Canton Network: Wall Street's Blockchain

Key Takeaways

- Architecture is purpose-built for regulated institutions. Canton enables granular transaction privacy and validator-level control while maintaining interoperability across applications, addressing key compliance barriers for institutions.

- Adoption spans the full institutional financial stack. DTCC is bringing regulated collateral onchain, Broadridge processes more than $7T per month in repo activity, and Nasdaq is integrating Canton with its Calypso risk and collateral management platform.

- Network effects could increase coordination activity. As more institutions onboard and transact with one another, the number of counterparties grows and more transactions route through the Global Synchronizer, driving higher CC burns.

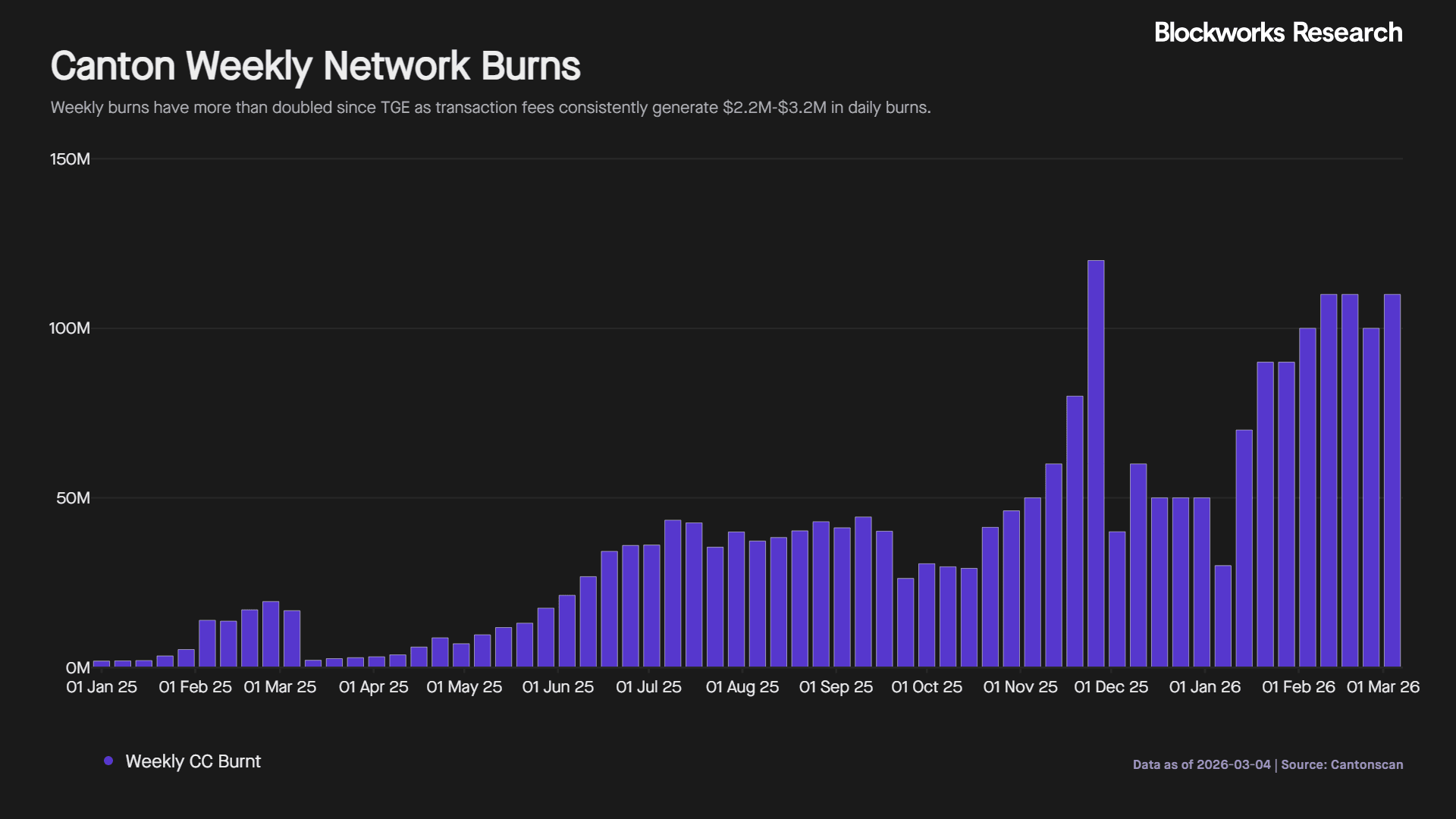

- Token economics are increasingly usage driven. Weekly burn has increased 216% since TGE, and the burn-to-mint ratio has risen to 0.90, bringing the network closer to potential deflation if activity continues to scale.

- Valuation remains discounted relative to peers. Canton generated the highest REV among major L1 networks in February yet trades at lower multiples, likely reflecting near-term inflation and the market viewing it more as financial infrastructure than a general purpose chain.

- Regulatory clarity and institutional rollouts are key catalysts. Passage of the Clarity Act and the rollout of DTCC’s broader tokenization platform in 2H 2026 could accelerate institutional adoption and increase the volume of assets and transactions moving through Canton.

