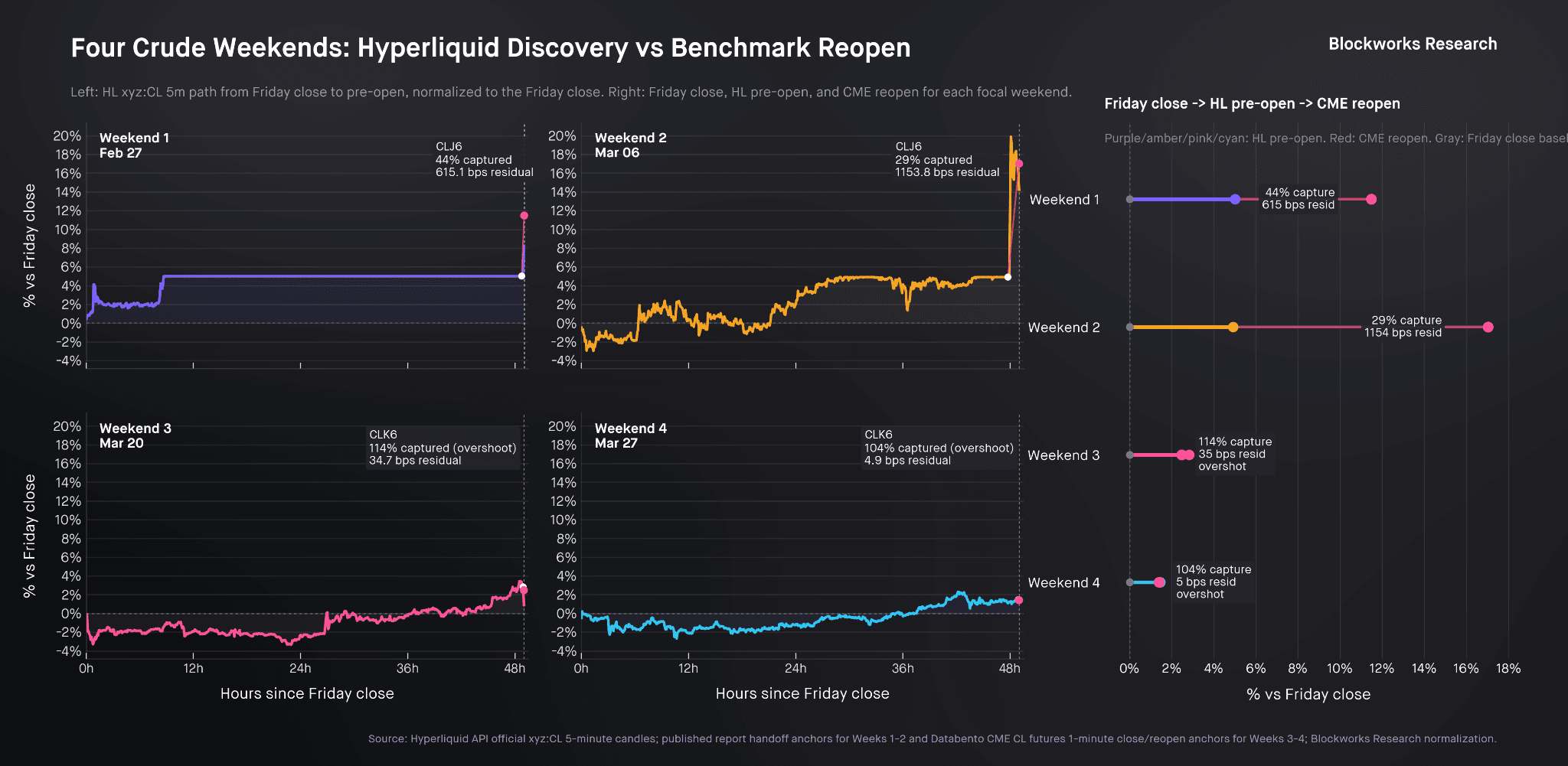

CME eventually reopened at $75, up $7.72 from Friday’s close of $67.28. Relative to Hyperliquid’s capped weekend level of $70.64, the remaining gap was $4.36, indicating that Hyperliquid had already absorbed roughly 44% of the full reopen move before benchmark futures came back online.

