This research report has been funded by GEODNET. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by GEODNET. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

GEODNET: Strengthening RTK Leadership

Key Takeaways

- Network maturation drives quality improvements: GEODNET has evolved from aggressive expansion to implementing strict performance standards through GIP-8, capping Location NFTs and implementing more strict uptime requirements, creating scarcity-driven tokenomics that prioritize network utility over pure growth.

- Strategic infrastructure migration accelerates ecosystem benefits: GIP-7's Solana transition provides superior liquidity, reduced transaction costs, and DePIN ecosystem synergies while maintaining 18-month Polygon compatibility, positioning GEODNET for enhanced scaling and user experience.

- Revenue diversification provides crypto-agnostic stability: The protocol currently generates ~$4.5M in onchain burns from ~$5.6M in total ARR, serving diverse web2 enterprise segments across agriculture, construction, and autonomous technologies. The 80% buyback-and-burn mechanism creates direct token value accrual independent of crypto market cycles.

- Competitive moats strengthen against incumbents: GEODNET maintains dramatic cost advantages and superior geographic coverage density, while legacy providers remain constrained by decade-old proprietary systems and technical debt.

Introduction

The RTK market remains critical to enabling centimeter-level positioning accuracy for autonomous technologies, such as Robots, Drones, and Autonomous Cars. GEODNET has maintained its competitive edge against multi-billion dollar incumbents Trimble and Hexagon through differentiated economics and vast geographic coverage. Recent governance proposals have addressed key operational challenges while strengthening the network's value proposition for enterprise customers demanding high-quality, reliable positioning data.

The convergence of precision positioning and robotics represents one of the most transformative technological shifts of the 2020s, creating unprecedented market opportunities for RTK providers like GEODNET. The robotics revolution is accelerating across multiple vectors, with Tesla's Optimus humanoid robot program potentially targeting 50-100K units by 2026, Figure AI's successful $1B Series C funding round at a $39B valuation with plans to ship 100K humanoids over four years, and Tesla's expanding robotaxi network that launched in Austin in June 2025 and San Francisco in August 2025. Together, these developments underscore the critical importance of centimeter-level positioning accuracy for autonomous systems operating in real-world environments.

Tesla's dual approach, combining humanoid robotics with autonomous vehicle technology, demonstrates the secular growth trends driving demand for precise positioning services. Elon Musk's projection that Tesla could become "the most valuable company in the world by far" based on autonomous vehicles and humanoid robots reflects the massive scale of this technological transformation. As Tesla progresses toward unsupervised Full Self-Driving capabilities nationwide and Figure AI begins alpha testing humanoid robots in homes during 2025, the addressable market for RTK services extends far beyond traditional applications into multi-trillion-dollar robotics ecosystems. However, industry experts note that the infrastructure challenges of deploying thousands of humanoids per facility, combined with current reliability limitations, suggest a longer timeline for mass deployment that favors early positioning infrastructure providers like GEODNET.

Two recent GEODNET Improvement Proposals (GIPs) demonstrate the protocol's commitment to operational excellence and strategic positioning. GIP-7 accelerates GEODNET's migration to Solana, offering deeper liquidity and improved user experience, while GIP-8 fundamentally improves network quality by implementing strict performance standards for Location NFTs. These changes reinforce GEODNET's technological and economic advantages while positioning the network for continued expansion in autonomous applications.