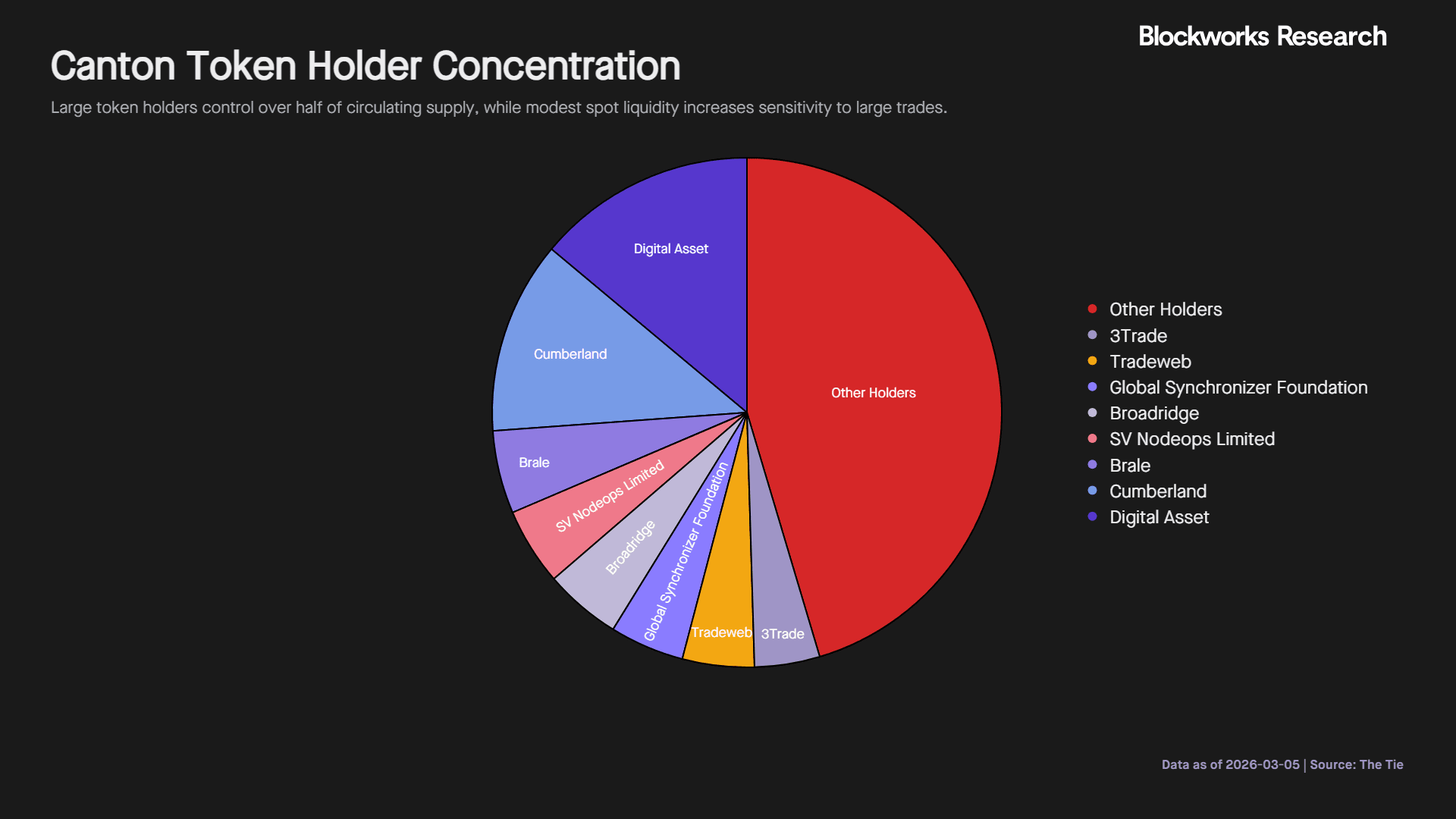

- Token concentration remains a potential risk. Roughly 54% of circulating CC is held by a small number of network participants, although many of these balances are operational rewards rather than speculative holdings.

Introduction

Several of the most important narratives in crypto are beginning to converge. These include RWA tokenization, institutional blockchain adoption, privacy infrastructure, and stablecoins as settlement rails. Canton Network sits at the intersection of these trends and has assembled one of the strongest groups of institutional participants in the industry.

Major financial institutions, including DTCC, Nasdaq, Broadridge, and several global banks, are already deploying real workflows on the network across treasury tokenization, repo financing, collateral management, and payments.

If this trend continues, Canton could become a coordination layer for tokenized financial markets where assets, cash, and collateral move between institutions in real time. As more financial activity flows through the network, transaction coordination increases, driving network revenue and token burns higher and pushing the network toward deflation.

Pain Points in Institutional Tokenization

Tokenization promises faster settlement, lower reconciliation costs, and more efficient capital usage. In practice, most blockchain designs force institutions to choose between regulatory compliance and the ability to transact across a shared network.

The Basel Committee on Banking Supervision has made clear that infrastructure choices directly affect regulatory treatment. Banks that tokenize traditional assets must demonstrate strong governance, clear validator controls, robust data privacy, and sound operational risk management. If these conditions are not met, tokenized exposures can face materially higher capital charges, eroding much of the economic benefit tokenization is intended to deliver.

Public permissionless blockchains provide interoperability and composability, but transaction data is visible to validators and often the broader market. For regulated institutions, broadcasting information about liquidity needs, margin movements, or collateral positions is not acceptable. Even pseudonymous activity can reveal commercially sensitive insights. Institutions require certainty over who validates their transactions and who can access their data.

Private blockchains restrict access but introduce fragmentation. Each network becomes a silo that limits asset mobility and cross platform liquidity. Privacy is often implemented at a broad channel level, where participants may still see more activity than a strict need to know model would allow.

Institutions therefore face a structural trade off. Public networks lack sufficient control, while private networks lack meaningful interoperability. Canton is designed to bridge this gap by combining granular privacy and validator level control with shared synchronization and atomic settlement across independent applications.

