This research report has been funded by Securitize. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Securitize. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

From Wrappers to Venues

Key Takeaways

- Tokenized equities have scaled ~30x to ~$1B since late 2024, yet still represent <0.01% of the $120T+ global equity market, highlighting substantial upside as major exchanges (NYSE/Nasdaq) move toward launch in Q2 2026.

- The market is transitioning from fragmented, offshore synthetic exposures to issuer-sponsored, legally anchored models, enabling canonical onchain shares with full rights, lower counterparty risk, and alignment with existing financial market infrastructure (FMI).

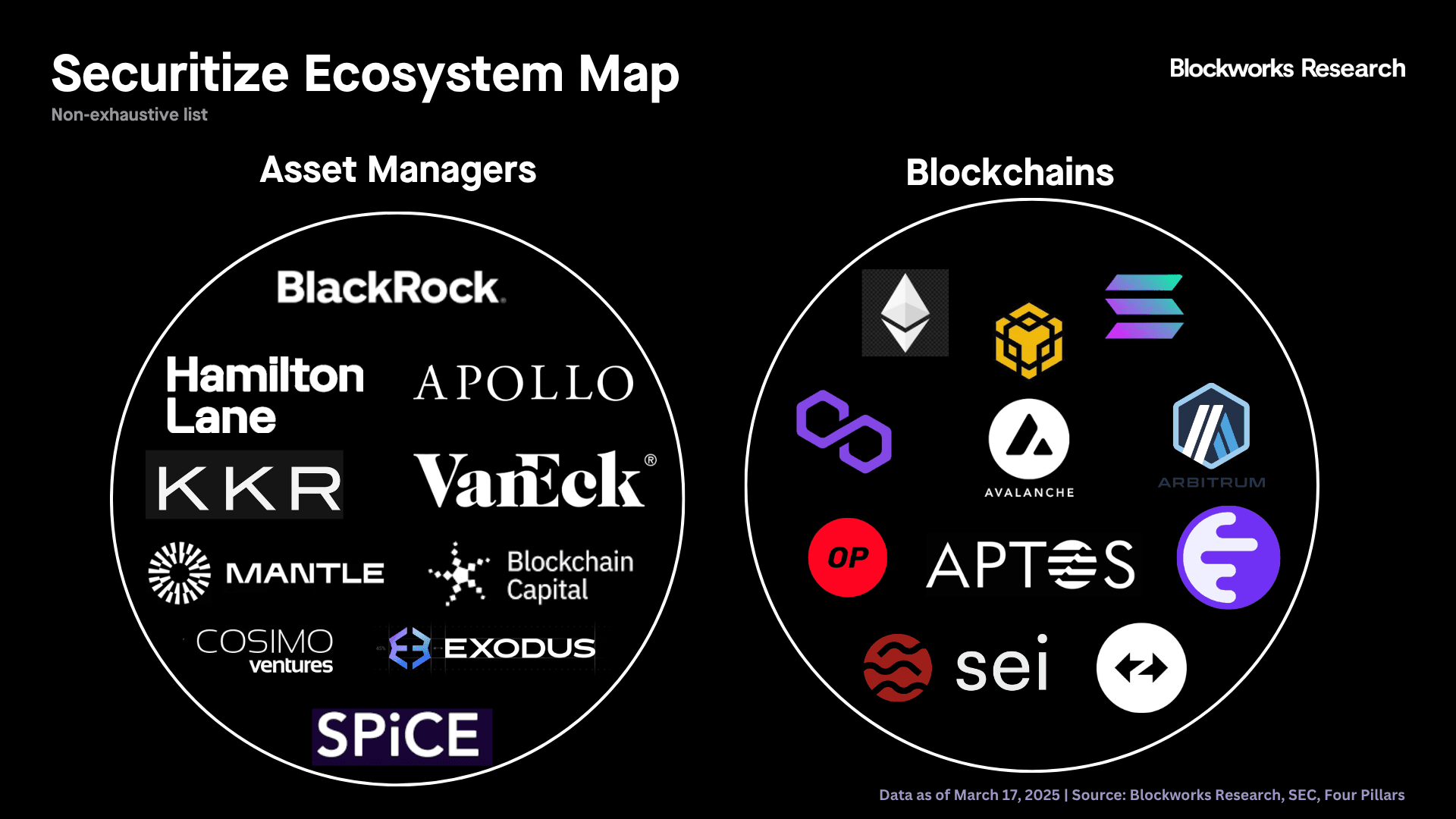

- Tokenization is converging around a small set of regulated platforms, with Securitize leading (~14% share) by offering an integrated stack (issuance, compliance, transfer agency, and distribution), positioning it as core infrastructure for institutional adoption.