Weekend Two: Series Of Regime Changes

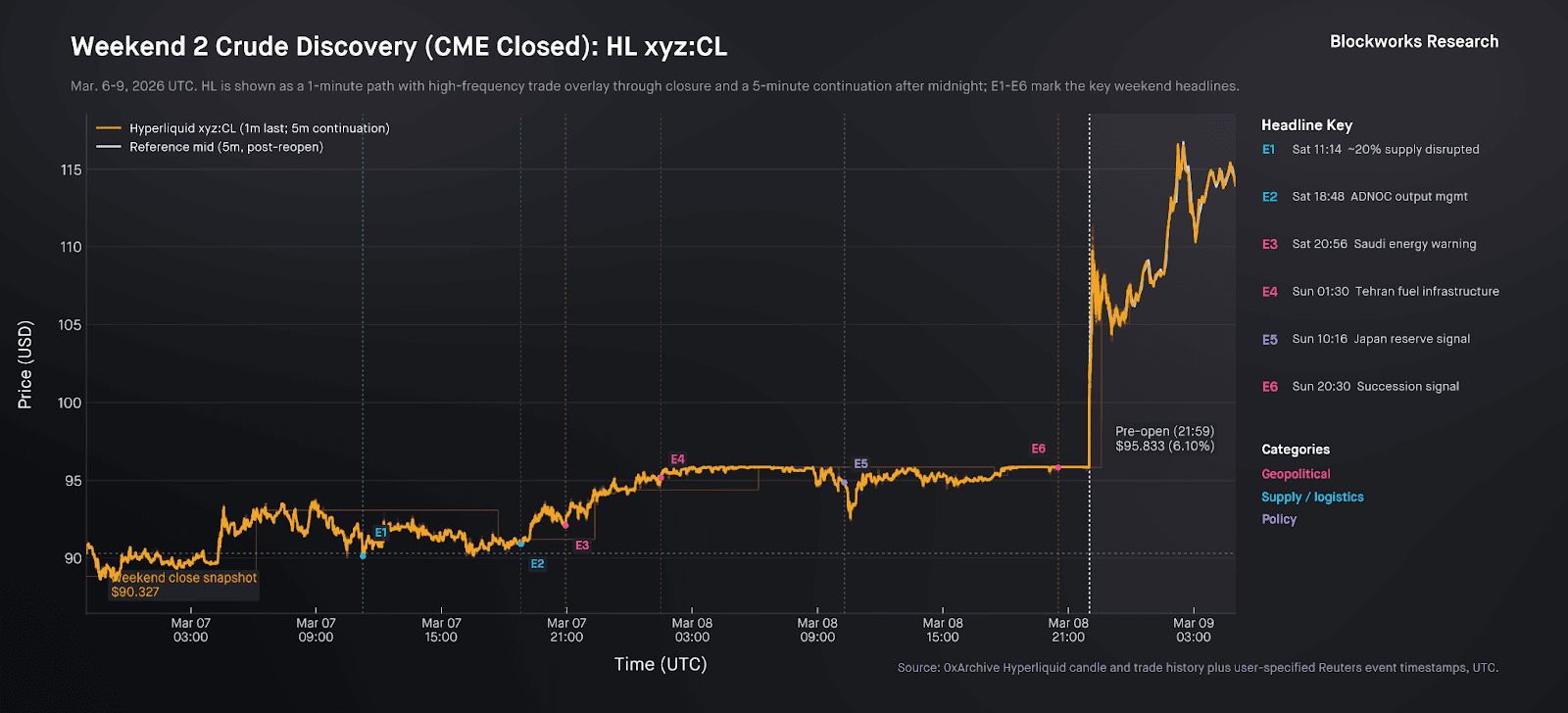

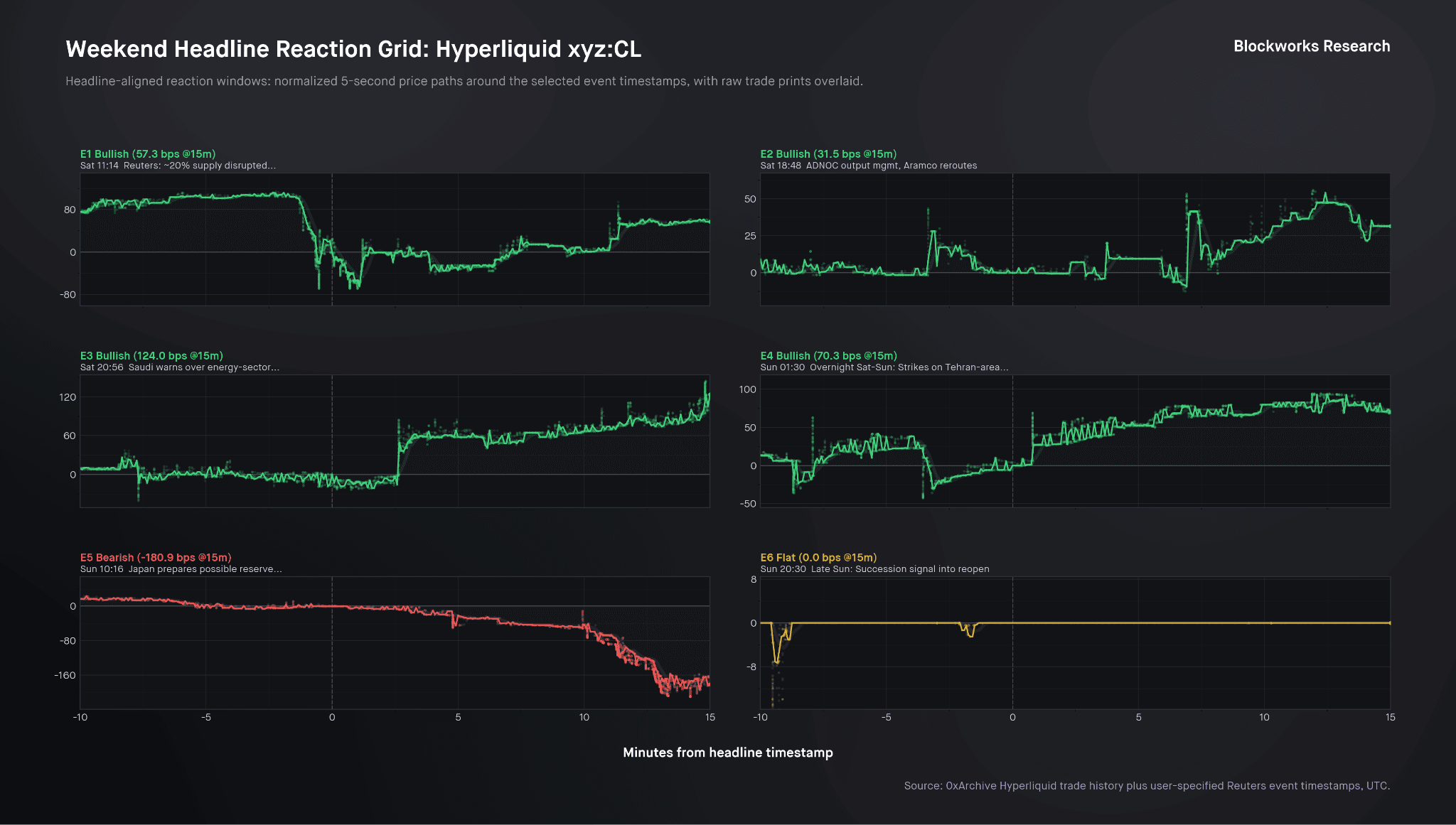

One week later, with CME closed on Friday (Mar. 6), Hyperliquid again became the only continuously open venue for CL risk transfer via TradeXYZ’s CL product. Unlike the first weekend’s single-shock repricing, this episode unfolded as a rolling sequence of supply-chain and infrastructure headlines, producing repeated repricing steps rather than one isolated jump.

Reuters reporting through Saturday increasingly framed the market as an operational supply crisis. Roughly one-fifth of global oil and gas flows remained disrupted, about 140 million barrels had already been withheld from refiners, and storage pressure across the Gulf was rising. Kuwait declared force majeure and began cutting output, ADNOC moved to manage offshore output under storage constraints, and further attacks on regional energy infrastructure reinforced the sense that the disruption was broadening rather than stabilizing.

Because Hyperliquid remained open throughout the weekend, each headline could be traded as it arrived rather than deferred into a single reopen print. The reactions were directionally coherent: supply-disruptive headlines were bullish for crude, while Japan’s reserve-release signal was bearish. Using 15-second normalized candles around each event timestamp, 30-minute responses were +139.6 bps for ADNOC and Aramco operational updates, +120.6 bps for the Saudi warning, +54.7 bps for Tehran-area infrastructure strikes, and -156.8 bps for Japan’s reserve-release signal.

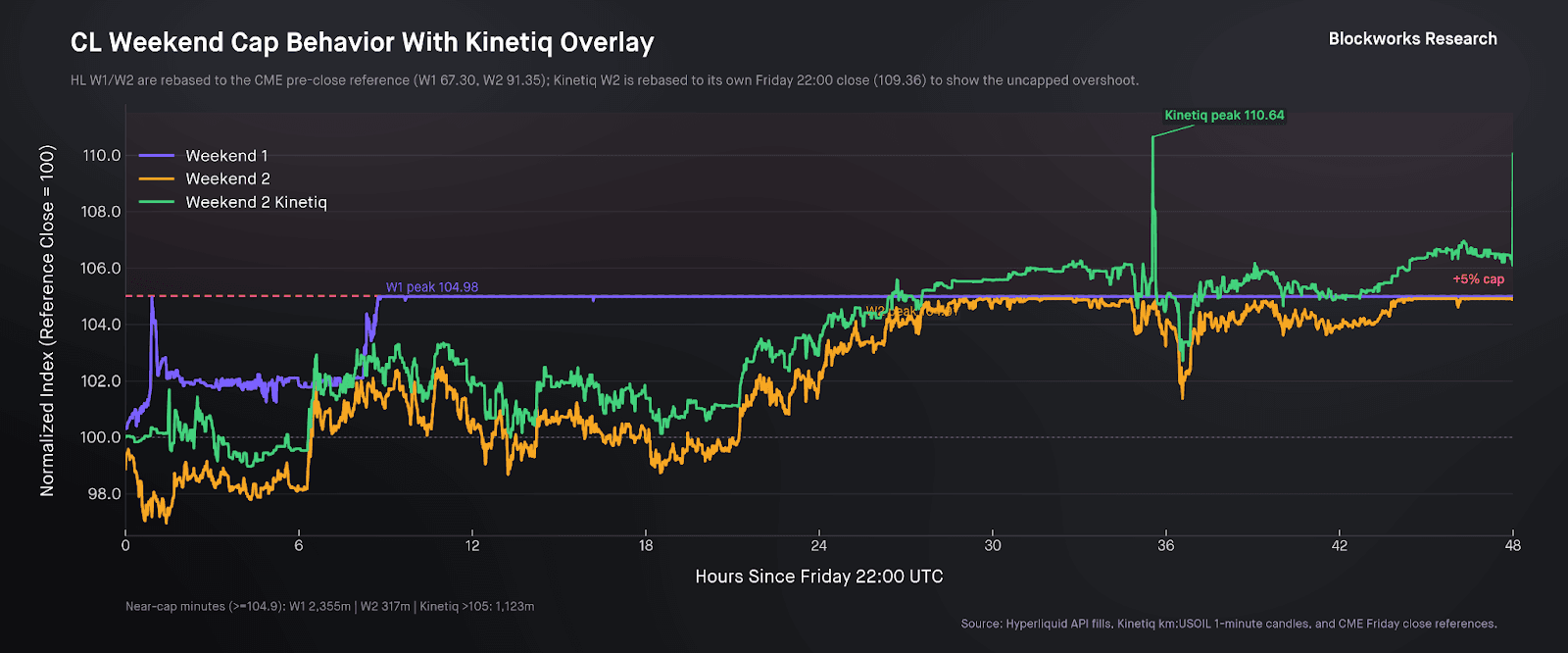

By the Sunday handoff, Hyperliquid’s last pre-open reference was $95.833, versus CME’s first CLJ6 print of $106.89, a gap of $11.06, or 11.54%. Relative to Friday’s CME close of $91.35, the reopening print was $15.54 higher, or 17.01%. Across both shock weekends, Hyperliquid was the only continuously open venue through which crude-linked risk could reprice while benchmark futures were shut.

Even under weekend bands, it had already repriced a substantial share of that move before benchmark futures reopened, processing roughly $305.6 million in weekend notional through a live sequence of tradable headlines.

Weekend Three and Four: A More Tradable Market

Weekends One and Two established that Hyperliquid could remain open and reprice crude while benchmark futures were closed.

