Equity Perpetuals Landscape Report

Key Takeaways

-

Perpetual futures offer linear payoffs and no time decay, making them the optimal instrument for the $48T monthly 0DTE options demand for leverage (54% of the $89T US options market, spanning equity and index options). Additionally, research shows that virtually 100% of net equity returns occur overnight, yet options force retail execution during a toxic 9:30 AM opening auction. Perps enable continuous capture of news and earnings in real-time, bypassing the structural drag of theta and implied volatility.

-

In terms of regulation, the Shad-Johnson Accord is the binding constraint, effectively banning single-stock perps for US retail by requiring dual clearing infrastructure that does not exist. This structurally sidelines incumbents (Coinbase, Robinhood) and shifts the opportunity to decentralized exchanges. These venues utilize Regulation S exemptions to serve the non-US market (largely APAC-driven), while proliferating into the US via permissionless, decentralized frontends.

-

Onchain architecture solves 24/7 operational limits that plague TradFi. Hyperliquid’s fully autonomous orderbook addresses Futures Industry Association (FIA) concerns around collateral movement, auto-liquidation, and surveillance through pre-funded stablecoin margin and distributed validators, but it cannot currently resolve external banking rails or weekend hedging frictions for real-world assets.

-

Three critical design requirements define viable equity perps: (1) continuous oracles, (2) deep orderbook liquidity to prevent mark volatility and cascading liquidations, and (3) reliable hedging mechanisms that accommodate TradFi’s limited trading hours and T+1 settlement.

-

Ostium’s peer-to-pool model sacrifices 24/7 availability for active risk management. While direct oracle pricing eliminates slippage and offers cheaper SOFR-based funding, the model mandates weekend halts to align with offchain hedging rails. Although this active management reduces LP Value-at-Risk (VaR), the vault has been primarily under-collateralized for 85+ days, indicating that the costs of maintaining these hedges against informed flow continue to pressure the system’s two-tier buffer.

-

Hyperliquid's HIP-3 model establishes a powerful moat, processing $9.4B in equity perp volume in 30 days. Deployers inherit institutional-grade orderbooks and 880k users, with Unit's Trade.XYZ seizing dominance via its spot tokenization monopoly. While Felix competes through USDH denomination (20% lower fees, 50% better maker rebates), the HIP-3 auction-based listing system allows Trade.XYZ to aggressively bid for new markets, erecting significant barriers to entry for prospective entrants.

-

Vest Exchange offers an alternative risk-based model using zkRisk for coherent cross-market pricing and offchain hedging on CME/Nasdaq, attracting sophisticated trading firms (Jane Street, Amber Group) as investors.

-

Solana hosts tokenized spot assets (xStocks) that already trade 24/7. While Hyperliquid leads in distribution, Solana protocols can theoretically utilize the tokenized asset itself as the underlying oracle reference. This eliminates the need for synthetic weekend pricing and enables atomic cross-margining, where xStocks serve as collateral for delta-neutral carry trades without legacy banking friction.

Perpetual Futures Contracts

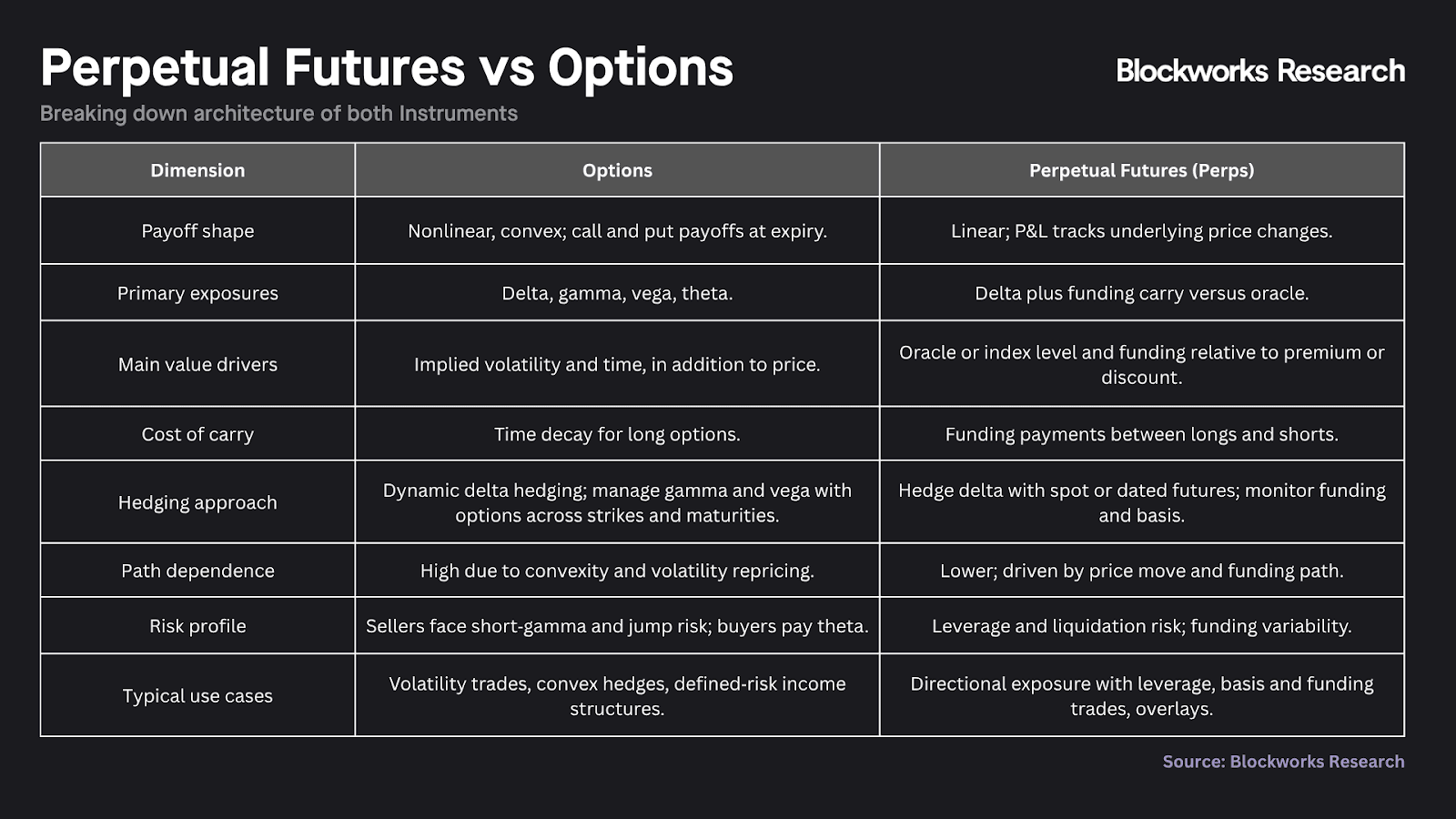

A perpetual future is a cash-settled, delta-one derivative that replicates spot exposure with no expiry. Absent a delivery date, perpetuals offer no direct claim on the underlying asset. Instead, price convergence is enforced via a funding mechanism. This periodic exchange of payments between longs and shorts tethers the contract price to the underlying spot index.

- Oracle Price: A composite reference built from multiple liquid spot venues. Exchanges apply aggregation, such as medians or volume-weighted averages with short smoothing, to reflect underlying spot value while reducing venue-specific noise.

- Mark Price: The exchange’s estimate of the contract’s fair value used for P&L, margin, liquidation, and funding. It blends the oracle with venue-specific signals from the local order book and recent trades, often with short-horizon smoothing, to measure the premium or discount of the perp relative to the underlying.

- Funding: Transfers value between longs and shorts to keep the mark aligned with the oracle. When the perp trades at a premium, funding is positive and increases the cost of carry for longs. Arbitrageurs short the perp and buy spot or dated futures to capture the funding rate, creating sell pressure that drives the mark price toward the oracle. When the perp trades at a discount, funding is negative and makes shorts costly. Arbitrageurs buy the perp and sell spot or dated futures, which lifts the perp toward the oracle.

Positions may be held indefinitely because there is no expiry. Funding provides the economic anchor, while leverage introduces liquidation risk if margin falls below maintenance levels.

Perpetuals are operationally straightforward. Exchanges standardize risk parameters like open interest and max leverage, then feed only mark and oracle price references into the matching engine. Centralized risk engines, insurance funds, and auto-deleveraging limit bilateral counterparty exposure. However, this efficiency requires three critical conditions:

- Robust, continuous oracle: The oracle must run 24/7, draw from deep spot liquidity, apply rigorous outlier controls, and refresh frequently so the mark reflects true market conditions. This favors underlyings with simple cash pricing that avoid dividend, borrow, and stock-split adjustments (e.g., major crypto spot indices).

- Adequate exchange liquidity: Deep orderbooks and stable two-way flow are required to limit mark volatility. Where liquidity is thin, mark-price liquidations become more likely and funding rates can spike as the premium or discount whipsaws. Exchanges mitigate this through structured liquidity programs (e.g., Hyperliquid’s HLP Vault).

- Efficient spot market integration: Traders need a liquid hedge venue and close operational proximity between spot and perps so hedges can be executed immediately, reducing liquidation risk. For example, posting BTC as collateral and hedging on a tightly linked spot venue offers superior capital efficiency and speed compared to hedging TSLA across fragmented traditional brokerages.

These conditions explain why perpetuals have thrived in crypto. In 2022, perpetual contracts reached a median daily volume of $101.9B, supported by 24/7 spot markets, deep venue liquidity, and seamless spot collateral bridging. Other asset classes, such as equities, have seen limited adoption in perpetual futures due to 24/5 trading hours, constrained onchain liquidity, and hedging that depends on traditional rails with operational frictions.

We view perps as efficient tools for linear, spot-like exposure with round-the-clock liquidity. Their potential extends beyond crypto as index construction, venue liquidity, and collateral plumbing converge toward a 24/7 standard.

Options Contracts

An option gives the holder the right, not the obligation, to buy (call) or sell (put) an underlying at a strike price exercisable only at expiry (European-style) or at any point prior to expiry (American-style). Buyers pay a premium and have limited downside. Sellers collect premium and accept open-ended risk for calls and large downside risk for puts.

Value depends on spot (S), strike (K), time to expiry, interest rates, dividends or carry, and implied volatility. Beyond price, implied volatility and time are the primary drivers.

At expiry, a call pays (S – K) when the spot price exceeds the strike, and zero otherwise. A put pays (K – S) when the strike exceeds the spot price, and zero otherwise.

Risk and hedging focus on four core sensitivities. Delta measures first-order price exposure, gamma captures how delta changes as price moves, vega measures sensitivity to implied volatility, and theta measures time decay. Options require dynamic hedging and are path dependent, while perps are mainly driven by price change and the funding path.

We summarize the key differences below for quick reference:

While options were designed for volatility and convexity trading, a significant market segment now uses them primarily for leveraged directional exposure. This is suboptimal: it introduces unnecessary complexities like time decay and implied volatility sensitivity that obscure simple price bets, in contrast, perpetual futures are purpose-built for this use case.

Perps deliver cleaner, more efficient directional leverage. They are intuitive, programmable, and easier for liquidity providers to manage, with no expiry to complicate positioning. While options remain superior for non-linear or dated risk, perpetuals are the more effective instrument for satisfying market demand for straightforward leveraged delta-one exposure.

Framing the Market Opportunity

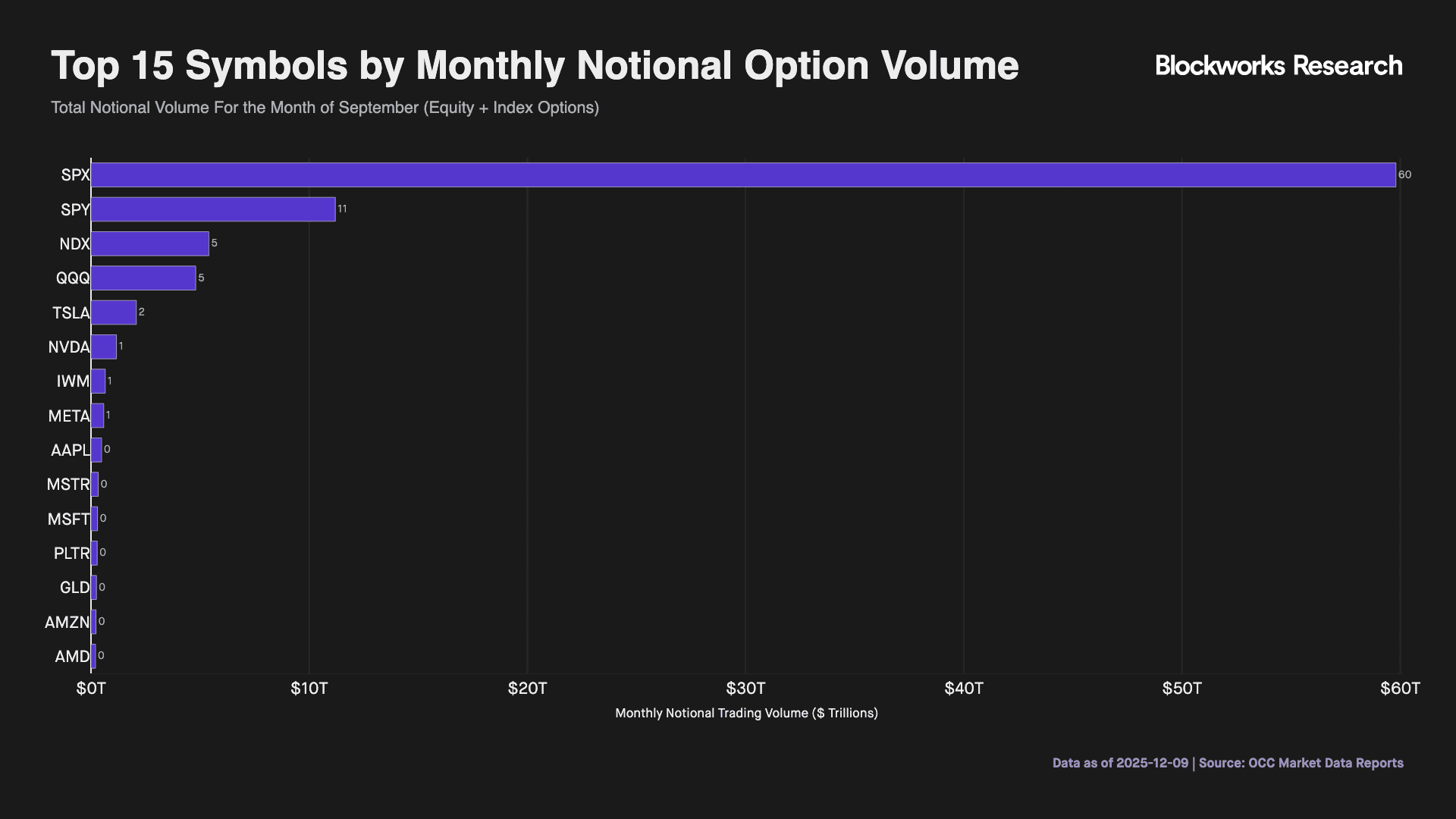

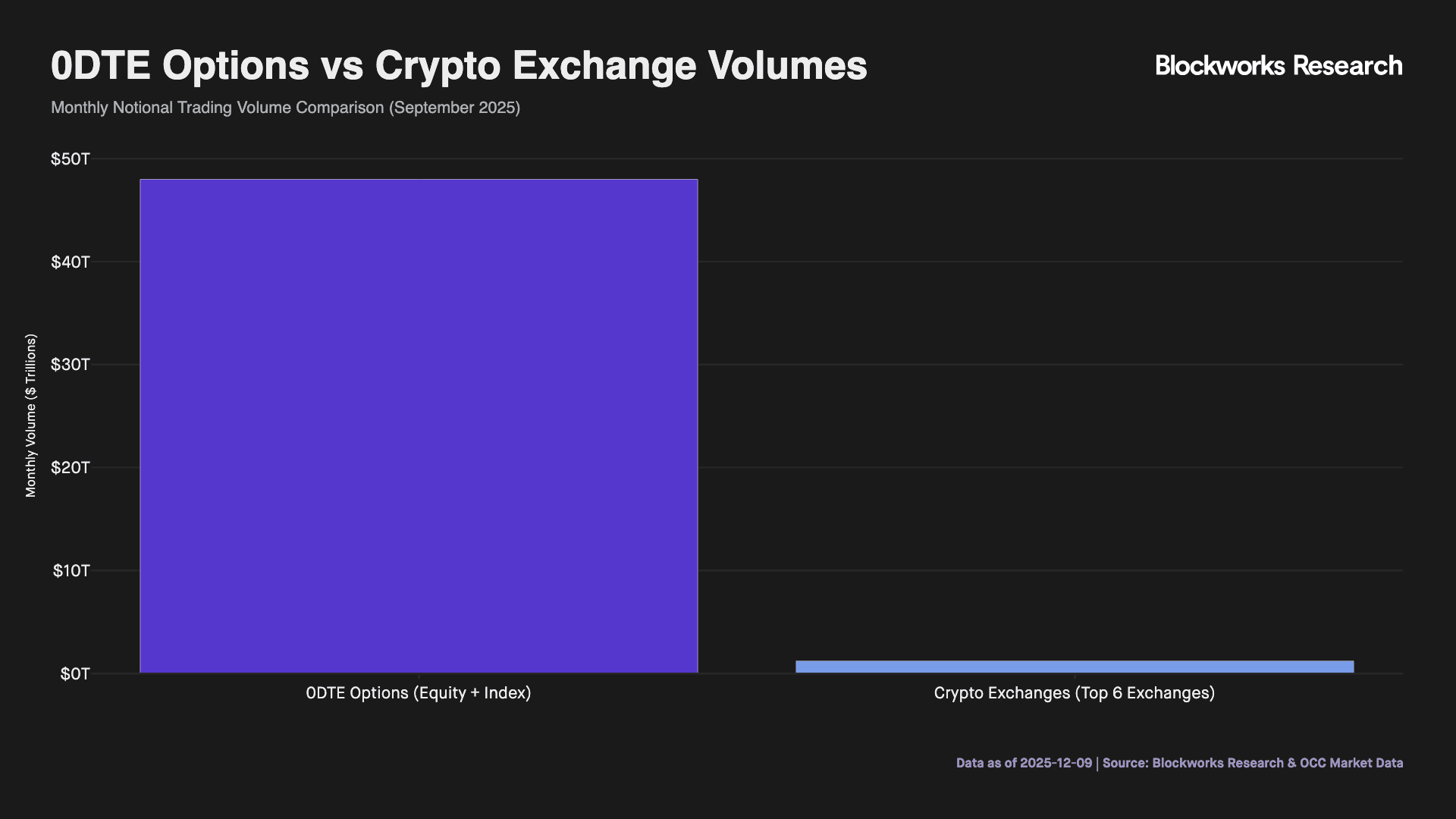

US equity options provide the clearest proxy for perpetual futures' addressable market. The OCC reported 10 billion equity option contracts YTD through September 2025, representing 91.4% of total volume.

Standard contract-based reporting obscures true notional exposure, so we aggregated OCC data across 20 exchanges and converted to dollar terms using closing prices. This includes both equity options (SPY, QQQ, single stocks) and index options (SPX, NDX) cleared through OCC, yielding $89T in monthly notional turnover for September 2025.

