Cross-chain Liquidity: The Next Iteration of Perp DEXs

Key Takeaways

- Derivatives in DeFi have shown significant growth, but the proliferation of new perp DEXs has led to fragmented liquidity across various DEXs and chains.

- Vertex, known for its vertically-integrated DEX that includes spot, perpetual, and integrated money markets, is now tackling cross-chain liquidity fragmentation through horizontal integration with the launch of new Edge instances.

- Vertex's integrated offerings and cross-margined account structure amplify the benefits of new instances: native cross-chain spot trading, optimized cross-chain basis trading, consistent interest rates, reduced bridging friction, and more.

- Edge transforms the typical subtractive creation of new protocols on new chains, which fragments liquidity, into a synergistic, value-additive endeavor, which is groundbreaking for a multi-chain future.

The DeFi space has witnessed an impressive proliferation of perpetual decentralized exchanges, with over 150 different derivatives protocols spanning multiple blockchain networks. This rapid expansion, driven by the strong product-market fit of perp DEXs, has led to fragmented liquidity across various DEXs and chains, presenting a challenge for traders and investors. TVL in DeFi derivatives has surged from $1.8 billion to $3.4 billion since the beginning of this year, highlighting the increasing adoption and demand for these products.

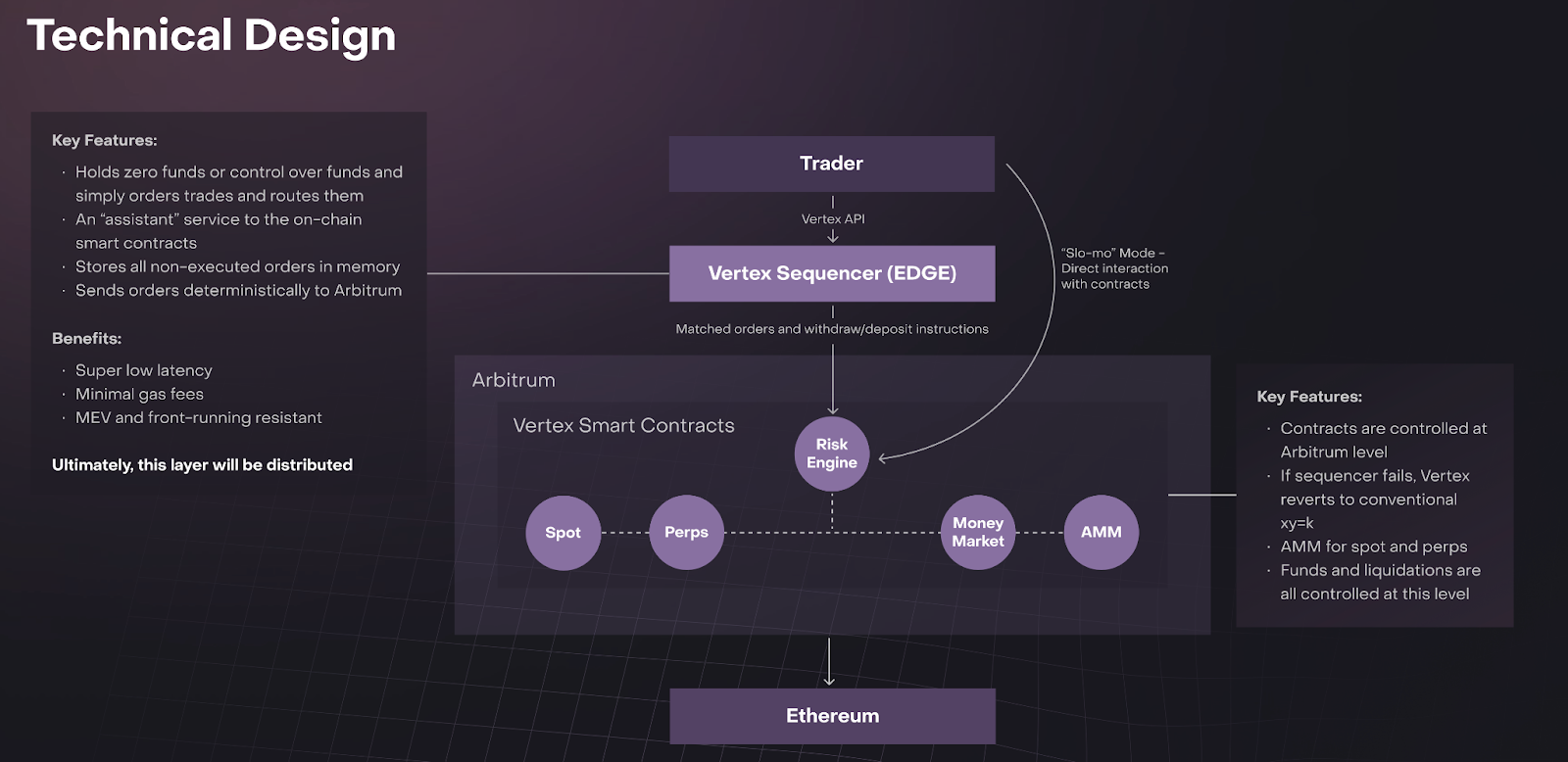

Vertex, known for its vertically-integrated DEX that includes spot, perpetual, and integrated money markets, is now tackling cross-chain liquidity fragmentation through horizontal integration. Vertex Edge, Vertex’s latest product, addresses this by offering synchronous orderbook liquidity, effectively unifying liquidity across different chains. Essentially an enhancement to the Vertex sequencer, Edge extends its capabilities to operate across any supported ecosystem. To fully appreciate Edge's potential, let’s revisit Vertex’s architecture and understand how this upgrade integrates into its existing framework.