Network Growth and Performance Metrics

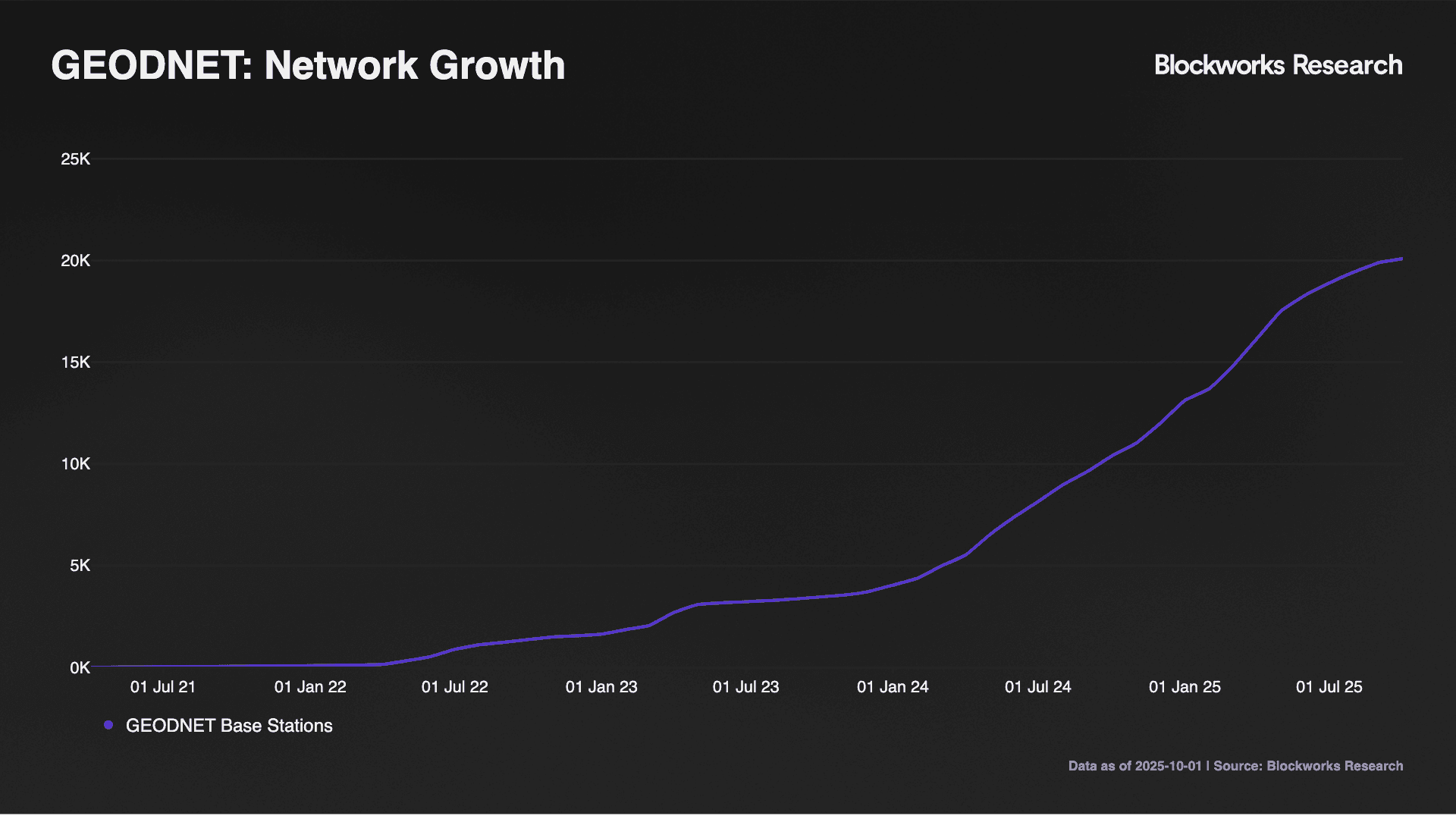

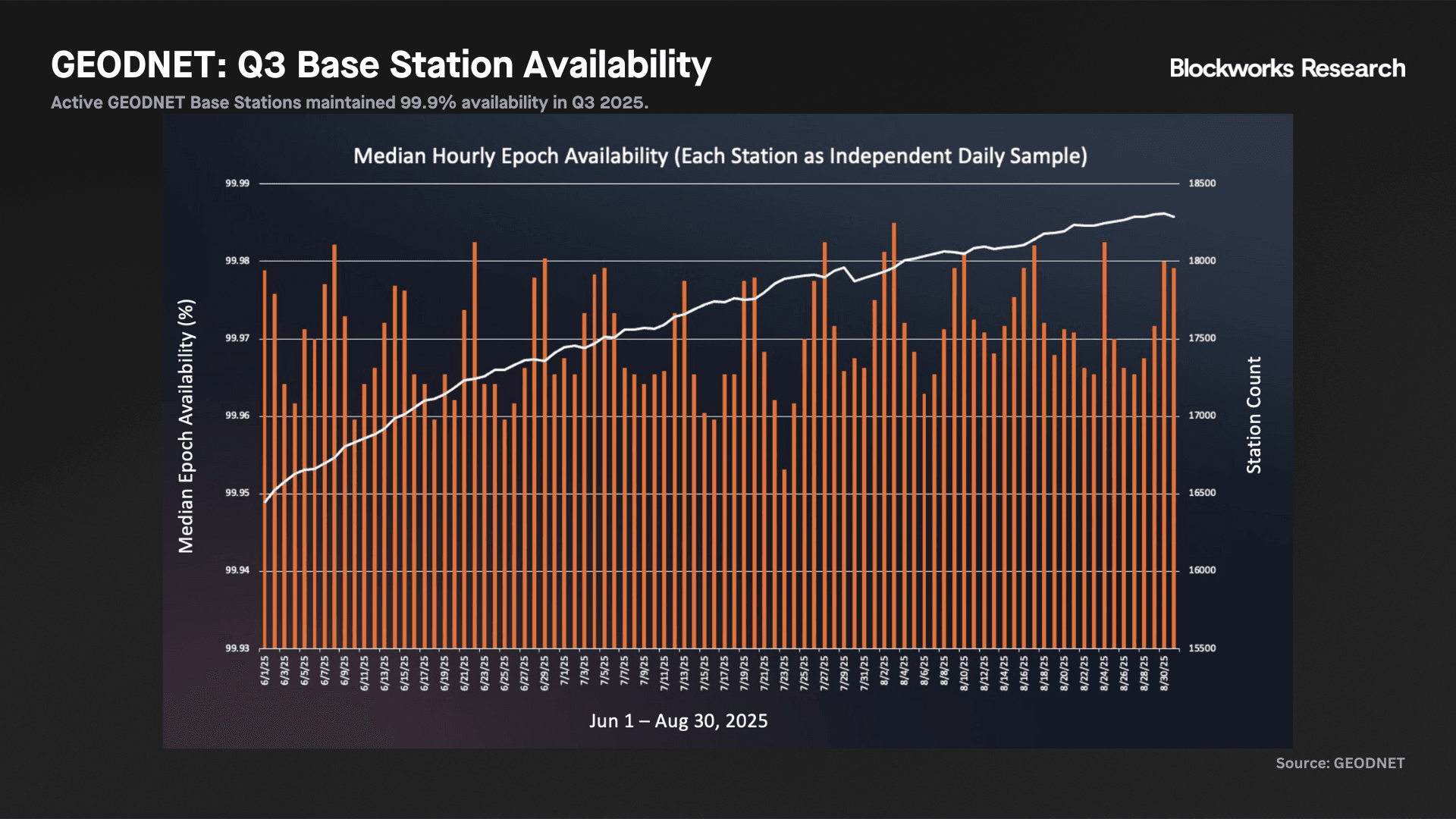

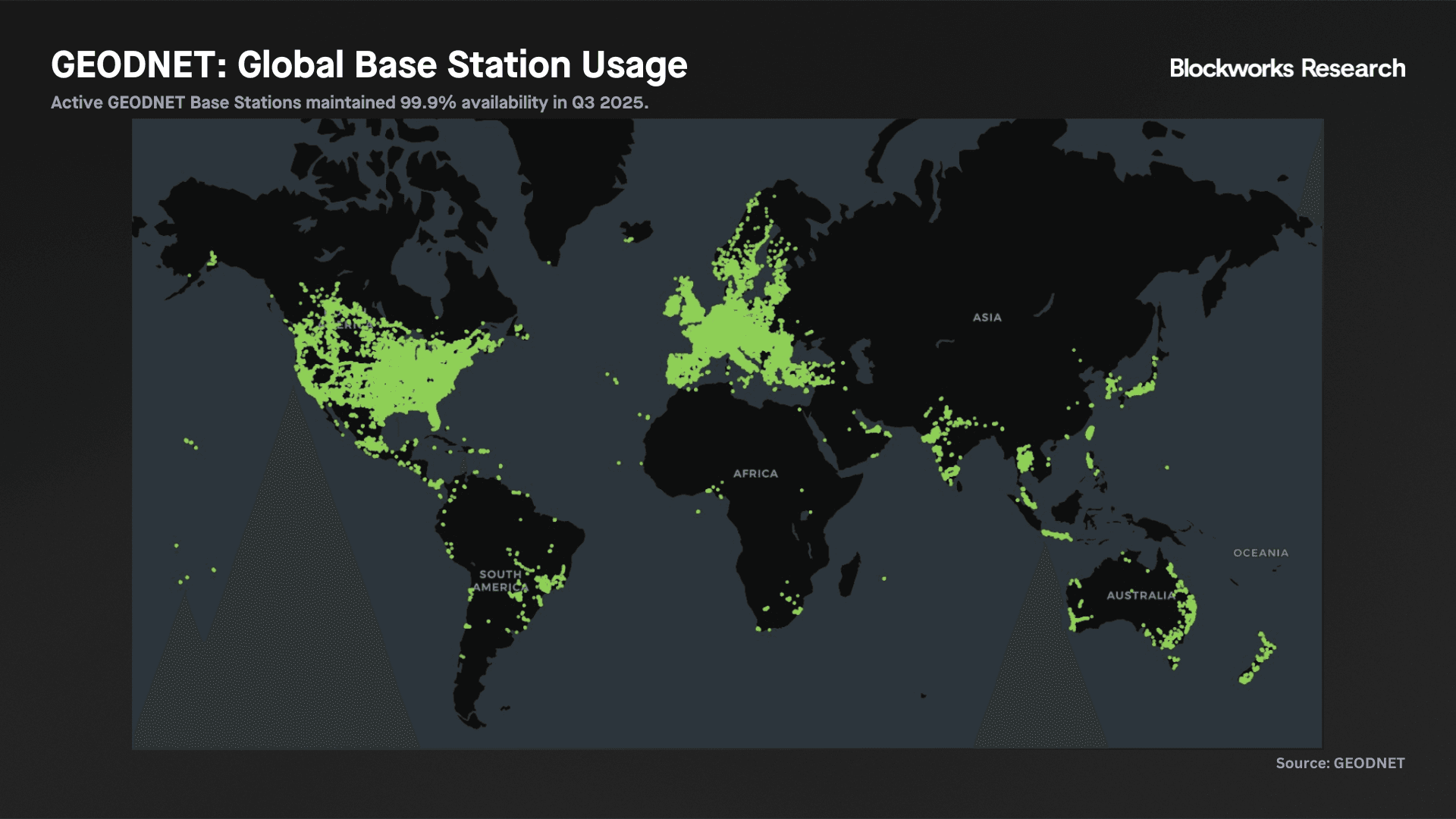

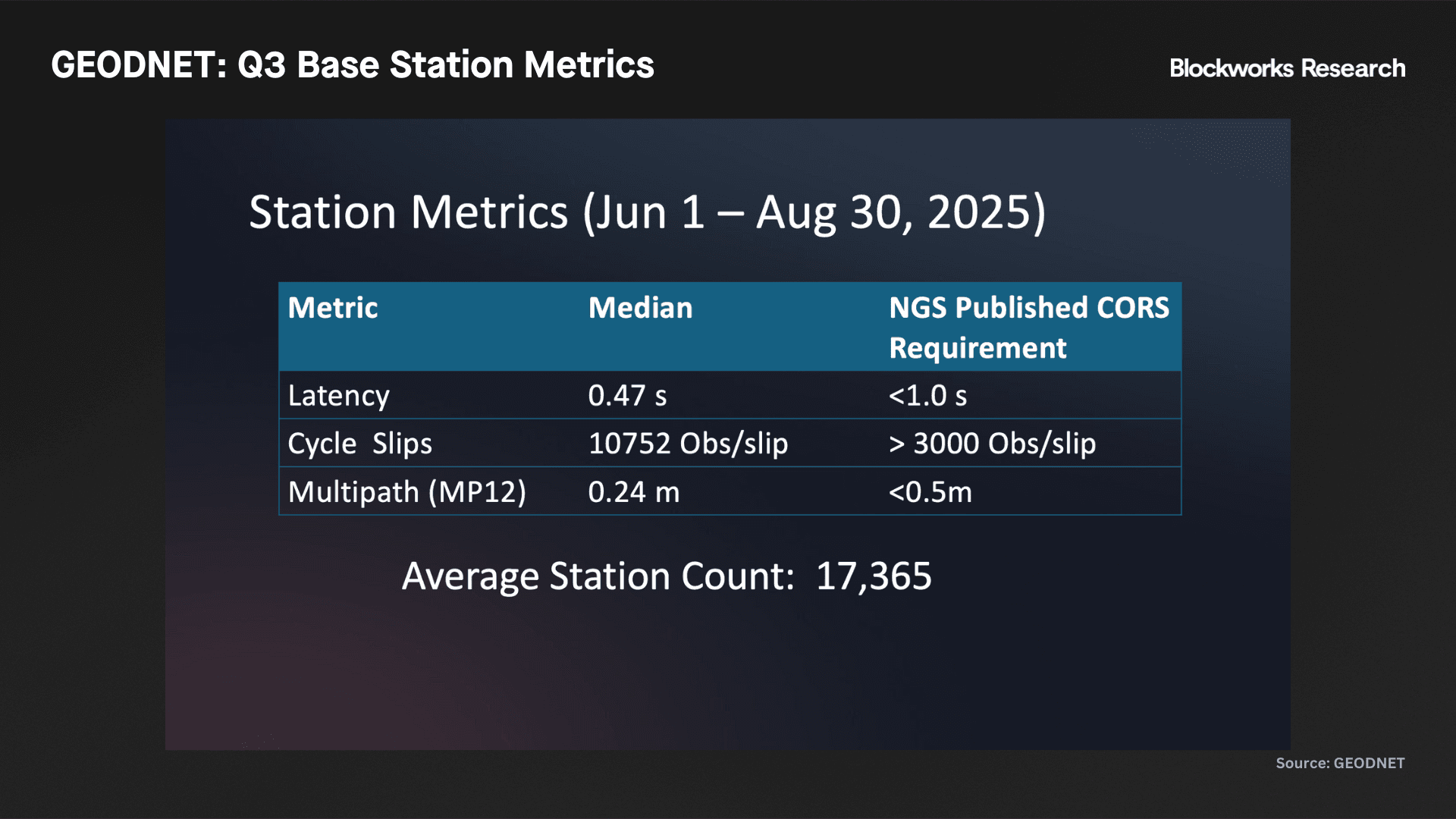

GEODNET's network has expanded significantly from ~10K stations in November 2024 to >17K active stations across 147 countries as of September 2025, cementing GEODNET's position as the world's largest RTK network by both station count and geographic coverage area, currently serving ~25K unique end-device connections and ~18K unique users daily.

The network's aggressive expansion phase is largely complete, with coverage established across the US, Europe, and India, and strategic expansion now focused on underserved regions through a SuperHex staking program. Current data suggests the supply side has reached sufficient density for enterprise applications, with the network's growth rate stabilizing as geographic gaps are filled.