Market Overview

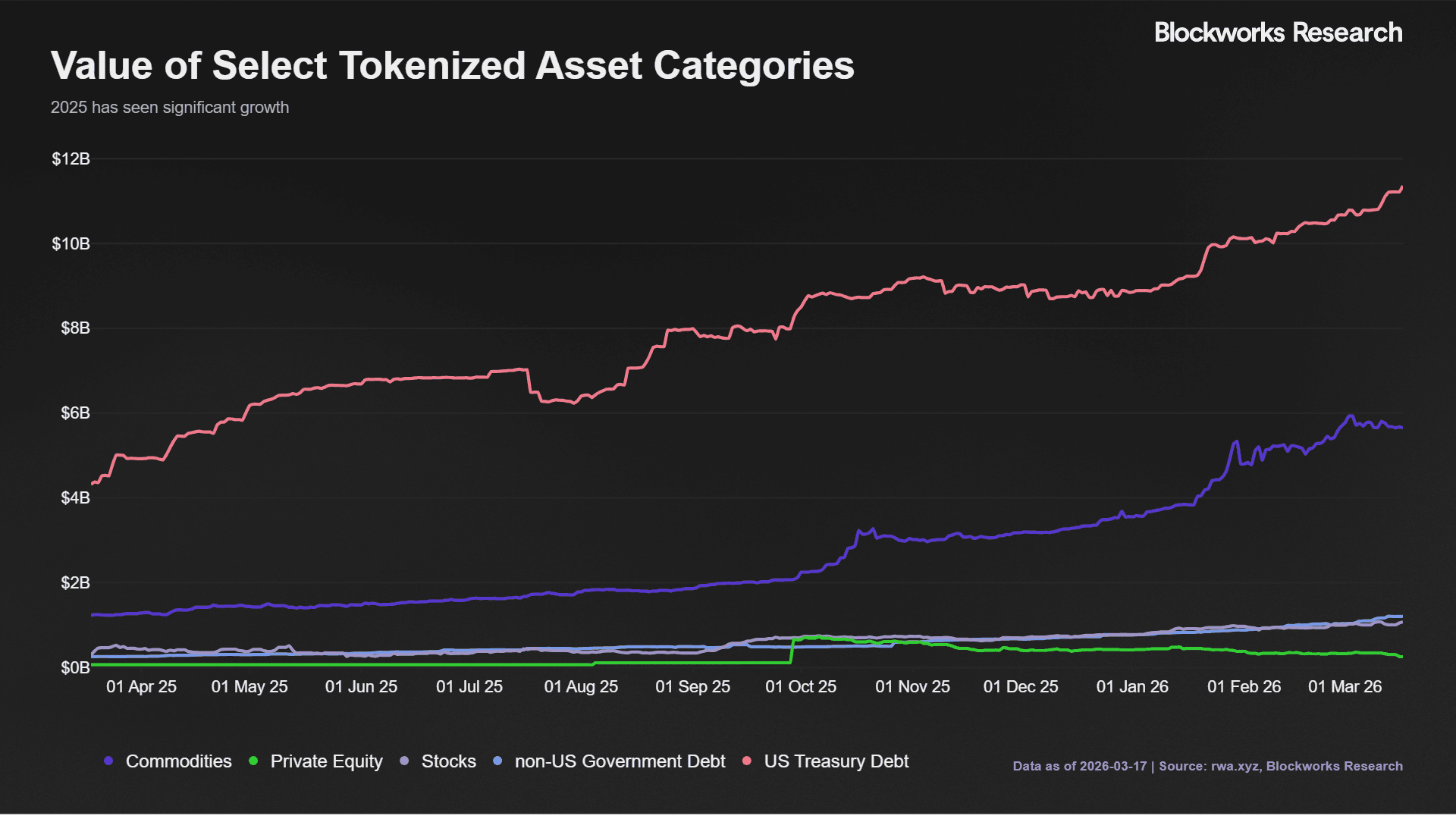

Tokenization has clearly moved beyond experimentation and into early production-scale adoption across fixed income, fund shares, and private-market exposures. The most mature segment today is tokenized cash equivalents, primarily Treasuries and money-market funds, where flagship products such as BlackRock’s BUIDL and VanEck’s VBILL have become reference points for institutional activity. These instruments give institutions a regulated and operationally sound entry point to onchain finance, pairing 24/7 settlement, programmatic distributions, and composability with the familiar risk profile of short-duration government securities rather than crypto-native volatility.

Recent market-sizing estimates reinforce this shift from proof of concept to production. As of April 2026, public dashboards place tokenized Treasuries as the largest segment, at $13B, with commodities approaching $6B as of March 2026. While methodologies differ, these numbers should be viewed as directional indicators, not precise absolutes — the overall trend is unmistakable.  Looking at the tokenization platforms, Securitize currently leads the tokenization platform landscape with ~14% market share (as shown below). Securitize, through its affiliates, doesn’t just issue tokens; it bundles compliance (KYC/AML), transfer agent services, broker-dealer capabilities, blockchain issuance, and fund administration into a single workflow. That integrated stack is critical for institutions that need legal clarity and operational simplicity, which is why activity clusters heavily rather than fragmenting across dozens of protocols.

Looking at the tokenization platforms, Securitize currently leads the tokenization platform landscape with ~14% market share (as shown below). Securitize, through its affiliates, doesn’t just issue tokens; it bundles compliance (KYC/AML), transfer agent services, broker-dealer capabilities, blockchain issuance, and fund administration into a single workflow. That integrated stack is critical for institutions that need legal clarity and operational simplicity, which is why activity clusters heavily rather than fragmenting across dozens of protocols.