Index options dominate this volume. SPX alone accounted for $59.8T (67%), with NDX adding another $5.4T (6%). Among equity options, SPY contributed $11.2T (13%) and QQQ $4.8T (5%), with twelve single-name equities each exceeding $150B monthly

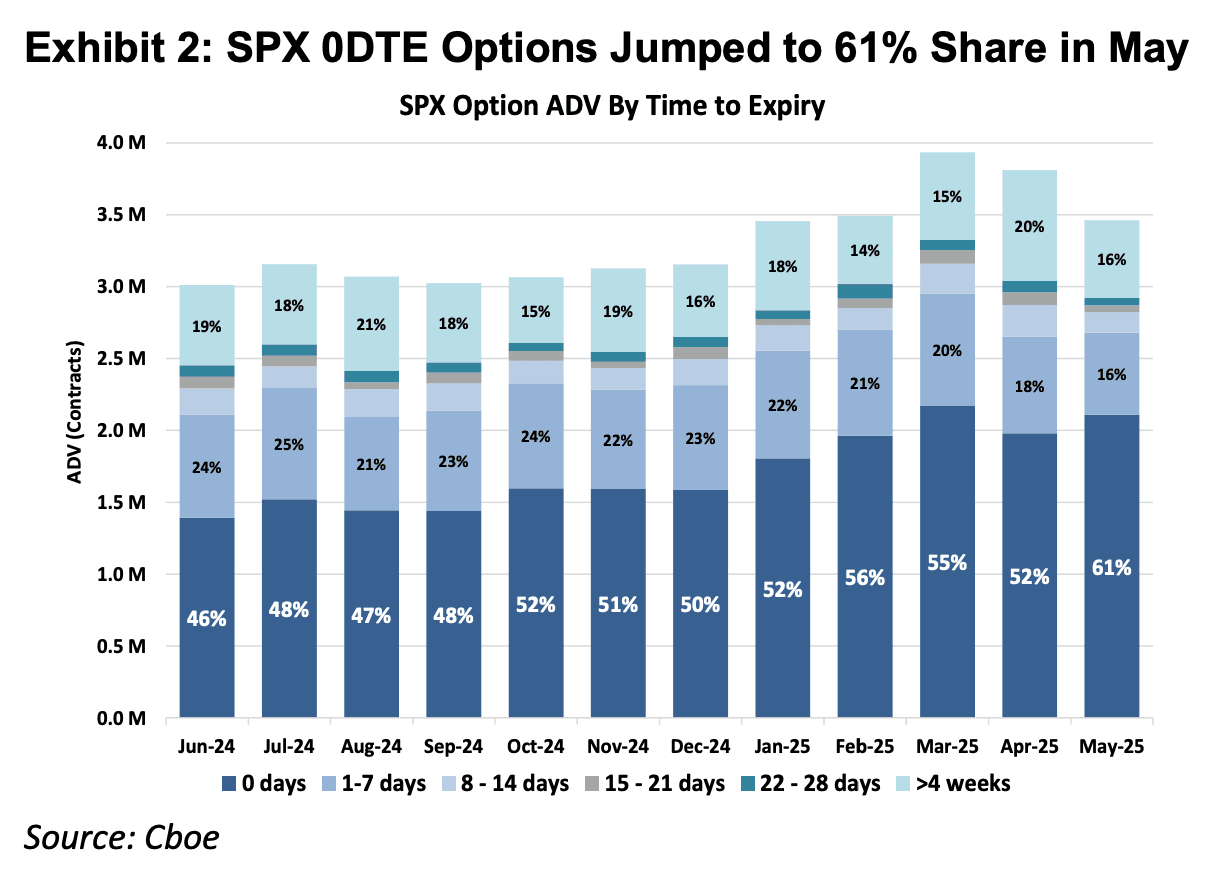

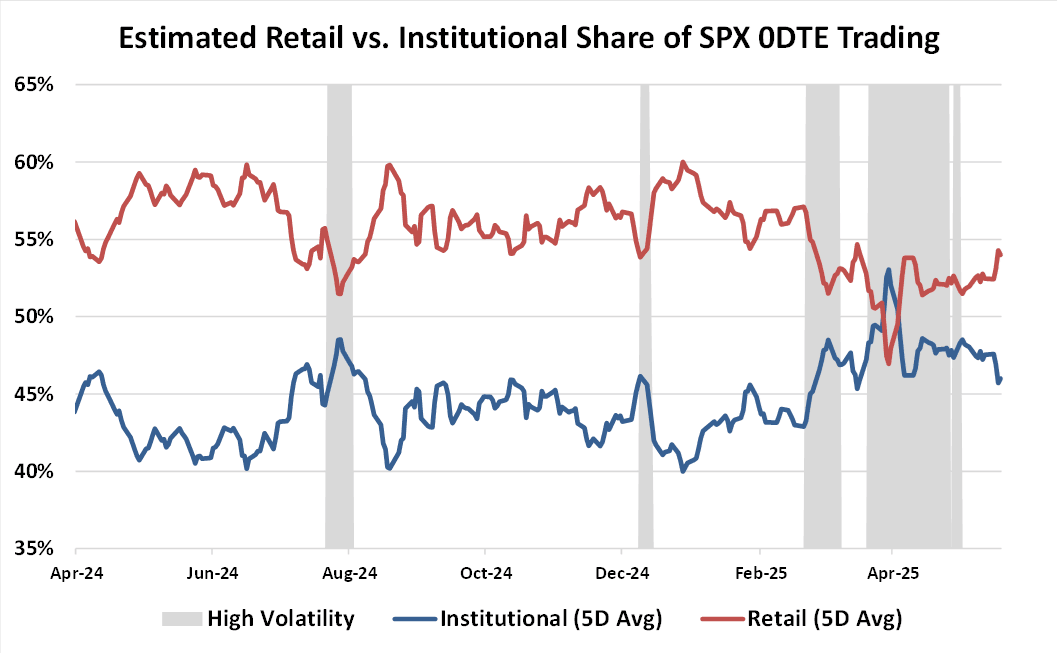

Next we turn to 0DTE options (contracts expiring within one day) as the clearest expression of retail leverage demand, distinct from institutional hedging. In SPX, the most actively traded market, 0DTE volume has increased from 5% of total volume in 2016 to 60–62% today, while contracts with 0–7 days to expiry accounted for 77% of all options volume in May 2025.

Source: Cboe Macro Volatility Digest

Cboe estimates retail traders drive 54% of SPX 0DTE volume, the cohort seeking leveraged directional exposure. These contracts embed median leverage exceeding 200x (10th–90th percentile: 150x–350x), offering convex exposure that incurs extreme theta decay. This represents a revealed preference for short-duration leverage, which perpetual futures can replicate linearly without theta decay.

Source: BIS “What could explain the recent drop in VIX?”

Applying this ratio to our notional value findings, 0DTE volumes imply ~$48T in monthly notional traded value—roughly 40x the $1.2T traded across all perpetuals on centralized crypto exchanges in September 2025

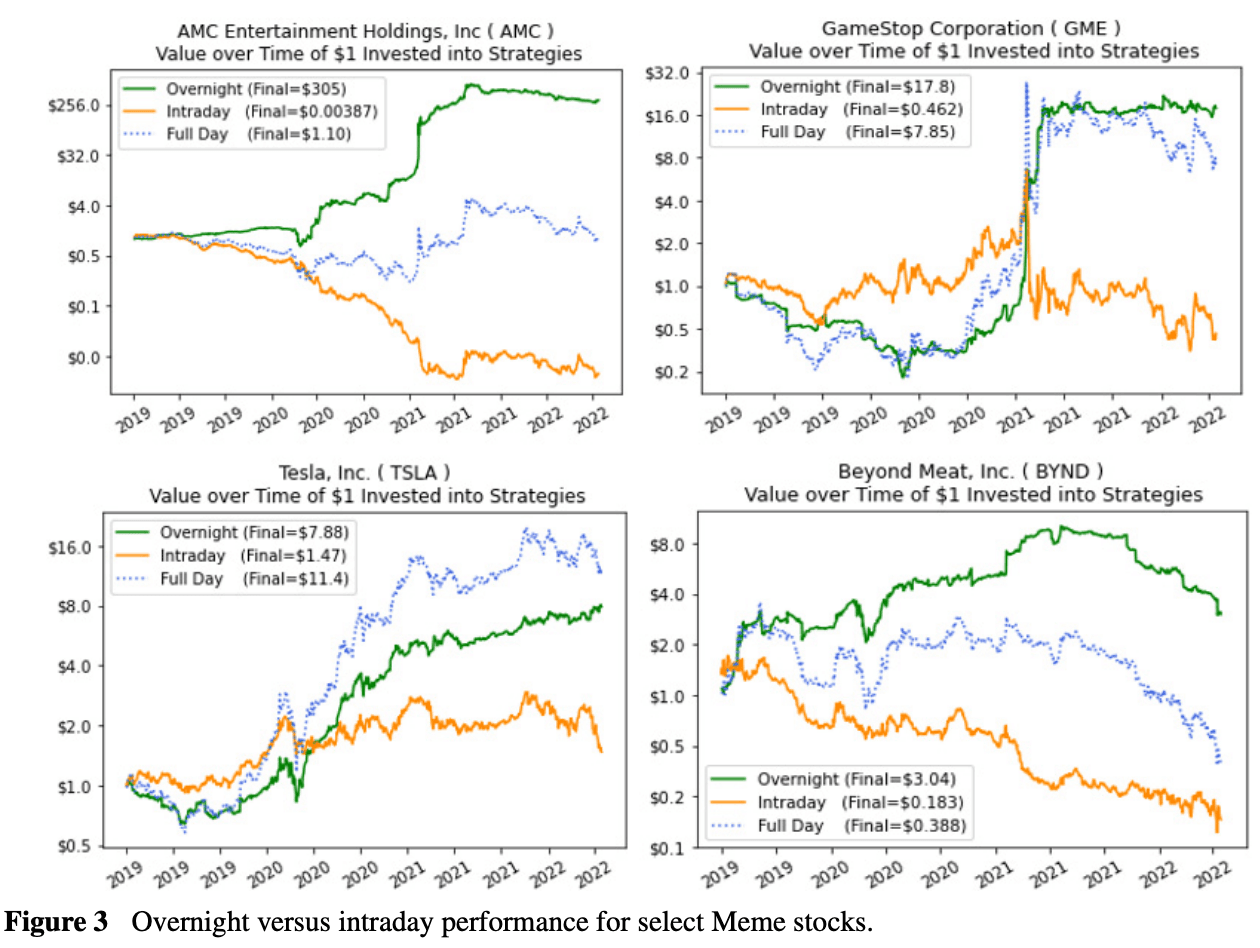

Beyond delta-one efficiency, 24/7 equity perpetuals resolve a fundamental market asymmetry regarding return realization and liquidity pricing. Research shows that virtually 100% of net equity returns occur overnight. Since 1993, the S&P 500 returned approximately 1,650% overnight versus a -13% loss intraday. This divergence is exacerbated in retail favorites like AMC (+30,000% overnight vs. -99.6% intraday).

Source: Is the Overnight Drift the Grandmother of All Market Anomalies?

This friction is most acute around earnings, as approximately 95% of US companies report outside regular trading hours. When a company beats expectations at 4:05 PM, a perpetual futures trader can execute instantly, capturing the move as it happens. In contrast, a 0DTE options trader is structurally locked out until the market reopens at 9:30 AM the next morning.

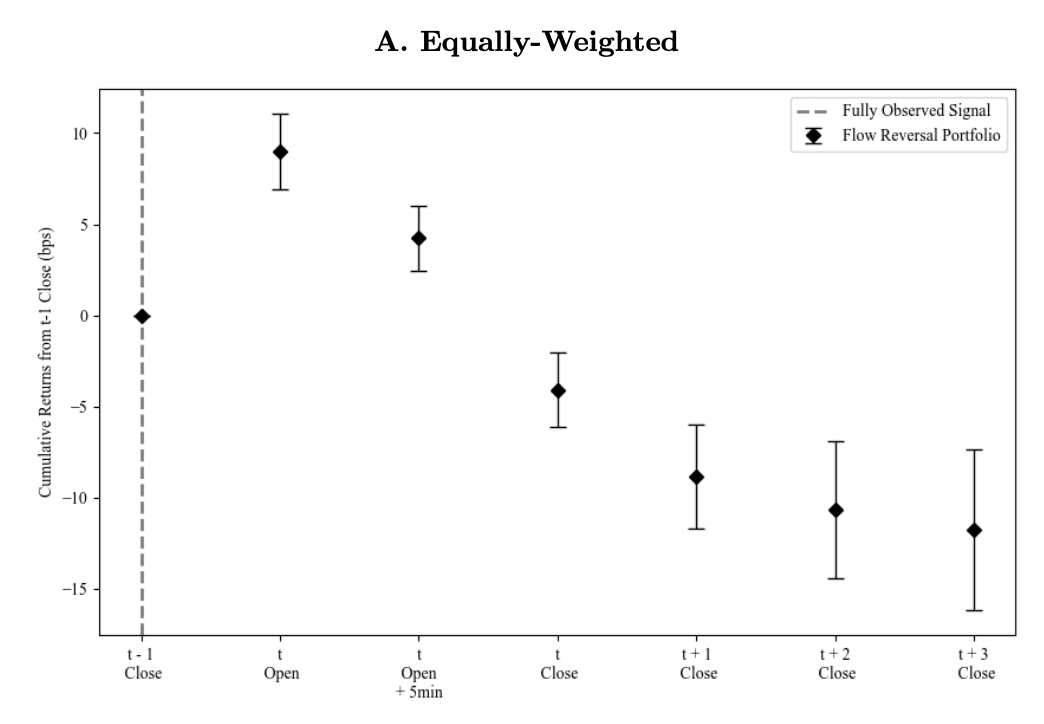

Furthermore, the 9:30 AM open is statistically the most adverse execution window. Mechanical buying from retail "Market On Open" (MOO) orders creates a buy-side imbalance that forces the Opening Auction to overshoot fundamental value. New research (Brown, 2025) confirms this auction is toxic. Prices consistently peak at the open and reverse immediately, with nearly 50% of the daily negative return occurring within the first 5 minutes.

Source: The Auction Trap (Brown, 2025). The chart tracks the price of retail-favored stocks. They drift higher overnight, peak exactly at the 9:30 AM Auction, and crash immediately after. Retail traders executing at the Open are structurally forced to buy at the exact top of the daily range.

This renders 0DTE options structurally ill-suited for news-based trading. It forces users to execute at the 9:30 AM bell, buying the top of the reversal while missing the overnight appreciation. Perps solve this via continuous exposure, allowing traders to capture the news event in real-time.

With crypto exchanges having built the underlying perpetual infrastructure, and with perps already the dominant form of trading, this offers a natural expansion opportunity to capture equity-leverage demand and materially expand their addressable market, applying their exchange technology to assets beyond crypto.

Regulatory Framework: The Binding Constraint

US regulation has effectively blocked retail perpetual futures by subjecting them to Dodd-Frank's futures framework, requiring DCM/SEF execution and CCP clearing — constraints fundamentally incompatible with crypto's integrated stack.

While the CFTC’s withdrawal of its March 2025 advisory opened a narrow lane for commodity perpetuals via Coinbase Derivatives and Nodal Clear, equity perpetuals remain stifled by the Shad-Johnson Accord, a relic of the early 1980s. With no viable clearing infrastructure on the horizon, incumbents like Robinhood and Coinbase are structurally sidelined from the single-stock perpetual market. Consequently, the most probable path forward lies with decentralized exchanges. These platforms are positioned to capture liquidity in a regulatory gray zone by leveraging Regulation S (Rules 903 and 904), offering equities strictly through 'offshore transactions' while avoiding 'directed selling efforts' in the United States.

Source: NASDAQ looking at 24 Hour Trading

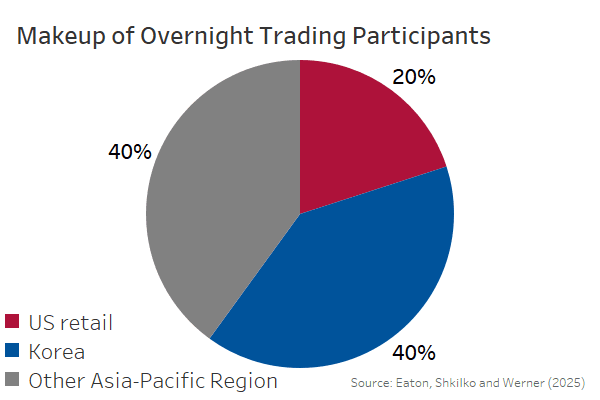

Data suggests that excluding US persons leaves the majority of the addressable market intact, particularly for 24/7 products. Microstructure data indicates that 80% of overnight volume originates from the Asia-Pacific (APAC) region, with Korean and other APAC participants vastly outsizing US retail flow during these hours.

Perpetual Futures Classification

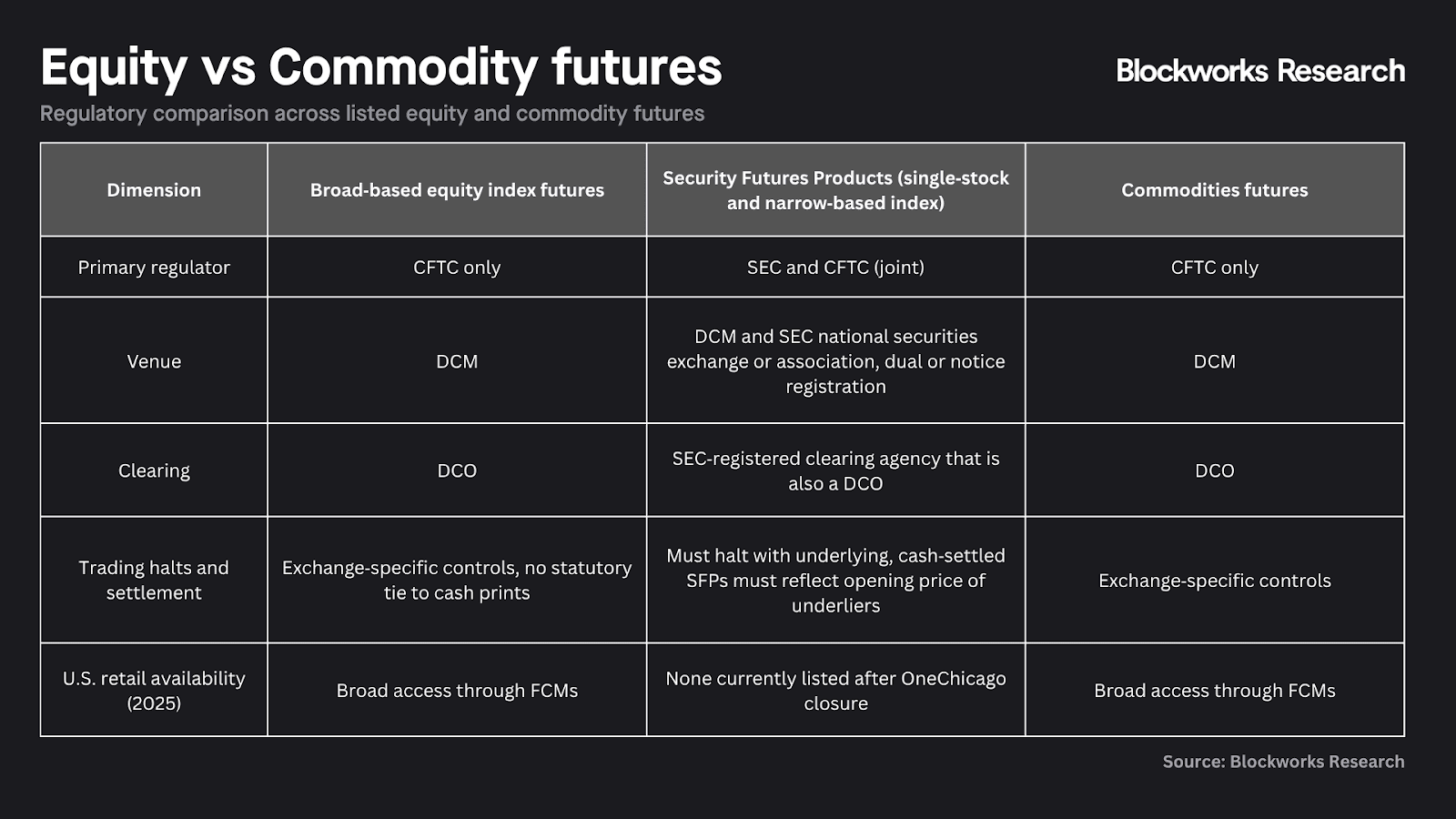

Perpetual futures offer clear advantages, but access for US retail remains limited because perpetual swaps are treated as futures‑like contracts subject to strict domestic rules. Under the Dodd‑Frank Act, CEA applies futures‑equivalent on‑exchange and registration requirements to leveraged or margin commodity transactions offered to retail unless physical delivery occurs within 28 days. Because perpetuals never deliver, they are captured by this provision. This classification imposes two core requirements:

Execution on regulated venues. Under CFTC jurisdiction, perpetuals must trade on Swap Execution Facilities or Designated Contract Markets. Security‑based swaps under SEC oversight must trade on Security‑Based SEFs or national securities exchanges.

Clearing through regulated central counterparties. CFTC products must be cleared at Derivatives Clearing Organizations and SEC products at SEC‑registered clearing agencies, typically accessed through FCMs or broker‑dealers with full KYC and AML.

These constraints effectively kept perpetual futures off US exchanges until recently, pushing activity offshore while domestic platforms focused on spot trading.

The Architecture of Futures Exchanges and Settlement

To understand the implications of this rule, we need to differentiate between the structure of crypto and traditional finance.

Crypto venues operate integrated stacks that onboard users, custody collateral, define products and margin rules, run matching engines, set marks and funding, and clear trades as the effective counterparty. Risk is centralized through venue‑set initial and maintenance margin, real‑time marking, automated liquidations, and backstops such as insurance funds and auto deleveraging. The system runs continuously, so trading, collateral checks, and settlement occur 24/7 without external brokers or independent clearinghouses.

Traditional futures markets separate these layers across three entities:

- The FCM (Futures Commission Merchant) serves as client intermediary, performing KYC/AML, holding segregated funds, collecting initial and variation margin, running daily segregation calculations, issuing margin calls, and reporting to the CFTC and NFA.

- The DCM (Designated Contract Market) lists contracts, certifies them, operates the order book and matching engine, conducts surveillance, enforces position limits, and manages halts.

- The DCO (Derivatives Clearing Organization) accepts matched trades, novates them to the CCP, sets initial and maintenance margin, calls daily and intraday variation margin, nets settlements, runs default waterfalls, and protects customer assets through segregation.

In practice, a client opens an account at an FCM such as Charles Schwab, posts margin, and routes orders to a DCM such as the CME Group. The DCM matches trades and submits them to the DCO for novation and margining. The DCO may call variation margin intraday; if the client fails to meet the call, the FCM can flatten the position.

Therefore, for crypto exchanges currently handling all layers in‑house, listing futures on DCM and DCO rails requires fundamental architectural redesign and conflicts with the integrated model.

Regulatory Implications and Commodity Futures

To comply in the United States, crypto exchanges (functioning as FCMs) must work through intermediaries; they cannot list futures directly. A US perpetual must therefore be redesigned to fit DCM and DCO standards: defined expiry, benchmarked settlement, cash‑adjustment funding synchronized with CCP margin cycles, conservative collateral, and critically, 24/7 trading support.

From May 2023 to March 2025, a CFTC staff advisory imposed heightened scrutiny on digital asset clearing, signaling extra review for any DCO attempting to clear crypto products. In March 2025, the CFTC withdrew the advisory, stated that crypto derivatives should receive standard treatment, and requested comment on 24/7 perpetual trading.

Nodal Clear (DCO) responded by adding weekend trading support and creating a cash‑adjustment flow for funding payments, synchronized with midday and end‑of‑day margin cycles. Coinbase Derivatives, a CFTC‑regulated DCM, then self‑certified nano BTC and ETH perp‑style futures cleared at Nodal Clear, the first US retail‑targeted perpetual product, featuring hourly funding that settles twice daily with a five‑year contract expiry, to remain compliant with futures guidelines.

This structure enables DCMs to list new futures by self‑certifying compliance rather than seeking prior approval. Crypto exchanges that have acquired CFTC exchanges and DCO connections include Coinbase (FairX to Nodal Clear), Cboe (ErisX to Cboe Clear US), Crypto.com (Nadex to CDNA as its own DCO), and Kraken (Small Exchange, historically OCC). While these moves support crypto perpetual growth, scale will ultimately depend on clearing capacity, collateral policies, and continuous operations.