Vertex Overview

Vertex employs a hybrid orderbook AMM design. Its trading and risk engine, which encompasses all Vertex products such as spot, perpetuals, and money markets, operates onchain and is governed by smart contracts on Arbitrum. Meanwhile, the sequencer, acting as a high-performance orderbook that matches inbound orders from the protocol layer, operates offchain. This creates a hybrid model where the sequencer handles trade ordering and routing. In this system, the onchain AMM's pooled liquidity complements the bids and asks on the Vertex orderbook, serving as an additional market maker via smart contracts. The AMM liquidity is merged with liquidity from automated traders through the sequencer, providing users with a unified liquidity source. The sequencer ensures trades are filled with the best available liquidity, simultaneously utilizing limit orders and liquidity provider positions.

If the sequencer fails, the DEX defaults to a traditional xy=k model, ensuring the onchain AMM continues to function as the protocol's fallback, a mode referred to as "Slo-Mo Mode."

This liquidity model offers several clear advantages. Firstly, it guarantees more consistent liquidity since the DEX can always rely on the AMM when orderbook depth is insufficient. This makes it easier to bootstrap markets with passive AMM liquidity while still allowing for customization through limit orders on the orderbook.

Additionally, projects like Elixir facilitate easy liquidity deployment across orderbook exchanges. Users can select a pair to provide liquidity, and the protocol automatically deploys this liquidity through automated market making strategies. Currently, Elixir enhances orderbook liquidity on Vertex with 23 perp liquidity pools, adding $13.9M to Vertex’s orderbook on Arbitrum. Moreover, there are five additional pools providing spot liquidity, currently with $17.5M in TVL for Vertex.

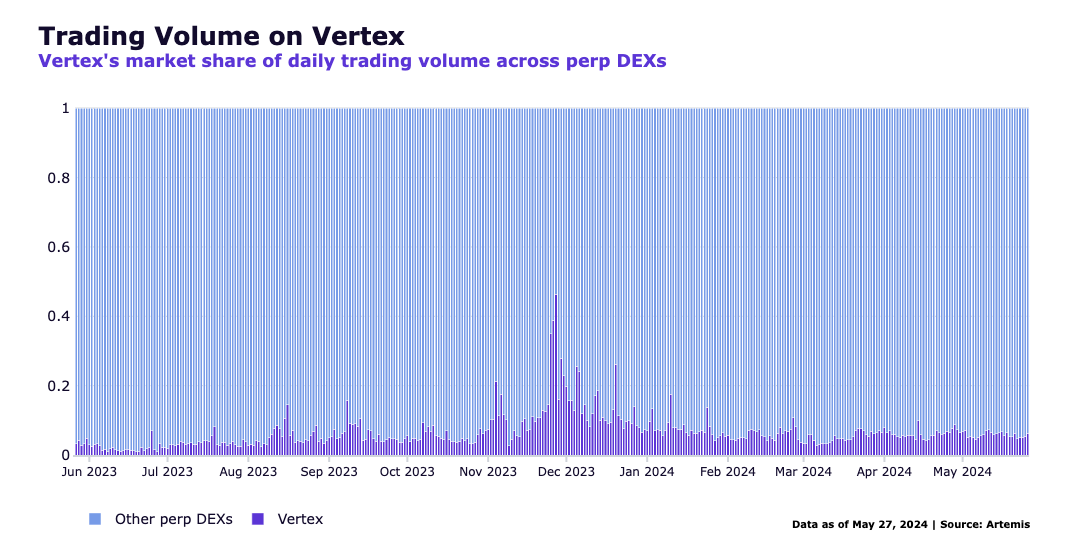

As of now, Vertex presents a total cumulative volume of $88.72B and a user base of 26,650, with $81.37B coming from perpetuals trading. Over the past month, the total average daily trading volume for both perp and spot markets has averaged around $280M, and the TVL in money markets stands at $96.79M. Vertex gained significant traction during its initial incentives and token launch, capturing considerable market share in the perps market. Shortly after it declined as expected through the exit of mercenary liquidity, but since then, it has maintained a steady market share of around 7%, as illustrated in the chart below.

The Sequencer Orderbook

The Vertex sequencer is a custom, parallel EVM implementation of an offchain orderbook and trading engine built in Rust. Currently, the sequencer operates as an independent offchain node, with plans to decentralize it via Vertex governance in the future. The orderbook is a key feature that sets Vertex apart as a high-performance perp DEX. Compared to the onchain latency of distributed node consensus, it achieves average order-matching execution speeds of 5-15 milliseconds and supports 15,000 transactions per second (TPS), making it competitive with centralized exchanges. It complements the Vertex AMM by providing a low-latency, central-limit orderbook (CLOB) for traders who want to place limit orders, engage in faster trading, and execute automated strategies. Pairwise LPs from the AMM contribute to the orderbook, enhancing its liquidity.