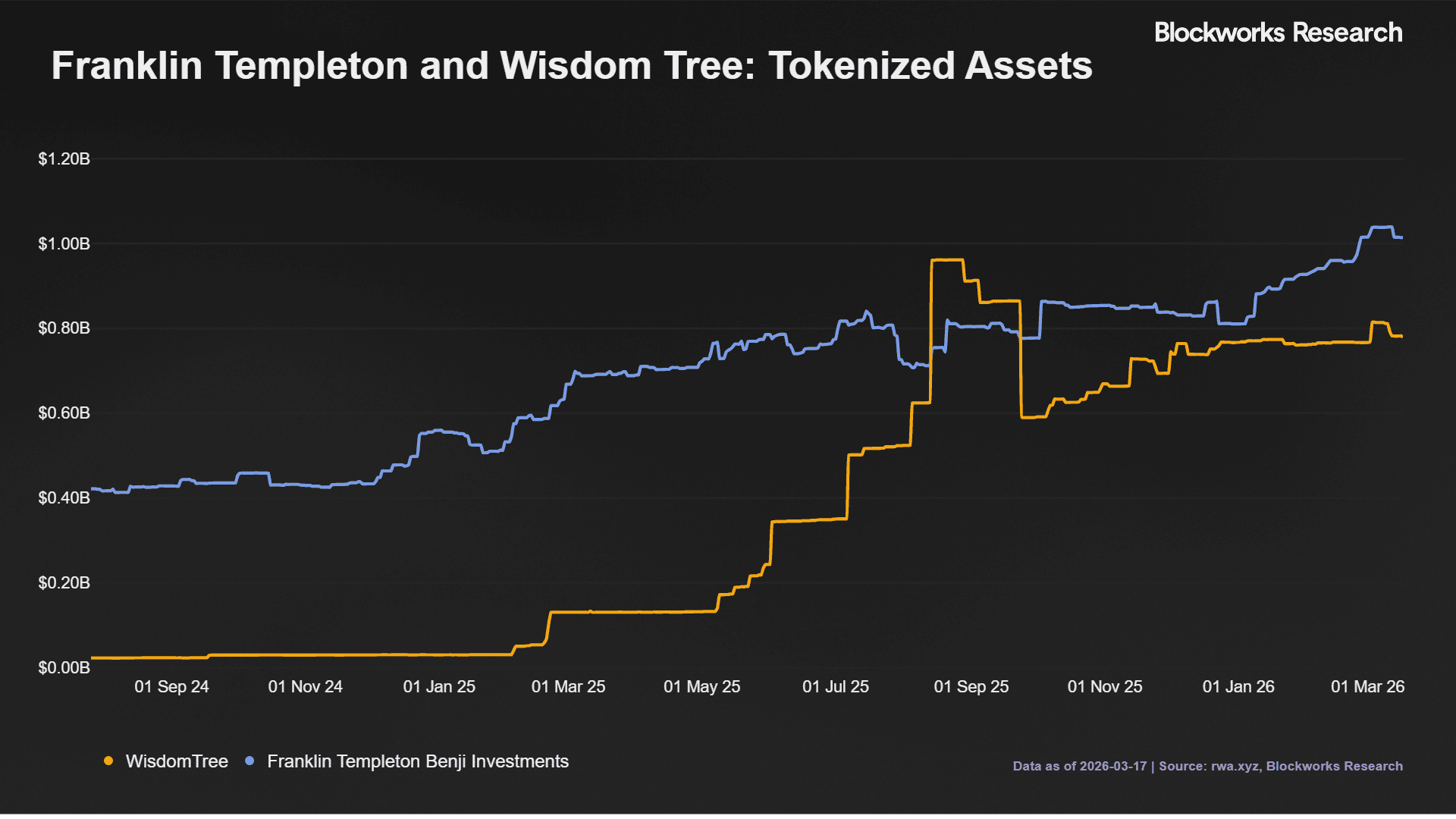

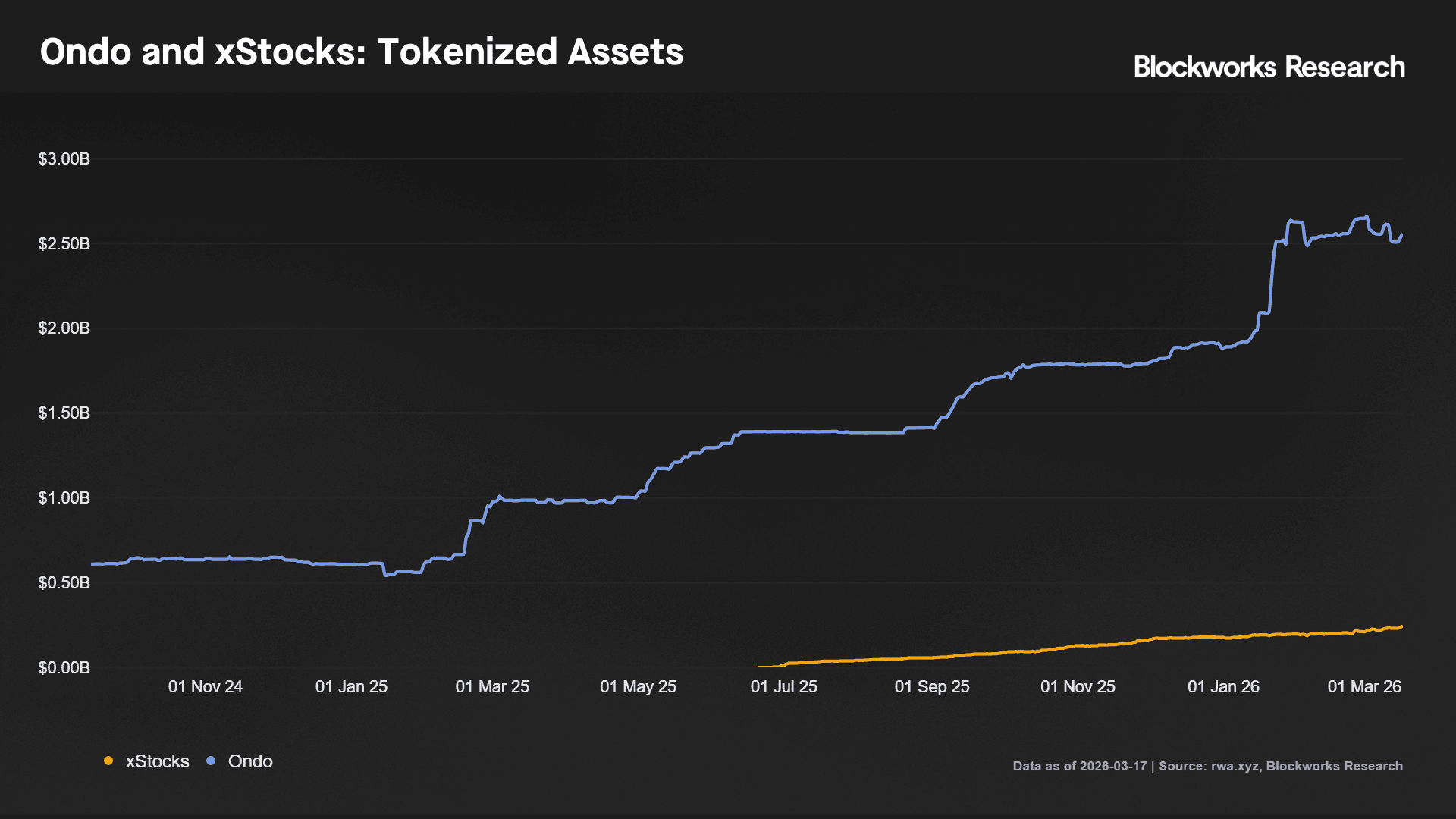

The rest of the landscape reinforces this pattern. Players like Tether (~10.8%) and Ondo (~9.45%) capture demand through product-led distribution, primarily through price exposure only, yield instruments and gold. Meanwhile, Franklin Templeton and WisdomTree represent traditional asset managers extending existing funds onchain. Despite their brand strength, their smaller shares (~3–4% each) suggest that incumbents are still experimenting rather than fully committing balance sheets and distribution to tokenized rails. For tokenized equities specifically, the market will likely evolve as an oligopoly of regulated platforms rather than an open, permissionless ecosystem. Beyond issuance, the key battleground will be secondary liquidity. Whoever can pair compliant