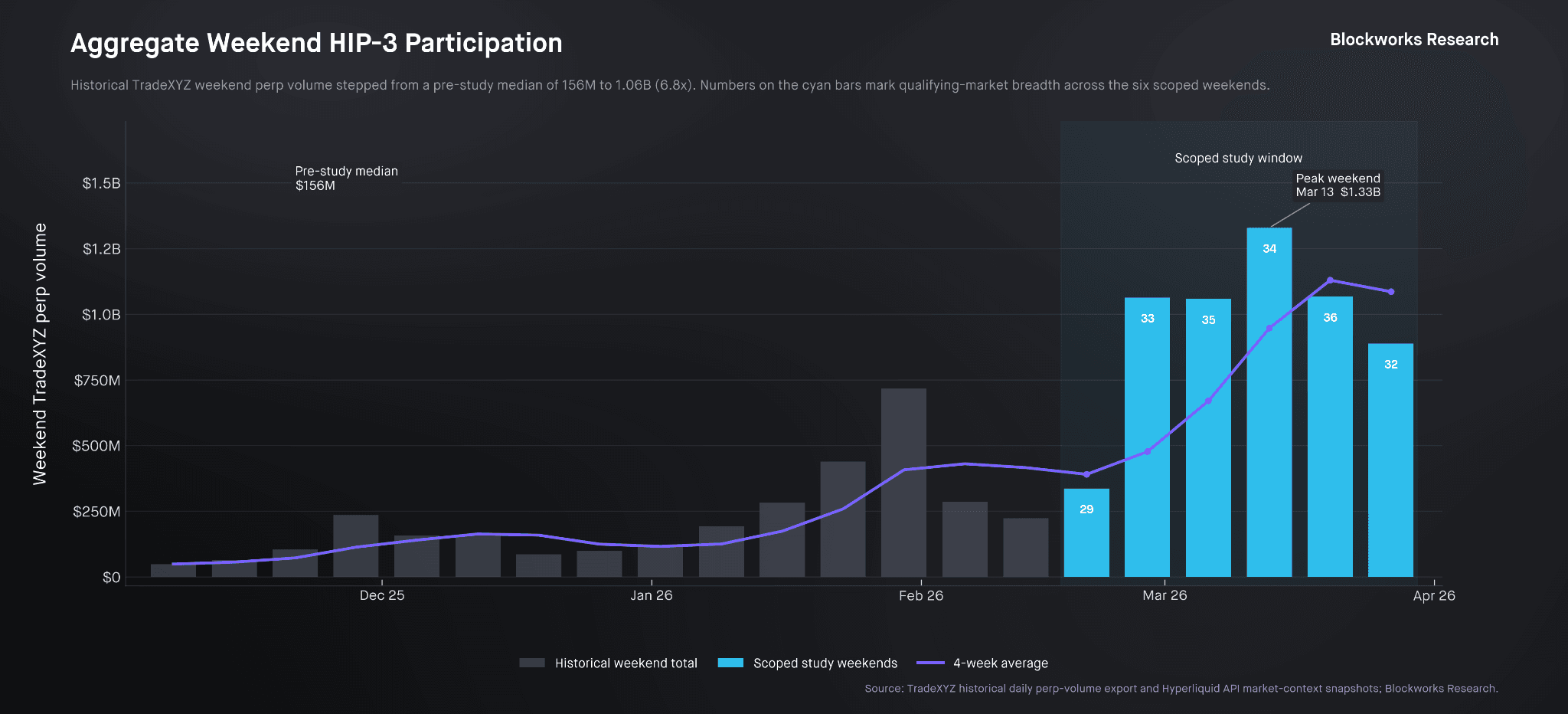

By late March, the question had shifted from responsiveness to market quality. In our earlier Silver report, we found that weekend spreads could remain relatively tight, but under much quieter conditions. This sample is a stricter test. Aggregate weekend participation across the refreshed HIP-3 study universe rose from roughly $1.24 billion on February 27 to $1.97 billion on March 6 and $2.13 billion by March 27, while weekend CL notional rose from $14 million in the initial shock weekend to $305.6 million on March 6 and remained elevated at $175.9 million and $256.6 million on the subsequent March weekends.

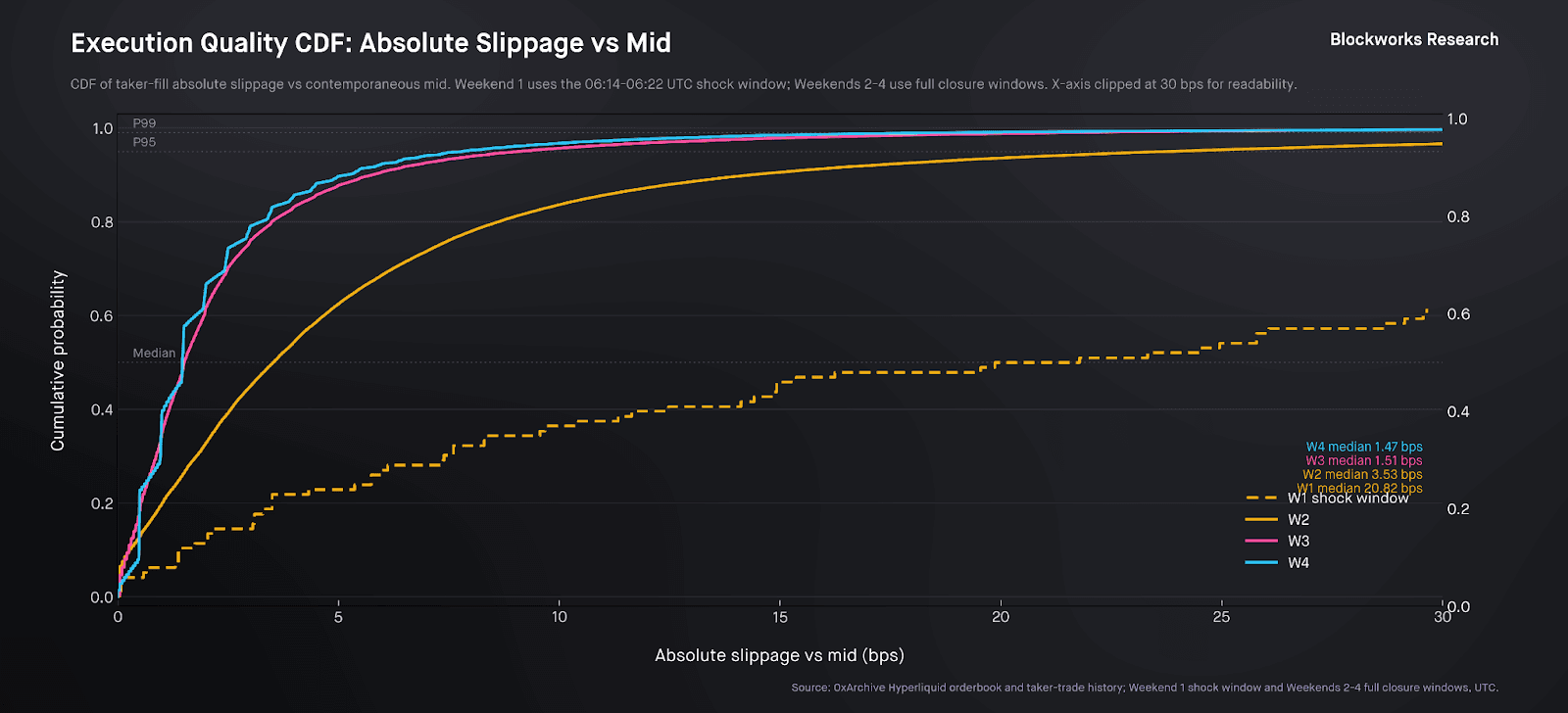

Quoted spreads and execution costs compressed sharply as activity deepened. Median quoted spread fell from 16.9 basis points in the initial shock window to 4.1 basis points on March 6 and to roughly 2 basis points on March 20 and March 27. Median absolute trade-to-mid slippage fell from 17.9 basis points to 3.5 basis points and then to roughly 1.5 basis points on the later two weekends, while 95th percentile slippage narrowed from 88.6 basis points to 23.8, 9.1, and 7.8 basis points, respectively.

By late March, Hyperliquid’s weekend crude market was handling far more notional with materially tighter quotes and much cleaner execution than during the initial shock regime.

The four-week progression reveals a market learning to price in real time. On Weekend One, Hyperliquid captured roughly 44% of the eventual reopen gap. By Weekend Two, the extreme severity of the shock exposed the limits of the static +5% bounding bands; because the market was artificially pinned at the ceiling, the capture rate mechanically fell to roughly 29%. Only when the shock intensity dropped below that threshold in Weeks Three and Four did the platform's true efficiency emerge: by March 20, Hyperliquid finished within 34.7 basis points of the reopen, and by March 27, that residual compressed to just 4.9 basis points.

What began as a partial, band-constrained mechanism had become, within a month, extremely accurate to the benchmark itself.

Bounding Bands

To understand why those first two weekends stopped short, it helps to distinguish between the underlying asset and the price that actually governs trading on TradeXYZ. CL-USD is a linear perpetual contract designed to replicate delta-one exposure to the front-month crude oil market. But the economically relevant price on the platform is the mark price, which governs margin, liquidations, stop and limit triggers, and unrealized profit and loss.

During normal trading hours, the mark price is calculated as the median of three inputs: the oracle price; the oracle price adjusted by a 150-second continuous-time exponentially weighted moving average of the difference between the perpetual mid-price and the oracle; and the median of the best bid, best ask, and last trade. In normal conditions, this allows the perpetual to reflect local order-book conditions while remaining anchored to the external market.

On weekends, no live benchmark market is available for publishers to reference. TradeXYZ therefore fixes the external price at the last externally derived fair value while the oracle continues updating through the platform’s internal pricing mechanism. Because liquidity is thinner and market makers cannot hedge continuously in the underlying venue, open interest carried over from the weekday session faces greater liquidation and inventory risk. Bounding bands were introduced to limit how far the mark price can deviate from that reference during internal pricing sessions.