Regulatory Implications For Equity Perpetuals

While a path now exists for commodity perpetuals, equity perpetuals remain difficult. Single‑stock futures were banned under the 1982 Shad‑Johnson Accord and later permitted by the 2000 Commodity Futures Modernization Act through Security Futures Products on single stocks or narrow‑based indexes under joint CFTC‑SEC oversight.

To reach retail, execution must occur on a national securities exchange listing security‑based swaps, requiring a clearing agency for equity SBS. Currently, US clearing is concentrated in CDS at ICE Clear Credit, with no widely available equity SBS clearing comparable to options and equity markets. Unlike commodities, no off‑the‑shelf exchange and clearing combination exists for equity SBS, making retail equity perpetuals a long‑lead project requiring both listing and clearing partnerships.

Additionally, the FIA stated it does not support extending trading and clearing to 24/7 until key issues are resolved. The primary concern is that current banking rails do not move margin 24/7, creating under‑margined exposures on weekends and holidays and credit risk for FCMs and DCOs. We view these operational dependencies as binding constraints even as product design advances. Even with commodity perpetuals progressing, a compliant single‑stock perpetual is likely a long way off.

Onchain Solutions for Equity Perpetuals

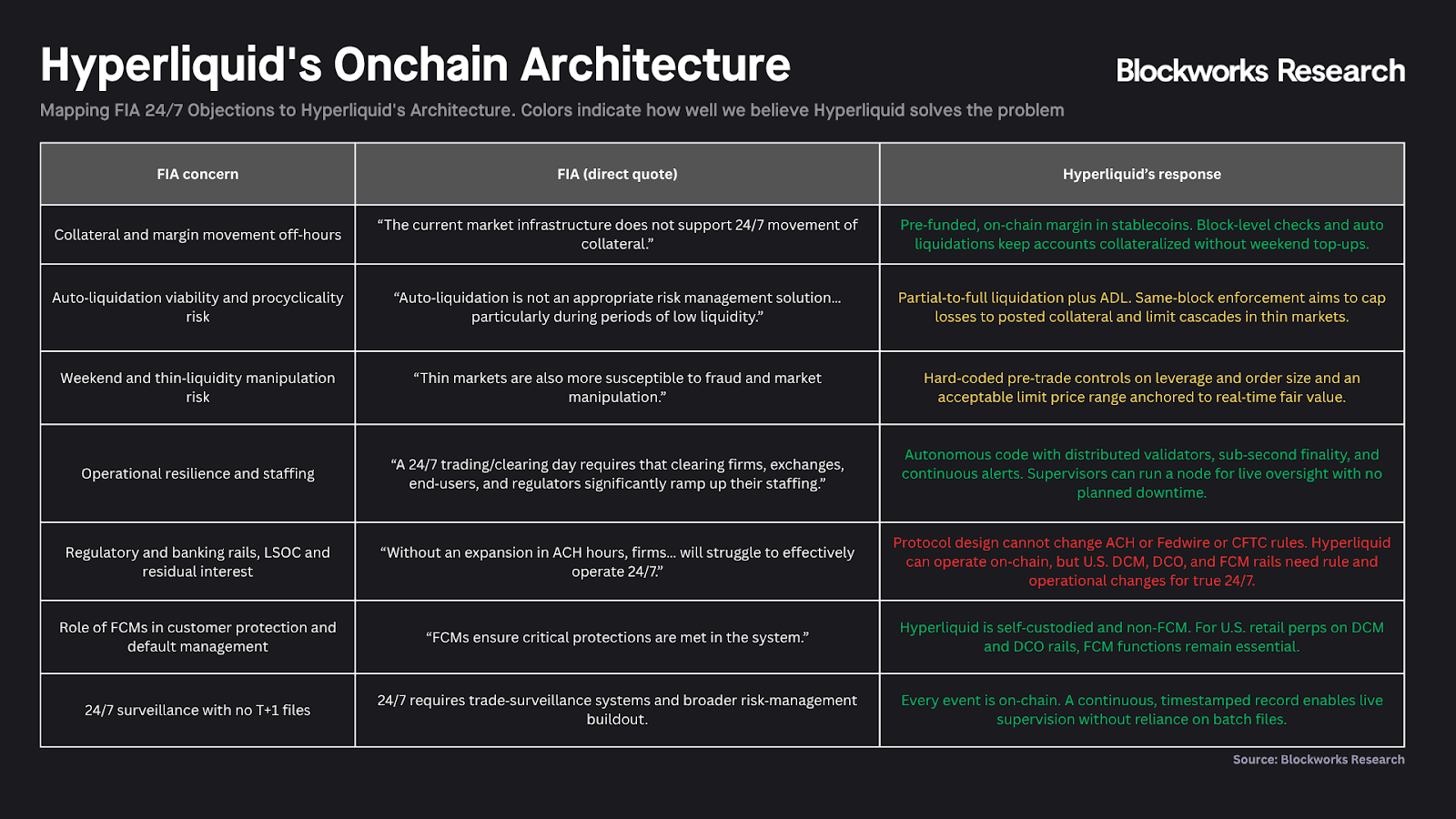

While the FIA argued that 24/7 trading is infeasible under current US clearing infrastructure, Hyperliquid's fully on‑chain orderbook demonstrates a functional alternative by translating operationally intensive clearing functions to autonomous, permissionless logic. Though this model does not comply with DCM/DCO rails, it directly addresses each FIA concern by reimagining the architecture rather than retrofitting legacy systems.

Hyperliquid’s response to the CFTC RFC for 24/7 trading has been mapped below against the FIA's specific objections.

We believe Hyperliquid's track record validates this approach. $300B October volume and $3.13T cumulative notional demonstrate that 24/7 perpetual trading via on‑chain architecture is operationally viable at institutional scale. However, this success is bound to crypto assets.

Expanding to real‑world assets such as equities introduces distinct constraints: banking rails remain closed on weekends, and external hedging venues operate on limited hours that cannot be solved by on‑chain logic alone.

The following sections assess whether existing orderbook DEX designs can support equity perpetuals, what design considerations become critical, and which platforms are positioned to capture this emerging opportunity.

Designing an Effective Equity Perpetual

To succeed onchain, equity perpetuals must satisfy three design requirements: a reliable continuous oracle, adequate exchange liquidity, and tight spot‑market integration.

Requirement One: Robust, Continuous Oracles

If US equities traded continuously like crypto, perpetual design would be straightforward. Oracle prices would track the stock's expected future value, adjusted for dividends, financing, and borrow costs, with funding rates driving perpetual prices toward this forward‑fair level.

Current solutions already achieve 24/5 coverage. During active market hours, Chainlink and Pyth deliver robust, licensed equity prices with built-in freshness checks.

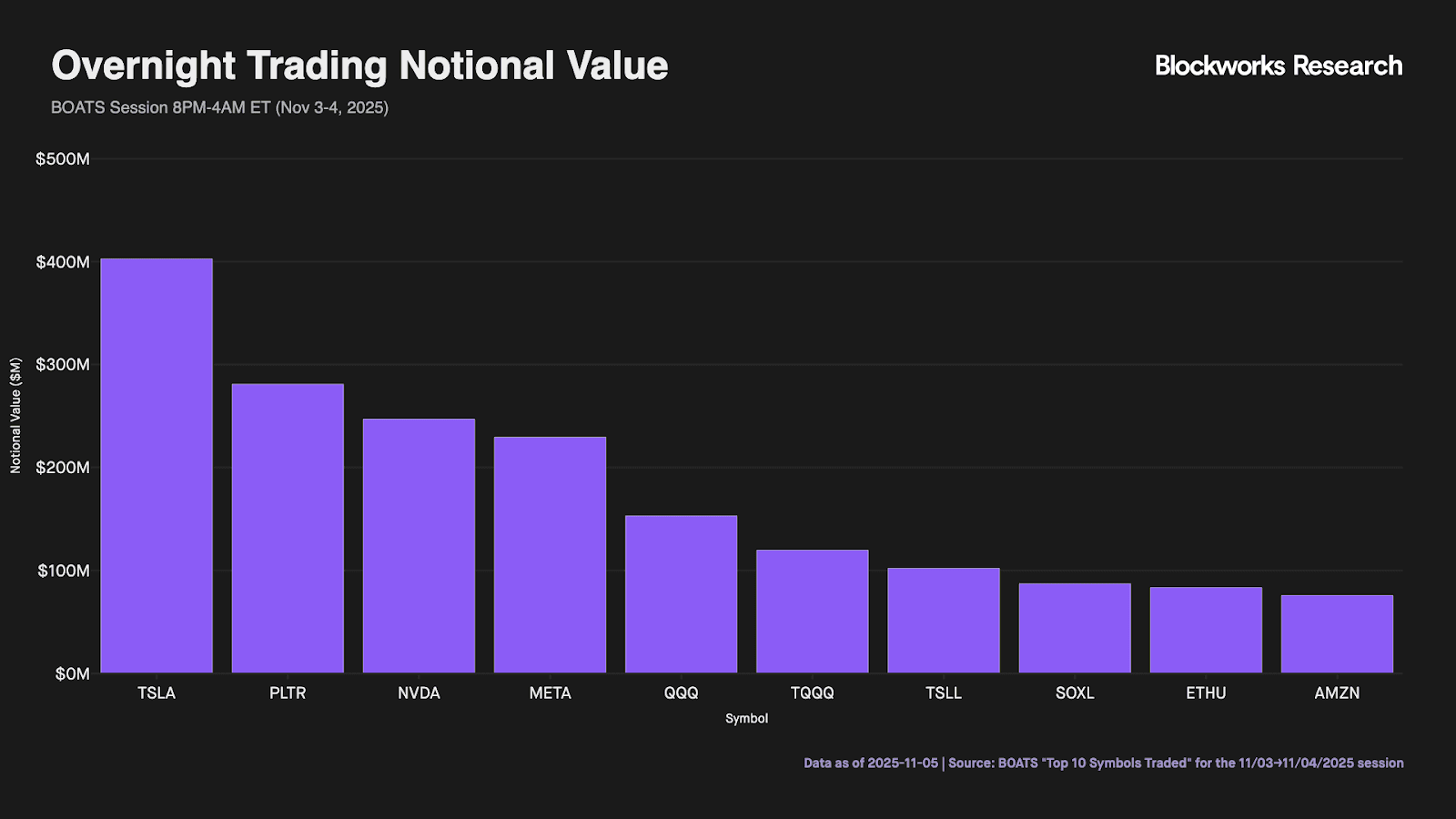

For overnight trading, Blue Ocean ATS (BOATS) provides the primary source of price discovery. While often dismissed as insignificant retail flow, recent market microstructure analysis reveals that the 8:00PM to 4:00AM window carries disproportionate information content relative to its volume. Although this window represents only ~0.38% of consolidated share volume, it accounts for approximately 9% of daily price discovery (Weighted Price Contribution), with that figure rising to 17.4% for ETFs.

Approximately two-thirds of these nocturnal price changes do not revert by the next market close, indicating that this flow drives permanent price formation. For equity perpetuals, this validates the use of overnight feeds as oracle inputs — particularly for index and ETF products where overnight price discovery is strongest, and indicates the importance of overnight trading.

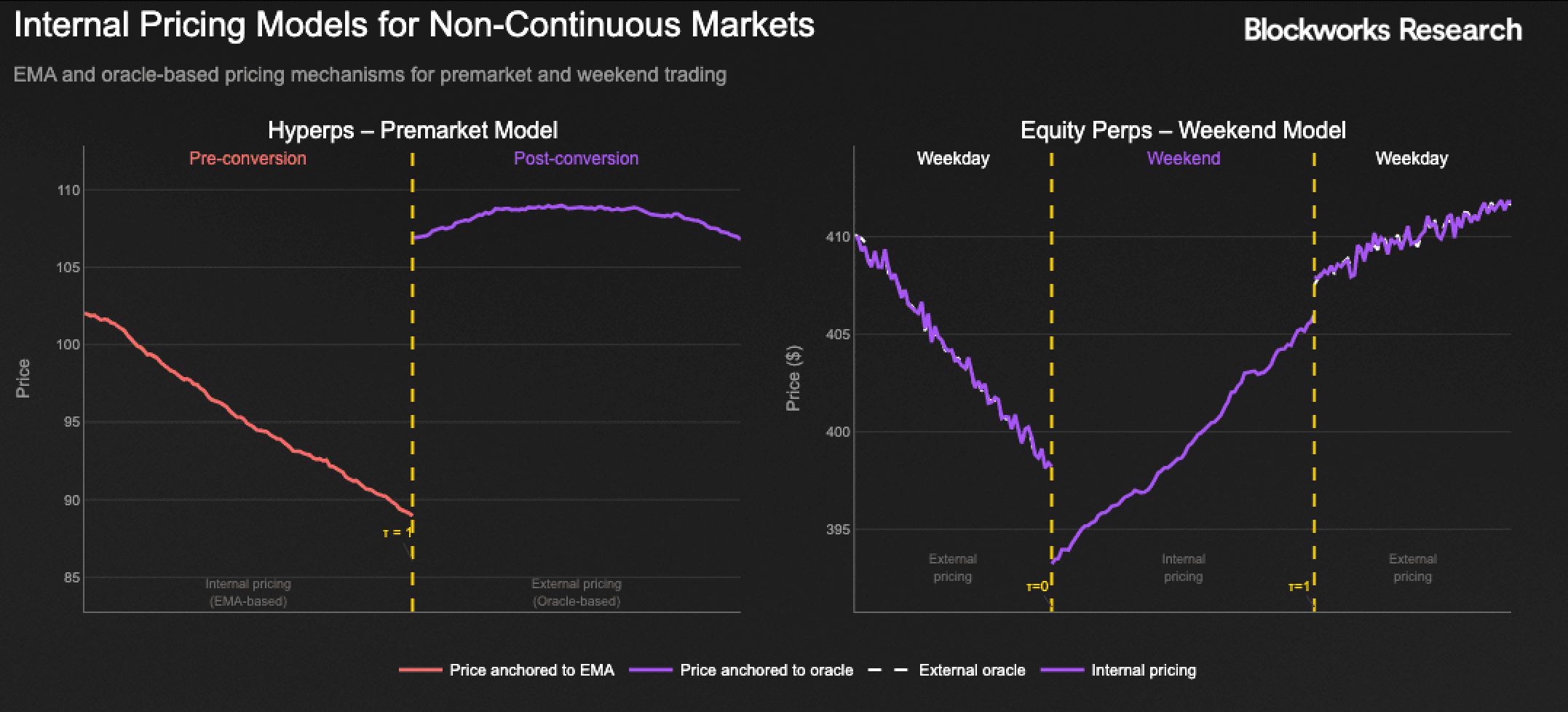

The remaining design question is how to handle weekends when all external price sources are dark. Some crypto protocols, such as Ostium, disable weekend trading entirely. The alternative is to run internal pricing that does not rely on a live spot oracle, instead using an exponential moving average or fixed anchor price of the internal futures contract price with predefined risk parameters to guide the mark until external prices resume.

Operating without a live reference may seem counterintuitive for a delta‑one instrument designed to replicate an underlying. Hyperliquid's Hyperp premarket provides a helpful analog that has already attempted the model at scale. Since hyperps trade pre‑launch assets with no spot reference, they substitute an 8‑hour exponentially weighted average of the prior day's minute‑by‑minute mark prices as the oracle input. When the asset begins trading, the market converts the premarket Hyperp to a standard perp, referencing the actual spot price as the oracle price: this conversion mechanism allows traders to price the premarket fairly. The model has seen strong adoption, with Hyperliquid's PUMP premarket recording over $100M in daily volume.

Equity perps can apply the same concept. When traders know the contract will revert to Monday's opening price, internal pricing keeps the mark near fair value during weekend sessions. The figure below illustrates this alongside Hyperliquid's premarket model.

We believe this model for weekend price discovery is a viable solution that requires circuit breakers, open interest caps, and project‑specific risk parameters to function properly — topics we address in later sections.

Requirement Two: Adequate Exchange Liquidity

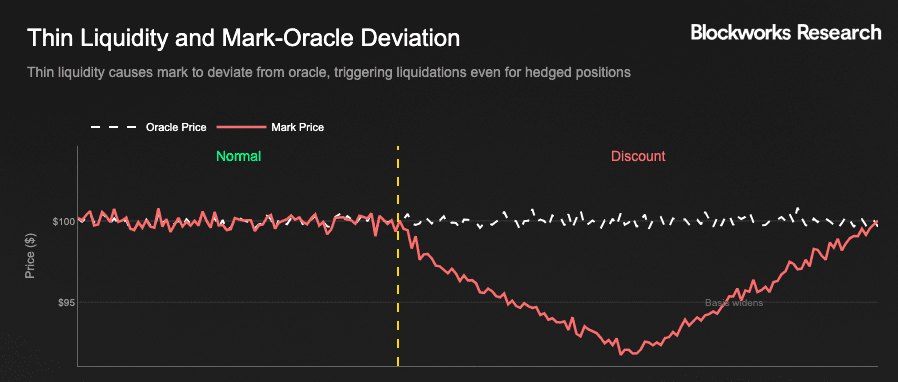

The second requirement for performant equity perpetuals is robust liquidity. While anchoring to an accurate oracle is necessary, a deep internal order book is equally critical. Liquidity depth matters not just for execution quality but for several structural reasons:

- Funding Rate Stability: Funding is set by the mark's premium or discount to the oracle. In a thin book, the mark fluctuates excessively, the basis widens, and funding can spike to levels that make it unprofitable to hold positions or maintain hedges. Depth keeps the mark anchored to the oracle, ensuring predictable carry costs.

- Mark Price Integrity: The system uses mark price for P&L, margin, and liquidations because liquidations must reference tradable prices. A trader who is delta-neutral away from the venue can still be liquidated if the on‑venue mark deviates while the oracle remains stable.

- Liquidation Contagion: When maintenance margin is breached, the risk engine reduces exposure by selling contracts into the order book. With depth, liquidation clips fill near the mark and the process remains controlled. With shallow liquidity, forced selling pushes price, widens the basis, and can trigger cascading liquidations.

The following figure illustrates this risk: aggressive selling into the order book for short contracts can cause dislocations between the perp contract and its oracle, since liquidations trigger based on the mark price.

This creates problems even for market makers who may be hedged and delta-neutral but get liquidated due to mark price deviation that doesn't reflect the underlying at the point of liquidation. Hyperliquid's Hyperp premarket experienced similar issues with XPL and MON, where a trader hunted liquidations of users who had hedged locked tokens via premarket shorts but could not supply collateral in time.