issuance with deep, always-on trading venues (potentially integrating ATSs or onchain order books) will define the next phase of growth.

Current state of tokenized equities

Current state of tokenized equities

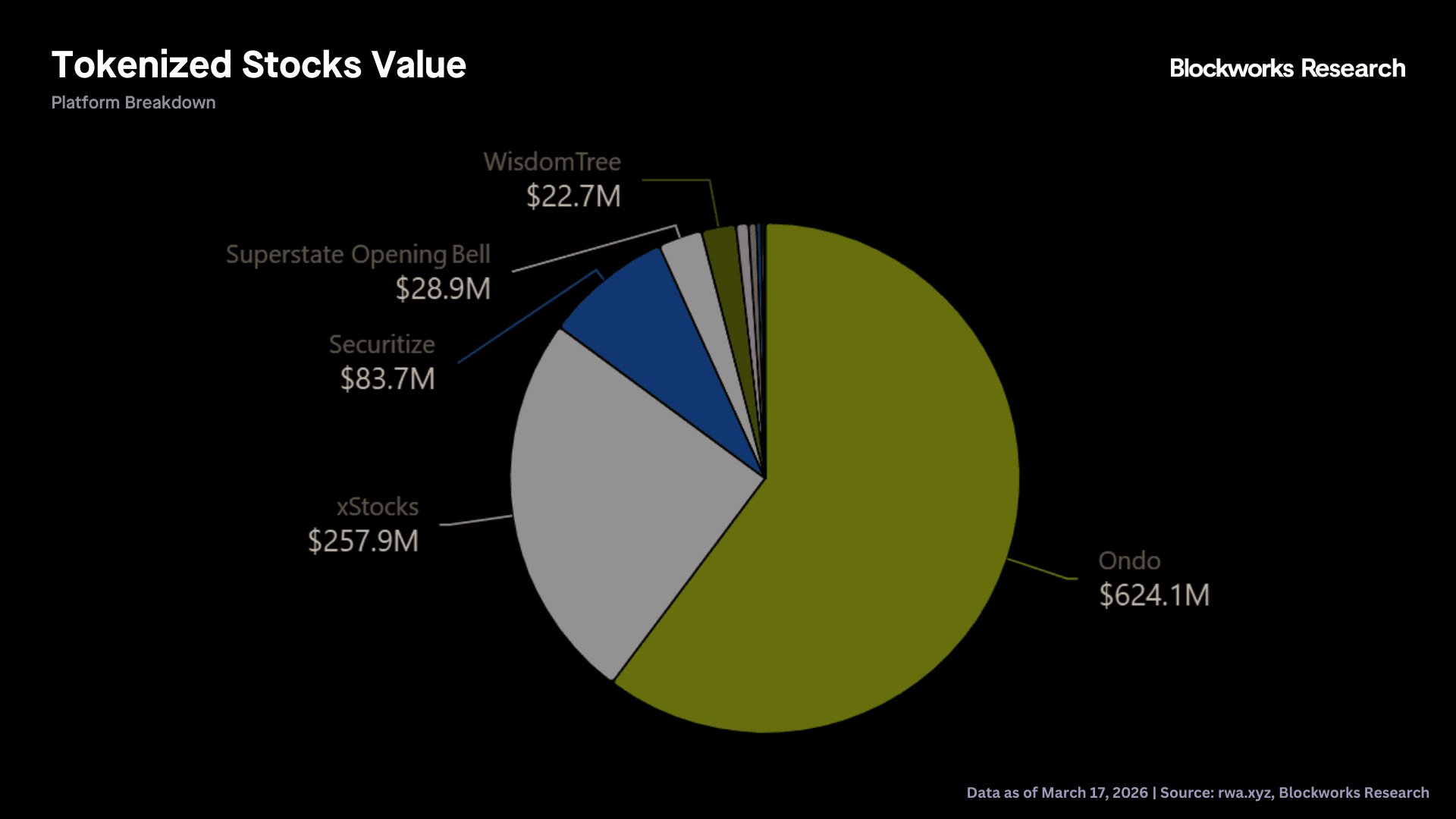

Equities started from a smaller, more experimental base. Over the last year, however, tokenized stocks have gone from a niche to an early‑stage but real market. Multiple data sources indicate that tokenized equities have grown from roughly $30M in late 2024 to around $1B in outstanding value by Q1 2026, nearly 30x growth. Against a global listed equity base north of $120T, $1B is negligible, far less than 0.01% penetration. But within RWAs, equities are now one of the fastest‑growing segments, closing the attention gap with tokenized treasuries even as the latter remain larger by dollars.