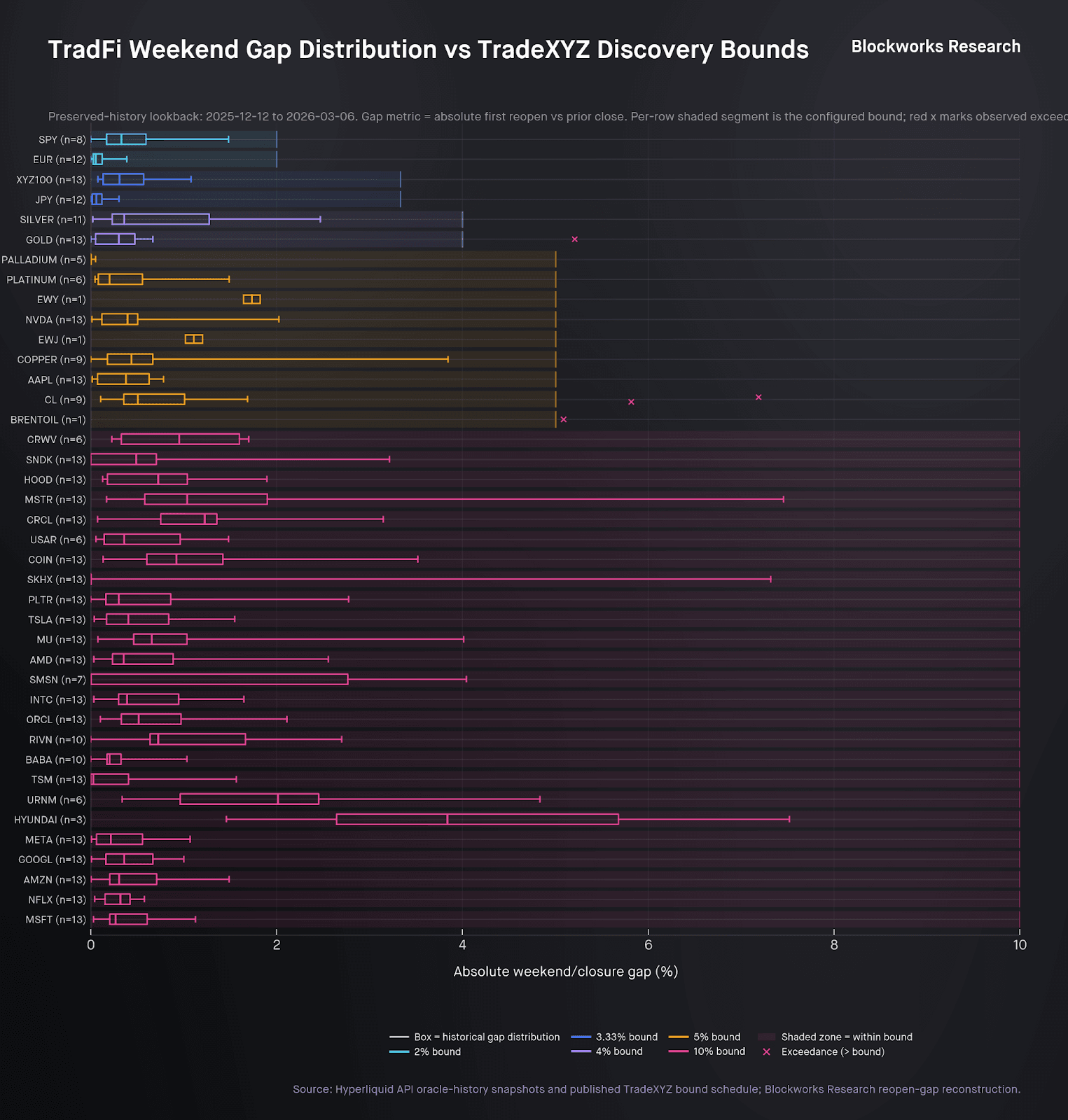

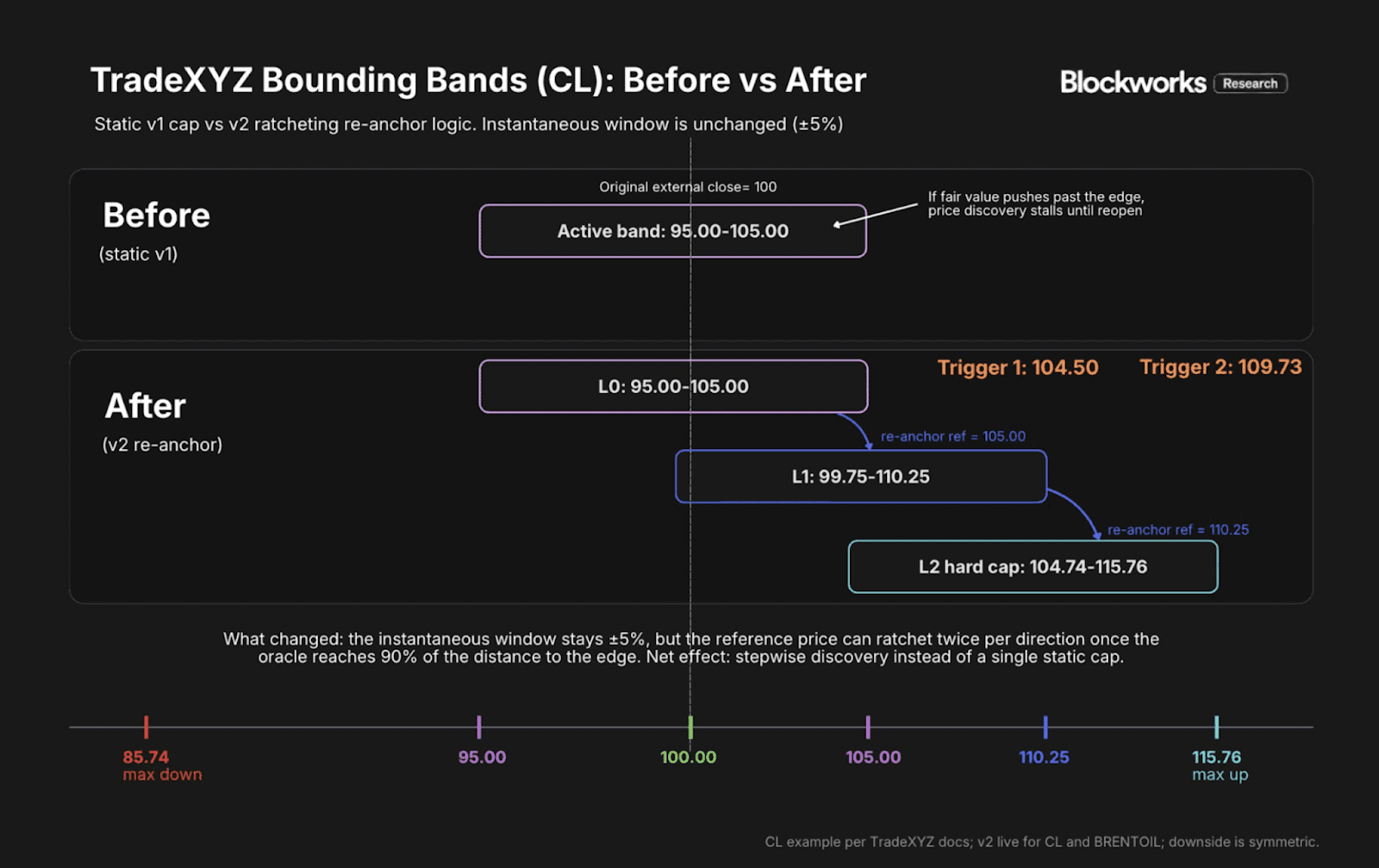

Before the March 13, 2026 methodology update, TradeXYZ used a static v1 band: during internal pricing sessions, the mark price could move only within ±(1 / max leverage) of the last externally derived price.

In practice, that meant CL was capped at ±5% and SILVER at ±4%. The design gave market makers a fixed off-hours risk envelope and protected positions whose liquidation prices sat outside the active band. In ordinary conditions, that tradeoff appears to have been broadly well calibrated. Across 40 mapped underlyings and 2,069 TradFi reopen events, the median exceedance rate was 0%: 25 assets never breached their configured bound, 30 of 40 breached in 2% or fewer events, and 35 remained at or below a 5% breach rate. Backtested against ordinary closure-window reopen behavior, static bands generally served their intended purpose: capping disorderly mark drift while preserving a bounded risk envelope for market making and margin.

However, as evidenced by CL, the tradeoff appears in edge regimes, which are also the regimes that matter most economically. Additionally, sStatic bands constrain the maximum leverage that can be safely offered, since tighter allowed price movement is required to support more extreme leverage. More importantly, when the economically correct move exceeds the cap, price discovery does not disappear but becomes incomplete.

In the two focal crude weekends, TradeXYZ’s CL market moved decisively in the right direction and materially closer to the eventual benchmark reopen, but once price reached the upper weekend limit it could no longer express additional information through additional repricing. The market could still show persistent demand at the ceiling, yet part of the adjustment had to be deferred into the external reopen.

The comparison with other builder-deployed perpetuals makes that constraint easier to see: Kinetiq’s crude market traded as high as 110.64% of its Friday reference, or about +10.6%, materially beyond TradeXYZ’s +5% weekend cap.