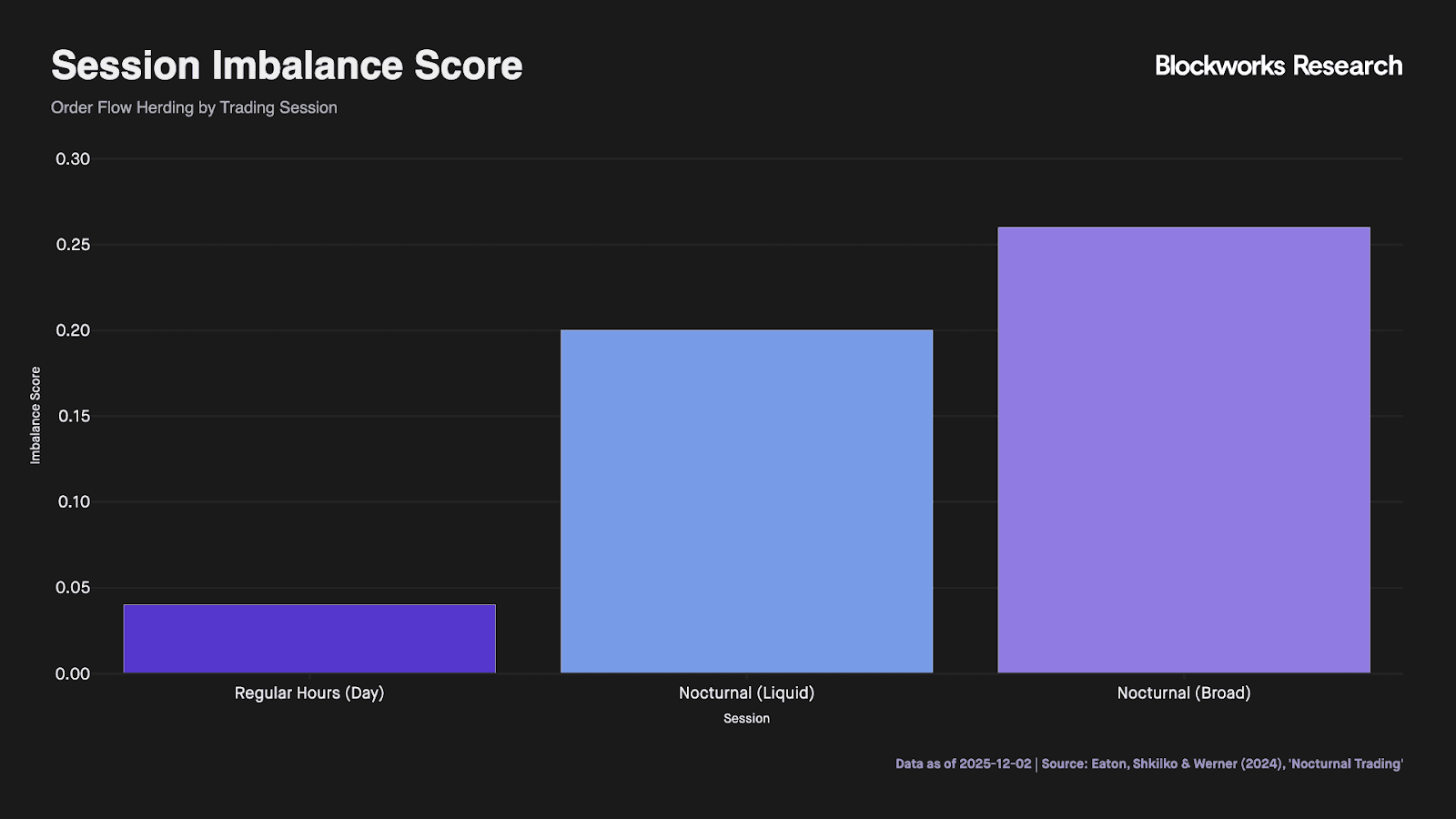

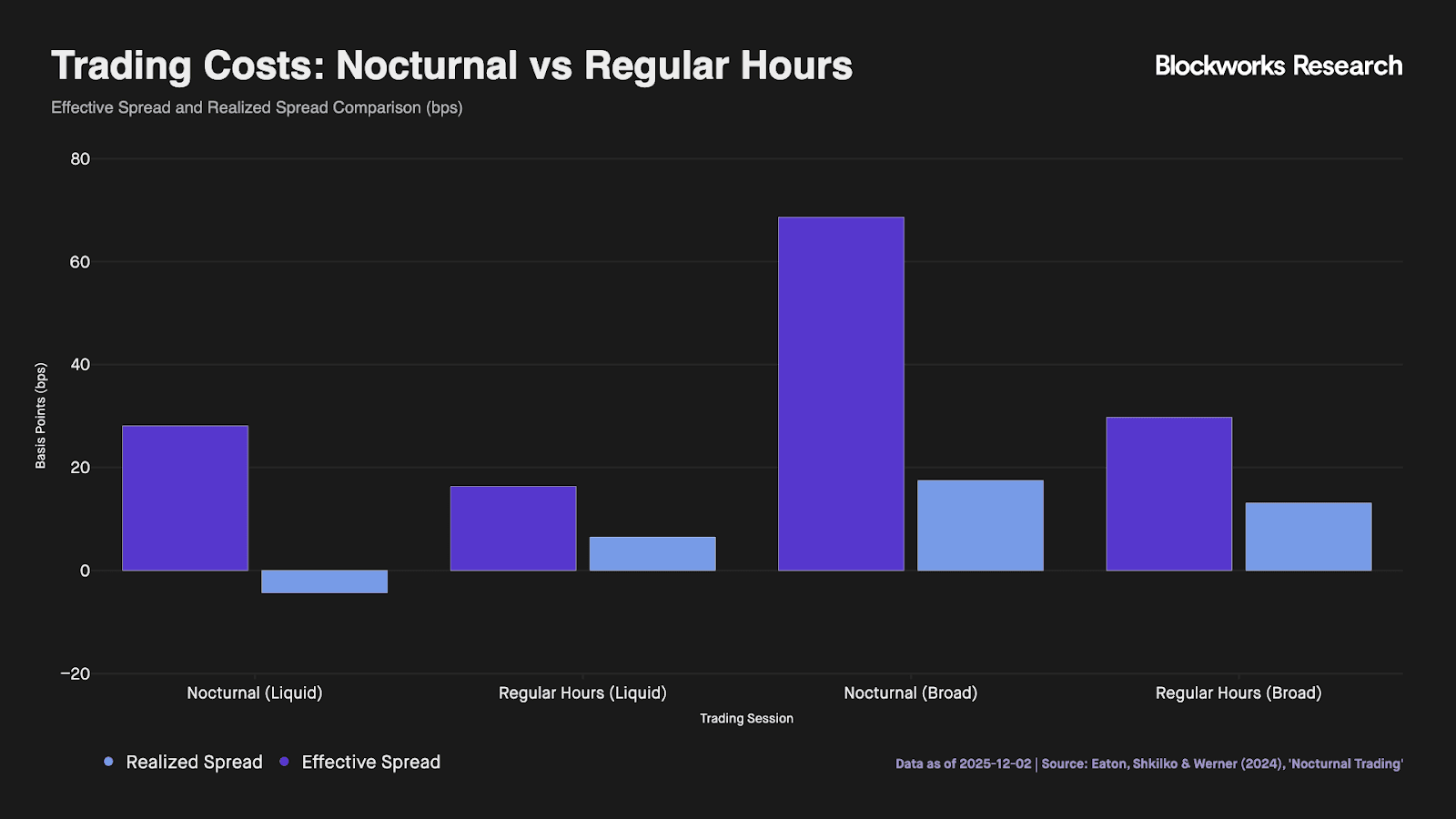

Importantly, providing liquidity is difficult even for established market makers. Microstructure analysis of the 8:00 pm to 4:00 am session shows a structural order imbalance of 0.20–0.26, indicating highly one-sided, herding flow.

Consequently, overnight liquidity provision suffers from acute adverse selection. Despite quoting defensive spreads (~27 bps), Market Makers incur negative realized spreads (-4.3 to -6.8 bps) due to the highly directional nature of order flow during these illiquid windows. This structural unprofitability is exacerbated on permissionless venues, where non-KYC access encourages toxic flow to aggregate.

Thus, adequate exchange liquidity for equity instruments is critical.

Requirement Three: Enabled Reliable Hedging Mechanisms

Equity perpetuals must enable reliable hedging for market makers — a significantly greater challenge than in crypto‑to‑crypto flows. In crypto, makers can offset exposure using on‑venue spot or another perp with near‑instant stablecoin transfers and cross‑margin, allowing rapid price correction and arbitrage. Protocols like Liminal already automate this by shorting the perpetual while buying the underlying spot.

Equity perps face structural friction because the hedge must sit on traditional platforms with limited hours and end‑of‑day clearing. Market makers must transfer collateral between traditional venues and crypto platforms to rebalance positions — for example, hedging a UNIT long with an E‑mini Nasdaq‑100 short. They cannot hedge on weekends, and overnight trading incurs wider spreads. This creates three critical risks:

- Weekend delta gap: If the perp moves on Saturday, market makers cannot adjust stock or futures hedges and must carry the full delta until reopen.

- Basis widening: Funding accrues while the TradFi hedge is frozen, and a thin book can dramatically widen the basis.

- Collateral Duration Mismatch: A structural misalignment exists between the instantaneous settlement of crypto margin calls (T+0) and the delayed settlement of traditional banking rails (T+1/T+2). During weekend volatility, a Market Maker may remain solvent on a hedged basis yet become effectively illiquid, as they cannot mobilize fiat capital to meet onchain margin requirements.

To avoid these failures, equity perps require a second venue for the other leg, fast collateral mobility between both venues, and a mark‑and‑liquidity regime that does not surprise delta‑neutral traders.

Current Landscape

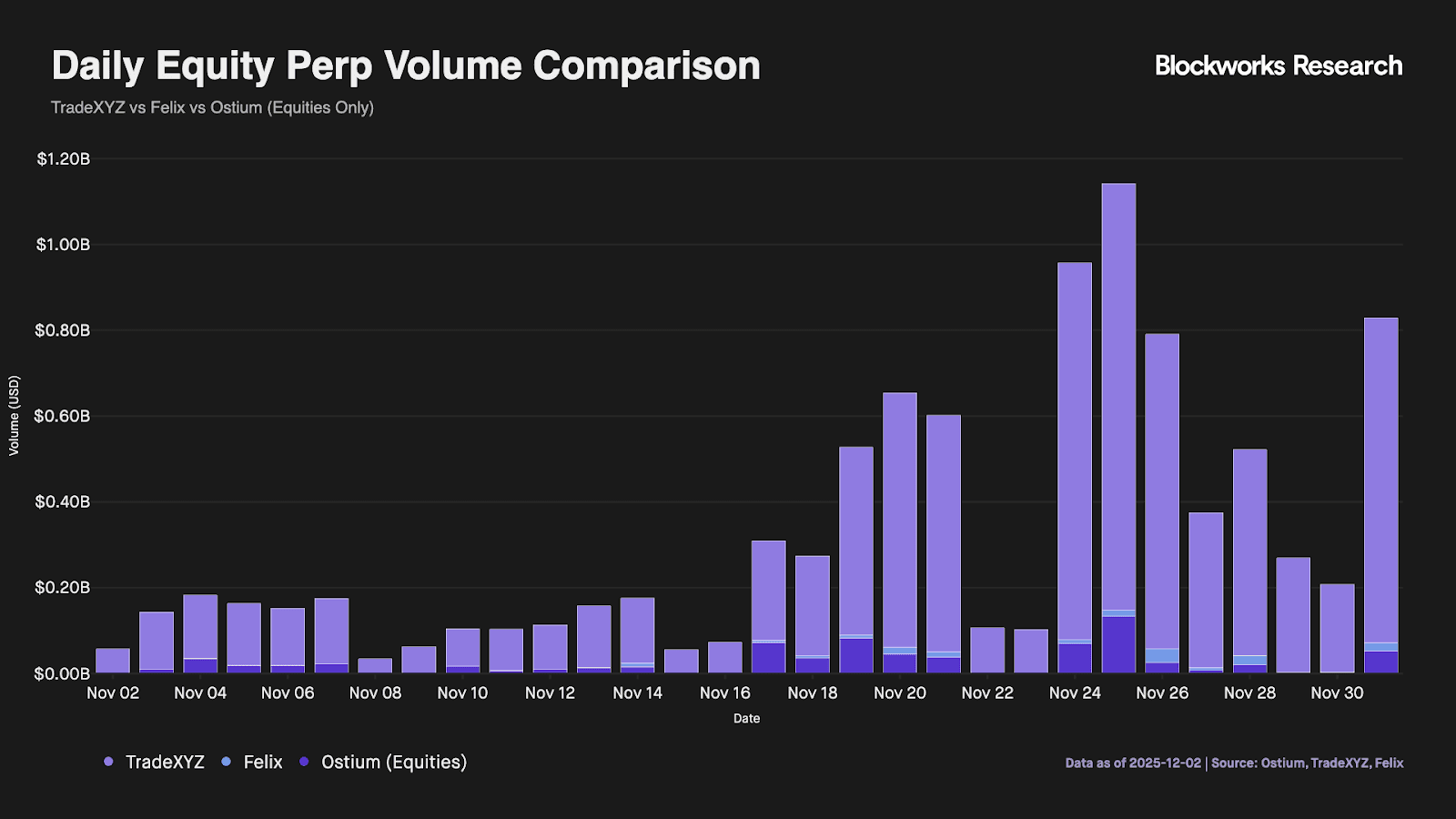

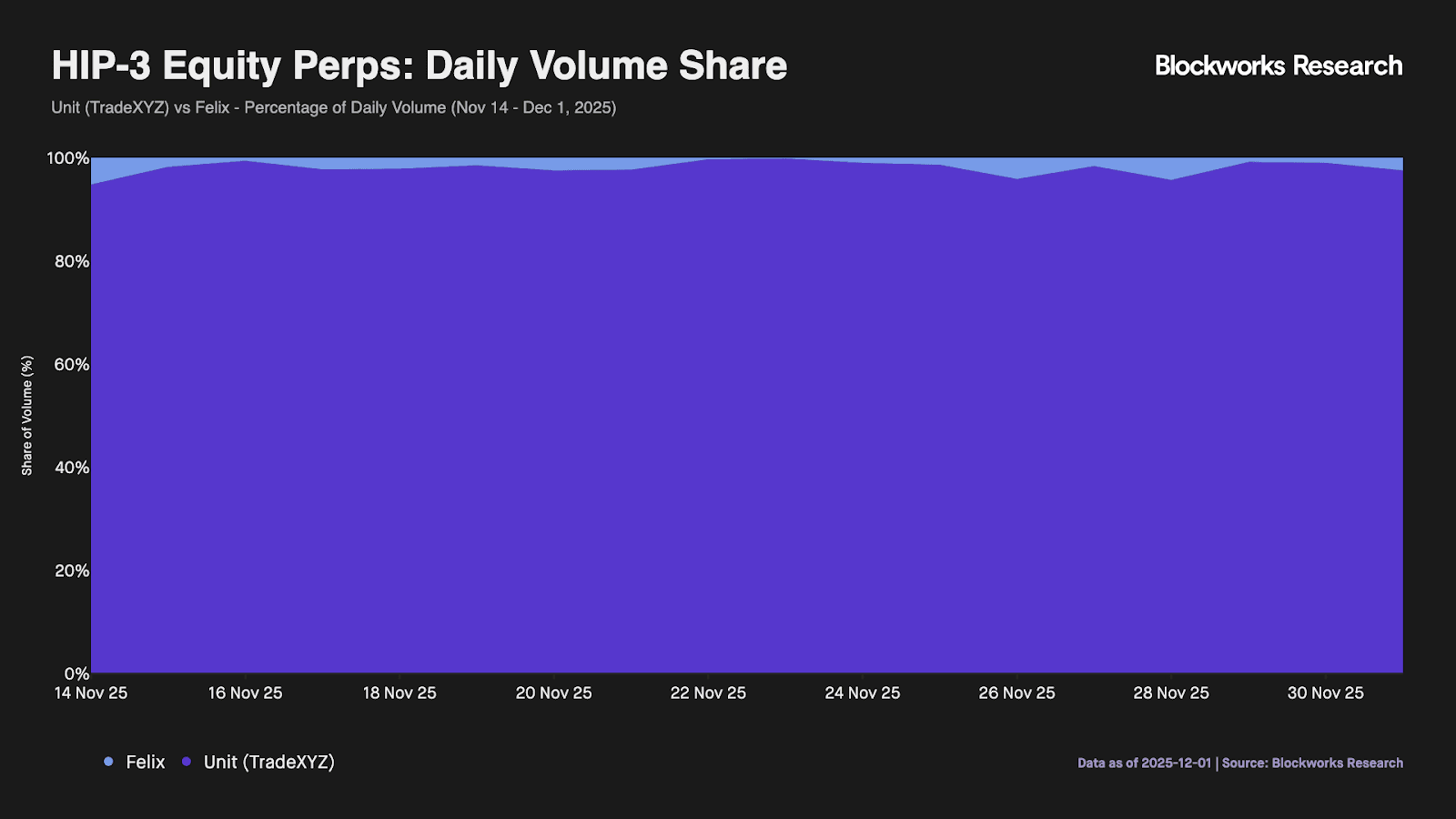

While equity perpetuals represent a significant addressable market, long-term viability is contingent upon resolving the structural constraints of oracle continuity, liquidity depth, and hedging efficiency. Initial volume data validates the thesis: combined turnover across Trade.XYZ, Felix, and Ostium exceeded $9.4B over a 30-day period, peaking at above $1B daily. However, the 70–90% contraction in weekend volume highlights a persistent dependency on traditional equity market hours for price discovery and liquidity provisioning.

The following section evaluates four distinct architectural frameworks to determine which design is best positioned to solve these liquidity constraints at scale: Ostium's synthetic peer-to-pool model, Hyperliquid's decentralized orderbook (HIP-3), Vest Exchange's risk-based margining system, and Solana's spot-integrated ecosystem.

Ostium

Overview

Ostium is an Arbitrum-based perpetual DEX purpose-built for synthetic exposure to real-world assets (FX, commodities, indices, and single-name equities). These assets are delivered via onchain perps rather than tokenized wrappers or bridges. Following its initial $3.5M seed round in October 2023, the protocol significantly capitalized its balance sheet in December 2025, announcing a $20M Series A and strategic raise co-led by General Catalyst and Jump Crypto, with participation from Coinbase Ventures, Wintermute, and GSR. This round valued the protocol at approximately $250M.

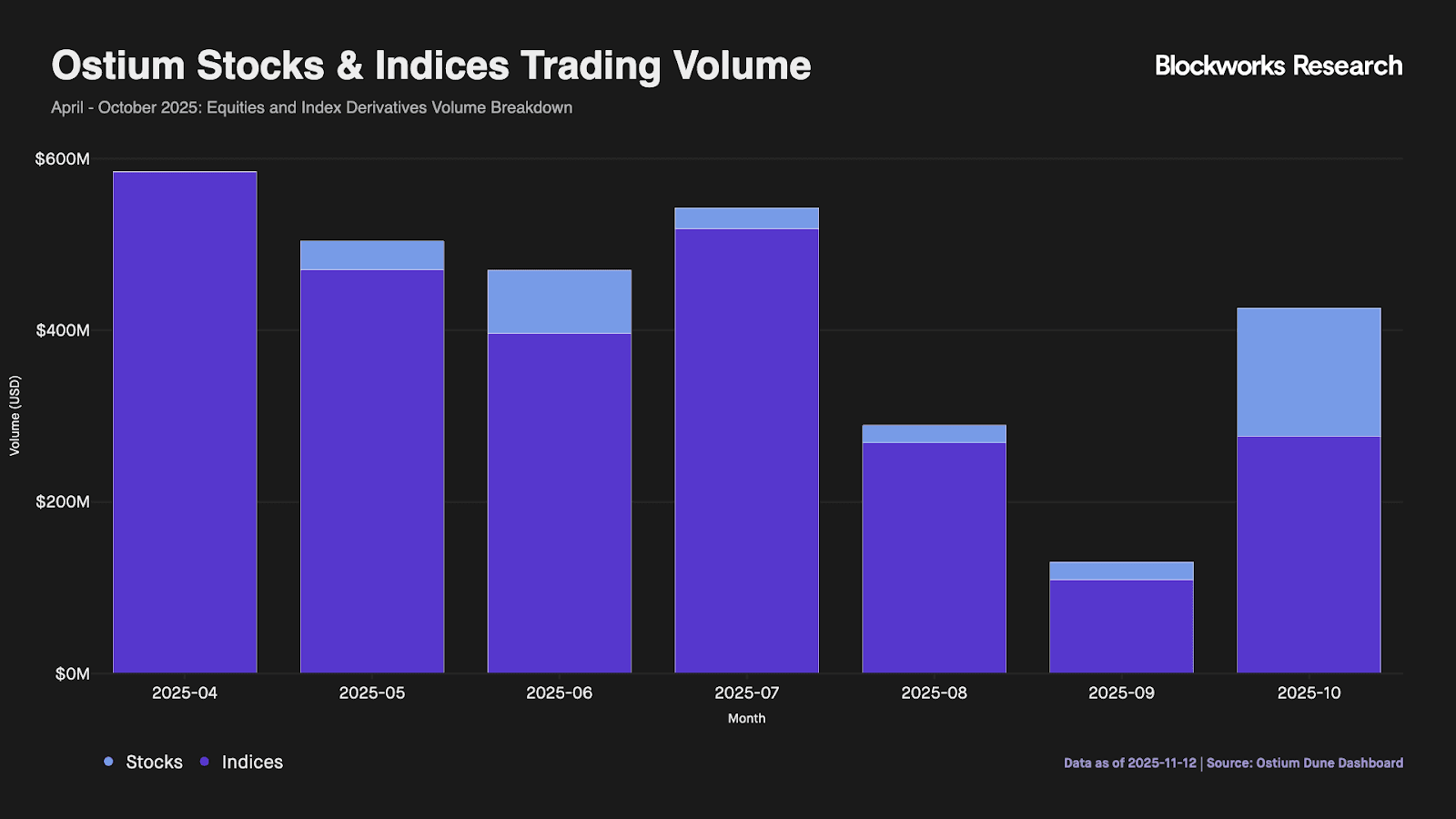

The platform utilizes a peer-to-pool architecture where traders open positions against a protocol-owned liquidity pool acting as the singular counterparty, rather than a central limit order book (CLOB). Ostium established itself as a leading RWA exchange, generating nearly $600M in weekly equity volume at its peak.

Oracle Design

Ostium sources prices from purpose-built RWA feeds operated with Stork for non-crypto markets. Execution uses the live bid/ask/mid from the oracle rather than a mark derived from internal orderbook liquidity. This differs materially from orderbook venues: traders can execute directly at TradFi-equivalent prices without waiting for a market maker to quote near the oracle. The pool absorbs the immediacy risk, and the venue charges a fixed opening fee (2–6 bps) plus a rollover fee that accrues per block.