Given the relatively small value, today’s tokenized equity market is highly concentrated. A few infrastructure providers and issuers account for the majority of supply and trading. Secondary trading is similarly clustered in a handful of centralized exchanges and onchain venues that support stock‑linked tokens.

However, the structural case for tokenized equities is stronger than for almost any other asset class:

- Liquidity and familiarity: Listed stocks already trade in deep, continuous markets with tight spreads, futures, options and broad index coverage. Tokenization leverages existing demand rather than inventing a new asset.

- 24/7 and global access: Tokenized stocks can trade around the clock on digital venues, letting non‑US and retail investors access US and global names with small tickets and without traditional brokerage friction.

- Fractionalization and distribution: Onchain issuance makes it trivial to fractionalize high‑priced names and distribute positions across wallets and applications, enabling portfolios that mix tokenized equities, stablecoins and other digital assets. Moreover, transactions conducted via blockchain are accessible to investors worldwide.

- Low fees: Tokenized stocks significantly reduce the number of intermediaries involved, allowing investors to benefit from lower fees.

- Settlement and collateral: Tokens can settle near‑instantly and serve as onchain collateral once custody and legal frameworks are in place, mirroring how tokenized treasuries like BUIDL are already posted as collateral on major derivatives venues.

- Smart contracts: Beyond simply holding and trading stocks on a blockchain, investors can leverage stock tokens for a wide range of financial activities through smart contracts.

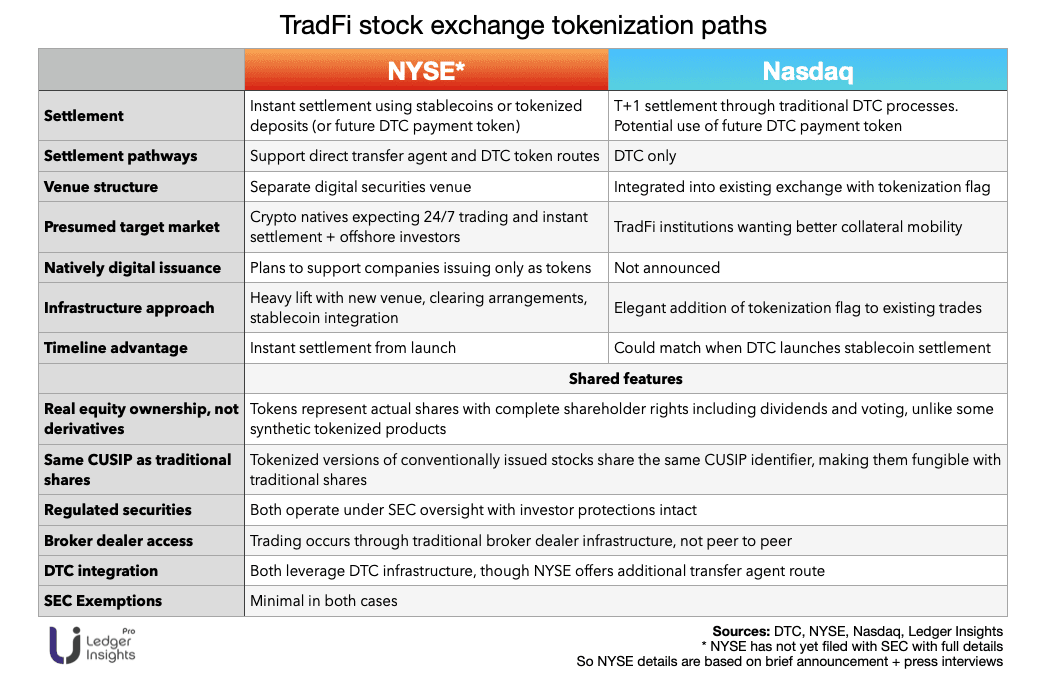

Moreover, Delaware's 2017 amendments to DGCL explicitly authorize corporations to maintain their stock ledger on "one or more distributed electronic networks or databases.” This is why major exchanges are now moving from observation to participation. Nasdaq has outlined multiple initiatives to support tokenized securities and explore extended or 24/7 trading windows via blockchain‑based representations of existing instruments. The goal is to enhance flexibility and settlement efficiency without exiting the regulatory perimeter that governs traditional exchange trading. The NYSE also partnered with Securitize and announced plans for a blockchain‑powered venue that would list tokenized shares fungible with traditionally issued securities, emphasizing near-instant settlement and dollar‑denominated orders. Public materials stress that these tokenized shares would remain legally equivalent to their offchain counterparts and integrate with existing clearing infrastructure.

In parallel, post‑trade and FMI initiatives are exploring the tokenization of large equity indices and treasuries on approved chains, building the collateral and settlement rails required for institutional‑scale tokenized equity markets. Even modest penetration creates a massive addressable market. If tokenized forms capture just low single‑digit percentages of the $120T+ public equity universe over the next decade, onchain equity value would sit in the low trillions, orders of magnitude above today’s ~1B, and large enough to be systemically relevant.