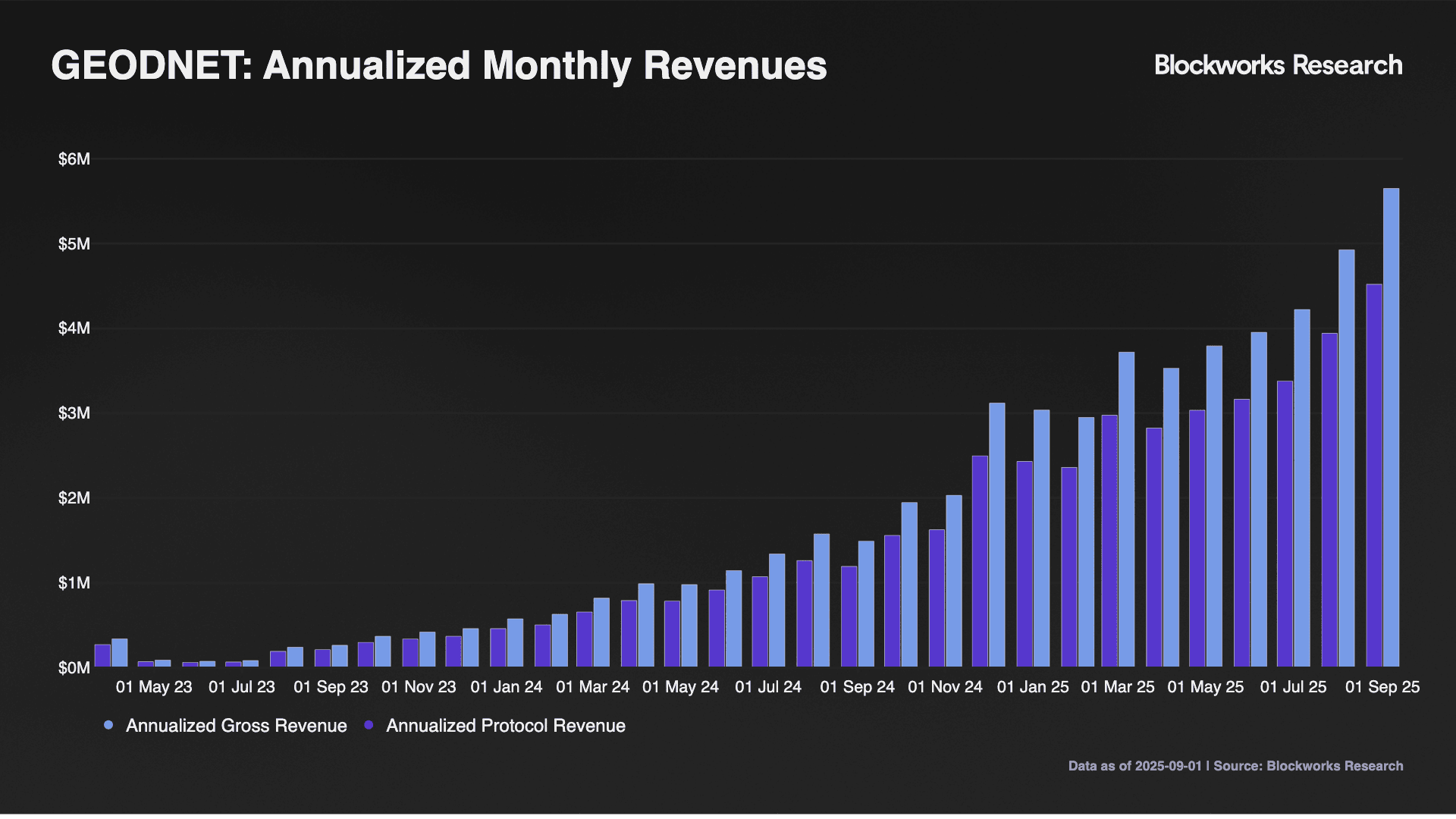

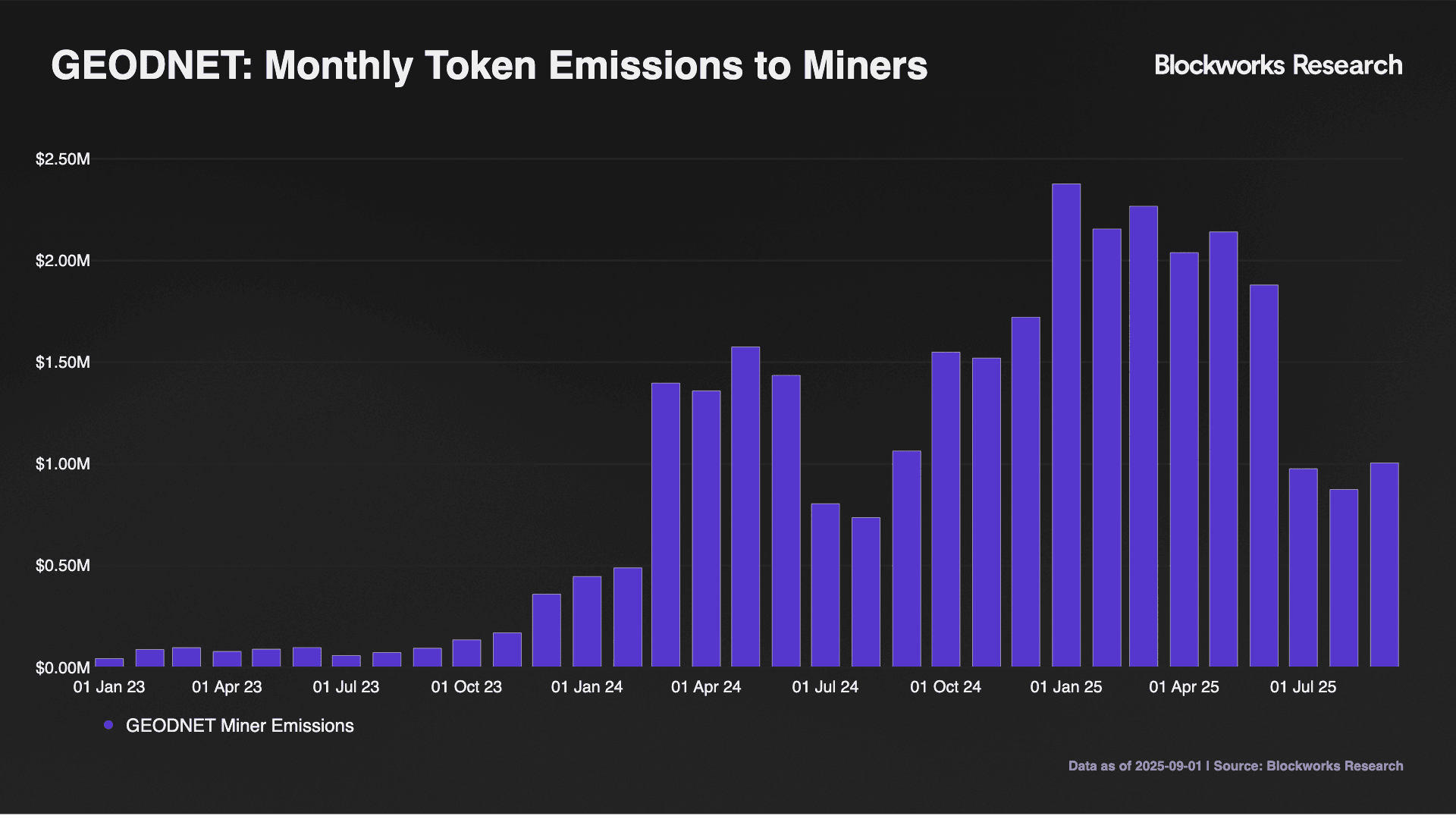

GEODNET utilizes a 50/50 revenue share with third-party web2 re-sellers and wholesalers, allowing different use cases to command different price points while maintaining competitive market positioning. The foundation employs an innovative buyback-and-burn mechanism where 80% of network revenues are used to purchase GEOD tokens in the open market, which are then permanently burned, and the remaining 20% flows to the foundation treasury. This mechanism provides transparency into revenue trends, with the network currently generating ~$4.5M in trailing 30-day burns, representing ~290% growth from late 2024 levels. Monthly burns have increased from approximately $200K in early 2025 to over $376K in September 2025, indicating accelerating revenue momentum. This creates direct value accrual to token holders that is superior to traditional share buyback models, as burned tokens can never be re-issued. However, achieving net token deflation, where burned tokens exceed newly emitted tokens in USD value, requires the network to reach ~$15.1M in total ARR, assuming current emission schedules and the 80% revenue burn rate remain constant.

Individual node operators benefit from a revenue-splitting system where earnings from a single Base Station can be proportionally allocated between a main account wallet and a profit-sharing wallet, enabling flexible business arrangements between hardware owners and location providers. Additionally, fractals.fun recently added support for fractionalized GEODNET deployments to its platform, allowing users to contribute USDC in exchange for a proportional amount of future rewards.

The network's revenue streams remain fundamentally untethered to crypto market cycles, continuing to generate steady ARR from diverse web2 customer segments spanning agriculture, construction, logistics, and emerging autonomous technologies. This revenue diversification provides stability in an otherwise volatile crypto landscape and appeals particularly to traditional finance investors seeking exposure to infrastructure plays with real-world utility.

However, reaching ambitious ARR targets of $40M and $100M requires patience due to enterprise deployment cycles. Notably, the ~$15.1M ARR threshold for net deflation sits comfortably below these targets, suggesting that meaningful deflationary pressure on GEOD token supply should emerge well before the network reaches its ultimate revenue potential.

According to CEO Mike Horton, comprehensive testing and deployment of GEODNET's precision positioning services into enterprise applications can take up to 24 months from initial integration to full commercial deployment. This extended timeline reflects the mission-critical nature of centimeter-level accuracy applications in autonomous vehicles, precision agriculture, and industrial robotics, where extensive validation and certification processes are required before full-scale adoption. While lengthy, this 24-month deployment cycle creates competitive moats once enterprises complete integration, as switching costs become prohibitively high for customers who have built GEODNET's corrections into their core operational workflows.

Market Position and Competitive Advantages

GEODNET's fundamental competitive advantages against incumbents remain intact and have strengthened through recent network improvements. The protocol's cost structure continues to provide substantial pricing advantages, with GEODNET pay-per-connected-device contracts initially priced at $40 per month per device or $400 per year per device, and decline with volume annually compared to incumbent pricing averaging $2.5K for comparable RTK-connected devices. Additionally, GEODNET also facilitates annual wholesale contracts for API access with RTK re-sellers in batches of 100+ stations.