Several important properties are worth highlighting. The sequencer protects traders on Vertex from validator MEV on the underlying blockchain, as validators cannot order or front-run transactions. Additionally, due to the millisecond-level operation of Vertex’s sequencer, MEV extraction becomes less attractive. It is important to note that while the sequencer is offchain, it does not have custody over user assets—custody is managed by smart contracts on the underlying chain. Furthermore, the sequencer cannot censor transactions, halt trading, or block withdrawals. Although certain trust assumptions are necessary, specifically, that the sequencer operates impartially and does not favor any entities, the ability to avoid MEV concerns can be a significant advantage.

Cross-Margined Accounts

A key advantage of Vertex is the capital efficiency enabled by its cross-margined accounts. By default, Vertex consolidates a user's liabilities across their trading account to offset margins between positions, meaning a user’s entire portfolio serves as collateral for multiple open positions. While cross-margined collateral has become more common on perp DEXs, Vertex takes it further by allowing multiple types of positions, including lending and spot positions, to collectively serve as margin. Additionally, Vertex employs portfolio margining, which means that unrealized profits can be used as margin for existing or new positions, further enhancing trading flexibility and efficiency.

In practice, this means that accounts generally have lower margin requirements compared to having the same positions in separate, isolated margin accounts. Vertex also features an automatic risk management system that helps traders avoid liquidations. It automatically calculates and transfers margin between open positions to maintain the required margin levels, which is particularly useful in volatile market conditions and when executing complex trading strategies.

In addition to improving capital efficiency, cross-margined accounts on Vertex enhance practicality and reduce costs for common strategies like basis trading. With linked spot and perpetual markets, Vertex offers native markets for basis trading, which is typically more capital-intensive on other exchanges due to the need for separate markets for perpetual and spot positions. For example, if you are long spot ETH on Binance and short ETH, you must maintain the full margin for the perp contract since it doesn't account for the offsetting spot position. Vertex’s onchain risk engine recognizes this redundancy, significantly reducing the margin requirement for the ETH perpetual position, making arbitrage trading more capital-efficient. Additionally, Vertex’s integrated money market allows assets to serve as both collateral and available for borrowing to leverage spot positions. This closely aligns the basis rate with the borrowing rate of stablecoins.

These advantageous arbitrage conditions on Vertex have the potential to generate greater trading volumes and improved liquidity, as traders can execute profitable basis trade strategies with leverage and lower margin requirements.

Vertex’s Portfolio Overview provides easy access to overall portfolio health and risk indicators, streamlining management for multiple open positions. All positions are linked and managed together, offering a comprehensive view of a trader’s risk. An account’s health is determined by assigning weighted values to each balance and position. Vertex simplifies risk management by distinguishing between Initial Health and Maintenance Health. When Initial Health is depleted, the account enters Maintenance Mode, preventing new risk-taking actions like opening new positions. The remaining Maintenance Health acts as a buffer, allowing users to de-risk before facing liquidation. If Maintenance Health is fully depleted, the account becomes susceptible to liquidation.

In determining an account’s health, certain special cases can offer significant benefits to traders. As always, the devil is in the details. Spreads, which involve offsetting positions on the same underlying asset, are inherently less risky than individual spot and perpetual positions. Recognizing this, Vertex assigns health benefits to these spread positions, enabling a much larger capital efficiency.

Key Details

Liquidations

Spot oracle prices are utilized for liquidations, ensuring robust pricing and shielding users from temporary liquidity shortages that might affect spot prices. Additionally, an independent oracle price is in place for USDC, enabling accurate health calculations and trading even during USDC de-pegging events. Vertex Protocol adopts a multi-oracle approach, gathering prices from various providers. Presently, most Vertex markets rely on Stork, but the recent deployment of Chainlink Data Streams on Vertex initially supports ETH markets, with plans to expand to other markets.

Any user can buy assets from the liquidating account at a discount or settle its debts at a premium until the account's Initial Health surpasses zero. If an account's Initial Health exceeds zero at any point during the liquidation process, the liquidation halts.

Vertex Protocol earns 25% of the profits generated by liquidators, with these fees going to the insurance fund to safeguard protocol health. In the event of insolvency, the account's positions are exited at a loss, resulting in bad debt. Vertex's last lines of defense are then activated: USDC from the insurance fund is allocated to the insolvent account to compensate liquidators for undertaking the underwater positions. If the insurance fund is depleted, losses from underwater positions are distributed among other perpetual accounts in the market. If this isn't feasible, losses are spread across all USDC holders. Currently, the Insurance Fund holds 1.26M USDC on Arbitrum and 0.12M USDC on Blast, totaling approximately 1.4M USDC to offset bad debt.

Fees

Vertex offers a competitive trading fee model, featuring low fees for takers and zero fees for makers across spot and perpetuals. The current taker fee structure entails a 2 bps fee for takers, applied only after a certain minimum order size. This effectively yields a total fee rate potentially smaller than 0.02%.