Market structure and fragmentation

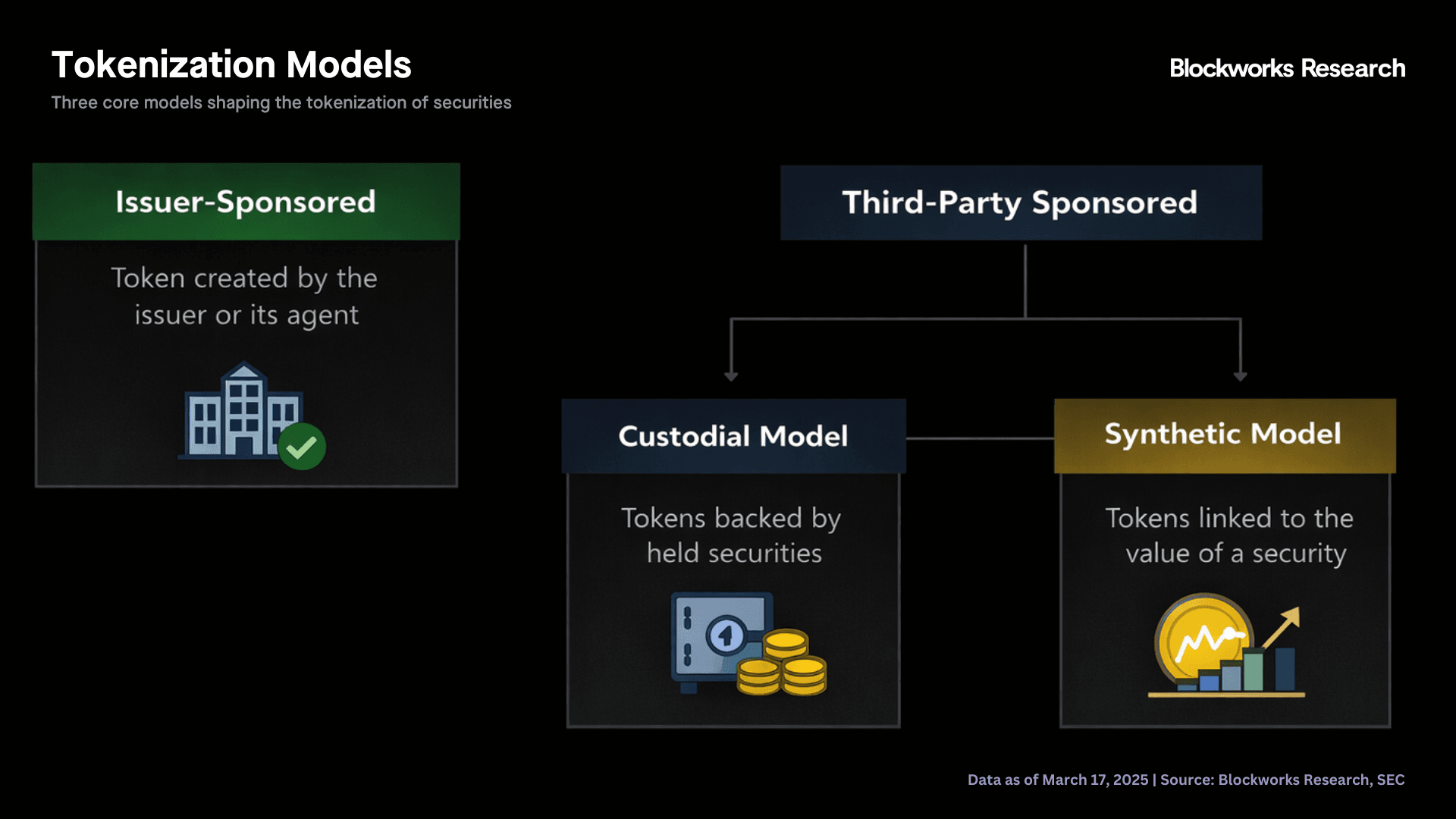

However, tokenized stocks differ fundamentally from fiat or bonds due to their multifaceted rights, economic ownership plus governance (voting), cash distributions (dividends), and corporate actions (splits, mergers), which resist uniform tokenization. Major providers diverge sharply: Securitize pursues issuer-sponsored direct issuance, while Backed and Ondo (NVDAon, NVDAx) favor custodial/entitlement models, and Robinhood deploys EU wrappers/synthetics. The SEC taxonomy frames this as issuer-sponsored (direct from issuer/Transfer Agent, DLT-integrated or mirror recordkeeping) vs. third-party sponsored (custodial entitlements or synthetic exposure), per January 2026 guidance.

Because much of the first generation of tokenized stocks emerged on offshore and crypto‑native platforms, the market today is riddled with multiple, non‑fungible versions of the same underlying names. NVIDIA is a useful illustration: there are several distinct “NVDA tokens” across chains and venues, including NVDAon (Ondo issued), NVDAx (xStocks issued), bNVDA (Backed issued), and others, including synthetic derivatives that simply track NVDA’s price without directly holding the stock. NVDAon and NVDAx are primarily traded on specific onchain venues with differing KYC/whitelisting, while bNVDA is often positioned as an institutional‑grade, fully backed product.