Under the standard 50/50 revenue sharing agreement, GEODNET retains $200 of each $400 annual fee. Integration partners such as positioning device manufacturers like Bynav, Quectel, Ublox, and Septentrio, and wireless module providers serving autonomous vehicle manufacturers, handle customer support, sales integration, and act as the primary customer interface, eliminating the need for a separate GEODNET Labs sales function.

The network's hardware costs remain dramatically lower than traditional RTK infrastructure. While incumbent stations typically cost $5-20K, standard GEODNET Base Stations retail for $700 with zero ongoing rent due to community operation. Additionally, a recent partnership with Wingbits introduced “dual mining” functionality, allowing owners of compatible stations to provide coverage to both networks simultaneously. As outlined in our November 2024 GEODNET report, this cost advantage enables superior geographic coverage, with GEODNET achieving >20K stations compared to ~5K stations across the largest incumbent networks.

Geographic density remains a critical competitive moat. For equivalent $1M deployment budgets, GEODNET can deploy roughly 1.4K stations covering approximately 100K sq. km, while incumbents deploy only 40 stations covering less than 5K sq. km. This coverage advantage directly translates to improved network reliability and customer experience. Legacy incumbents remain constrained by technical debt and proprietary systems dating to early 2000s deployments. Their decade-old GNSS receivers lack compatibility with latest satellite technology, while proprietary RF components prevent cost-effective hardware upgrades. These structural limitations suggest incumbent networks will struggle to match GEODNET's scale and efficiency going forward.

The robotics sector represents a paradigmatic shift in GEODNET's addressable market, with humanoid robots alone projected to reach $5T by 2050 according to Morgan Stanley, while Goldman Sachs estimates the market could hit $38B by 2035 with manufacturing costs declining 40% faster than previously anticipated. The secular growth dynamics are unprecedented: the global humanoid robot market is expected to expand at a 39.2% CAGR through 2035, with Tesla potentially scaling to 1M units annually within five years. Tesla's Optimus program exemplifies the intersection of robotics and precision positioning. With Tesla planning to deploy Optimus robots internally in factories before broader commercialization, and Figure AI's Figure 02 already earning revenue from commercial deployments at BMW facilities, the demand for centimeter-level accuracy in robotic applications is evolving from experimental to mission-critical. While humanoid robotics companies focus on hardware development and securing funding, GEODNET's ~$4.5M in trailing 30-day ARR from enterprise customers provides concrete validation in a market where most robotics plays remain speculative.

Tesla's autonomous vehicle ambitions further amplify these dynamics. The company's robotaxi service launched with 2M app downloads, surpassing early adoption rates of Uber and Waymo, while Tesla continues expanding unsupervised Full Self-Driving capabilities across U.S. cities. With Musk projecting that autonomous vehicles and humanoid robots could make Tesla worth "more than the next top 5 companies combined," the scale of investment and deployment in precision-dependent autonomous systems creates sustained, high-growth demand for GEODNET's RTK infrastructure. Interestingly, the extended 24-month enterprise deployment cycles that challenge robotics scaling benefit GEODNET by allowing time to establish positioning infrastructure as the industry standard before mass autonomous deployments occur.