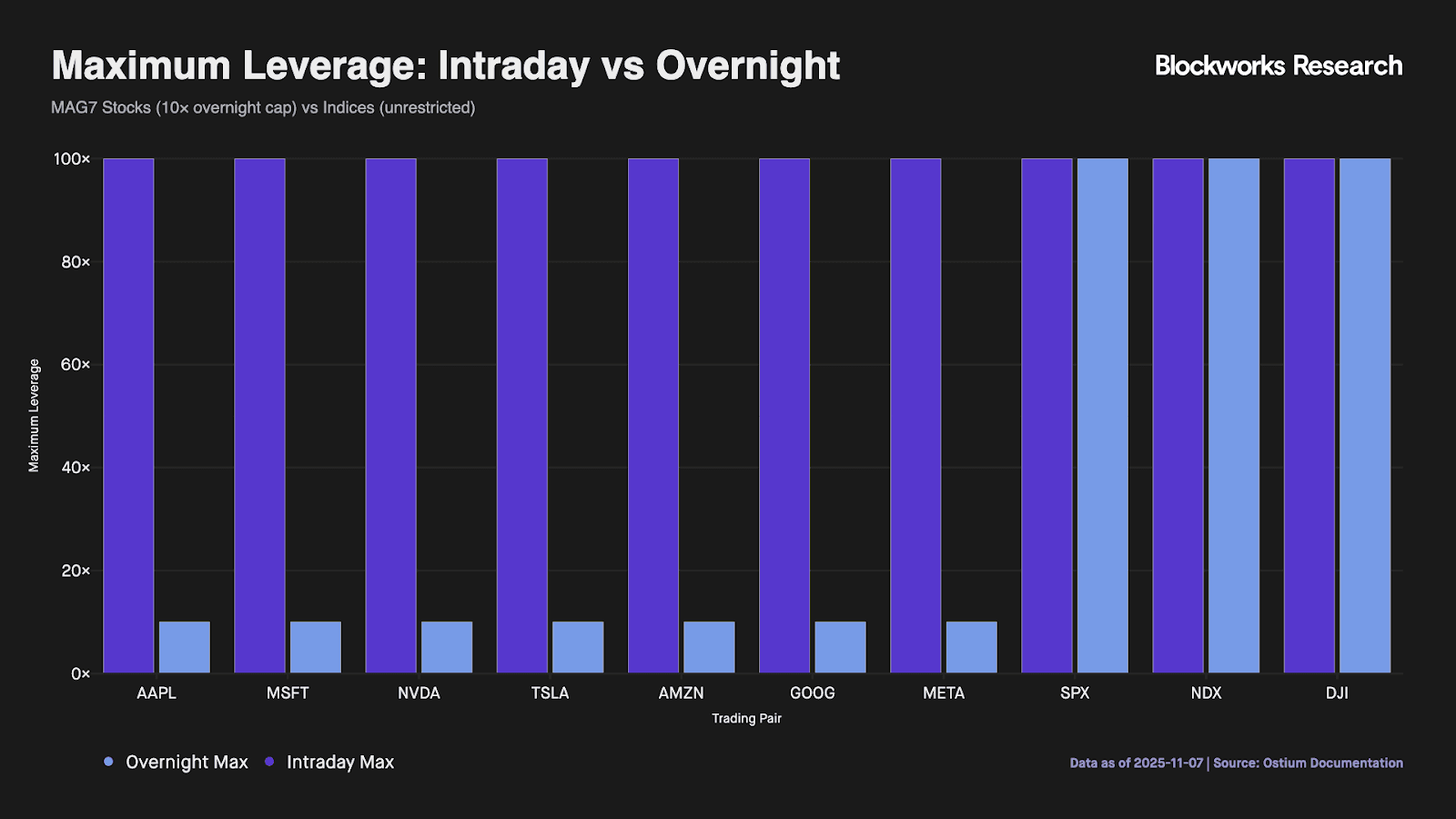

However, this direct-oracle dependency imposes a hard operational cap on trading hours. Since the venue lacks an internal price discovery mechanism, it cannot facilitate execution when the underlying TradFi oracle is offline. Ostium therefore implements limited-hour trading for equity pairs. Overnight positions are automatically capped at 10x leverage, and weekend trading is disabled entirely.

Absence of an internal mark price means the contract cannot reference an exponentially weighted average or synthetic anchor when the underlying cash market is closed and the contract halts. From a trader perspective, this creates clean execution during market hours but forfeits the 24/7 composability that defines crypto perps. For LPs, the pool’s exposure to net directional risk becomes the binding constraint.

Liquidity

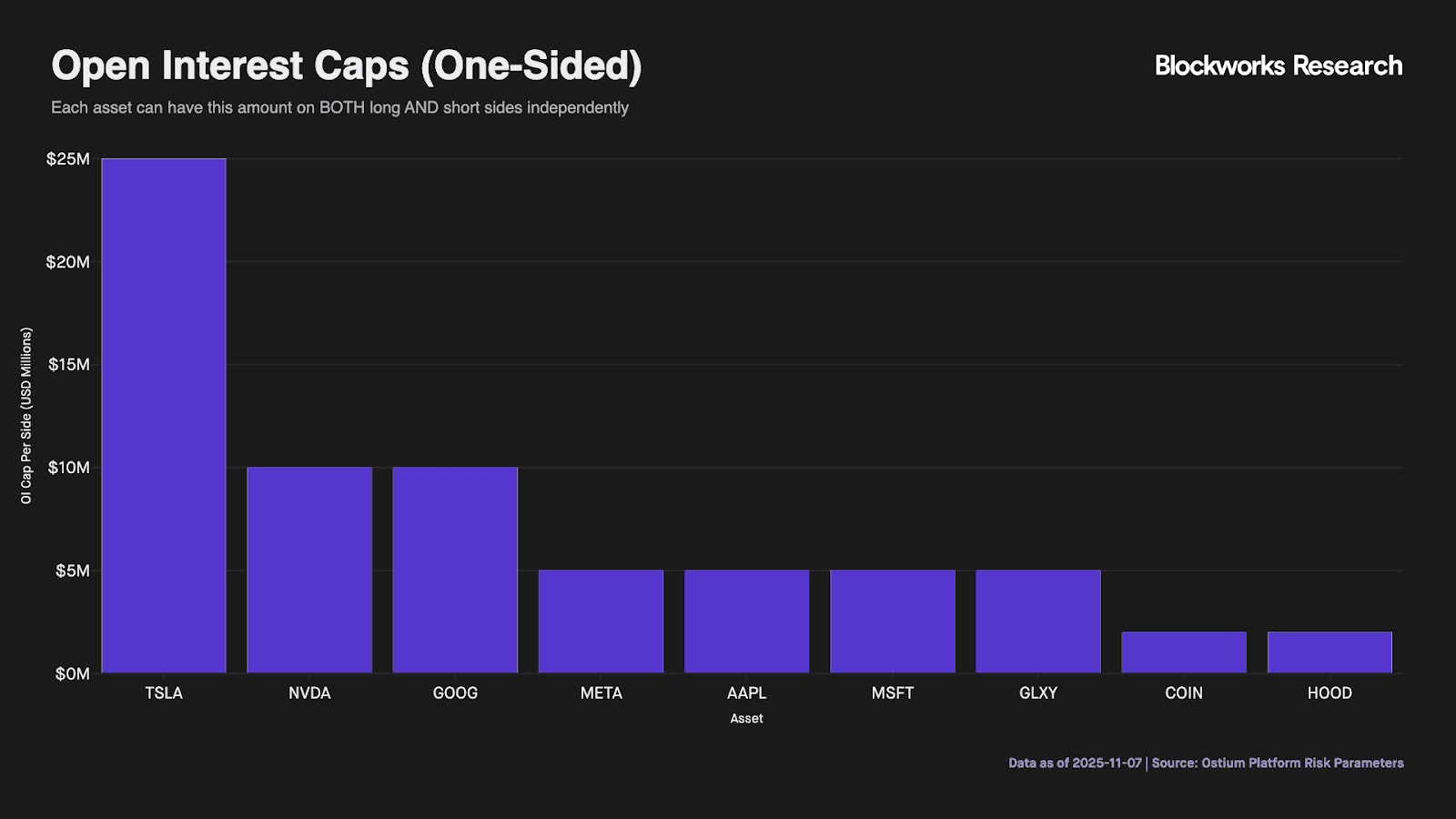

In a peer-to-pool model, "liquidity" is defined not by orderbook depth but by open-interest capacity and counterparty risk tolerance. This creates significant constraints on open interest (OI), since OI equals the directional risk the LP is willing to carry unhedged. Ostium manages this via a net volume threshold per pool, which represents the maximum net notional exposure the pool will carry before activating dynamic spread penalties. For example, the META/USDT pair has a "NetVolThreshold" of $1M. Once net open interest exceeds a $1M long or short imbalance, the venue widens spreads to disincentivize further imbalance.

This design allows for "infinite" liquidity up to the threshold but does not generate true two-way flow. To contain risk, OI caps are set conservatively: $25M for TSLA, $10M for NVDA and GOOGL, and roughly $5M for other single-name equities. Equity longs pay a rollover rate (live SOFR 5.3% + premium, compounded per block) that compensates the pool for directional risk, while shorts pay nothing.

This yields a substantial cost-of-carry advantage for traders. Ostium’s SOFR-anchored rates (~5.3%) are significantly cheaper than the volatile funding rates inherent to orderbook venues, a disparity highlighted by Kaledora’s co-founder, who observed that Unit’s XYZ-100 Nasdaq perp funding spiked to -600%. However, this pricing could be considered misaligned: LPs are at risk for a fixed-income return, effectively subsidizing trader leverage.

Hedging

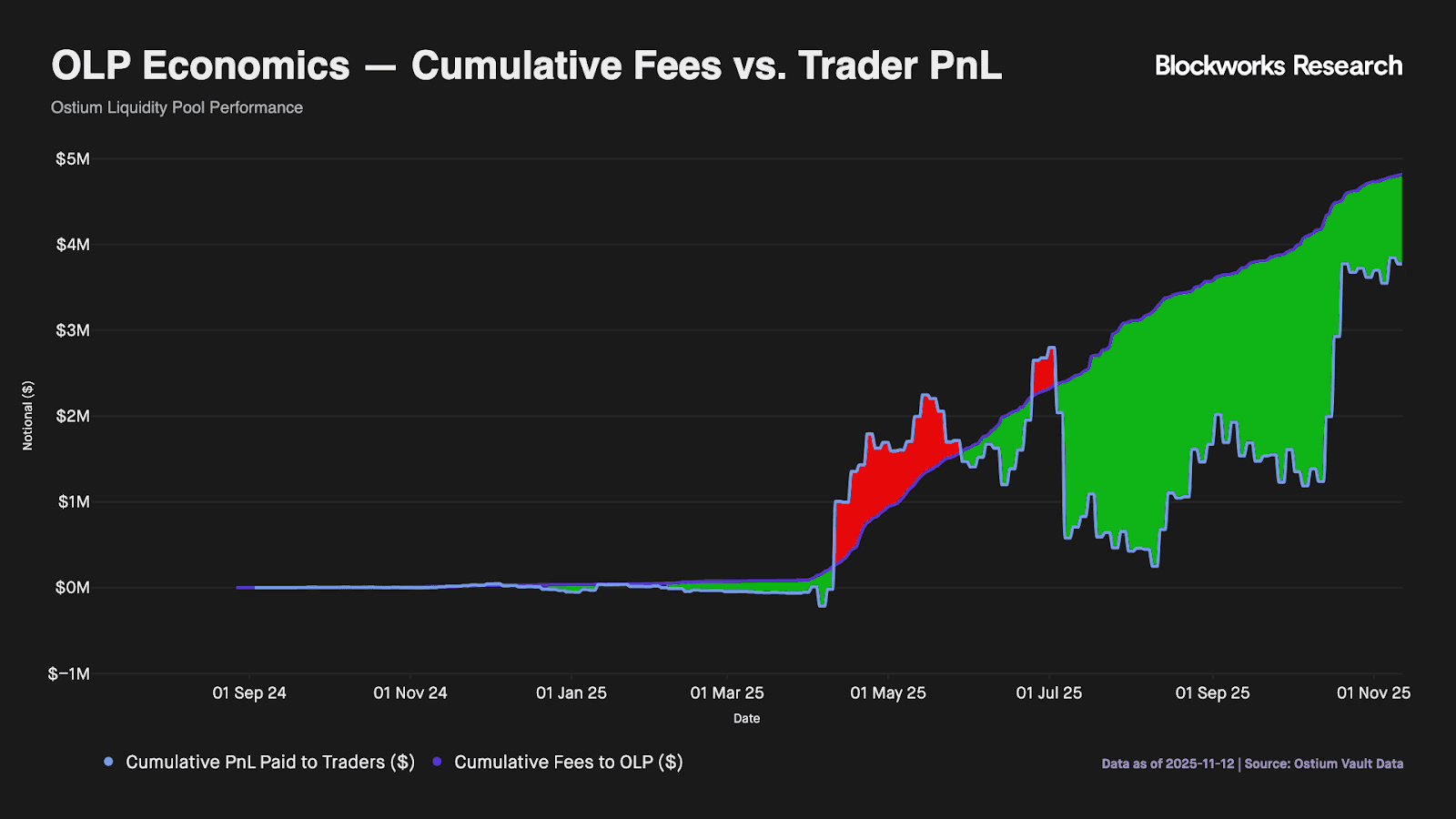

The primary challenge for peer-to-pool architectures is protecting Liquidity Providers (LPs) from informed flow. In a model where the pool acts as the counterparty, traders with an informational advantage—particularly in single-stock equities—can extract value directly from the system. To date, Ostium traders have realized $1.7M in net profit. In a pure peer-to-pool model, this would represent a direct dollar-for-dollar loss to LPs.

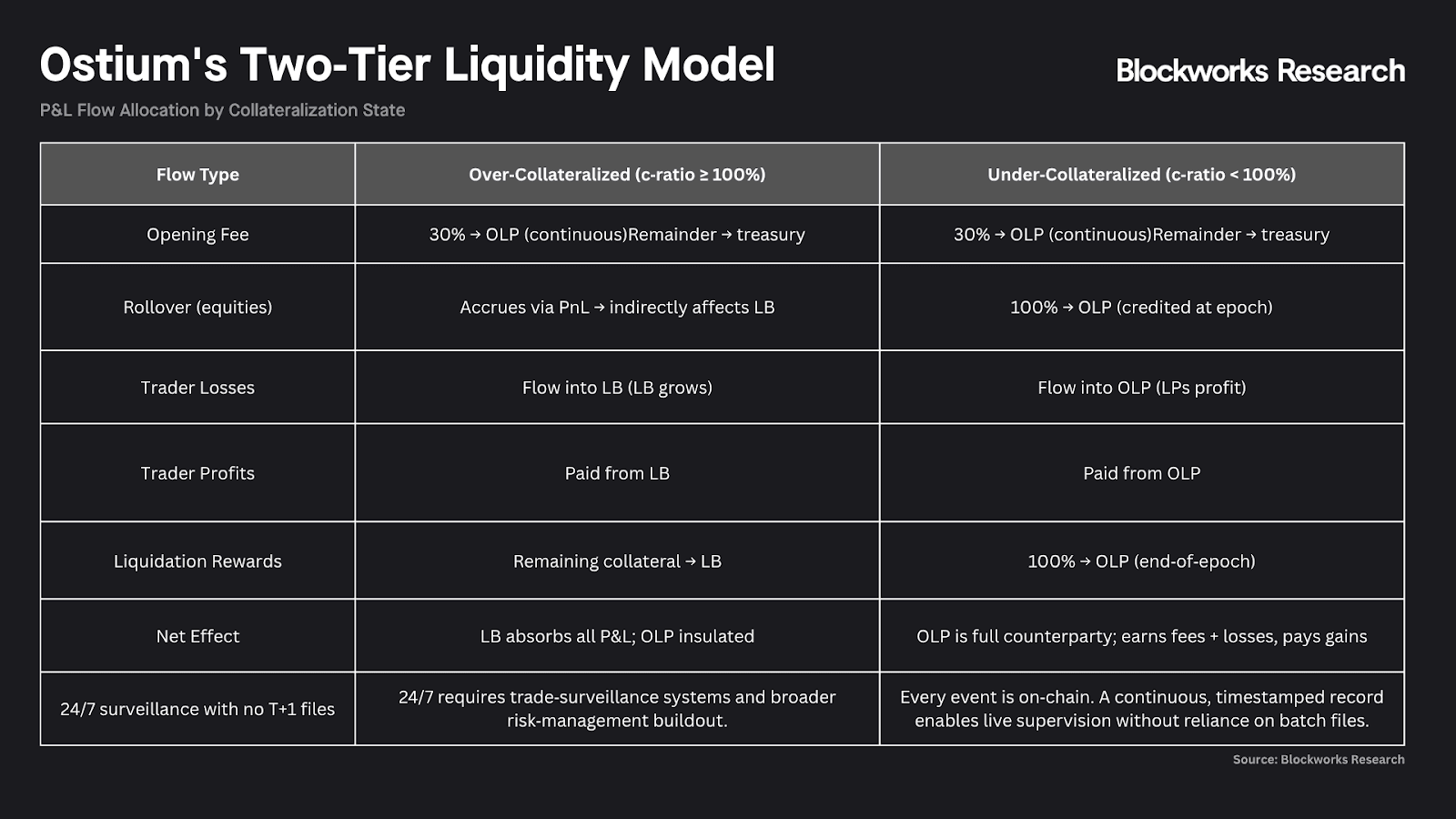

Ostium attempts to insulate LPs from this volatility via a two‑tier counterparty design:

- Liquidity Buffer (LB): Protocol‑owned; absorbs trader losses first and pays trader profits first.

- Market‑Making Vault (OLP): LP‑funded; backstops the buffer only when the LB cannot cover a payout.

The system uses a collateralization ratio (c‑ratio) to measure how much buffer remains before LPs take principal losses. It compares the vault's actual value to what it would be worth if only trading fees had accrued (no P&L impact). When c‑ratio is at or above 100%, the protocol‑owned Liquidity Buffer fully absorbs all trader P&L, and the LP‑funded vault (OLP) simply collects fees while remaining insulated from losses. When c‑ratio drops below 100%, it signals that trader profits have depleted the buffer; the OLP then becomes the direct counterparty, absorbing both trader gains and losses. In short, c‑ratio ≥ 100% means LPs earn fees safely; c‑ratio < 100% means they are actively taking directional risk.

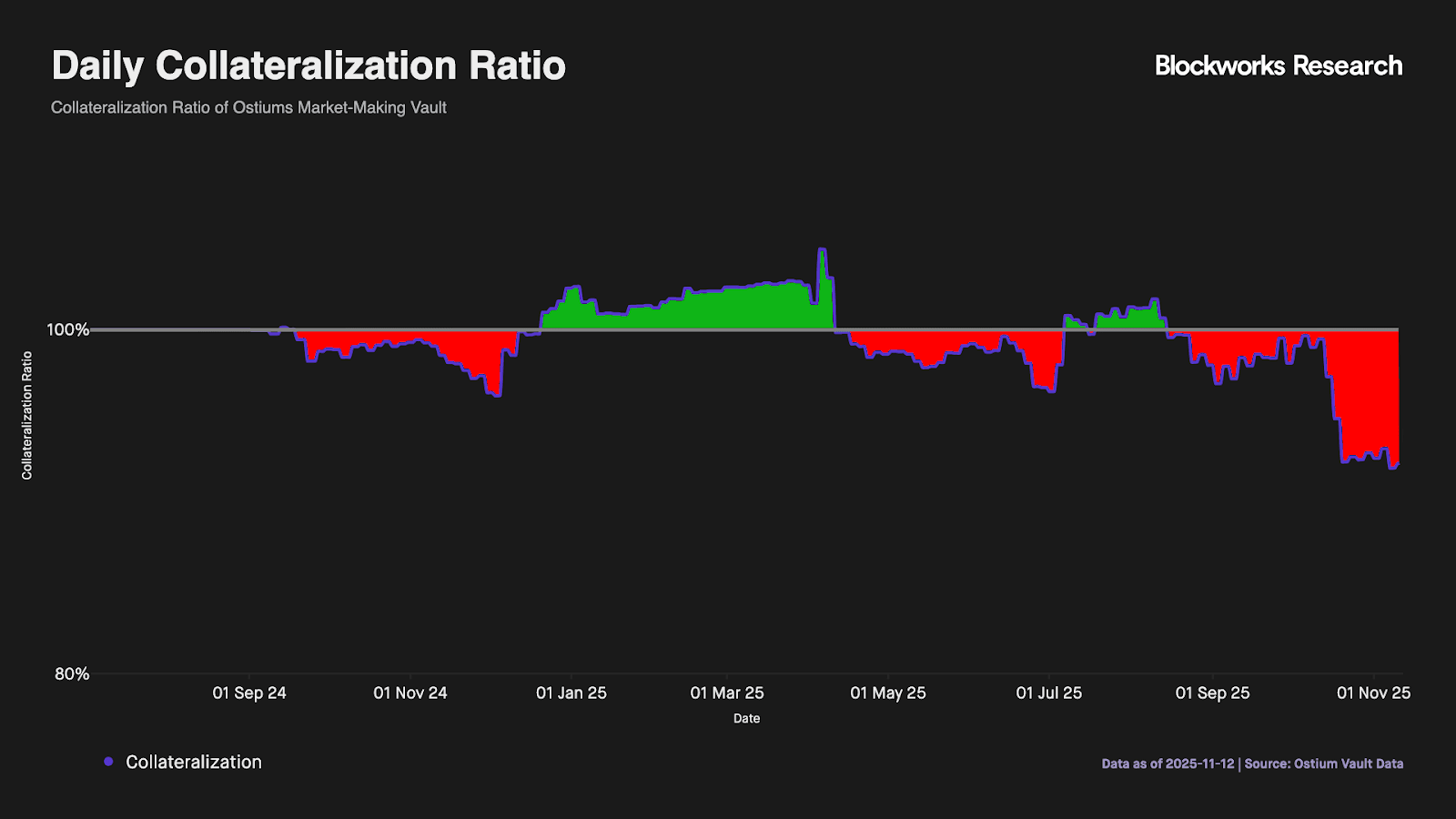

In practice, the data diverges sharply from the two‑tier design's theoretical protection. The vault has been Under‑Collateralized since 15 August 2025, with the c‑ratio reaching a low of approximately 91.9%. This means the Liquidity Buffer has been fully depleted; 8% of the cumulative fee cushion has been consumed by trader profits.

The OLP has served as the live counterparty for roughly 85 days (the longest under‑collateralized episode), and 100% of the last 30 days have registered c‑ratio below 1. Despite this, the OLP token trades at approximately $1.08 because total fee accrual ($3.84M) still exceeds the trader P&L losses allocated to the OLP ($2.10M). However, fee income does not restore the c‑ratio; the vault requires roughly $2.10M in net trader losses or an external recapitalization to return to an over‑collateralized state.

The two-tier design works in theory, but trader profits have depleted the buffer in practice, collapsing it into a standard peer-to-pool structure with the same limitations that have historically constrained these models.

To prevent this directional exposure from becoming a solvency risk, Ostium employs a hybrid defense. Onchain, dynamic spread and funding mechanisms incentivize traders to correct Open Interest imbalances naturally. Simultaneously, market makers actively hedge exposure offchain. This approach externalizes delta risk to established traditional venues. By executing offsetting trades on the underlying asset, these actors neutralize the directional exposure of the pool.

Ostium’s risk dashboard validates the efficacy of this hybrid defense, demonstrating a 90% reduction in Value at Risk (VaR) from roughly $743K down to $66K. Functioning similarly to a traditional CFD broker, the protocol utilizes dynamic fees to encourage risk internalization (the "B-Book") while systematically externalizing residual Net Delta to TradFi venues (the "A-Book"). This allows Ostium to hedge only the net imbalance rather than every individual trade, minimizing execution drag

However, this mechanism is not without structural flaws. The OLP retains significant residual exposure, forcing LPs to take concentrated bets rather than remaining market-neutral. Unlike orderbook models, traders execute against an oracle price before the hedge is finalized, creating a liability window where the pool holds unhedged "B-Book" risk until it can externalize the position. As such the OLP has drawdowns which should not exist for a truly hedged position.