Supplementing this model is the Vertex Maker Program, which incentivizes price makers with a rebate-based trading fee program and VRTX token incentives based on a scoring function prioritizing market support, uptime, and fees. All trading fees are paid in USDC, initially allocated to secure the protocol, fund ongoing expenses, seed VRTX liquidity, and drive value to the VRTX token via tokenomics mechanics. Additionally, Vertex charges a flat fee in USDC for interactions with the Sequencer to cover gas costs, with fees subject to change over time but expected to remain relatively stable within months of launch (e.g. 1 USDC for submitting a liquidation or minting/burnin LP tokens).

The cross-chain fee accounting model maintains the same fee structure while distinguishing between fee payouts for cross-chain versus single-chain scenarios. In a cross-chain order match between two instances, the taker fee is charged on the taker chain, and the maker rebate is charged on the maker chain. In the Edge ecosystem, takers generally incur a 2bps fee and makers receive a 0.5bps rebate. So, in a cross-chain match between a taker on Blitz and a maker on Vertex, the taker fee on Blitz is 1bps, the maker rebate on Vertex is 0.5bps, and the fee accrual for Vertex is 0.5bps. This structure ensures that revenue accrues to the maker chain, keeping makers incentivized through token rewards and rebates. If the taker and maker are on the same chain, the taker fee is 1.5bps, with a 0.5bps fee accruing to the same chain.

UX

Vertex's 1-click trading (1CT) feature replicates the ease of trading on centralized exchanges, allowing users to opt-in while retaining manual signing as the default mode. 1CT simplifies trading by generating a secure private key for automated transaction signing, requiring two signatures upon activation. Users must confirm ownership at the start of each session, and 1CT enables trigger orders for uninterrupted trading. Vertex supports stop market, take profit, and stop loss orders (excluding stop limit), with trigger prices based on Mark Price or Last Price for the entire position size. Partial position orders and advanced trading strategies like TWAPs or scale orders are currently unavailable.