Network Architecture and Privacy Model

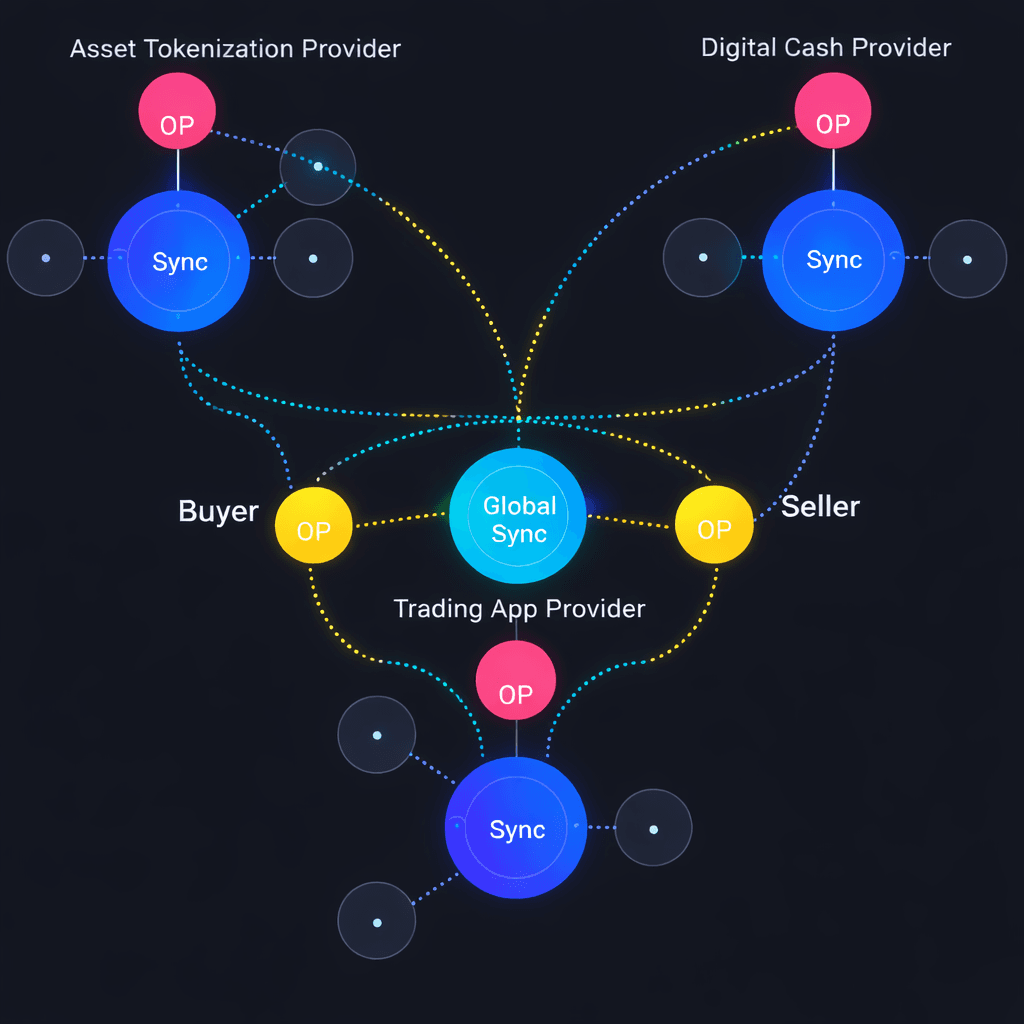

Canton separates execution from coordination. Smart contracts written in Daml run on validator nodes operated by participating institutions and application providers. Each organization runs its own validator, which acts as its gateway to the network and validates only the transactions it participates in. This design allows institutions to maintain control over their infrastructure and transaction validation.

Validators connect to a synchronizer that routes and orders messages between parties. The synchronizer ensures that multiparty transactions settle atomically and consistently across participants. It does not validate transactions and cannot view transaction data because all messages are end-to-end encrypted. The synchronizer simply orders encrypted payloads, similar to a post office handling sealed envelopes.

Canton supports multiple synchronizers. The Global Synchronizer acts as the shared public coordination layer operated by Super Validators using Byzantine Fault Tolerant consensus. It provides a neutral backbone that allows independent applications and institutions to interoperate while preserving flexibility in how ecosystems connect.

Network Participants

Validators are infrastructure nodes operated by institutions. They store contract state, validate the transactions they participate in, and provide application interfaces for users and services.

Applications contain the business logic deployed on validators. They define contract rules and data permissions for use cases such as stablecoins, repo, custody, and tokenized assets.

Super Validators operate the Global Synchronizer and secure decentralized message ordering for the public network. Validators validate only the transactions they participate in, while Super Validators secure the shared coordination layer.

Governance is transparent through the Canton Foundation and follows institutional standards. Anyone can see or make Canton Improvement Proposals (CIPs). Super Validators that operate the Global Synchronizer vote on key decisions, including upgrades and changes to code and services. The Canton Foundation supports the development and oversight of the Global Synchronizer, ensuring governance actions are publicly visible and member involvement. It runs a node on behalf of its members and participates in governance votes, helping maintain neutrality and trust in the network.

Institutional Adoption Thus Far

DTCC Integrates DTC Custodied Treasuries with Canton

DTCC is the core post trade infrastructure provider for US capital markets. Through its central securities depository subsidiary, The Depository Trust Company, it safeguards more than $100T in assets under custody across equities, ETFs, money market instruments, and other securities. Its decision to tokenize DTC custodied Treasuries on Canton represents a structural step toward bringing core market collateral onchain.

After receiving an SEC No Action Letter, DTCC announced plans to mint a subset of DTC custodied Treasuries onto Canton with an MVP targeted for 1H26. These are not synthetic assets. The tokenized Treasury retains the same CUSIP, meaning it remains legally and operationally the same security within existing market infrastructure. Participants can use the asset in traditional systems or in tokenized form without changing its legal status.

DTCC has also joined Canton as a Super Validator, operating infrastructure for the Global Synchronizer and participating in network governance.

More important than issuance is demonstrated usage. A Canton working group that includes Bank of America, Circle, Citadel, Cumberland, Société Générale, Tradeweb, and Virtu has already completed live onchain US Treasury financing against stablecoins. These transactions included weekend repo, atomic settlement, and real time collateral reuse.

DTCC’s initiative brings regulated collateral onchain, while these transactions demonstrate that the assets can be actively financed and mobilized at an institutional scale.