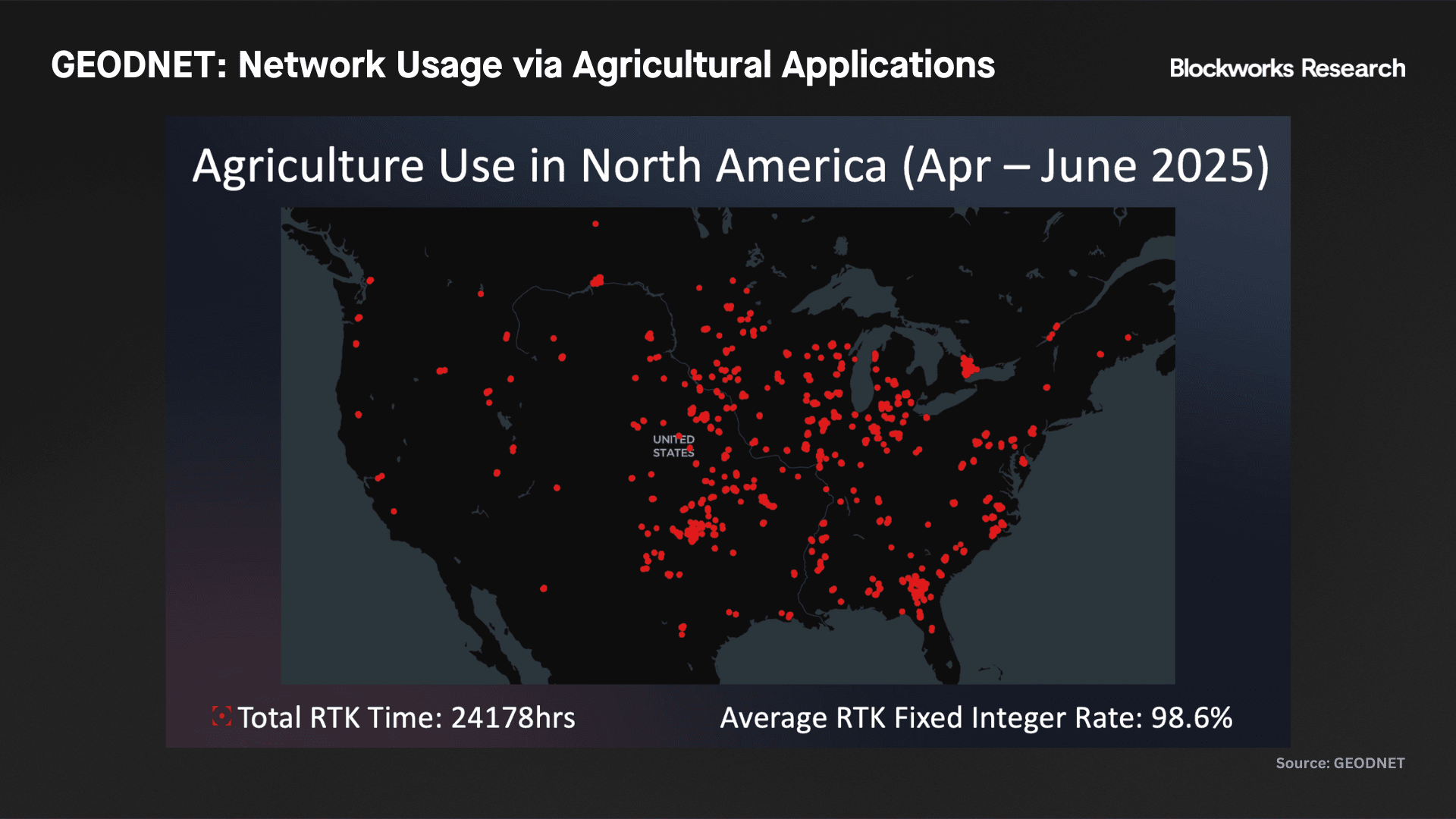

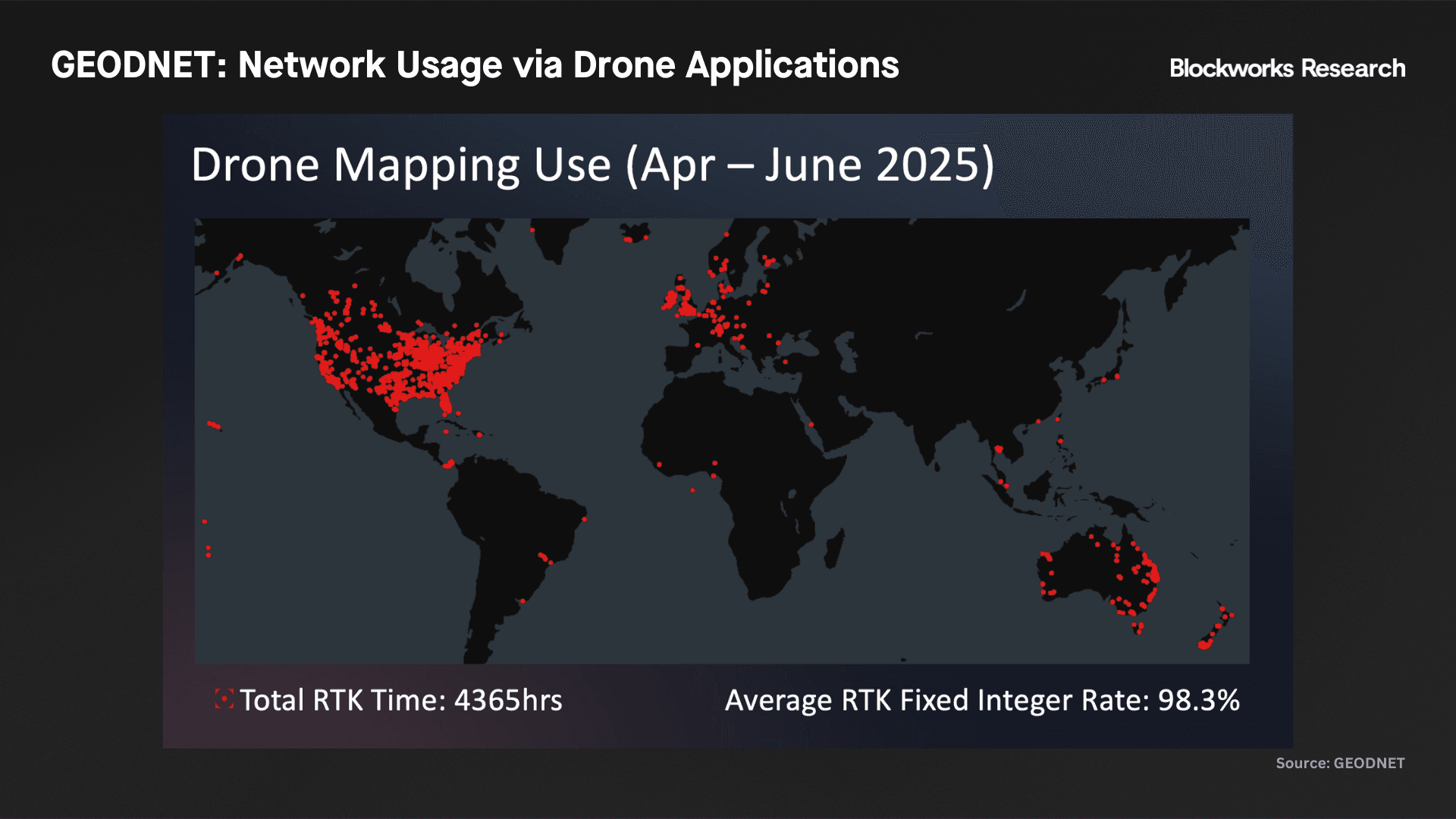

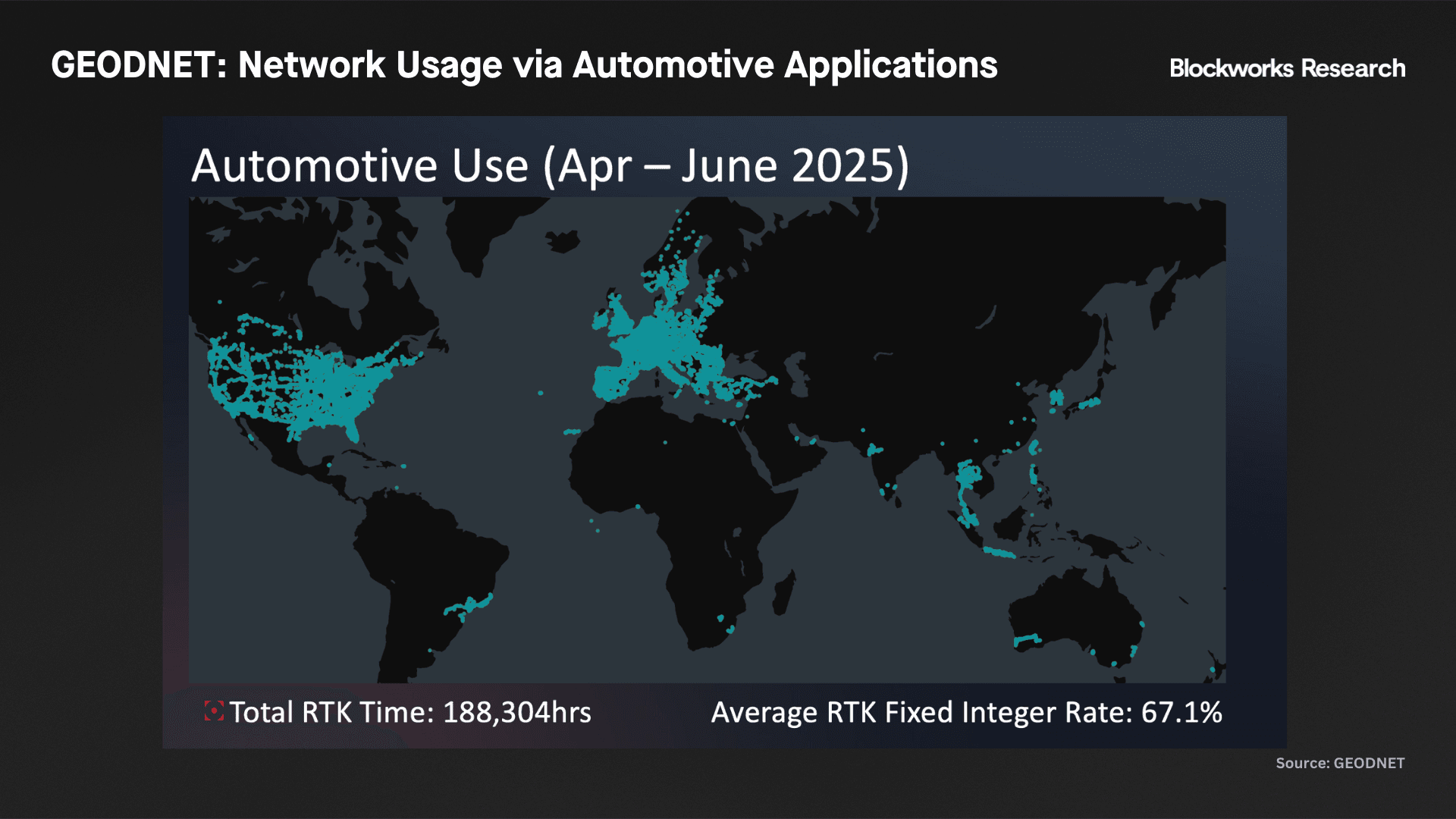

GEODNET's addressable market spans a range of primary growth sectors that significantly outpace GDP expansion rates. Geographic market outlook reveals a maturing network with global product-market-fit (PMF) achieved across core regions, though expansion opportunities remain in strategic markets. In the US, the most lucrative RTK market today, GEODNET has largely completed its buildout, positioning the network to capitalize on the autonomous vehicle and commercial drone boom, markets projected to reach $4.5T by 2034 (37.1% CAGR) and $14.11B by 2033 (9.2% CAGR) respectively. With over 25 states now implementing AV testing frameworks and the commercial drone market already valued at $5.85B in 2023, combined with sales lead times for enterprise RTK contracts typically extending 6-24 months, early market completion provides significant first-mover advantages as demand accelerates. Geodnet has also demonstrated acceleration in the Canadian market, receiving compliance validation from NRCAN, which oversees all RTK networks operating in Canada, allowing surveying use cases to leverage Geodnet across the entire North American continent. Core European markets similarly demonstrate comprehensive coverage. Additionally, precision agriculture technology continues expanding at >4x GDP growth rates. The project's end markets (drones, ag-tech, and IoT) represent multi-billion dollar TAM opportunities where centimeter-level positioning accuracy becomes increasingly critical as autonomous technologies mature.