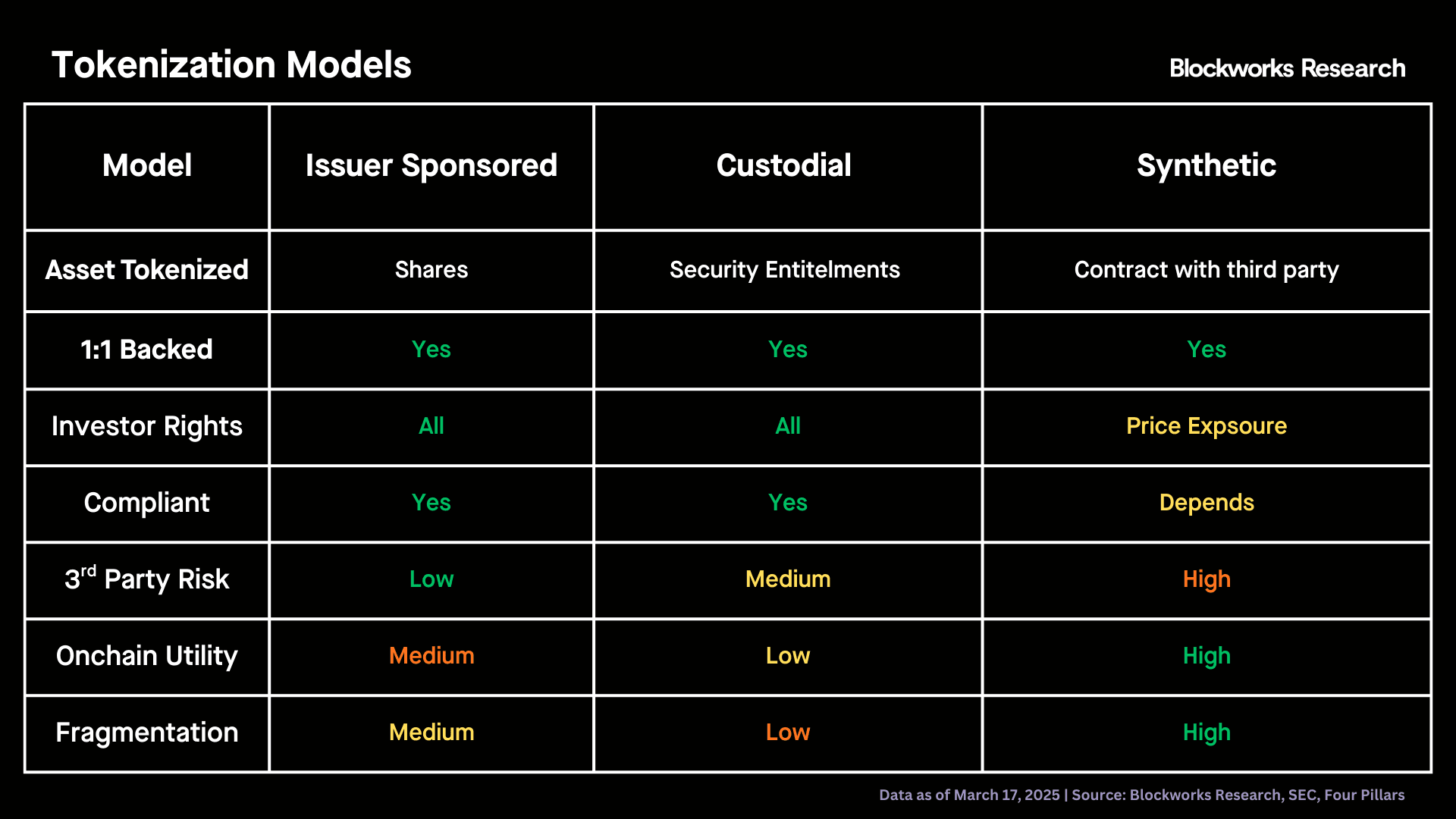

Tokenization Models

Issuer-sponsored (direct) models, where the issuer/TA makes the blockchain the authoritative ledger, deliver low third-party risk (direct claim on issuer), full rights (voting/dividends via TA proxy), and low fragmentation (one canonical token/CUSIP). Onchain utility is moderate — 24/7 trading, some DeFi composability, and high legacy efficiency from integrated settlement. However, it requires issuer buy-in and regulatory setup, slowing initial launches but enabling institutional scale.

Custodial (entitlement) models offer 1:1 backing and full rights but medium counterparty risk (custodian default/reconciliation failure) and moderate fragmentation (multiple custodians per stock). Onchain utility skews low (trading/DeFi limited by offchain dependencies), with medium legacy efficiency. It offers faster deployment than direct, but operational drag from dual ledgers scales poorly for high-volume names.

Synthetic (price-tracking contracts/wrappers) models aim to maximize onchain utility (DeFi composability, leverage) and economic efficiency (no share custody needed) but deliver only price exposure, high third-party risk (wrapper issuer), and higher fragmentation (unlimited competing tokens). Legacy efficiency is low (no true rights), and while ideal for speculation/global retail, it is structurally incompatible with institutional mandates requiring shareholder standing.

Below, we highlight these dynamics. Direct models excel in efficiency/liquidity with minimal risk, custodials balance backing but add silos, and synthetics prioritize utility at fragmentation/rights cost.

BIS confirms optimal tokenization requires authoritative chain recordkeeping for programmability/composability/settlement gains. Issuer-sponsored minimizes "multiple NVDAs" via canonical tokens, while third-party structurally fragments across custodians/wrappers. SEC mandates fungibility (CUSIP/rights parity), custody carryover, and regulated venues over unregulated synthetics. Tokenized equities remain securities, demanding compliance-by-design. As NYSE/Nasdaq consolidate via Q2 2026 venues, direct models should dominate infrastructure economics.

Platform archetypes and leaders

Tokenized equities are now being piloted by a widening mix of brokers, asset managers and banks, with early‑mover activity concentrated on Ethereum and Solana through regulated platforms that span issuer‑sponsored guardians of the ledger, fund‑centric tokenizers, and equity‑heavy custody‑based venues. These institutions use onchain equities for 24/7 settlement, cross‑border distribution, and integration with tokenized cash and derivatives, while still anchoring operations in traditional custody, broker‑dealer, and clearing infrastructure. The ecosystem is coalescing around the three main archetypes aforementioned (issuer-sponsored, custodial, and synthetics), with the former two focused on Treasuries and money‑market products and the latter on equities. Each reflecting different trade‑offs between regulatory integration, onchain utility, and target investor base but all operating under the same “tokenized equities as securities” regime.

Issuer‑sponsored infrastructure: Securitize

Securitize exemplifies the issuer‑sponsored, ledger‑integrated archetype: as a registered US transfer agent, broker‑dealer, and ATS, it issues tokenized equities where the blockchain is the authoritative record, granting full shareholder rights, low counterparty risk, and canonical fungibility (one token per CUSIP). Its platform supports a broad range of assets, including equities, funds, and private securities, while integrating with DeFi rails and major exchanges such as Binance and Deribit, where tokenized products like BUIDL are already accepted as collateral. This is likely why the largest asset managers choose to work with Securitize.