Broadridge: Institutional Repo at Production Scale

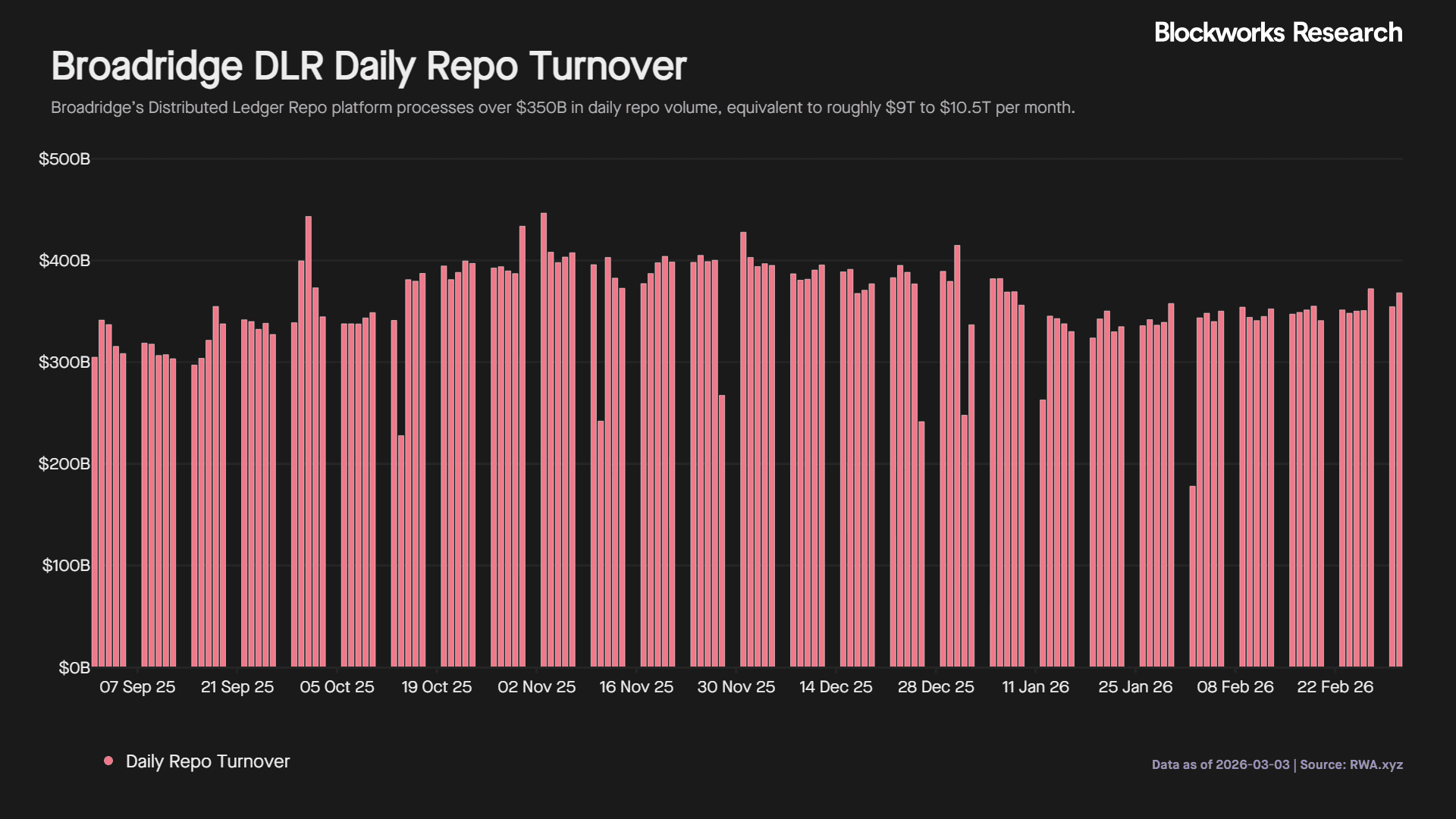

Broadridge’s Distributed Ledger Repo (DLR) platform currently processes more than $350B in average daily volume. Repo is short term secured funding typically backed by US Treasuries and serves as the core liquidity engine of global capital markets. This activity is already running in production on Canton.

DLR has been operating since 2021, and its user base includes major banks, broker dealers, and traditional asset managers. The platform is integrated with existing market infrastructure, including custodians, front office trading systems, and back office settlement platforms, allowing institutions to onboard with minimal operational disruption.

Within DLR, the key components of the repo lifecycle are handled onchain. This includes custody of tokenized collateral, execution of the repo transaction, and settlement of cash and securities between counterparties. Certain operational processes remain offchain, such as archival record keeping and updates to the control of underlying collateral held in traditional custody accounts.

DTCC’s plan to tokenize DTC custodied Treasuries introduces regulated, high quality collateral directly onto Canton. As more assets such as stablecoins, tokenized deposits, and digital bonds move onto the network, the repo financing associated with those assets can also occur onchain, which would increase repo activity on Broadridge's DLR platform.

Nasdaq: Onchain Margin and Collateral Infrastructure

Nasdaq has completed a pilot connecting the Canton Network to its Calypso platform, one of the most widely used institutional systems for managing risk, margin, and collateral. Calypso is embedded across major banks and asset managers globally. The pilot demonstrated how onchain infrastructure can integrate directly with existing institutional risk systems.

The test was conducted with QCP, Primrose Capital, and Digital Asset. Firms can automatically calculate margin requirements and move collateral between counterparties onchain at any time of day while continuing to use their existing portfolio and risk systems. For institutions operating across time zones and asset classes, this reduces operational friction and improves capital efficiency.

Nasdaq has also joined Canton as a Super Validator. This builds on Nasdaq’s strategic investment in Digital Asset, the creator of Canton, alongside institutions including BNY, iCapital, and S&P Global.

Other Key Institutional Partnerships

Several other global institutions are also building on Canton. JPMorgan plans to bring JPM Coin natively onto the network to enable 24-hour institutional cash and collateral settlement. London Stock Exchange Group is launching its Digital Settlement House on Canton to support real time post trade workflows. Lloyds Banking Group executed the UK’s first production tokenized gilt and deposit transaction on the network.

These initiatives are supported by a growing set of Super Validators operated by institutions including Digital Asset, Tradeweb, Cumberland, and others.