However, geographic expansion faces distinct regional challenges that highlight both infrastructure constraints and growth opportunities. APAC markets, particularly Japan and Korea, present deployment difficulties due to limited real estate ownership among potential operators, constraining station density in otherwise attractive high-value markets. Conversely, Middle Eastern markets represent significant near-term expansion priorities, driven by accelerating robotaxi deployments, with the market projected to grow from $4.82B in 2024 to $24.89B by 2031 at a 63.4% CAGR, and daily customer pressure for increased coverage fueled by elevated demand for contactless, on-demand transport and widespread pilot program launches across major metropolitan regions. The network's ability to address these geographic imbalances while maintaining cost advantages will determine its competitive positioning as autonomous vehicle adoption scales globally.

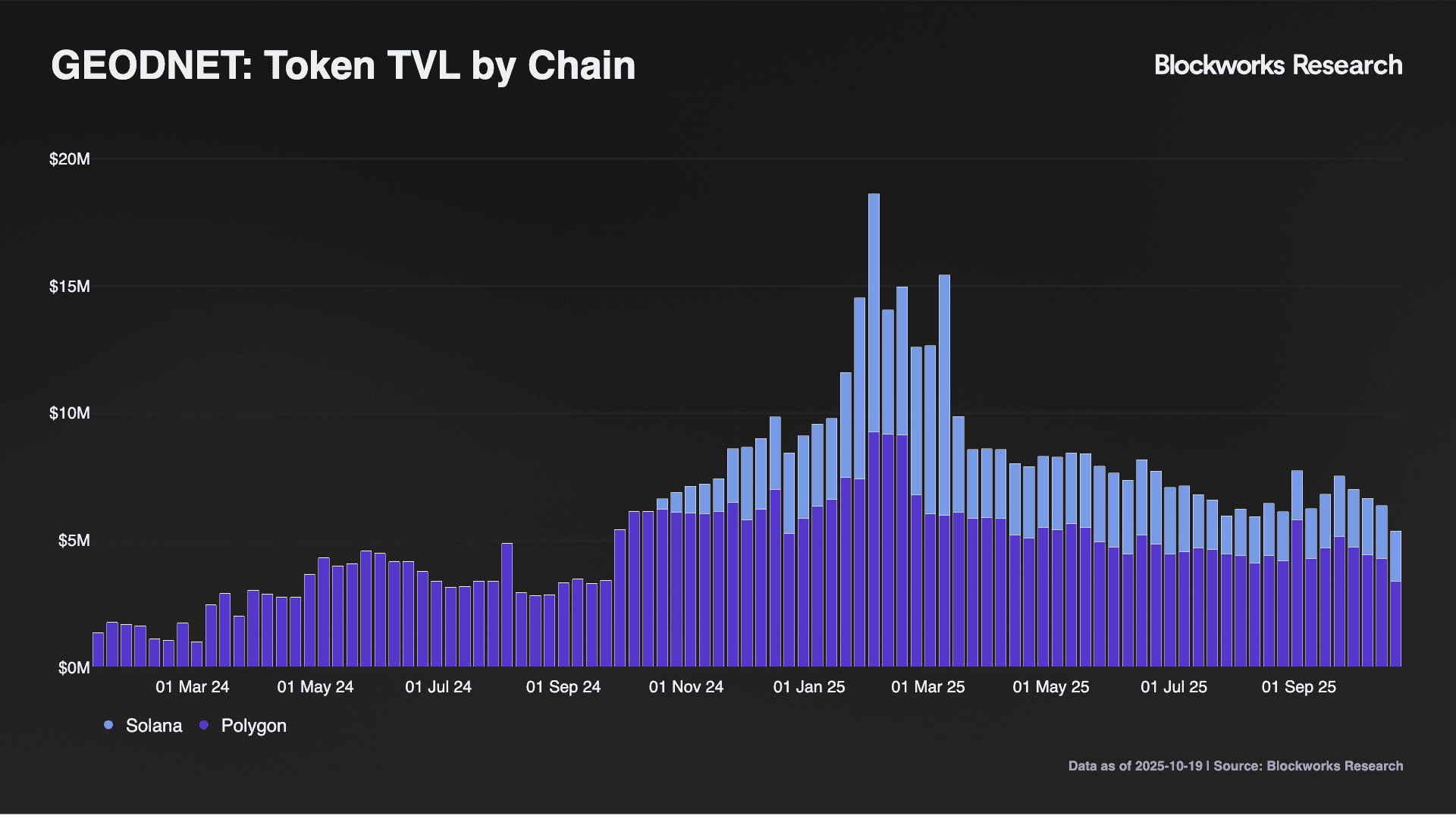

GIP-7: Accelerating Solana Transition

The passage of GIP-7 marks a strategic inflection point for GEODNET's blockchain infrastructure. Starting September 15, 2025, the protocol began implementing a comprehensive migration from Polygon to Solana, driven by the promise of deeper liquidity, simplified user onboarding, and enhanced ecosystem integration.

The migration includes a 30-day incentive program allocating up to 4M GEOD tokens (0.4% of total supply) to token holders who transition from Polygon to Solana between September 15th, 2025 and October 14th, 2025. This migration window provides clear economic incentives while maintaining user choice, with Polygon support continuing until March 2027 to ensure a smooth 18-month transition period.

The strategic importance of this transition was emphasized by key stakeholders, with GEODNET investor Santiago Santos noting that when he invested, "what I asked Mike to give me a soft commit on was redeploying on Solana." This investor confidence reflects broader recognition of Solana's technical advantages and ecosystem potential for GEODNET's growth trajectory.

The Solana migration addresses several operational improvements. Solana's superior throughput and lower transaction costs benefit both node operators and enterprise customers requiring frequent positioning data updates. Additionally, Solana's growing DePIN ecosystem provides natural synergies for GEODNET, particularly with projects that could complement GEODNET's infrastructure with enhanced connectivity solutions.

GIP-8: Strengthening Network Quality Through Location NFTs

GIP-8 represents perhaps the most significant operational improvement in GEODNET's recent history, introducing critical supply constraints that fundamentally alter the network's tokenomics. The proposal establishes a 20K cap on active Location NFTs (reduced from 100K) while implementing strict performance requirements that prioritize network quality over quantity, creating a scarcity-driven model. Currently, ~4.3K unique owners hold ~11.8K Location NFTs, with significant concentration among top holders, with the largest holder owning 279 NFTs and the top 10 holders controlling approximately 13% of all NFTs.

Under the new framework, only stations maintaining at least 98% Real-time kinematic Reception Rate (RRR) can earn Location NFTs, while stations must maintain RRR at or above 80% to retain existing NFTs. This "one NFT per Hex" policy ensures that the highest-performing station in each geographic area claims the NFT, preventing underperforming stations from blocking superior alternatives. Critically, this mechanism creates a direct link between network utility and supply limitation, where only the most productive infrastructure contributors can access the primary reward mechanism.