Bounding Bands v2 changes the reference architecture rather than the width of the active band. For CL, the active window remains ±5%, but the last external close now serves only as the initial reference. Once the oracle reaches 90% of a bound, the reference re-anchors and a new ±5% window opens. This can repeat twice per direction before the band becomes a hard cap. In TradeXYZ’s CL example, that expands maximum discovery from the original close to +15.76% on the upside and -14.26% on the downside.

The effect is to preserve the same per-step risk controls while allowing materially more genuine weekend price discovery in large macro moves.

Are Weekend Markets Informative?

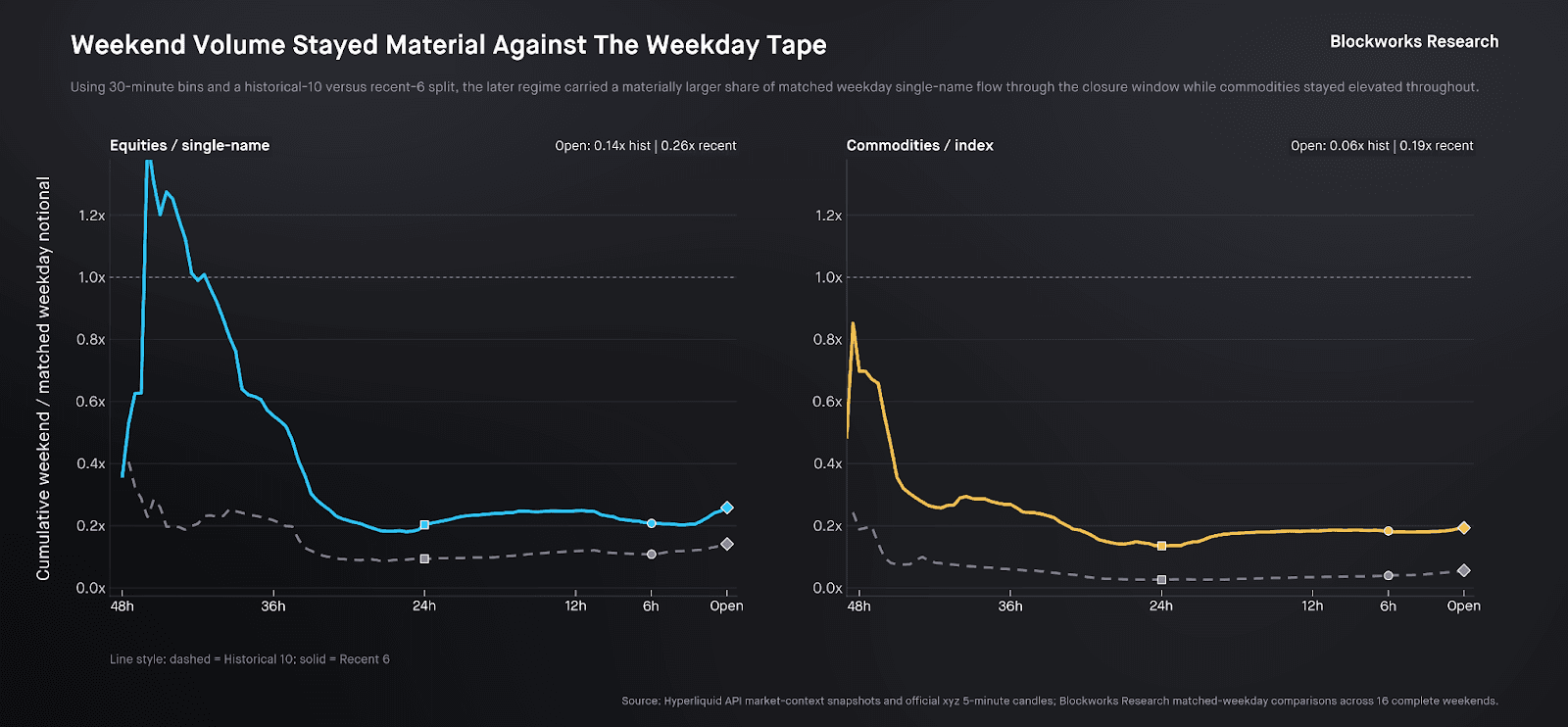

While crude oil was the clearest expression of the weekend shock, it was far from the only HIP-3 market to reprice off-hours. By late February and March, Hyperliquid’s weekend tape had broadened into a more active cross-asset market rather than a single crude-led episode. Relative to matched weekday windows, the recent six weekends carried a larger share of normal trading activity by the reopen, with cumulative weekend volume rising from 0.14x to 0.26x of weekday flow in single-name equities.

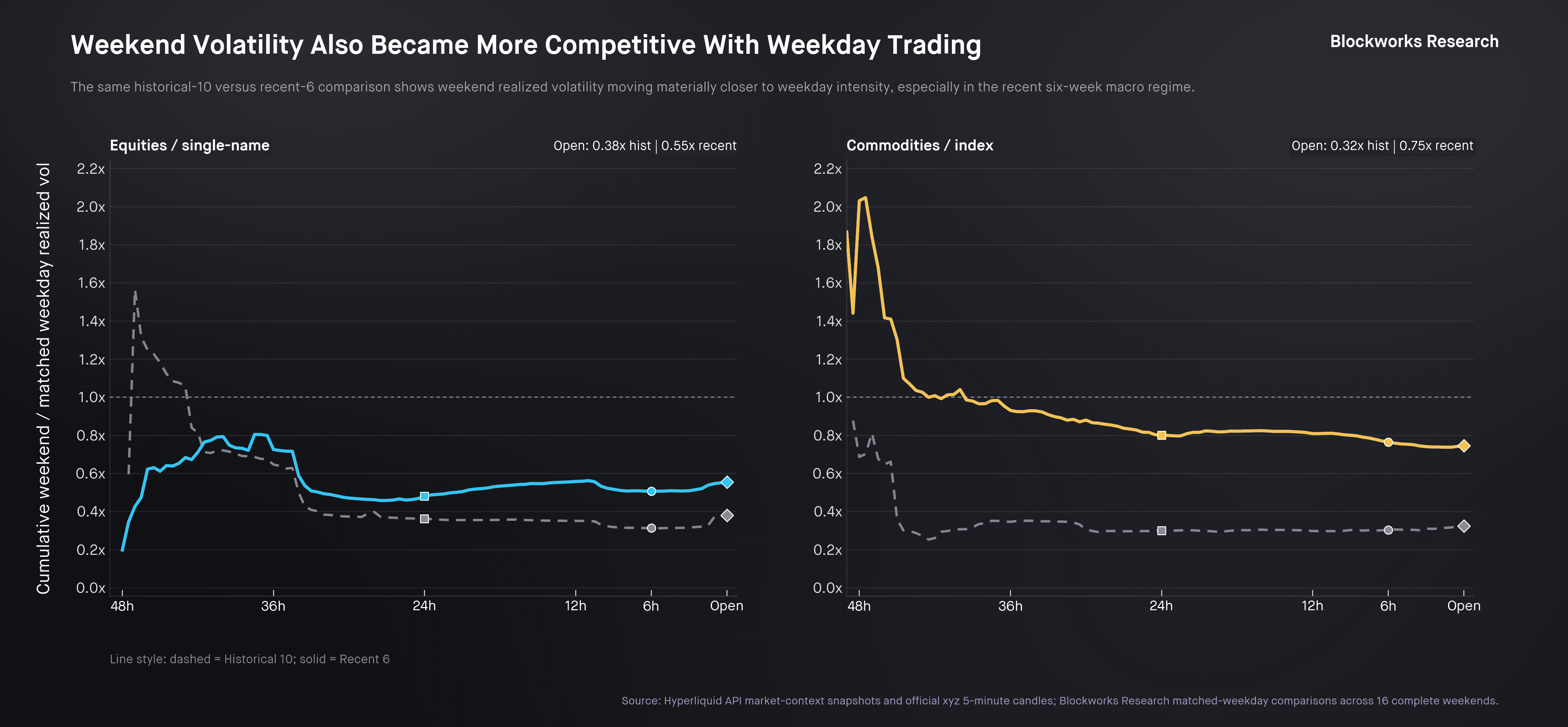

Weekend realized volatility moved the same way, rising from 0.38x to 0.55x of weekday levels. Relative to our earlier Silver work, this suggests Hyperliquid’s weekend markets were not only functioning credibly, but were also absorbing a larger share of genuine off-hours trading, repricing, and risk transfer.