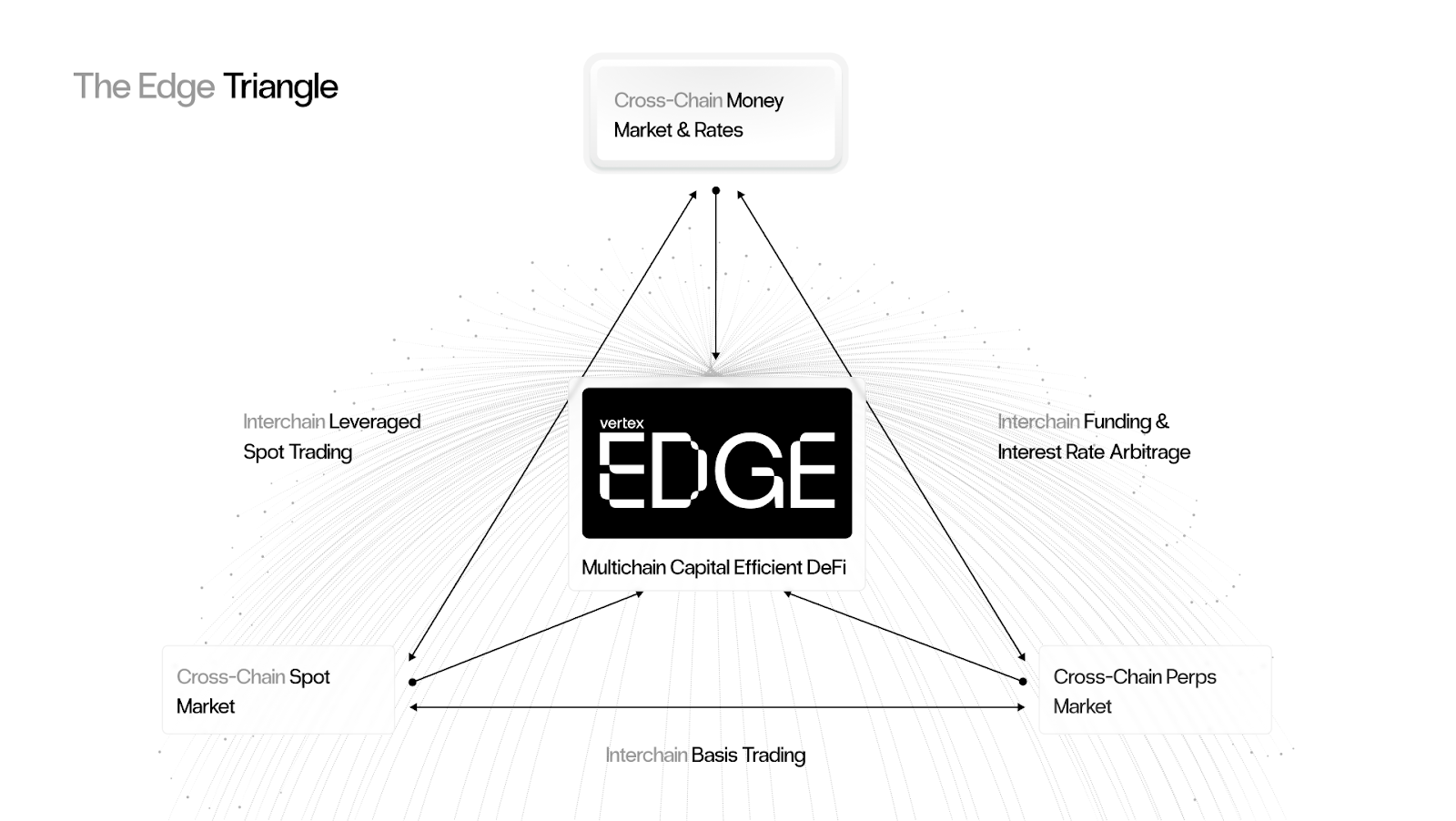

Vertex Edge - Cross-chain Liquidity

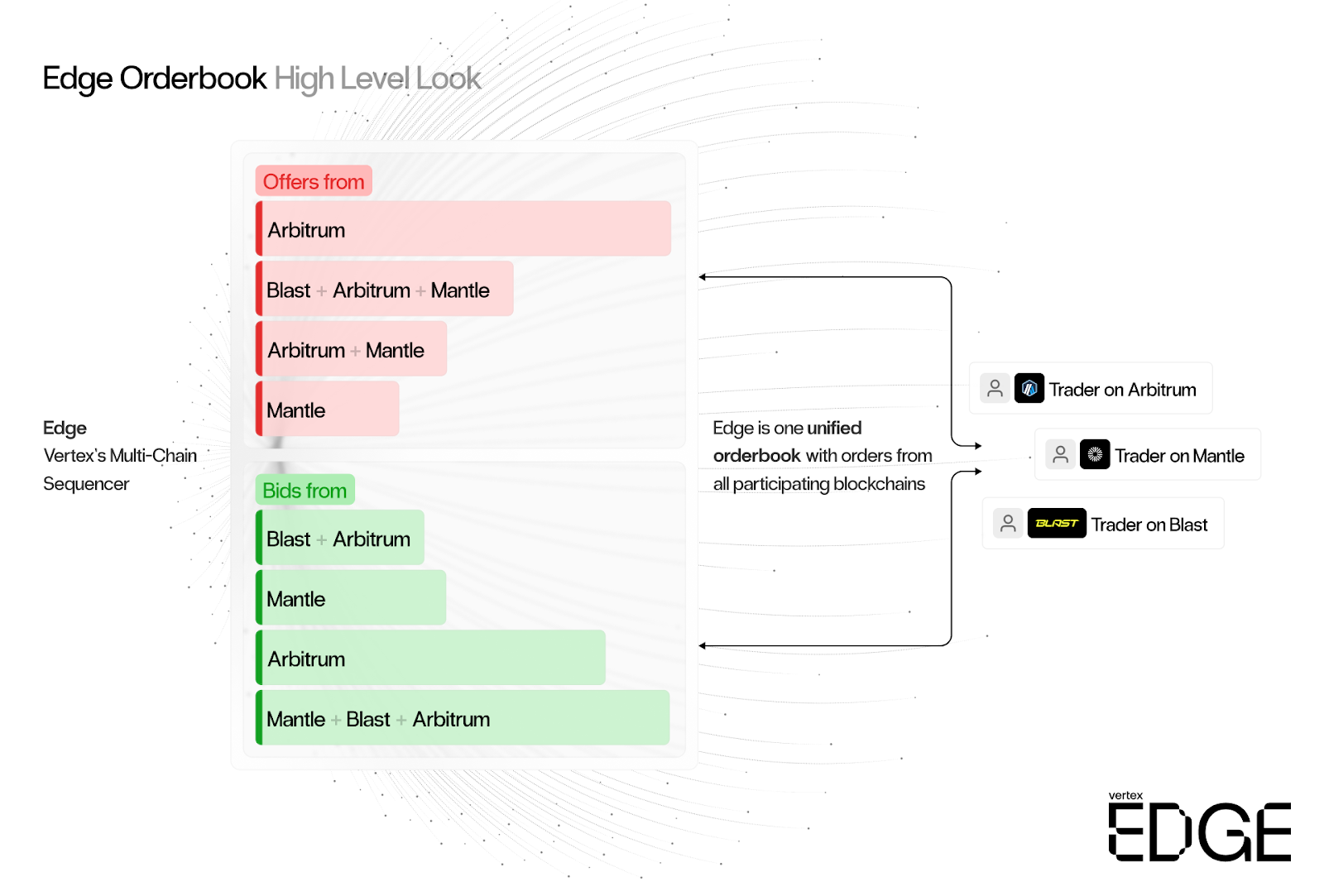

Vertex Edge introduces cross-chain liquidity through a synchronous orderbook, consolidating liquidity from various instances and settling transactions onchain at the source base layer. This extension of the sequencer's capabilities broadens its reach across supported base layer ecosystems, with the sequencer's state sharded and updated across all chains. Inbound orders from each chain are aggregated and matched against the total liquidity pool, with the sequencer (Edge) automatically hedging and rebalancing liquidity between chains. Essentially, Edge operates as a virtual market maker, focusing on resting liquidity (maker orders) across sharded states of Edge instances, while taker orders are submitted directly to Edge's unified liquidity layer from independent instances.