Furthermore, the magnitude of these pre-hedge imbalances indicates that endogenous mechanisms alone cannot balance the book; because the majority of positions are directional and require active offchain hedging, the protocol effectively functions as an actively managed fund rather than a passive peer-to-pool, a dependency that structurally restricts the venue to traditional 24/5 market hours.

Ostium Synthesis

Ostium delivers genuine advantages for traders, which explains its historic dominance in RWA volume: direct oracle pricing eliminates slippage, SOFR‑based rollover offers cheaper carry than crypto‑native perps, and the UX is efficient during market hours. The two‑tier buffer is theoretically elegant—insulating LPs from P&L volatility while the Liquidity Buffer absorbs shocks—and the OLP token continues to trade above par at ~$1.08.

However, these benefits come with a distinct structural cost. The constraint is not that the protocol cannot hedge, but rather that it is operationally dependent on physical offchain hedging to remain solvent. While the hybrid model successfully neutralizes the majority of delta risk, it forces the venue to mimic TradFi hours, halting execution on weekends and breaking 24/7 composability. Furthermore, the persistent depletion of the Liquidity Buffer reveals that this hedging is not frictionless; LPs suffer from execution drag and the latency between trade acceptance and hedge execution, and TVL is still a constraint for positions.

Consequently, Ostium struggles to capture meaningful platform revenue, as fees must flow directly to liquidity providers to compensate them for this risk rather than being retained by the protocol. Nevertheless, with a fresh $24M Series A supported by leading market makers, Ostium stands as a sophisticated onchain replication of the CFD model.

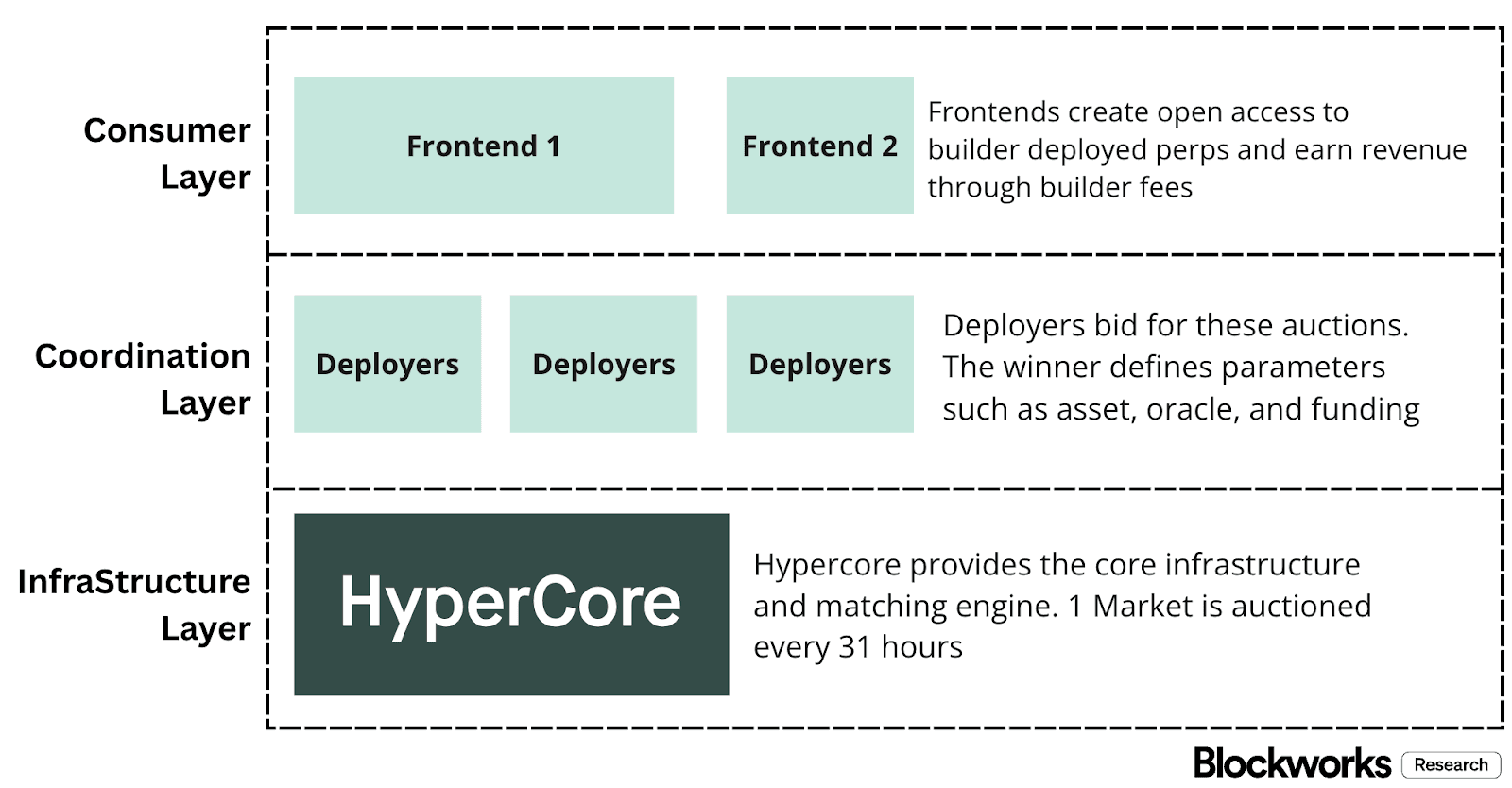

Hyperliquid: Equities Via HIP-3 Deployers

HIP-3 Overview

We have discussed Hyperliquid's end goal in depth. HIP-3 represents the structural evolution of this thesis: transforming Hyperliquid from a vertical exchange to a settlement infrastructure layer. By decoupling market creation from the core exchange engine (HyperCore), the protocol replicates the disaggregated clearing model of traditional finance (DCM/DCO). This architecture allows Deployers to function as broker-dealers, competing on distribution and fees while inheriting a unified, institutional-grade risk engine.

In addition to abstracting the complexities of orderbook infrastructure (analogous to the DCM and DCO technology in crypto for a fully integrated exchange), HIP-3 offers multiple benefits. First, deployers inherit Hyperliquid's battle-tested infrastructure, the same engine that processed $3.22T in volume. Second, it plugs into Hyperliquid's distribution layer; markets appear on Hyperliquid's native frontend and can be integrated by builders (who drive 37% of users) on wallets like Phantom.

To create these markets, deployers stake 500k HYPE (subject to slashing for irregular behavior), plug mark and oracle inputs into HyperCore's unified engine, and capture 50% of fees. Recently, Hyperliquid enabled a Growth Mode that reduces user fees by 90% to competitively bootstrap liquidity against centralized venues and attract initial liquidity. This enables permissionless and performant markets ranging from trading cards to pre-IPOs, with equity perpetuals as a primary use case. Here, two players have emerged: Unit's Trade XYZ and Felix's Trade Product.

Unit’s Trade.xyz

Overview

Trade.XYZ is built by HyperUNIT. To understand Trade.XYZ’s positioning, one must analyze Unit’s role within Hyperliquid’s ecosystem. While HIP-3 outsources perpetual market creation and has only recently launched on mainnet, the concept of Hyperliquid outsourcing its markets was already established via HIP-2, the protocol's spot token standard.

Just as HIP-3 requires complex oracle design, HIP-2 requires bridging infrastructure. Native BTC, ETH, and SOL must be custodied, verified, and minted into HIP-1 wrappers (UBTC, UETH, USOL), then burned on withdrawal for the asset to be tradable on Hyperliquid.

Rather than manage this process internally, Hyperliquid decentralized it and allowed any deployer to bid and create spot markets. Unit, led by Shoku, captured dominant market share by establishing itself as the primary tokenization layer. By handling deposit and withdrawal flows, finality checks, and deploying not only core majors (BTC, ETH, SOL) but also native launches like PUMP and listings such as Plasma’s XPL, Unit secured a collateral moat.

Essentially all spot volume on Hyperliquid for majors (excluding HYPE) comes from Unit’s assets rather than Hyperliquid-deployed spot pairs.

Like HIP-3 markets, HIP-2 deployers receive 50% of fees, while Hyperliquid takes the remaining 50%. While this raises questions about value leakage, Unit has so far used all revenues to buy back HYPE, creating an alignment mechanism similar to the assistance fund.

With HIP-3 live on mainnet, Unit launched Trade.XYZ as its equity-perp deployment. The philosophy remains unchanged: Unit handles market listings, while Hyperliquid supplies the DCM/DCO-style infrastructure. The builder-defined pattern that succeeded on spot (shared fees, protocol-provided exchange logic) now maps onto equity perps, with Unit again acting as the primary builder.

Trade.XYZ debuted a whitelist-gated frontend with its first product, the XYZ100 perpetual, a modified cap-weighted US large-cap index. Unit has already won auctions for TSLA, NVDA, GOLD, HOOD, INTC, PLTR, COIN, META, AAPL, and MSFT as the sole HIP-3 bidder currently operating. Given Unit’s dominance in HIP-2 spot market share, it occupies a strong competitive position to capture equity-perp flow.

Felix Trade

Overview

Like Unit, Felix entered HIP-3 from the infrastructure side. On HyperEVM, Felix operates the feUSD CDP (a Liquity-v2–style over-collateralized stablecoin) and Vanilla variable-rate lending, giving traders venue-native credit and stable liquidity. The protocol focused on broad financial primitives, though this generalist approach has increasingly been overtaken by specialized projects. Its USDHL stablecoin was effectively replaced by the native USDH ticker, and its lending model faces pressure as Hyperliquid begins testing its own Borrow/Lend Protocol in-house.

We view Felix’s model as an "integrated financial suite" within the ecosystem. Similar to Jupiter on Solana, it offers a set of complementary products built on HyperCore that bridges HyperEVM, including a trading frontend, stablecoins, and now perpetuals. With HIP-3 live on mainnet, Felix launched its own builder-deployed DEX focused on single-ticker equity perps, with the goal of enabling a cross-margin exchange. To execute this, Felix partnered with Hyperion DeFi in a strategic partnership to build its HIP‑3 equity markets and earn its 500k Hype requirement.

With two players competing, differentiation becomes critical. Both deployers can create markets for the same underlying (e.g., Unit and Felix both offer TSLA perps). Before HIP-3 integration into Hyperliquid’s frontend, owning distribution and user flow mattered. Now, as the frontend aggregates all markets, the specific DEX brand matters less than liquidity and cost. As seen in Hyperliquid UI below, the perp DEX name itself remains the only differentiator for users who, in practice, understand little about oracle differences and will simply trade the most liquid market.

Felix's approach to compete against UNIT with its equity markets is to denominate its perps in USDH rather than USDC, making its perpetual exchange "Hyperliquid Aligned." This grants users tangible economic benefits: 20% lower taker fees, 50% better maker rebates, and 20% more volume contribution toward fee tiers following Hyperliquid's stablecoin mandate. Additionally, USDH has pledged 50% of its revenues as incentives to aligned HIP-3 markets.

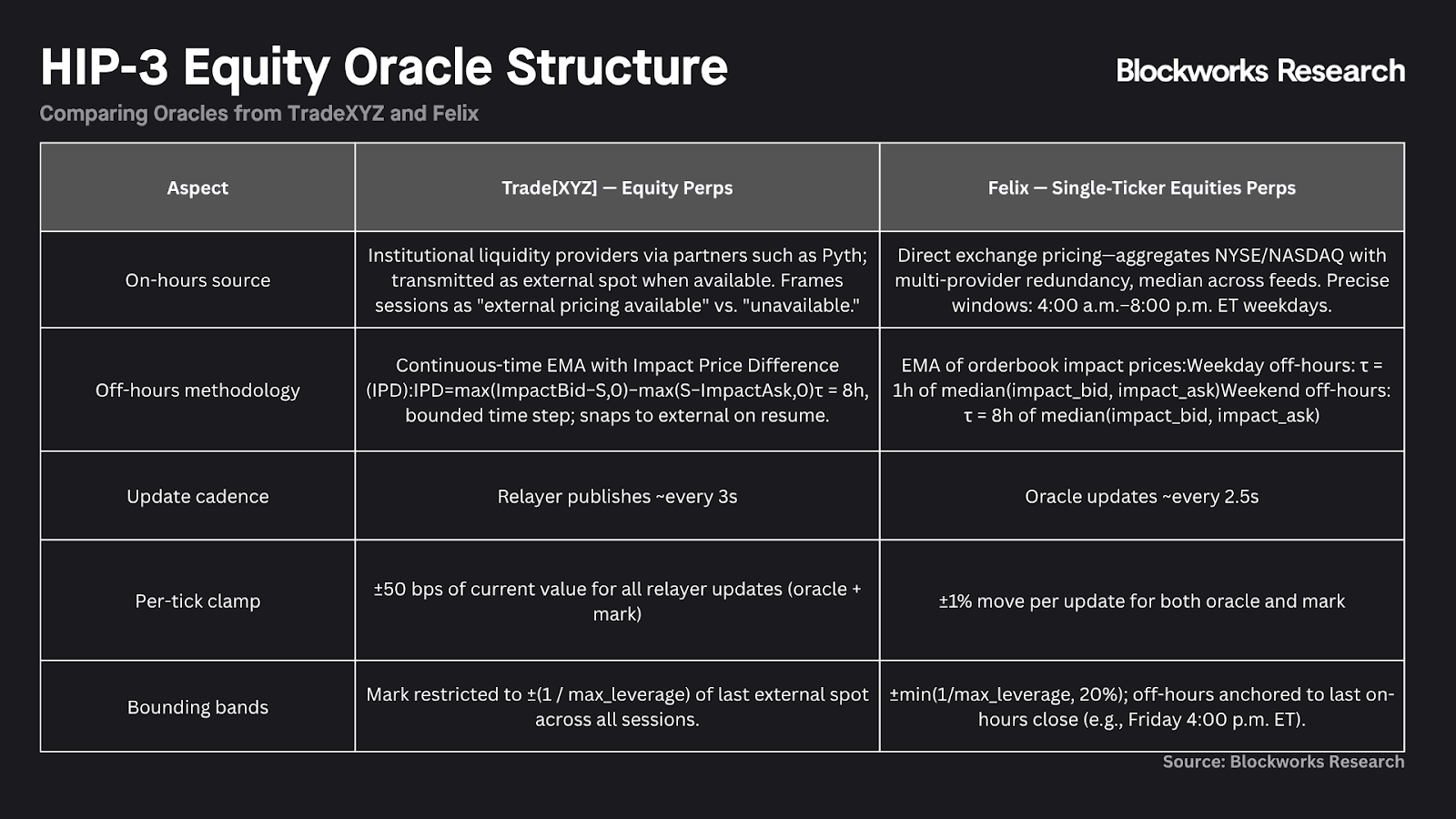

Trade and Felix: Oracle and Mark Infrastructure

Both support weekend price discovery via internal pricing. With no external liquid venue, market makers may arbitrage between the two, keeping prices aligned. The critical detail is the bounding bands, which cap off-hours deviation. Trade uses ±(1/max leverage); Felix uses the lower of 20% or ±(1/max leverage). This range guarantees that hedged positions cannot move beyond a defined bound when adjustments are impossible.

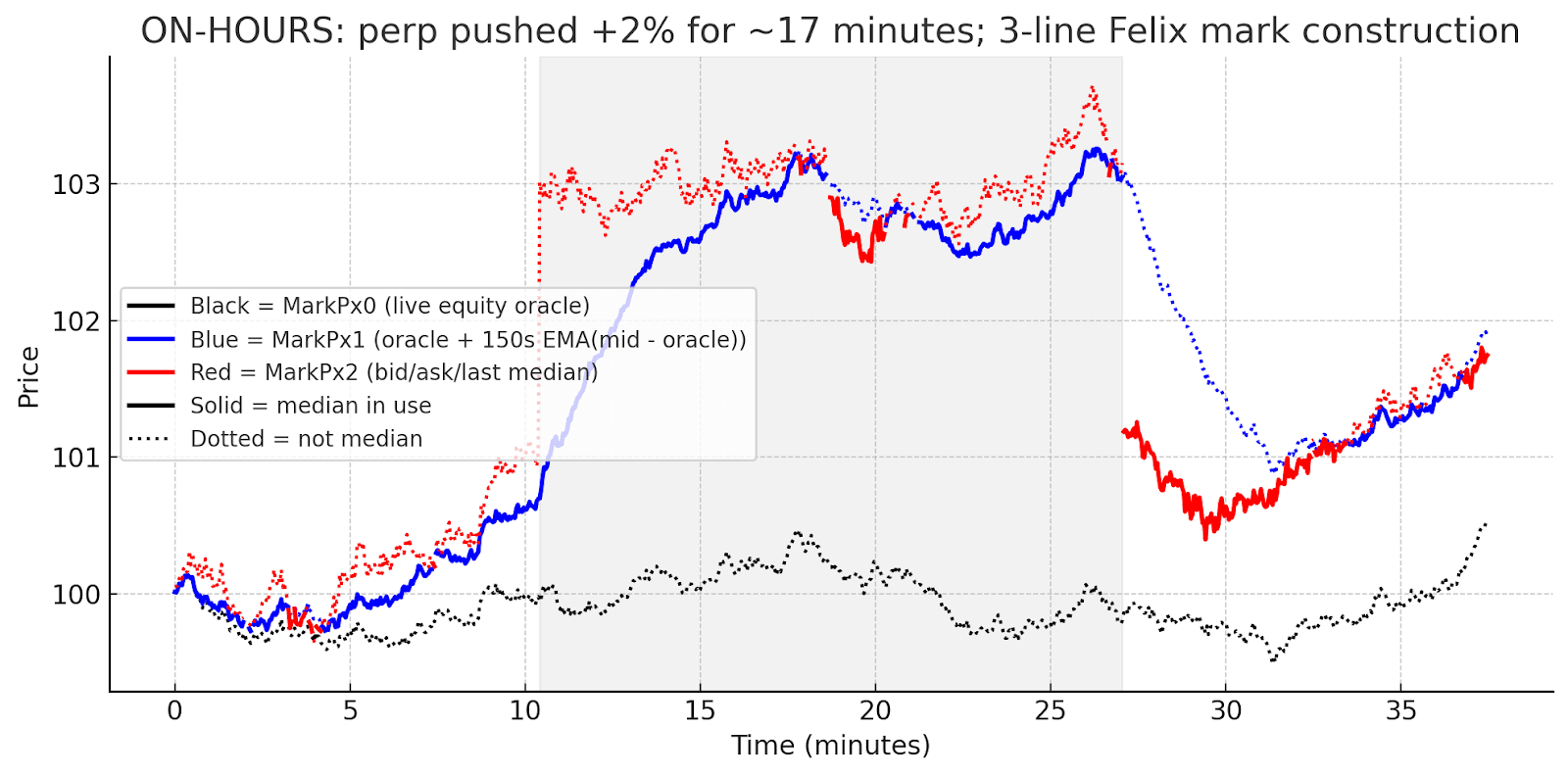

With billions of dollars potentially in open interest, internal pricing must remain stable to prevent mark-price liquidations (such as manipulating the internal price to trigger forced liquidations). To test this, we examined Felix’s methodology and simulated an attack.

During trading hours, we simulate an attacker pushing the perp price above the underlying stock price. The perp input reacts instantly, but the mark (which is the median of the live stock oracle, the perp price, and a smoothed basis) only follows if the attacker sustains the premium long enough for the Exponential Moving Average (EMA) to adjust. In practice, the mark can be moved, but only through real, prolonged trading rather than momentary spoofing.

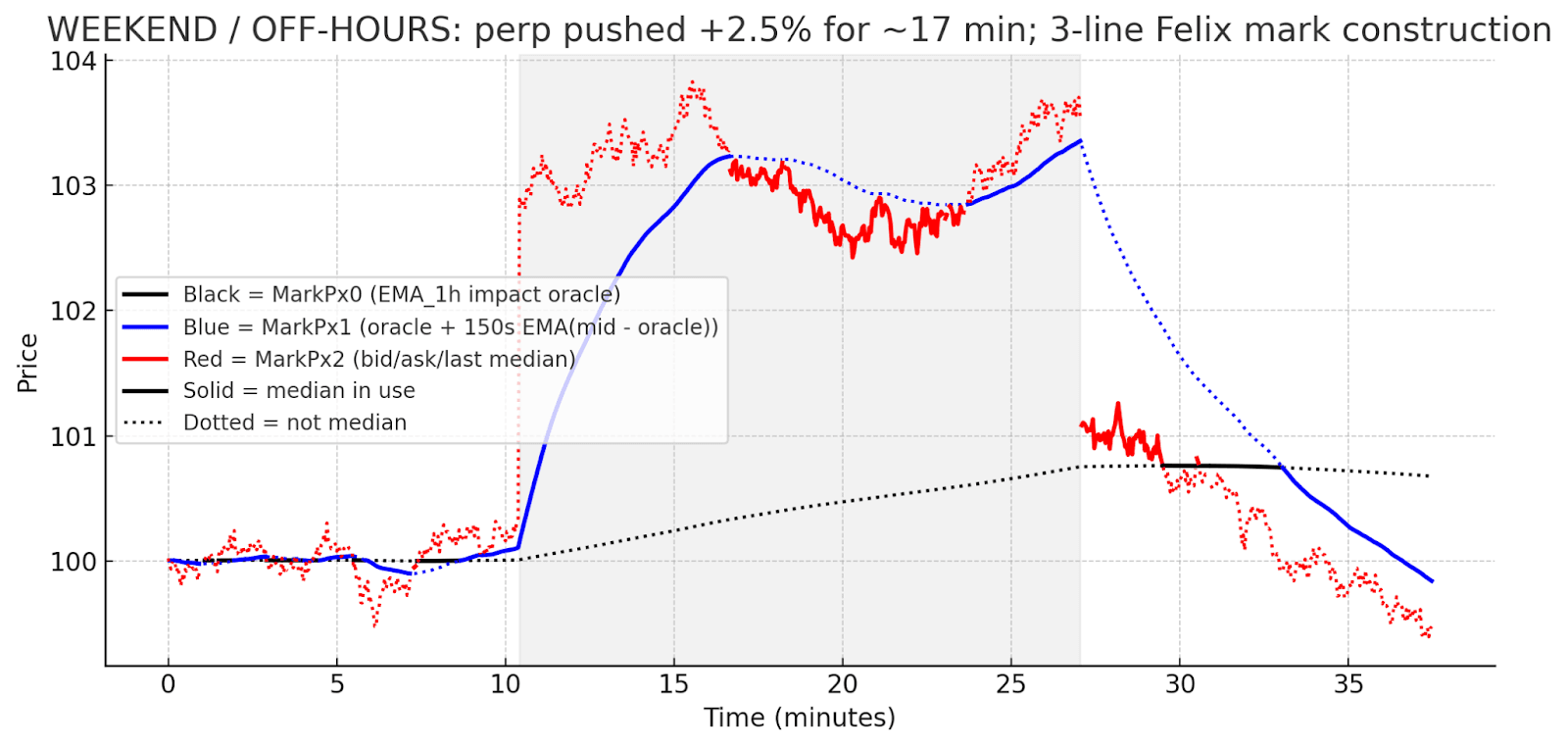

Off-hours, the system relies on its impact-driven internal oracle. If an attacker keeps lifting the perp long enough, both the short-term basis and the slow internal oracle drift upward. In other words, the price can be manipulated on weekends, but only through sustained, size-backed buying.