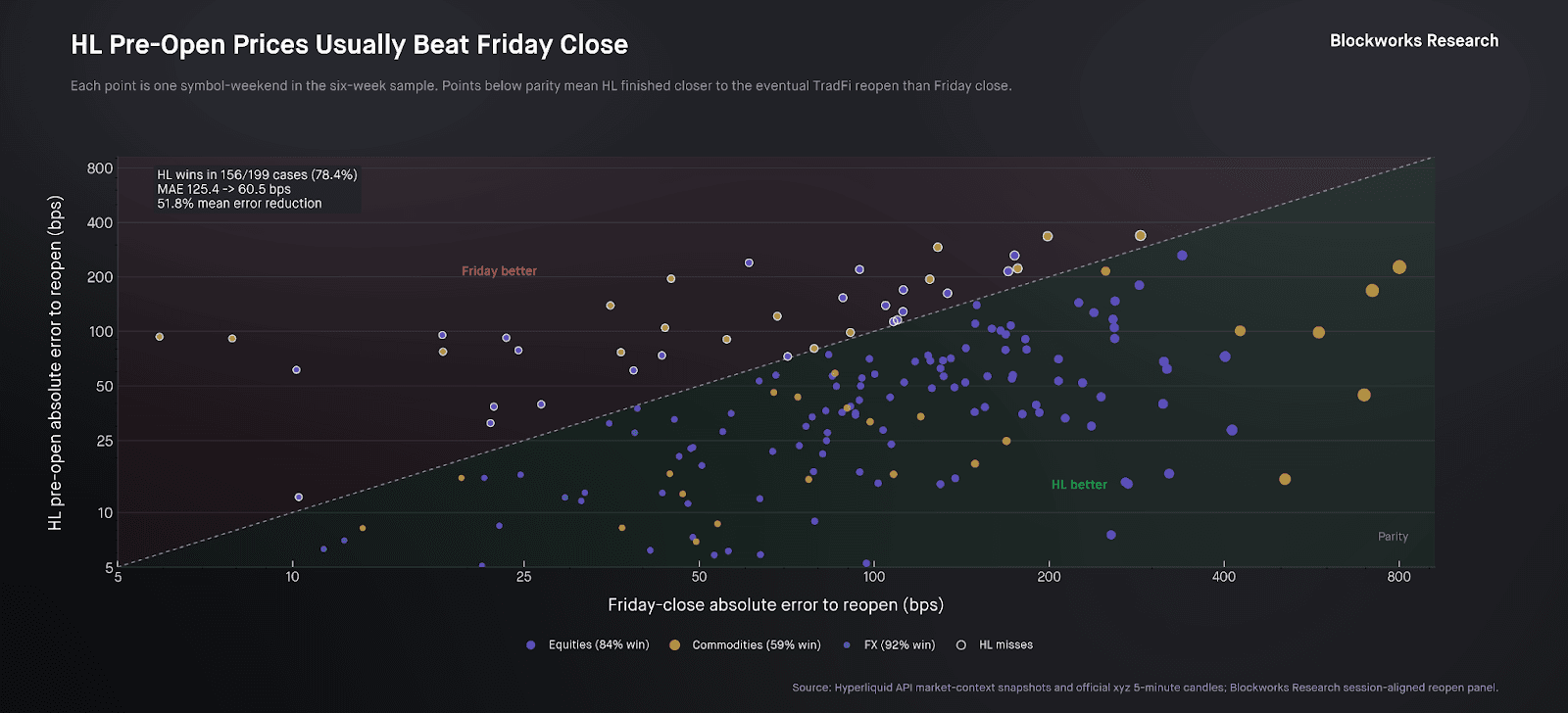

We compare two reopen anchors across the six complete weekends from February 20 through March 27, 2026: Friday’s close and Hyperliquid’s final pre-open price. Applying the same scoped filter, excluding Korea-linked symbols and requiring at least $1 million in weekend participation proxy, yields 199 symbol-weekend observations across 37 symbols.

Within that sample, Hyperliquid finished closer to the eventual TradFi reopen than Friday’s close in 156 of 199 cases, or 78.4%. That improvement was economically meaningful. Mean absolute reopen error fell from 125.4 basis points using Friday’s close as the anchor to 60.5 basis points using Hyperliquid, a 51.8% reduction, while median absolute error fell from 92.8 to 38.4 basis points. Across the cross-section, Hyperliquid’s final pre-open was usually the better reopen anchor.

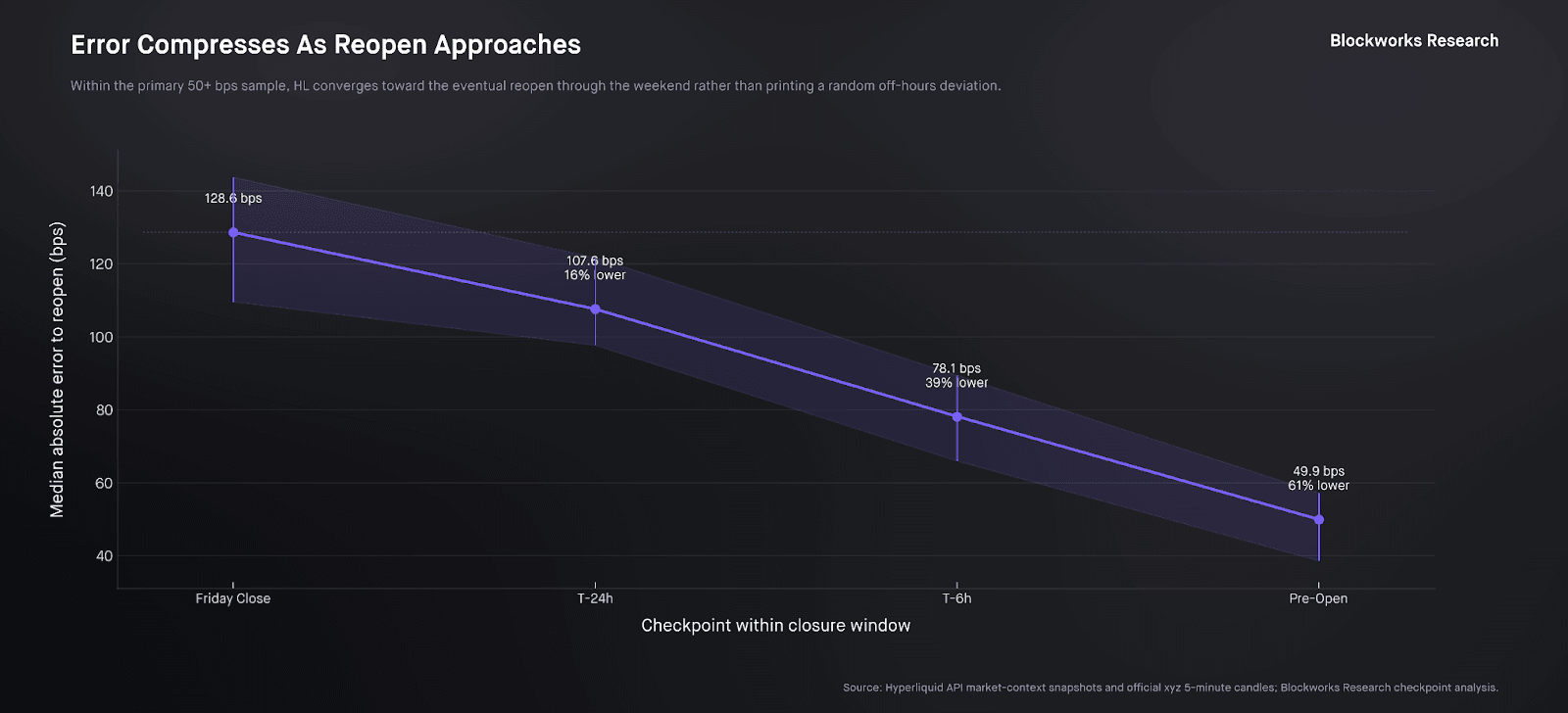

Hyperliquid progressively assimilated information through the closure window. In the primary 50+ basis-point sample, median absolute error to reopen fell from 128.6 basis points at Friday’s close to 107.6 basis points by T-24h, 78.1 basis points by T-6h, and 49.9 basis points immediately before reopen.