Institutional Impact

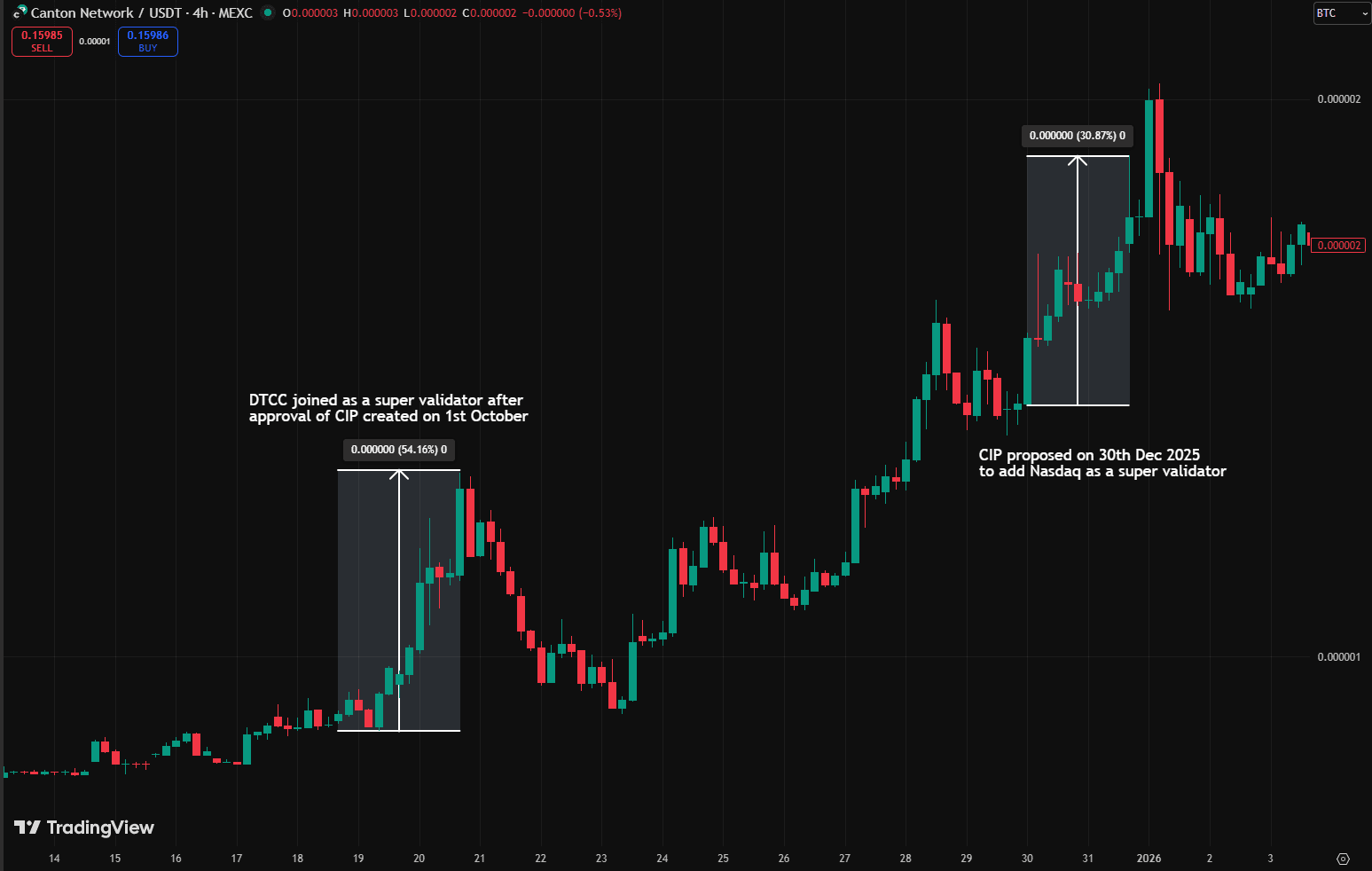

Super Validator announcements from major financial institutions have acted as short term price catalysts. Following confirmation of DTCC and Nasdaq as Super Validators, CC outperformed BTC by 54% and 31%, respectively, over the following two days. The move likely reflects increased market confidence that globally recognized financial institutions are committing to the network at the infrastructure and governance layer rather than only experimenting at the application level.

Beyond narrative driven price movements, these developments could translate into sustained network activity over time.

Nasdaq’s work focuses on collateral management. Margin recalculations, collateral pledging, and portfolio adjustments are high frequency activities. If these workflows move onchain across independent institutions, they generate recurring coordinated transactions.

DTCC and Broadridge represent the asset and funding layer. DTCC is bringing regulated collateral onchain, while Broadridge already facilitates large scale repo financing activity. Tokenizing an asset is a one time action. The real impact comes when those Treasuries are repeatedly financed, pledged, and reused across counterparties.

Today, much of the activity from large institutions operates within private synchronization environments rather than through the Global Synchronizer. As a result, that activity does not yet materially contribute to Global Synchronizer message flow.

However, as more independent institutions onboard and begin transacting with one another, coordination requirements increase. Each new participant expands the number of possible counterparties, strengthening network effects across the system. Transactions that span multiple validators are routed through the Global Synchronizer. As cross institutional financing and collateral activity scale, message volume increases, translating into higher CC burned.

Tokenomics

Transactions that span multiple validators are sequenced through the Global Synchronizer, where fees are paid by burning CC. Fees are denominated in USD per MB of transaction data but settled in CC using the onchain conversion rate. These fees are burned rather than paid to validators, directly reducing token supply. This structure allows institutions to pay predictable dollar based infrastructure costs while linking network usage to token supply dynamics.

Since TGE, weekly CC burned has increased 216%, rising from 46.2M to roughly 100M. In dollar terms, daily fees have ranged between $2.2M and $3.2M in recent weeks. As a share of circulating supply, weekly burns have increased from 0.14% to 0.26%, with several weeks exceeding 0.30%.

Burn activity predates TGE because the Global Synchronizer and Canton Coin went live in July 2024, though the token only became transferable on Oct. 31, 2025. Notably, CC follows a pure earn model. There were no pre-allocations to investors, the team, or the foundation. All tokens are minted through network participation.