Fund‑centric tokenization: Franklin Templeton and WisdomTree

Franklin Templeton and WisdomTree represent the fund‑centric, primarily fixed‑income/RWA path: Franklin’s tokenized US Treasury money‑market fund (FOBXX, ~$380M) lives on Stellar and other chains, with BENJI tokens enabling peer‑to‑peer transfers and 24/7 onchain liquidity while still backed by underlying government securities. WisdomTree, in turn, has secured SEC approval to trade tokenized shares of its Treasury money‑market fund around the clock, blending round‑the‑clock settlement with regulated fund structures and experimenting with yield‑bearing and options‑overlay tokenized funds.

Equity‑heavy custodial models: Ondo and xStocks

Ondo and xStocks anchor the equity‑heavy, custodial‑synthetic bucket: both platforms issue tokenized US stocks and ETFs that are 1:1 backed by underlying shares held at regulated custodians, but with stronger DeFi and 24/7 trading orientation than traditional issuers. Ondo Global Markets, operating initially on Ethereum and expanding to Solana, targets institutional‑style liquidity and collateralization, with tokens minted against securities held at broker‑dealers like Alpaca and DTC‑linked accounts, while xStocks leverages Backed Finance’s European‑licensed custodial structure and multi‑chain deployment (Solana, BNB Chain, etc.) to serve a more retail‑focused, DeFi‑native audience.

Future Outlook (2026+)

As NYSE and Nasdaq target tokenized equity venues in Q2 2026 with 24/7 trading and DTCC integration, tokenized stocks will transition from fragmented offshore wrappers to regulated infrastructure supporting institutional flows. Interoperability standards will harden around issuer-sponsored models (single canonical token per security), enabling cross-venue liquidity without bespoke bridging while preserving fungibility with primary listings. Notably, issuer activity is already beginning ahead of full exchange integration. Companies like Currenc Group are moving to tokenize equity in anticipation of these venues, suggesting that adoption may be driven by issuers as well as market infrastructure providers alike. Custodians like BNY Mellon and FMIs will expand tokenized equity settlement and corporate action automation, with compliance-by-design (embedded KYC, transfer restrictions) becoming table stakes for secondary markets. Institutional collateralization should deepen as tokenized assets evolve into standard forms of prime onchain collateral for derivatives, repo, and intraday liquidity. We expect this to expand well past the early exchange use cases and echo the broader ambitions seen in large-bank initiatives such as JPMorgan’s TCN model. Permissioned-asset frameworks like ERC-3643 and messaging-layer interoperability via SWIFT-style or CCIP-like protocols can enable cross-venue asset mobility without bespoke bridging. The broader RWA infrastructure stack will continue to build out as custodians, CSDs, and FMIs expand issuance, settlement, and corporate-action automation services. Meanwhile, policy frameworks are poised to mature. The EU’s DLT Pilot revisions, the UK’s Digital Securities Sandbox (DSS), and growing US state adoption of UCC Article 12 will collectively provide greater legal certainty, especially around secured lending over digital assets.

Through 2026, tokenized equity AUM should grow from the current $1B base toward low-double-digit billions as exchanges consolidate the fragmentation problem into unified representations, while direct models like Securitize capture infrastructure economics. Native tokenized share classes from regulated issuers will see faster adoption where transfer agents maintain authoritative onchain ledgers, though scale depends on custodian readiness and SEC taxonomy compliance. This positions tokenized equities, not just treasuries, as prime onchain collateral with programmable settlement and global 24/7 access.

Regulatory and legal landscape

Tokenized equities are being shaped by a patchwork of national‑level regimes that increasingly favor issuer‑sponsored, ledger‑integrated models over offshore wrappers or synthetic contracts. In the US, Delaware’s 2017 DGCL amendments authorize corporations to maintain their stock ledger on “one or more distributed electronic networks or databases,” giving legal grounding to issuer‑sponsored tokens where the blockchain serves as the authoritative shareholder record. Parallel US developments, such as UCC Article 12, treat digital assets as “controllable electronic records,” clarifying rights and secured‑party priority in DLT‑based securities and collateral arrangements.

The SEC’s January 2026 taxonomy for tokenized securities further tilts the field toward issuer‑sponsored structures by splitting the space into (1) issuer‑sponsored tokens, where holders receive direct rights to the underlying security, and (2) third‑party‑sponsored models (custodial entitlements and synthetics), which face higher scrutiny on custody, disclosure, and marketing. Across the Atlantic, the EU’s DLT Pilot Regime is being evaluated for permanence, with ESMA recommending that the framework be extended or converted into a standing regulation to support DLT‑based trading and settlement infrastructures. In the UK, the Digital Securities Sandbox (DSS) grants the Bank of England and FCA powers to disapply or modify existing rules for FMI‑grade pilots, enabling regulated entities to test tokenized equities on DLT under close supervision. Together, these frameworks push the market toward compliance‑by‑design architectures in which tokenized equities remain securities, with clear shareholder‑of‑record status, custody safeguards, and regulatory‑venue alignment setting the stage for issuer‑sponsored models to shine.

Conclusion

Tokenized equities have evolved from experimental wrappers to capital markets infrastructure, with issuer-sponsored direct models emerging as the clear winner over custodial and synthetic alternatives. Platforms like Securitize demonstrate how regulated transfer agents can deliver single-token-per-security fungibility, 24/7 liquidity, and institutional composability while NYSE/Nasdaq provide the primary venue plumbing. The next phase belongs to architectures that eliminate fragmentation and maximize alignment with existing securities law, positioning tokenized stocks as the bridge between traditional exchanges and programmable finance.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.