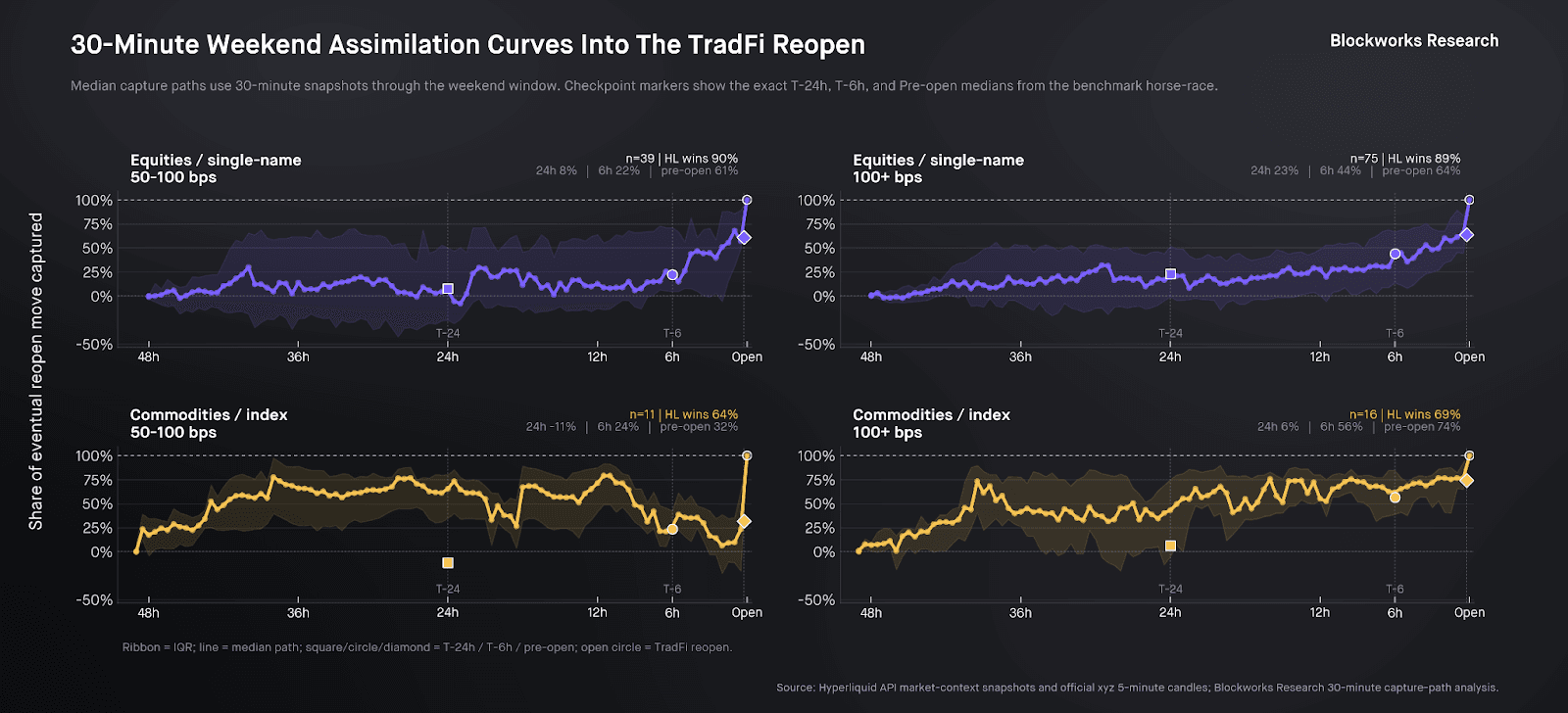

The path differed by regime. In 100+ basis-point equities, Hyperliquid had already captured 23% of the eventual Friday-to-reopen move by T-24h, 44% by T-6h, and 64% by pre-open; in 100+ basis-point commodities, the same sequence was 6%, 56%, and 74%. The reopen, in other words, was often the final handoff of a repricing process that had already been underway on Hyperliquid for most of the weekend.

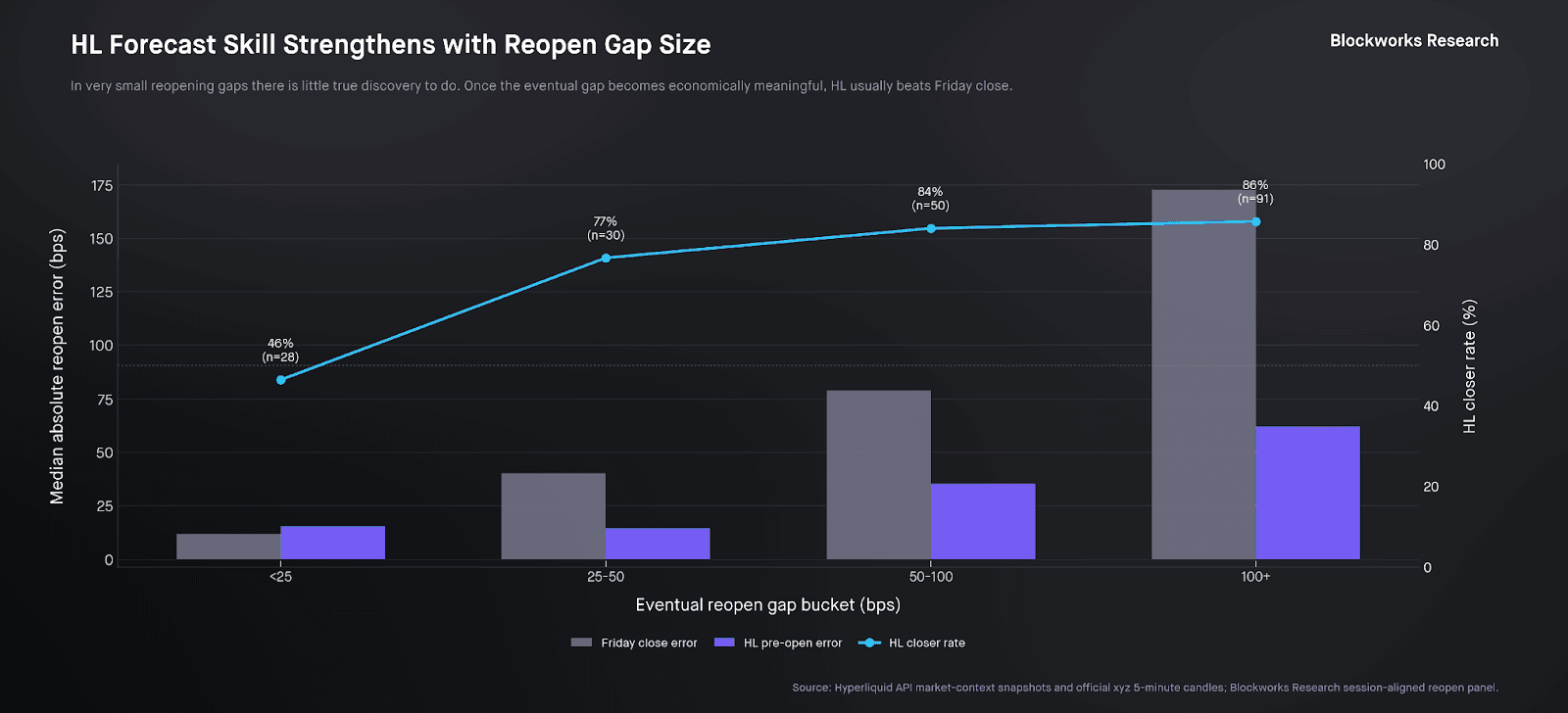

The signal was strongest precisely where there was real price discovery to do. On weekends where the eventual reopen gap was smaller than 25 basis points, Hyperliquid beat Friday only 46.4% of the time, with a slightly negative median improvement of -1.4 basis points. Once the gap became economically meaningful, the edge strengthened quickly: 76.7% in 25-50 basis point gaps, 84.0% in 50-100 basis point gaps, and 85.7% in 100+ basis point gaps, where median error reduction reached 103.5 basis points. Weekend markets therefore added the most value in the exact cases where Friday’s close had become the stalest benchmark.

Regressing the realized Friday-to-reopen move on Hyperliquid’s implied Friday-to-pre-open move yields a slope of 0.816, an intercept of -19.2 basis points, and an R-squared of 0.785, with directional agreement of 89.9%.

Hyperliquid’s weekend prices were therefore not a perfect one-for-one substitute for the TradFi reopen. But across the sample, they were clearly informative: an economically meaningful off-hours pricing signal that moved markets materially closer to where traditional venues ultimately reopened, especially in the regimes where Friday’s close had become least informative.

Are Weekend Markets Efficient

Finally, because these markets appear both active and informative into the reopen, we test how tradable they actually are. To do so, we analyze order book and trade data across 21 XYZ markets on weekends and weekdays, covering approximately 8.59 million weekday trades, 1.06 million weekend trades, 251,556 weekday order-book minutes, and 60,195 weekend order-book minutes, to compare liquidity and execution dynamics across regimes.