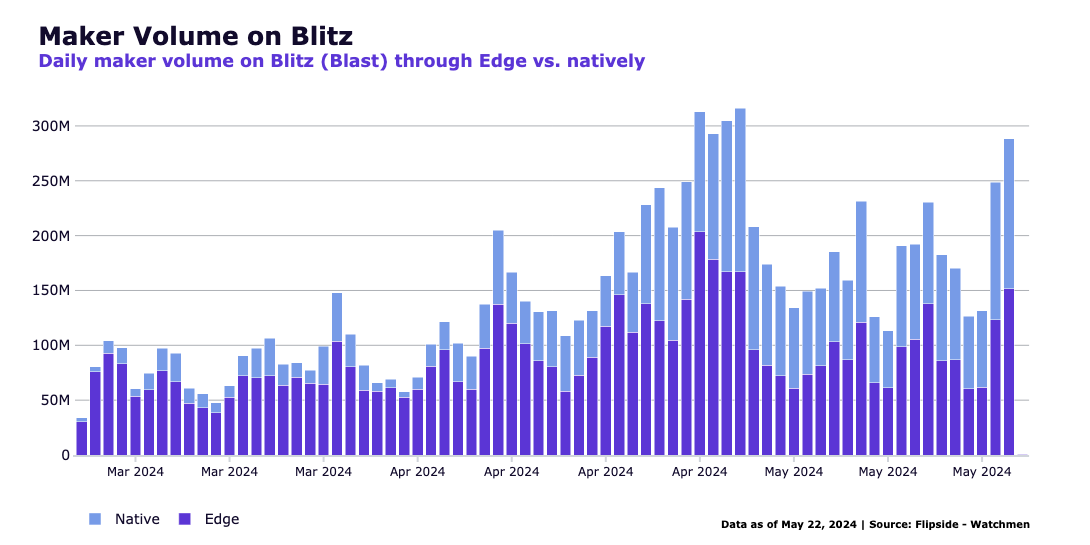

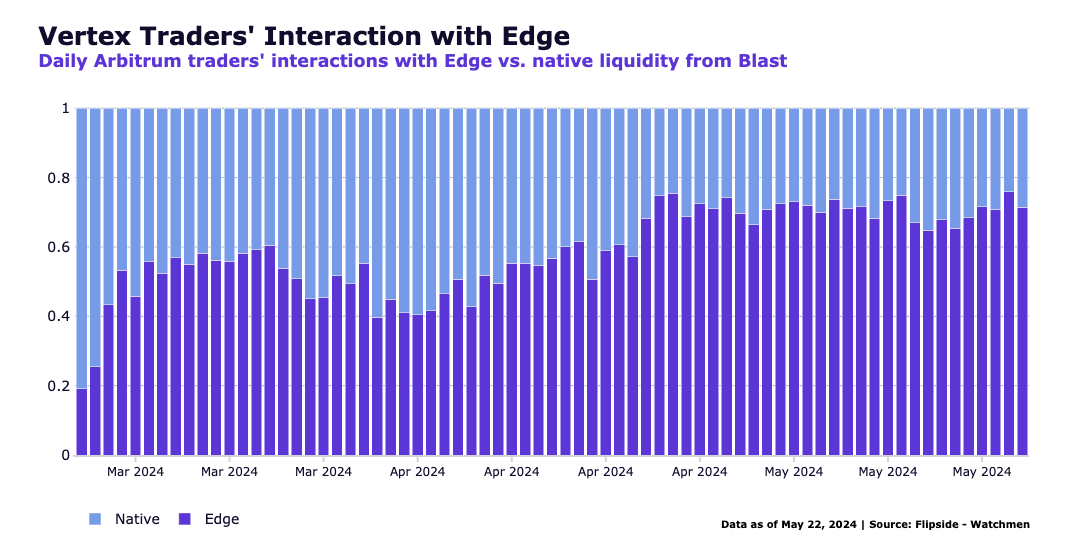

This innovation opens up possibilities for accessing unified liquidity on any chain. It's particularly beneficial for launching new perp DEXes on different early-stage chains, eliminating the need to attract liquidity initially, crucial for competitive price execution. Blitz on Blast, the inaugural instance by Vertex Edge, illustrates this transition: initially, volume predominantly stemmed from Edge, and is gradually drawing liquidity from the chain (Blast) over time. Since March 13th, shortly after Blitz’s launch on Blast, until May 22nd this year, Edge has contributed to 62% of Blitz’s maker volume. For total maker and taker volume, Edge’s contribution is 27%. As illustrated in the chart below, the trend indicates an increase in direct volume from Blast.

With each new Edge instance, benefits extend to both the new and existing instances. Increased liquidity in one instance translates to more liquidity available across all existing ones. Liquidity from non-Arbitrum instances, like Blitz, merges into a synchronous orderbook, combining liquidity from Vertex on Arbitrum and Blitz on Blast. Deploying on more chains adds liquidity rather than fragmentation, enhancing usage across all chains and providing value to apps on other chains. The chart below illustrates how Vertex, despite having more established liquidity, is progressively benefiting from Edge’s cross-chain liquidity.