With the 20K NFT cap and stricter performance requirements, GEODNET effectively implements supply control through merit-based allocation, ensuring that only high-quality stations can earn full rewards. This approach mirrors successful DePIN supply management strategies where token emissions or reward access become increasingly competitive as networks mature. The team's emphasis that "only some stations will earn full rewards, which will limit supply coming to the market" signals a transition from growth-phase incentives to a sustainable, quality-focused model that should support long-term token value.

These changes create several competitive advantages. First, they incentivize only high-quality station deployment, improving overall network reliability and customer satisfaction. Second, they eliminate geographic congestion where multiple low-performing stations previously competed within the same coverage area. Third, they enhance reward predictability for node operators while creating artificial scarcity that should support token value through improved network utility and controlled supply distribution.

The implementation timeline targets early October rollout, with development already underway. This rapid deployment demonstrates GEODNET's operational agility and commitment to evolving its economic model toward sustainability and value creation rather than pure network expansion. The ~97% approval rate validates strong community support for prioritizing network quality and token value preservation over unlimited growth.

Infrastructure Resilience and DoubleZero Partnership Potential

GEODNET's current backend infrastructure relies on AWS servers managed by the GEODNET Foundation, representing a six-figure monthly operational expense. Recent incidents, including the simultaneous offline status of 200 stations in Turkey due to ISP outages, highlight the importance of infrastructure resilience for enterprise customers who depend on consistent RTK availability.

A potential partnership with DoubleZero presents an intriguing solution to these infrastructure challenges. DoubleZero's specialized fiber optic infrastructure and ultra-low latency networking capabilities could provide redundant connectivity for GEODNET stations, reducing single points of failure while improving data transmission reliability.

DoubleZero has onboarded 400+ Solana mainnet & testnet validators to date, representing ~34% of Solana's mainnet stake. The project has raised $28M and launched its mainnet-beta on October 2nd 2025. The strategic value of combining GEODNET's positioning data with DoubleZero's connectivity infrastructure could create synergistic benefits for both networks.

The symbiotic relationship would leverage DoubleZero's optimized routing to enhance GEODNET's data delivery reliability while providing DoubleZero with additional use cases for its high-performance infrastructure. The GEODNET team disclosed to Blockworks Research that DoubleZero already operates two GNSS nodes on the GEODNET network, establishing a foundation for deeper integration as both protocols mature.

Beyond individual partnerships, DoubleZero's infrastructure represents a foundational shift for the broader crypto ecosystem by addressing the fundamental networking bottlenecks that have constrained blockchain performance since inception. The protocol's specialized fiber network and FPGA-based edge filtration technology could unlock new possibilities for latency-sensitive applications including MEV systems, high-frequency trading operations, and real-time DeFi protocols, while also enabling enhanced performance for L1 and L2 scaling solutions across multiple blockchain ecosystems.

Consumer Hardware Innovation

GEODNET continues expanding beyond enterprise applications into consumer markets. The team recently showcased a prototype consumer-ready sub-250g drone at UAV Expo 2025 in Las Vegas, with finalized specifications expected in the near future. This <$2,000 device, positioned as a Drone-as-a-First-Responder platform, is aimed for use in public safety and investigative applications where current drone technology may not currently be feasible or locally compliant. With regulatory pressure mounting against Chinese drone manufacturer and sub-250g market leader DJI, GEODNET appears to be well positioned to bring its yet unnamed product to market in the US while providing the underlying RTK coverage required for its operation. This consumer-focused product development represents a natural evolution for GEODNET's RTK technology, bringing centimeter-level positioning accuracy to broader applications including recreational drones, personal navigation, and emerging consumer autonomous technologies.

The GeoPulse Device, launched in November 2024, represents GEODNET's flagship consumer product offering a 10x improvement in positioning accuracy compared to traditional GPS with precision down to 0.1 meters. The device features an RTK-enabled GNSS receiver supporting dual-band signals across all major constellations (GPS, GLONASS, Galileo, BDS), integrated inertial measurement unit for dead-reckoning capabilities, and sensor-fusion technology that provides position updates even in challenging environments like garages and tunnels. Users can earn cryptocurrency rewards through "Token Quests" by completing navigation tasks that help verify network coverage and improve positioning accuracy, while the device integrates with IoTeX's decentralized infrastructure for blockchain verifiability.

Additionally, the Solana Seeker phone began shipping in August 2025 with an embedded dual-frequency GNSS receiver, enabling precise Proof-of-Location capabilities via the GEODNET Network.

In October 2025, GEODNET launched GEO-MEASURE, a handheld GNSS RTK receiver providing centimeter-level positioning accuracy. The integrated device supports multi-frequency signals from GPS, GLONASS, Galileo, and BeiDou constellations, with built-in Wi-Fi and Bluetooth connectivity. It includes a 1-year GEODNET RTK subscription for correction data, offers up to 30 hours of battery life, and features cross-platform mobile application support. Target applications include surveying, construction, GIS mapping, agriculture, and utility infrastructure work. The device extends the company's consumer product strategy beyond navigation and positioning into practical measurement applications, making professional-grade accuracy accessible to a broader market.

The consumer device strategy aligns with broader market trends toward accessible autonomous technologies. As regulatory frameworks continue evolving to support drone delivery and autonomous vehicle deployment, consumer-grade RTK devices could capture significant market share in applications previously limited to enterprise customers.

Conclusion

GEODNET's strategic positioning continues strengthening through operational improvements, geographic expansion, and technological evolution. The protocol has successfully navigated the transition from speculative DePIN project to revenue-generating infrastructure provider while maintaining its core tokenomic and competitive advantages.

GIP-7 and GIP-8 represent maturation milestones that address operational challenges while positioning GEODNET for continued growth. The Solana migration provides superior infrastructure for scaling, while Location NFT improvements ensure network quality meets enterprise expectations. These changes preserve GEODNET's cost advantages while improving service reliability and user experience.

The potential DoubleZero partnership illustrates GEODNET's strategic thinking around infrastructure resilience. While not immediately critical, such partnerships demonstrate awareness of enterprise customer requirements and commitment to addressing single points of failure that could impact revenue-generating relationships.

Looking forward, GEODNET's revenue diversification across multiple industries provides stability while autonomous technology adoption accelerates demand for centimeter-level positioning accuracy.

The protocol's first-mover advantage in decentralized RTK networks, combined with superior economics and continuous operational improvements, positions GEODNET to capture increasing market share from legacy incumbents and exemplifies sustainable DePIN value accrual.

GEODNET’s has helped to found the recently launched Intercognitive Foundation, working with other Web3 projects (Peaq, Mawari, Auki, and Tashi) building in or adjacent to the robotics space to establish clear standards for AI accessibility & interoperability. The gap between robotics industry funding announcements and real-world deployment capabilities validates GEODNET's revenue-first approach, positioning the protocol as essential infrastructure for the autonomous economy.

Key risks include network reliability challenges inherent to community-operated infrastructure, regulatory hurdles affecting autonomous technology adoption, and the ongoing experimental nature of DePIN tokenomics. However, GEODNET's revenue-generating status, diverse customer base, and operational improvements suggest the protocol is well-positioned to navigate these challenges while maintaining competitive advantages over traditional RTK providers.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. This is a sponsored report commissioned by GEODNET. While Blockworks Research maintains editorial independence, readers should be aware that GEODNET has compensated Blockworks for this analysis. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.