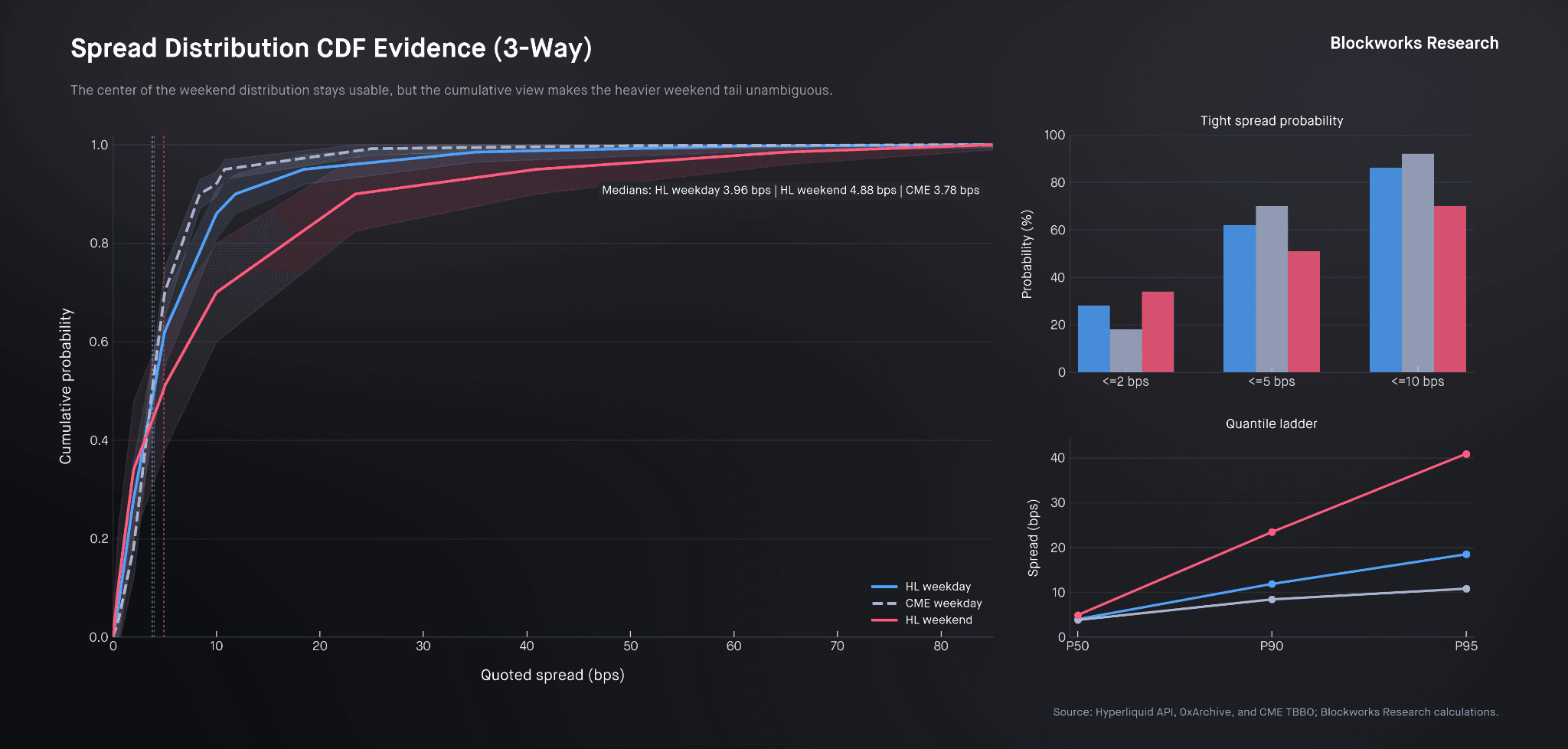

The median quoted spread is 3.96 basis points on Hyperliquid weekdays, 3.78 on weekday CME, and 4.88 on Hyperliquid weekends. The main penalty appears in the tails: weekend Hyperliquid reaches 23.43 basis points at the 90th percentile and 40.90 at the 95th percentile, versus 11.84 and 18.46 on Hyperliquid weekdays and 8.39 and 10.78 on weekday CME.

The cumulative distribution view points to the same conclusion. On an equal-weight all-market basis, median spread is 4.01 basis points on Hyperliquid weekdays, 3.78 on weekday CME, and 4.90 on Hyperliquid weekends.

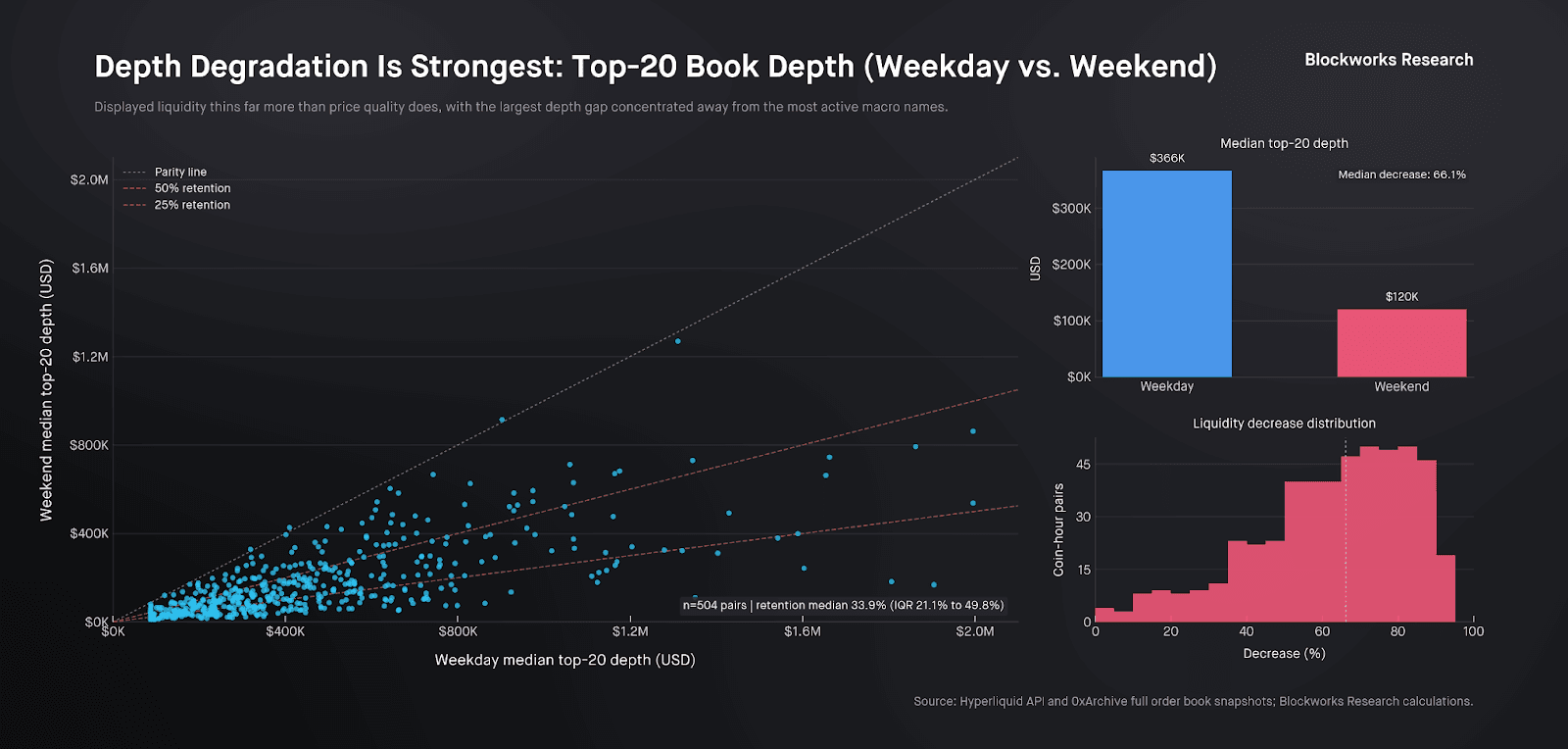

Depth is where weekend degradation becomes most visible. Across 504 market-hour observations, median weekend depth retention is only 33.9% of weekday levels, with an interquartile range of 21.1% to 49.8%, and in 381 of 504 cases, weekend depth falls below 50% of weekday depth. The main structural weakness of weekend trading is not stale pricing, but materially thinner displayed liquidity and less size behind the quote.

Still, weakness is not uniform across products. In the high-volume macro core, namely CL, XYZ100, EUR, SILVER, and GOLD, weekend execution remains efficient despite thinner depth. The share of trades with absolute slippage within 10 basis points rises to 89.7% on weekends from 77.7% on weekdays, while the share above 25 basis points falls to 4.0% from 8.5%. Notional-weighted slippage also improves, declining to 13.05 basis points from 16.69.

The main fragility of weekend trading is therefore concentrated outside the most active macro products. Where off-hours risk transfer matters most, market quality is already strong enough to be economically meaningful.

Conclusion

The Strait of Hormuz shock was the clearest test yet of whether Hyperliquid’s 24/7 market structure could do more than remain open while traditional venues were closed. Across both closure windows, Hyperliquid provided continuous crude oil risk transfer while benchmark futures were offline, repriced materially toward the new equilibrium before reopen, and processed a weekend macro shock in a way that was directionally coherent, economically meaningful, and increasingly orderly as participation deepened.

More broadly, across 199 symbol-weekend observations, Hyperliquid TradeXYZ weekend price finished closer to the eventual TradFi reopen than Friday’s close in 78.4% of cases, with directional agreement of 89.9%, a 51.8% reduction in mean absolute reopen error, and a near one-for-one relationship between implied and realized reopen moves.

Weekend markets were informative, with prices converging meaningfully toward subsequent TradFi opening levels. The evidence also suggests that this information was incorporated progressively through the closure window rather than appearing only at reopen, with weekend moves largely carrying through instead of reverting toward Friday’s close.

There are still constraints. Weekend depth remains thinner than under weekday conditions, and execution quality deteriorates in stressed tail environments. At the same time, the crude weekends highlighted how much was already achieved even under imperfect design. Static bounding bands limited part of the off-hours adjustment precisely when new information mattered most, yet Hyperliquid still transmitted substantial information, facilitated real risk transfer, and anchored prices materially closer to the eventual benchmark reopen. Core price discovery function is already present, and improvements to off-hours controls should expand its precision and capacity further.

Hyperliquid is already demonstrating that 24/7 onchain markets can play a meaningful role in price discovery for traditionally traded assets.

This content is for informational purposes only and should not be construed as legal, tax, investment, financial, or other advice. The views expressed are the author's alone and do not necessarily reflect those of Blockworks. This content is not an offer to buy or sell any securities or financial instruments. Blockworks does not provide investment advice and nothing in this content should be considered investment advice. Consult with your financial advisor before making any investment decisions.