It's crucial to highlight that matched orders are settled locally onchain to the user's origin chain, ensuring a net-positive impact on the local chain's blockspace demand. Each Edge instance showcases the combined orderbook liquidity of all interconnected chains on the app's trading interface, allowing access to this shared liquidity from any base layer.

Up next is Mantle, slated to receive its own Edge instance. With a TVL of $331.57M, approximately 11% of Arbitrum's TVL, Mantle stands to benefit significantly from access to deeper liquidity than currently available onchain. This expansion allows Mantle to accommodate a much broader user base.

Recently, the team unveiled plans to launch an Edge instance on Botanix, the Spiderchain EVM L2 on Bitcoin. The Edge deployment on Botanix introduces novel concepts for decentralizing the sequencer, with further details to be disclosed as development progresses. This move expands liquidity availability from Arbitrum and Blast to the Bitcoin L2 ecosystem, potentially bridging these two very separated worlds and catering to diverse user types.

Amplifying User Benefits

Vertex Edge's architecture facilitates multi-chain liquidity sharing through a unified, synchronous orderbook. However, thanks to Vertex's vertically integrated offerings (spot, perpetuals, and money markets) and cross-margined account structure, this entails more than just additional perp DEXs accessing consolidated liquidity. Instead, Vertex's design offers amplified benefits to all users across each instance and underlying network.

Through Vertex's spot market, users will be able to trade native spot assets across chains without needing to access the network of any specific asset. This is a significant step in the roadmap that will be key to reduce friction between networks and bridging risks. With the synchronized orderbook aggregating liquidity, sellers on one chain gain access to buyers on multiple chains, optimizing market depth and potentially reducing slippage.

Additionally, Vertex's cross-margined accounts with spot and perpetual products enhance basis trading opportunities across ecosystems, further optimizing market efficiency through Edge. Unified funding rates on Edge streamline trading, mitigating liquidity fragmentation.

Edge's money markets enable users to maintain collateral on their preferred chain without asset bridging, again reducing friction and expanding collateral options to enhance liquidity and trading efficiency. The synchronous orderbook layer retains Vertex's embedded money markets through cross-margin accounts, ensuring consistent interest rates across chains. This consistency facilitates easier cross-chain spot trading, enabling traders to access assets in different ecosystems without the need for stablecoin bridging, optimizing yields for passive lenders.

App Layer Alignment

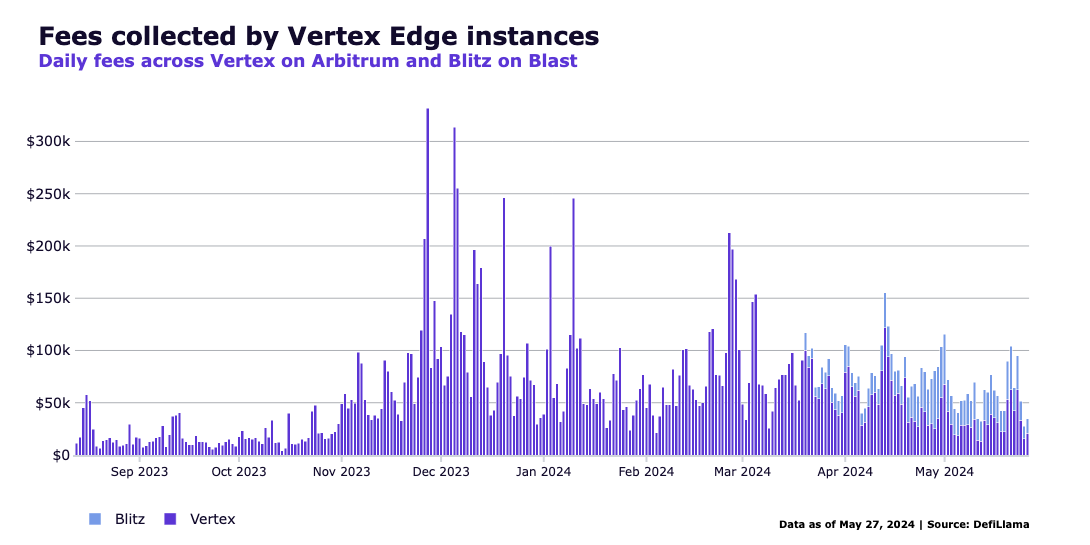

Vertex Edge offers three distinct benefits to base layer networks: increased blockspace demand, better onchain liquidity, and reduced development/integration costs. Vertex Edge's batched settlement model increases blockspace demand, as evidenced by Vertex contracts consistently ranking among the top gas spenders on Arbitrum in 2024. This alignment encourages more blockchains to integrate Vertex Edge, possibly offering native incentives such as the Arbitrum STIP.