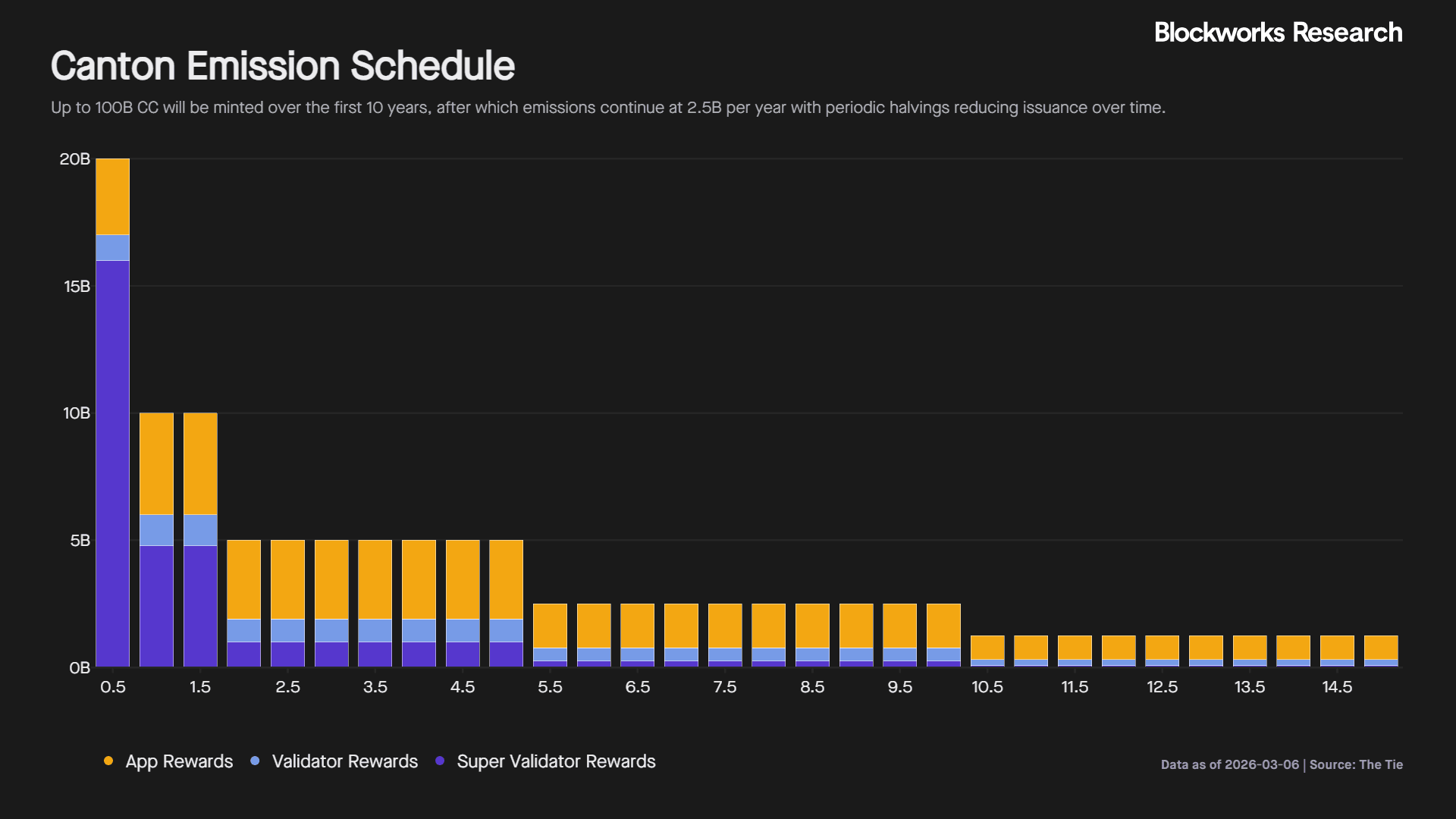

Emissions follow a fixed minting curve. A total of 100B CC can be minted over the first 10 years, after which 2.5B tokens are emitted annually. Periodic halvings reduce issuance over time, with the most recent on Jan. 12, 2026, cutting annual emissions from 20B to 10B.

Newly minted tokens are distributed across three groups that include applications, Validators, and Super Validators. Within each group, rewards are distributed based on recorded activity such as fees burned, traffic generated, or governance assigned weight, subject to minting caps.

Importantly, allocation shifts over time. Super Validator emissions have declined from 80% at launch to 20% today, while application rewards have increased from 15% to 62%. The system is intentionally moving from early infrastructure incentives toward application-driven incentives.