In summary, the median-of-three construction does not eliminate manipulation. Attackers can still move the mark if they commit real capital for long enough, especially off-hours when the oracle is impact-driven. However, the bounding band limits how far this drift can extend. Because the band is set to the maximum move that would liquidate a fresh max-leverage position, actively managed positions during the week face no liquidation risk from weekend volatility. When markets reopen, the oracle snaps back to live equities, collapsing weekend distortion toward fair value. This also makes manipulation economically inefficient because attackers cannot trigger liquidations that would allow them to profit.

Overall, we believe this approach is suitable for trading in its current form, given its clear limits on tail risk and its predictable re-anchoring at market open.

Trade and Felix: Liquidity

While HyperCore infrastructure provides performant orderbooks, HIP-3 deployers still have to source and coordinate liquidity for their own markets. Mark price methodology and bounded pricing ranges reduce the risk of extreme gaps or disorderly liquidations, but actual depth and two-way flow determine where traders route volume when tickers are otherwise undifferentiated.

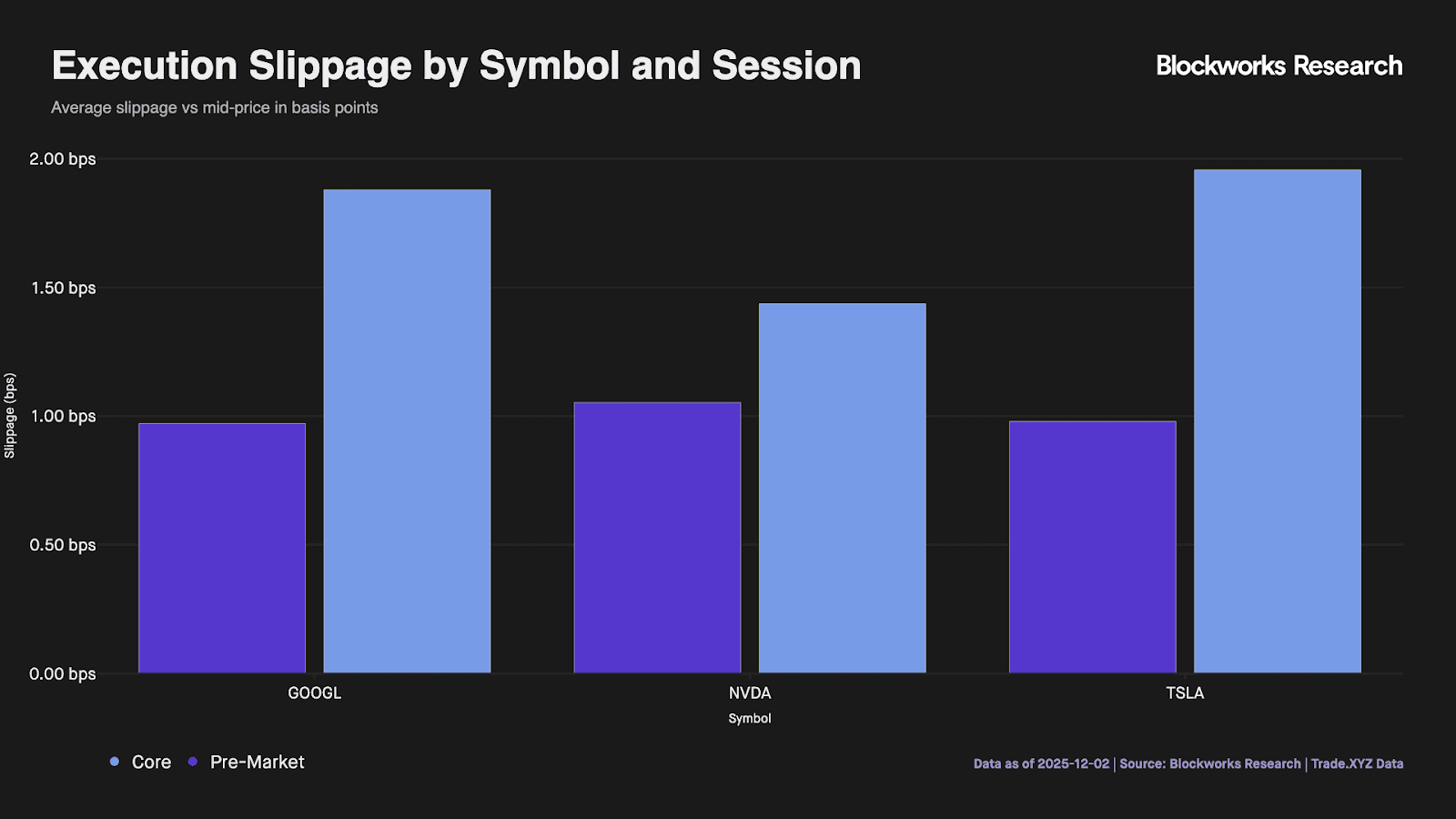

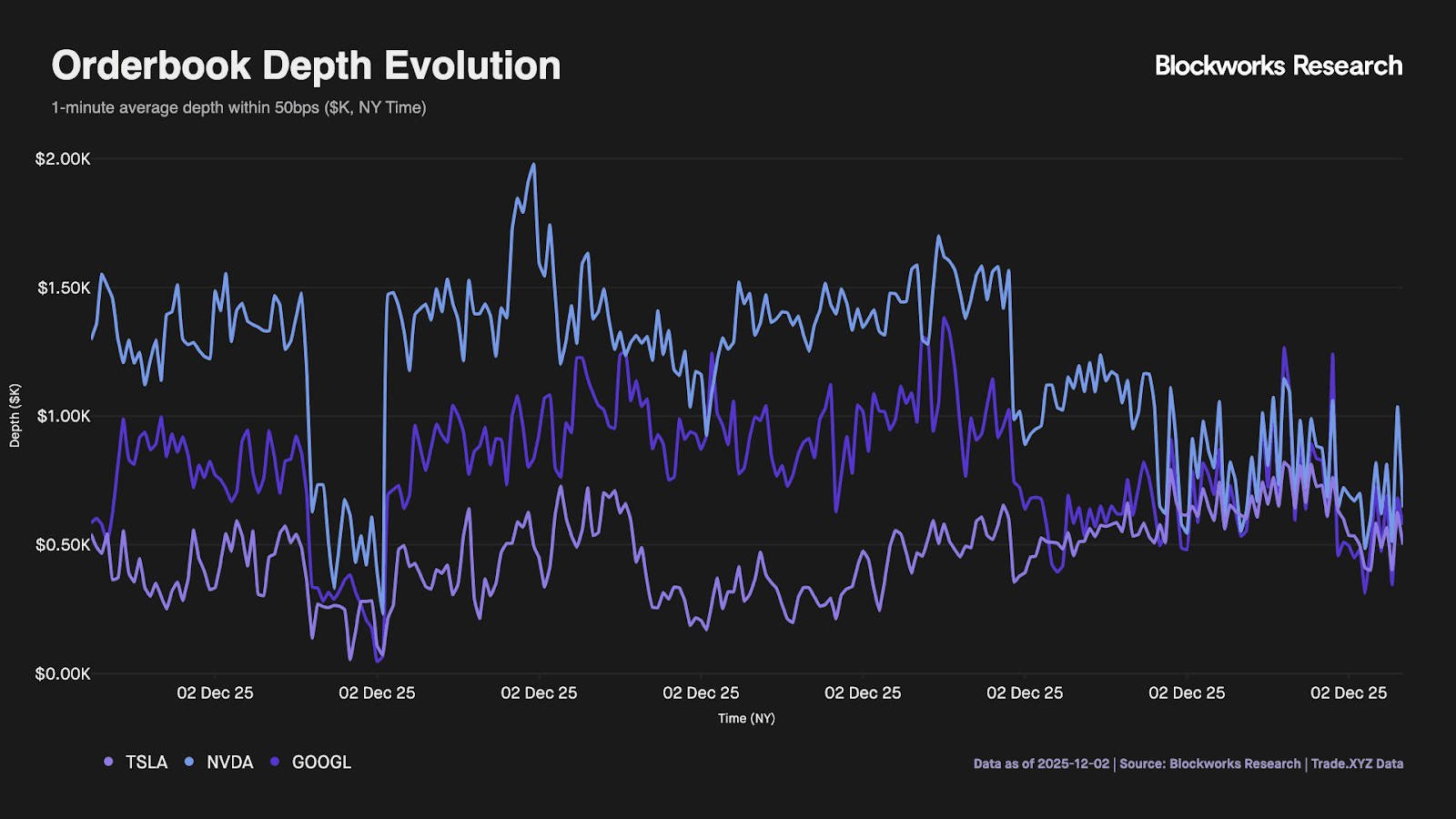

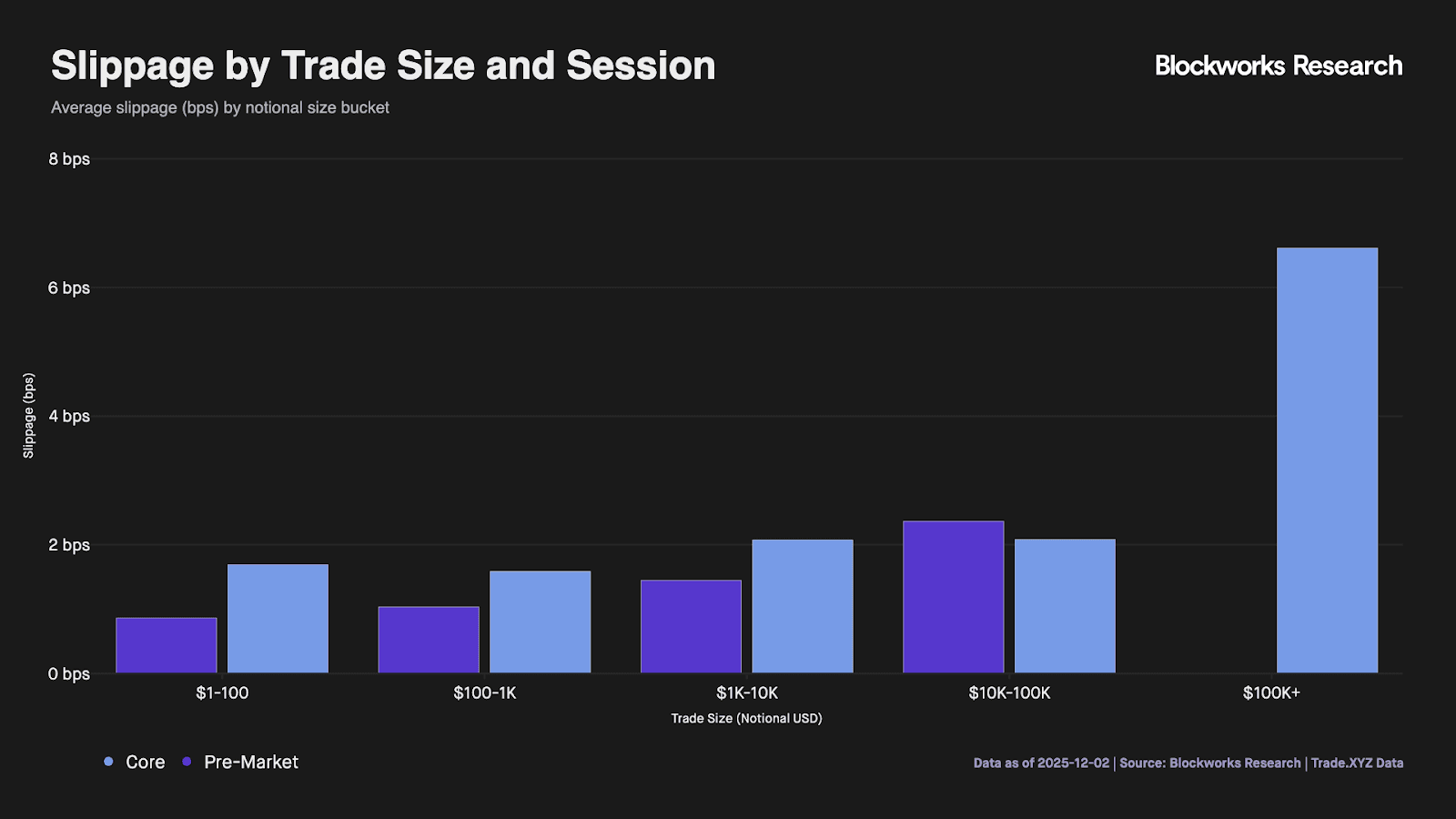

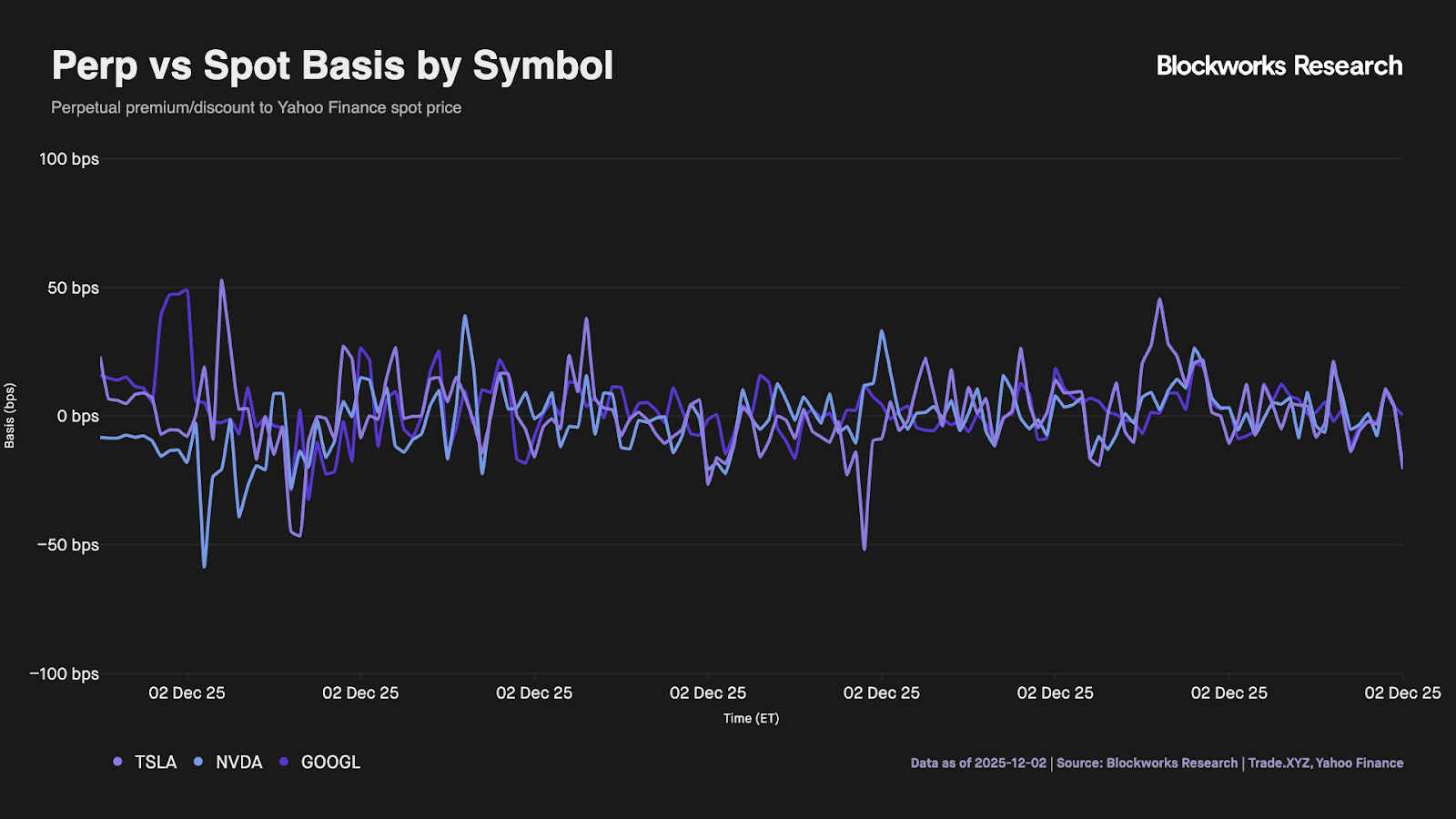

To validate whether HIP-3 equity perpetuals meet these design requirements, we conducted a liquidity study of Trade.XYZ's single-stock markets on Dec. 2, 2025, capturing approximately 79K orderbook snapshots and 32K trades across NVDA, TSLA, and GOOGL. We segmented the data into Pre-Market (6:30–9:30 AM ET) and Core (9:30 AM onward) sessions to isolate periods when traditional hedging venues are closed versus open.

Bid-ask spreads averaged 1.7 bps across all symbols. This compares favorably to traditional overnight equity trading, where spreads typically exceed 25 bps. Notably, Pre-Market spreads were 40–55% tighter than Core session spreads across all three symbols. This inversion of traditional liquidity dynamics suggests that crypto-native market makers are aggressively pricing the gap risk during off-hours to capture early flow.

Orderbook depth showed similar dynamics: average notional depth within 50 bps of mid-price reached $860K during Pre-Market versus $720K during Core hours. NVDA and GOOGL maintained deeper Pre-Market books, while only TSLA exhibited the conventional pattern of thinner off-hours liquidity. All three symbols displayed persistent bid-side imbalance (2 to 3.6x), indicating net long positioning and suggesting market makers are absorbing directional demand rather than facilitating balanced two-way flow (similar to what was seen in pre-markets on BOATS where liquidity is skewed on off hours).

Slippage scales modestly with size: small trades ($1-100) average 1.40 bps while large orders ($10K-100K) see 2.12 bps. Solid execution quality for a nascent market, but volume remains constrained to retail-scale flow, with only four trades exceeding $100K during the 4-hour sample period.

Finally, comparing perp mid-prices to underlying spot data, the average tracking error comes in around 10 bps. GOOGL tracks tightest at 8.6 bps, and TSLA loosest at 10.6 bps. About 36% of observations land within 5 bps of spot.

The liquidity profile demonstrates that HIP-3 infrastructure can support equity perpetuals at retail scale. Sub-2 bps spreads, controlled slippage, and 10 bps average tracking error represent viable market quality for an early-stage venue. Off-hours performance is particularly notable; Pre-Market spreads of 1.3 bps compares favorably to traditional overnight equity markets, where spreads typically exceed 25 bps and liquidity is sparse.

However, depth constraints above $100K notional, elevated tracking error relative to institutional benchmarks, and persistent bid-side imbalance indicate the market is not yet positioned for institutional adoption.