Edge's cross-chain liquidity access alleviates obstacles for users moving assets between chains, and retaining onchain capital by diminishing outflows seeking better DEX liquidity. Each new chain added to Vertex Edge's network enhances liquidity for all chains, creating a virtuous cycle of growth and liquidity. Additionally, Vertex Edge reduces development costs and resources for launching DEXs on L2s by leveraging existing liquidity, avoiding the need for extensive new technology development and deep liquidity creation.

Implications For The Token

VRTX functions as a utility token within the Vertex ecosystem, providing several benefits to users. It primarily serves as an incentive for the Vertex community, rewarding user activity, efforts, and transaction volume within the Vertex Protocol. These rewards vary based on contributions and commitments, encouraging ongoing participation over the long-term.

Staking VRTX is necessary to join the protocol's incentive program, signaling a user's commitment and adherence to standards. Staked VRTX generates voVRTX, a non-transferable token that acts as a multiplier for incentives, proportional to the staking duration. Users who stake longer (up to 183 days) can earn 1 to 2.5 times more rewards. Besides staking, voVRTX can also be earned through active and consistent participation, making it a comprehensive incentive model. This system encourages continuous contributions, creating a positive feedback loop.

Vertex's primary revenue comes from trading fees, which scale with trading volume. Up to 50% of trading fee revenue, excluding sequencer fees, is allocated to the Protocol Treasury for rewards, with the specific percentage determined each epoch based on the protocol's needs.

Just recently on May 16th, the team announced a VRTX Buyback & Burn program to replace the previous Buyback & Stake, meaning that VRTX purchased with protocol revenue will be periodically sent to a burn address instead of staked moving forward. It is designed to use a portion of retained protocol revenue from the Vertex protocol (e.g., trading fees) to purchase VRTX on a forward-looking basis.

The expansion to other chains through Edge instances is set to generate more trading fee revenue, leading to progressively more VRTX being burnt. With a fixed total supply of 1 billion tokens, and 90.85% of it to be distributed over the five years following the TGE, this supply reduction could drive significant value back to the token. Notably, 34% of the supply is allocated to ongoing incentives to be distributed over the next 6+ years, starting from Epoch 8. As more tokens are burnt due to rising revenue and fewer incentives are given out over time (as per the emission schedule), this could create buying pressure. The portion of revenue allocated to Buyback & Burn will vary based on the protocol's needs.

Risks

Cross-margined accounts offer significant capital efficiency and advantages for strategies like basis trading. However, they also present higher solvency risks compared to isolated margin systems. An example of this vulnerability is the Mango Markets hack in October 2022. Although oracle design and security measures have improved since then, it is important to acknowledge that more complex margin systems can inherently provide more opportunities for exploitation.

The Insurance Fund’s capability to cover bad debt in extreme scenarios must also be monitored. As new Edge instances are launched, it takes time for protocol revenue from liquidations to sufficiently bolster individual insurance funds. However, funds can be utilized where necessary in emergencies and losses can be socialized, resulting naturally in a poor user experience but avoiding protocol insolvency.

The offchain sequencer is a single point of failure, with its consequences increasing with the addition of more instances. This risk is mitigated by the Slo-Mo fallback, which allows trading against AMM liquidity. However, execution in this mode is not as efficient, potentially leading to losses and high opportunity costs, which may not be ideal at times for sophisticated and professional traders.

The perpetuals landscape is highly competitive and liquidity is known to be mercenary, with the current craze for points programs and typical inflationary token rewards making user retention challenging. Nonetheless, Vertex’s market share has remained relatively stable since its token launch, and its ability to expand into multiple protocols with additive liquidity is promising for its future.

Final Thoughts

Vertex Edge’s cross-chain liquidity addresses the growing need to aggregate liquidity in an increasingly fragmented blockchain landscape. As more blockchains (L1s, L2s, L3s) are created, trying to convince users to use one protocol on one network can become futile. Edge embraces the multi-chain future, finding a solution to unify liquidity across chains. By ensuring that deployment on more chains means increased liquidity for every chain, Edge offers a future-proof approach. Edge transforms the typical subtractive creation of new protocols on new chains, which fragments liquidity, into a synergistic, value-additive endeavor. This perspective is groundbreaking for a multi-chain future, allowing users to trade on their preferred chains without missing out on the best price execution and overall trading experience. For anyone who believes in the multi-chain future, Vertex is a standout project in the perps landscape.

App layer alignment with the underlying network means that more blockchains can welcome Vertex Edge into their ecosystems, potentially offering native incentives. This boosts adoption, especially if Edge launches on established networks to leverage local liquidity and users. While competition is stronger on these chains, the value add could be significant.

Low trading costs and increasing liquidity can sustainably attract more volume and drive value to the token. With the initial token phase incentives involving a 7-month lock period concluding soon, and with monthly emissions on a fixed schedule, combined with growing protocol revenue leading to more tokens being bought and burnt, the token could have a clearer path for value accrual.

Finally, improvements to the perp DEX trading UX, including reduced latency and fees, along with deep cross-chain liquidity that Edge offers, are paving the way for perp DEXs to gain market share from CEXs, growing the total market and changing market dynamics.

This research report has been funded by Unlimited Technologies PTE. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Unlimited Technologies PTE. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek the advice of a qualified financial advisor before making any investment decisions.