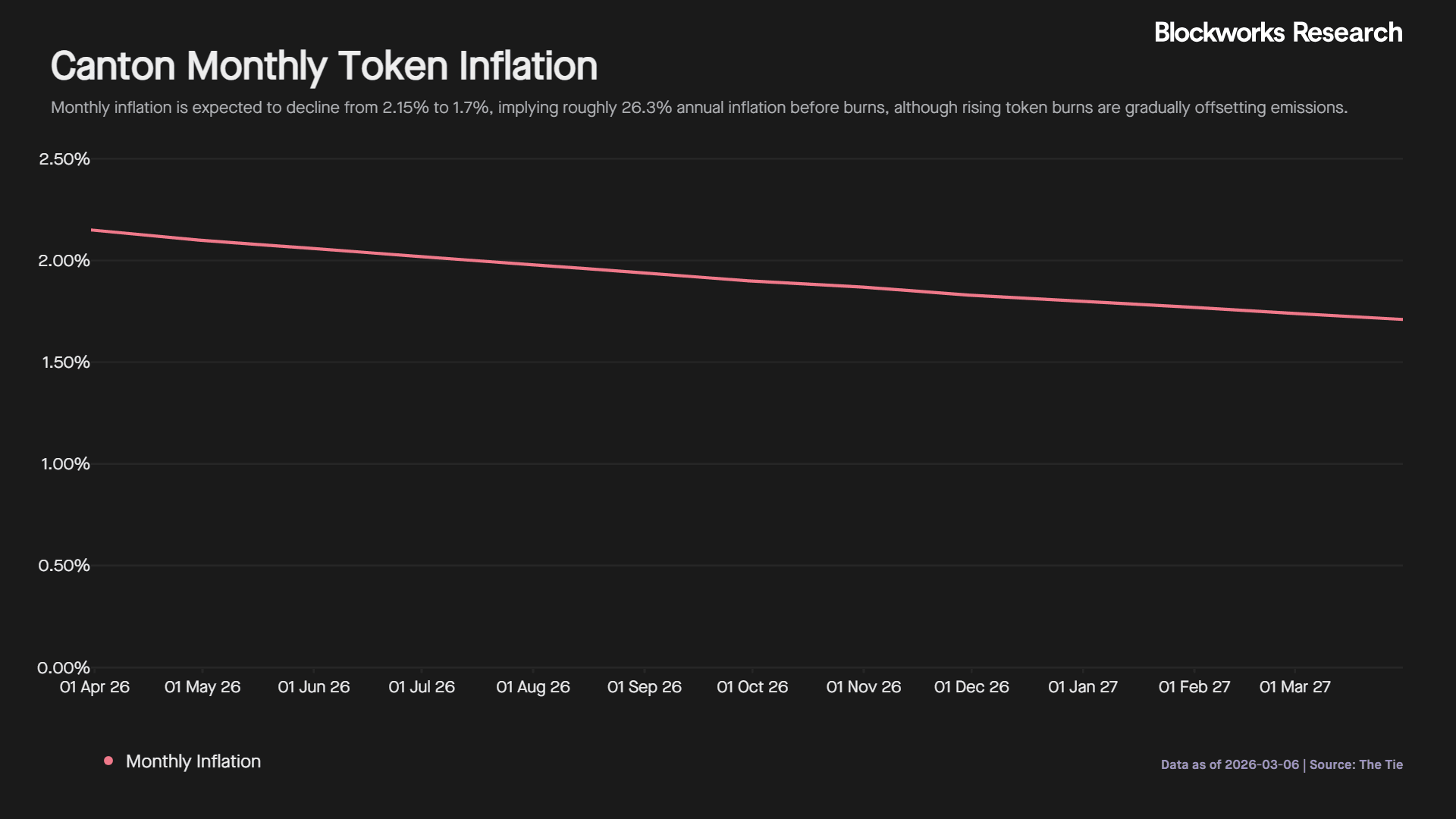

Looking ahead, monthly inflation declines gradually from 2.15% to 1.7%, implying approximately 26.3% annual inflation before accounting for burns. While this remains elevated relative to other L1s, the burn rate is rapidly closing the gap.

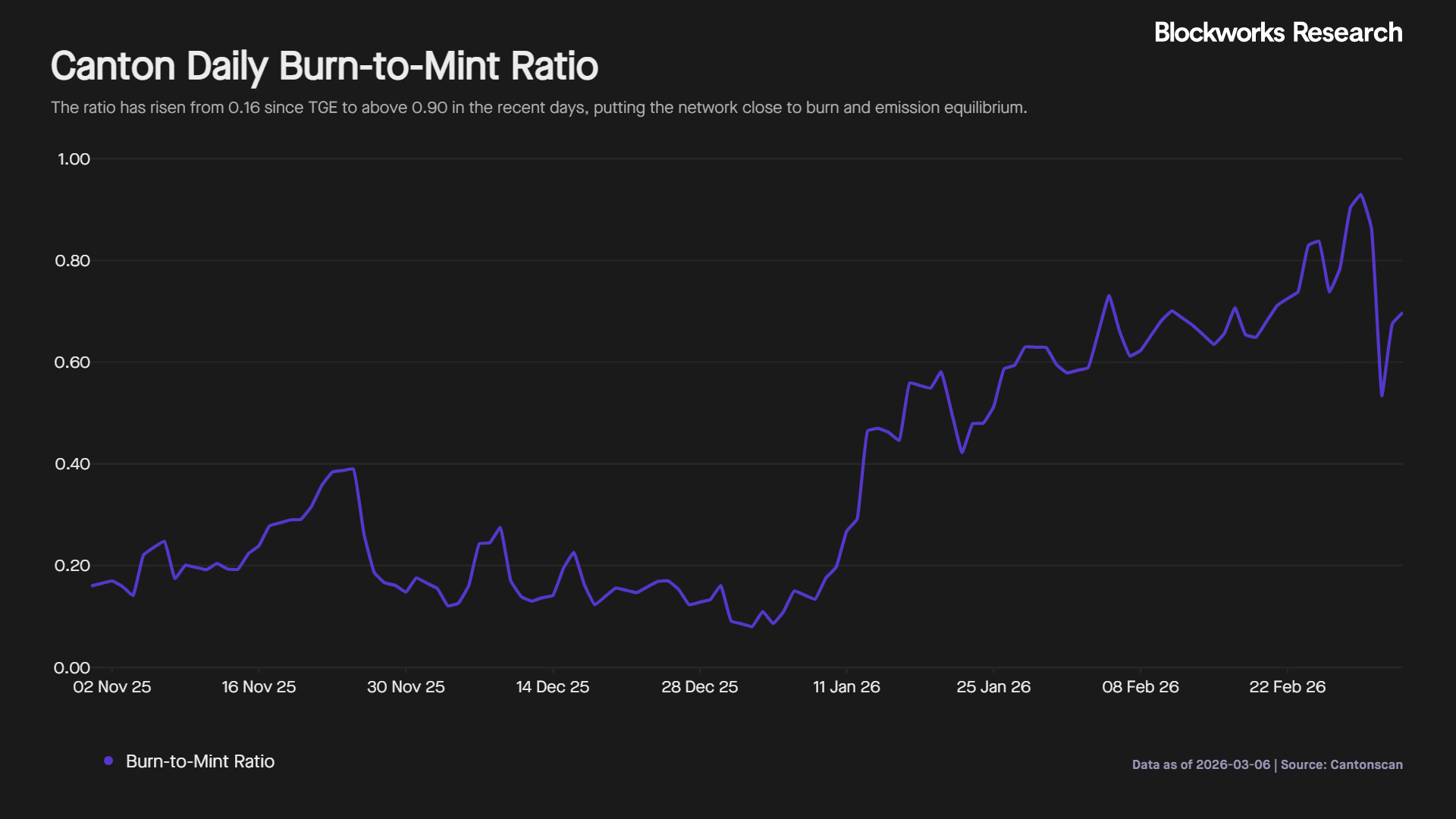

Since TGE, the daily burn-to-mint ratio has increased from 0.16 to 0.90, with most of the acceleration occurring in 2026. At the current pace, Canton is approaching equilibrium where daily burns match daily emissions.