HIP-3 Synthesis:

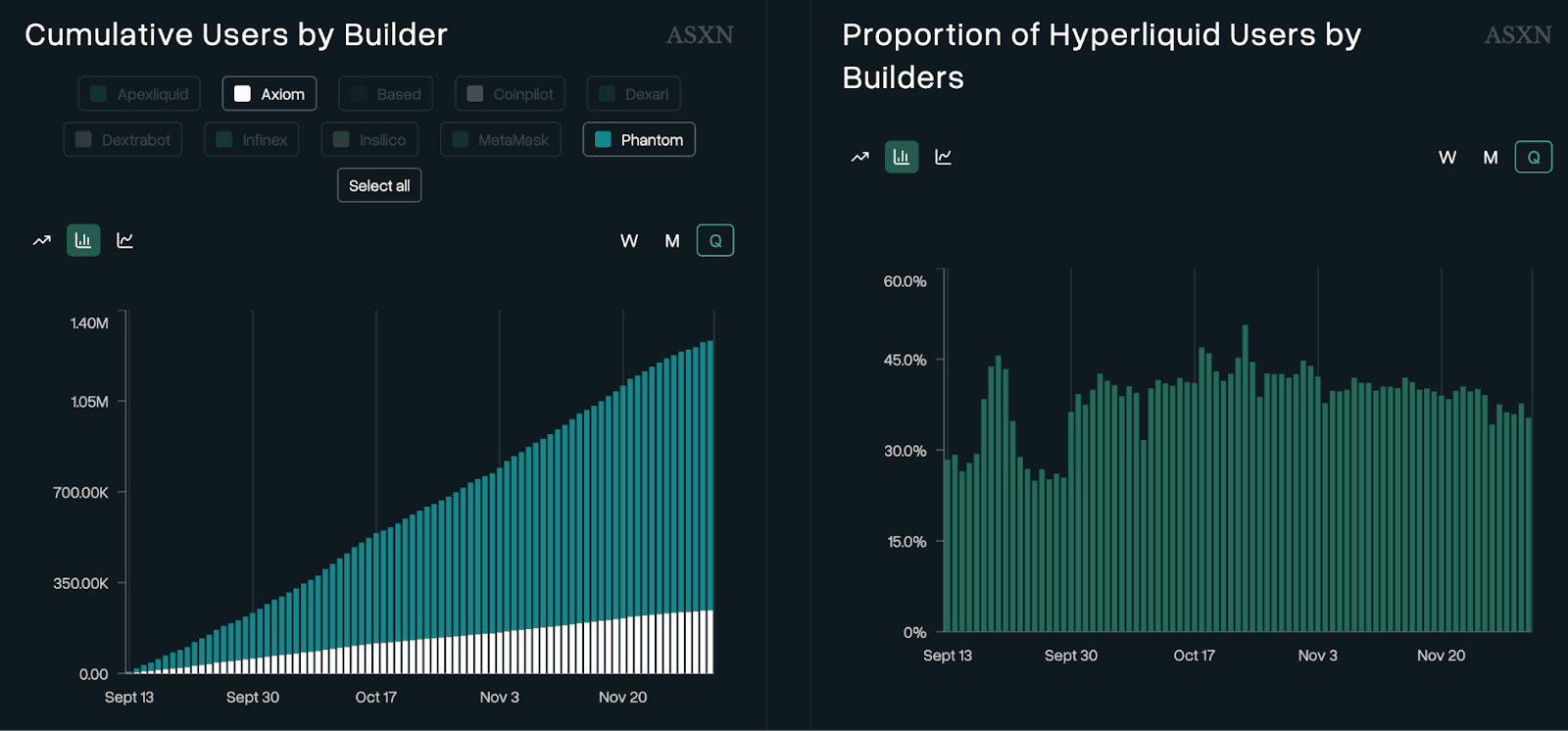

Hyperliquid's HIP-3 approach provides robust orderbooks and, critically, channels builders into a large established audience. Unlike traditional perp exchanges that must bootstrap from zero, traders can use existing collateral and their frontend of choice, whether Hyperliquid's native interface (880k cumulative accounts) or integrated builders like Phantom and Axiom (275k referred users).

Despite only two HIP-3 equity deployments being live, the competitive environment is already exhibiting monopolistic tendencies. Unit holds a commanding position and continues bidding daily. By winning nearly every auction, Unit effectively blocks new entrants and prevents liquidity fragmentation. With minimal product differentiation available on the frontend, liquidity naturally aggregates to the incumbent.

Felix attempts to challenge this monopoly through vertical alignment and incentives. First, by using USDH as its quote asset, Felix offers 20% lower taker fees and 50% better maker rebates compared to Unit's USDC markets. Second, Felix's live points program creates a speculative mechanism that Unit cannot match without deploying a token. When product offerings are otherwise identical, these incentives theoretically offer a path to shift volume.

However, this reliance on USDH acts as a structural constraint on distribution. While economically efficient for power users, USDH introduces integration friction for external builders. Major wallets like Phantom prioritize USDC for user experience and are unlikely to route to USDH-denominated markets to avoid confusing retail users. This structurally limits Felix’s visibility on the ecosystem's most potent distribution channels, effectively fencing its liquidity off from the broader aggregator layer.

Furthermore, Hyperliquid’s implementation of "Growth Mode" has arguably diluted Felix’s competitive wedge. By slashing protocol-level fees by 90% across all markets, the absolute economic benefit of Felix’s fee discounts has been compressed to a negligible margin. Without a significant cost differentiator to overcome the USDH friction, liquidity has aggregated around the incumbent’s network effects. Consequently, Unit has consolidated approximately 98–99% of daily volume share, establishing a near-monopoly that will be structurally difficult to disrupt without a fundamental shift in incentive design.

Regardless of how these internal competitive dynamics resolve, the HIP-3 framework has successfully secured the equities infrastructure layer for Hyperliquid, and, through builder distribution and performant markets, we believe HIP-3 will continue to dominate the perpetual equity landscape.

Vest Exchange

Overview

While Hyperliquid's HIP-3 establishes a dominant framework, alternative architectures remain viable for specialized market participants. Protocols that build proprietary infrastructure retain several distinct advantages:

- Customizable Fees: Unlike HIP-3's standardized structure, independent protocols can implement bespoke fee models, including zero-fee structures for specific markets or traders.

- Unlimited Markets: Rather than competing in daily auctions, autonomous perp designers can deploy markets permissionlessly and scale horizontally without gatekeeping constraints.

- Vertical Integration: Full-stack control enables the development of proprietary risk engines, margin systems, and ancillary infrastructure tailored to specific use cases.

Interestingly, these alternatives may ultimately benefit from HIP-3's liquidity depth, as arbitrage flows between exchanges represent the most readily hedgeable volume source, naturally correcting price discrepancies across venues.

Vest Exchange exemplifies this alternative approach. In March 2025, the protocol raised a $5M seed round led by sophisticated trading firms including Jane Street, Amber Group, Selini, QCP, and Big Brain to develop zkRisk, a zero-knowledge risk engine that enforces consistent, verifiable risk pricing across all markets and products. As the inaugural application of this stack, Vest Exchange functions as a perpetual DEX where pricing, funding rates, and capital allocation derive from a unified, mathematically coherent risk framework rather than ad-hoc open interest caps or venue-specific heuristics.

Liquidity

Liquidity

Vest further distinguishes itself through a unique liquidity architecture. The protocol maintains a Vest Liquidity Pool that dynamically hedges exposures offchain on established traditional venues such as NASDAQ and CME. This strategy parallels Hyperliquid's HLP bootstrapping phase but introduces an innovation, as Vest's pool continuously adjusts its hedges in response to evolving risk parameters, ensuring more capital-efficient market making and tighter risk controls.

This model faces the immutable constraint of banking hours. While continuous adjustment is viable intraday, weekend hedging remains structurally impossible without OTC arrangements. Additionally, Vest's competitive fee structure helps attract market makers who might struggle with higher fees elsewhere. It is important to note that Vest markets use a 1% fee on weekends, and 0.05% fee during extended hours to price this specific risk.

Solana Equity Perpetuals

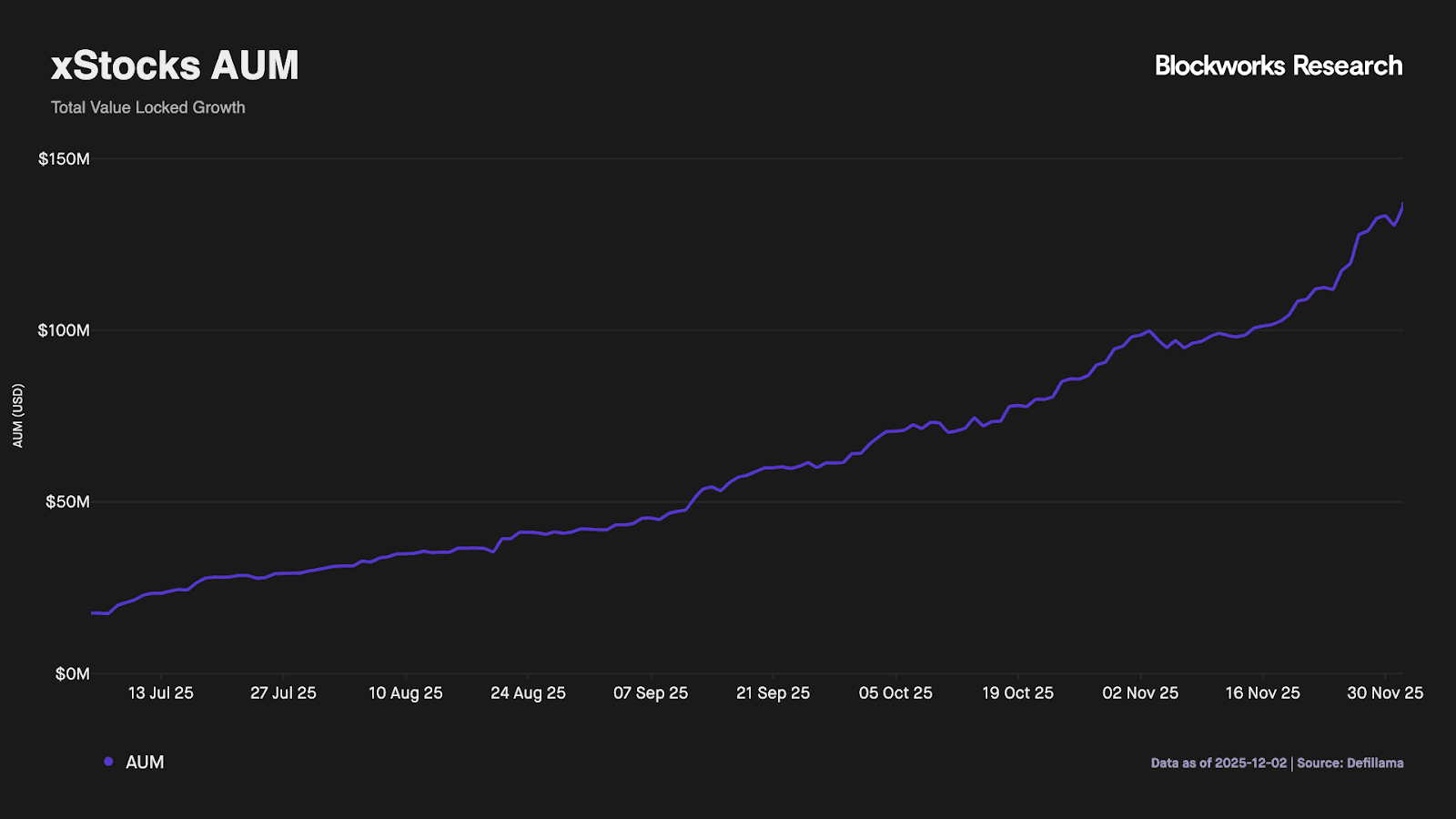

The Solana landscape represents a natural ecosystem for equity perps due to its focus on high-throughput, institutional-grade architecture. Co-founder Anatoly Yakovenko has described the network’s vision as “Nasdaq, but on a public, permissionless blockchain,” a goal that is finally materializing in the spot market. Since June 2025, over 60 tokenized major US stocks and ETFs (including Apple, Nvidia, and the S&P 500) have become available to non-US persons. This sector has seen impressive traction, with Solana-based xStocks reaching >$150M in AUM, alongside institutional validation from Galaxy Digital tokenizing its GLXY equity via Opening Bell and Superstate.

However, while Solana dominates onchain spot equities, it faces a steep uphill battle in the perpetuals market against Hyperliquid. Crucially, Hyperliquid has negated the usual advantage of general-purpose chains. Through Builder codes, they have secured direct integration with Phantom and Axiom, allowing users to access HIP-3 equities via the Phantom wallet without needing to bridge or leave their preferred wallet environment or ecosystem.

Source: ASXN Dashboard

Despite Hyperliquid’s distribution lead, Solana retains a potential structural advantage: proximity to the underlying spot assets. Unlike Hyperliquid, where the ecosystem is primarily derivative-focused, Solana hosts the actual tokenized stocks (xStocks). This offers a theoretical edge for market makers, since hedging between the perpetual product and underlying spot is simpler than routing into offchain equity liquidity. Protocols focused on scaling composability, such as Drift, are also positioned to address the cost of carry problem that plagues current onchain equity perps. In principle, users could collateralize xStocks (spot) to short an equity perp, creating a delta-neutral position that captures yield while mitigating funding costs.

To get there, protocols could:

- Enable cross-margin with xStocks as collateral. Here there is a clear advantage over HIP-3, where each market is still an isolated margin and only stablecoins can be used as collateral.

- Enable delta-neutral carry trades by allowing xStocks as collateral.

This setup could solve a number of issues. Perpetual DEXes can use the xStock oracle price (provided there is enough liquidity) and, since xStocks already trade 24/7, there is no need to constantly update oracles around equity market hours. The perp would effectively be written on the tokenized stock rather than the underlying offchain listing. This makes position management much simpler and allows users to hedge efficiently using xStocks as collateral. If liquidity is sufficiently deep, listing a new equity perp becomes almost as trivial as listing a crypto perp, since the instrument references the xStock market rather than stitching around legacy equity venue schedules.

Gate.IO has effectively validated this design on a centralized stack by listing perps on Backed-issued xStocks and allowing users to trade perps and the corresponding tokenized equities within a single margin system. Now that Kraken has acquired Backed, the same playbook is available: Kraken can combine its existing perp infrastructure with natively issued xStocks and potentially list equity perps that hedge directly into xStock spot. This is a clear expansion opportunity for Kraken, and by extension for Solana perps that can route into this liquidity, even if Solana-native perp protocols have not yet realized this margining and hedging opportunity in practice.

Gaining Exposure to Tokenized Equities

With the potential of tokenized equities clear and the landscape of key venues laid out, it is worth examining how to gain exposure to this trend. In practice, this is difficult, as none of the assets currently have tradable tokens.

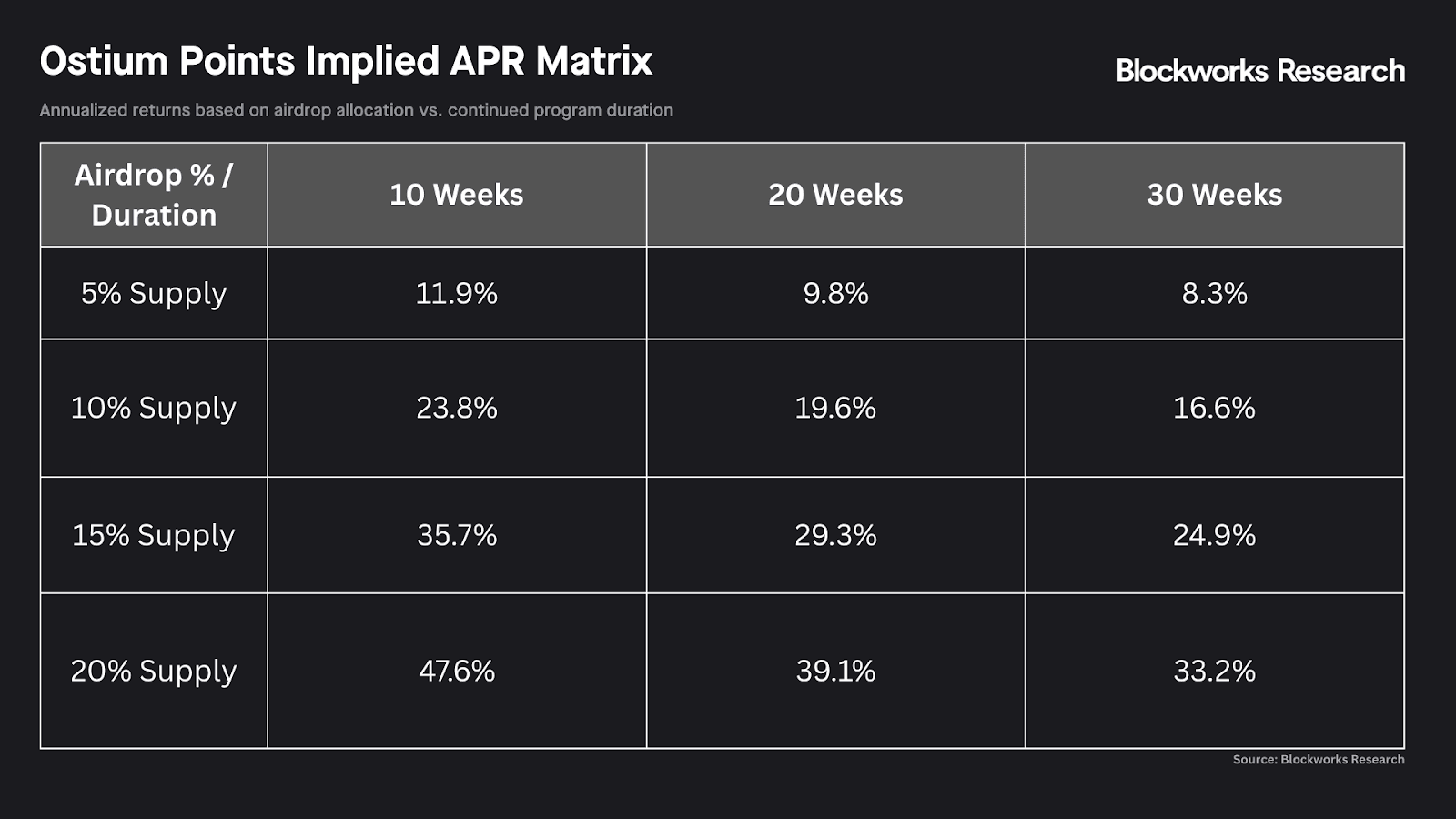

- Ostium: The protocol runs an active points program distributing 500,000 points weekly, split between trading volume and liquidity provision. While the OLP vault has exhibited historical volatility and periods of drawdown due to hedging friction, the incentives currently present a compelling opportunity given Ostium's recent Series A valuation of around $250M. The program has run for approximately 36 weeks, implying a current circulation of ~18M points. Based on our internal calculations from a monitored liquidity position, we constructed an APR matrix to project annualized yields, based on a $250M valuation. The analysis below estimates returns across varying airdrop allocations and potential campaign durations. We view an extension of the program (10–30 weeks) as the base case, as sustained incentives are structurally necessary to compensate LPs and attract sufficient capital to the vault.

- Unit / Trade: No token and no points program; the venue functions as Hyperliquid’s integrated spot and tokenized equity engine, with revenues directed into HYPE buybacks. It is unclear whether Unit requires a token at all, and the team has signalled in that direction. At this stage, Unit effectively operates as an extension of Hyperliquid itself rather than as an independent, value-accruing protocol.

- Felix: Lending layer with an active points program for liquidity provision and borrowing, which we have outlined in a previous report. At present, incentives are distributed on liquidity provision rather than on trading volumes, so exposure is primarily obtained by supplying and borrowing assets to accumulate points.

- Vest: 1 million weekly points program split between trading and VLP deposits, with a structural bias toward smaller accounts. Points are awarded pro rata based on weekly volumes, with a 1.5x multiplier for equity trading and additional allocation for VLP deposits, so exposure is gained by combining trading activity with VLP provision to build a points balance ahead of a potential token launch.

Therefore, unfortunately, there still exist limited paths to exploit this trend, beyond simply allocating to HYPE as the token that captures Unit’s HIP-3 market activity, with Ostium, Felix and Vest offering only points-based, pre-token exposure.

Conclusion

US options markets generate $89T in monthly notional turnover ($24T equity, $65T index), with 0DTE contracts accounting for roughly $48T. This volume is driven by a revealed retail preference for high-leverage, short-duration directional exposure. However, the option contract itself is structurally inefficient for this use case, burdening traders with theta decay and volatility sensitivity while forcing execution during toxic liquidity windows. Perpetual futures replicate the desired payoff profile more cleanly, offering linear exposure and 24/7 continuity that aligns with the market reality where the majority of net equity returns now occur overnight.

Structural barriers in the United States act as the primary catalyst for onchain migration. The Shad-Johnson Accord serves as a binding constraint for domestic incumbents, effectively blocking single-stock perpetuals due to a lack of dual-clearing infrastructure. This regulatory gridlock inadvertently favors decentralized architectures capable of servicing the $42T in annual non-US volume, particularly the 80% of overnight flow originating from the APAC region. Simultaneously, the proliferation of permissionless, third-party frontends ensures that access will proliferate globally — including into the US

We expect the next 12–18 months to be defined by consolidation around HIP-3. Hyperliquid has effectively secured the infrastructure layer, and the internal battle for liquidity appears largely settled. Unit (Trade.XYZ) stands as the undisputed category leader, commanding nearly 99% of daily volume. While Felix attempts to compete, its economic wedge is currently blunted by the distribution friction of USDH and the dilution of fee advantages under 'Growth Mode.' Consequently, until Felix launches a native token or Growth Mode expires, the market structure is likely to remain static with Unit as the entrenched monopoly.

In contrast, Ostium presents a viable alternative to the dominant CLOB model. While active orderbooks like Hyperliquid drive massive volume, they often suffer from volatile funding rates during directional moves. Ostium offers a middle ground by tweaking the traditional peer-to-pool architecture with a CFD-style hedging mechanism, prioritizing stable, predictable pricing for traders, albeit at the cost of 24/7 availability. However, liquidity provision remains the primary concern: the model's dependence on TVL restricts Open Interest and limits large-scale execution, while current liquidity levels appear heavily reliant on the protocol's points program to incentivize capital. Similarly, specialized engines like Vest are carving out niches for sophisticated makers via risk-coherent margining.

Solana represents a distinct structural outlier; the presence of xStocks theoretically enables an alternative design where the perpetual references the tokenized asset itself as the oracle rather than the equity feed, allowing for atomic cross-margining that bypasses legacy hedging constraints. However, until a major perpetual venue successfully integrates these assets to capture volume, this remains a latent architectural possibility rather than an immediate threat to Hyperliquid's hegemony.

This report was edited on December 9th, 2025. The original analysis included only equity options ($24T). We have since added index options (SPX, NDX), bringing total options notional to $89T, 0DTE notional to $48T, and the crypto comparison ratio to ~40x.

This content is for informational purposes only and should not be construed as legal, tax, investment, financial, or other advice. The views expressed are the author's alone and do not necessarily reflect those of Blockworks. This content is not an offer to buy or sell any securities or financial instruments. Blockworks does not provide investment advice and nothing in this content should be considered investment advice. Consult with your financial advisor before making any investment decisions.