Sustained burn ratios above 1 would push the network into net deflation, directly addressing one of the primary investor concerns and serving as a key metric to monitor going forward.

Live Applications and Emerging Use Cases

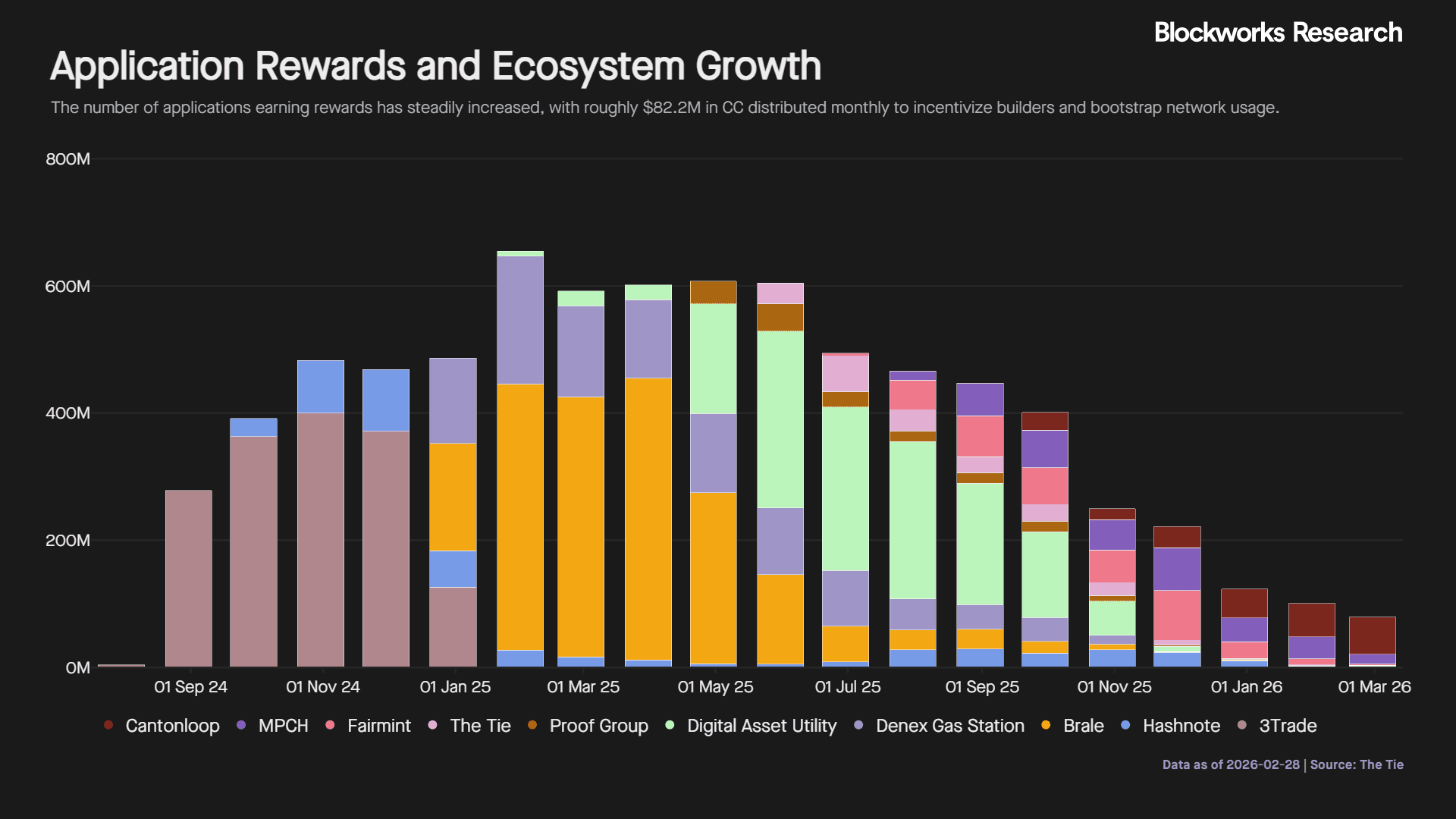

Looking at the top 10 applications by reward share, the number of active earners has steadily expanded over time, indicating a broadening and increasingly healthy ecosystem. At current prices, roughly $82.2M in CC is distributed monthly to applications. This creates a meaningful economic incentive for builders, who can also pass rewards to end users to bootstrap liquidity and usage.

Two standout applications are Brale and Hashnote. Brale currently leads by reward share, with Hashnote ranking fifth.

Brale has built a bridge that converts USDC and USDT into network-native equivalents on Canton, enabling private, institutional-grade payments and settlement. It effectively serves as an on and off ramp into the Canton ecosystem, allowing treasuries and capital markets participants to move cash onchain without exposing transaction details. Users who custody, mint, or settle through Brale can claim CC rewards, directly linking payment activity to token incentives.

Hashnote (acquired by Circle in Jan 2025) brings yield-bearing collateral onto Canton through USYC, a tokenized reverse repo product with over $1B in AUM. USYC functions as an onchain money market instrument that can be used for margin, collateral, and trading workflows while preserving privacy. Subscription fees are charged in CC, and Hashnote redistributes a portion of rewards to connected validators, reinforcing ecosystem alignment.

Other top reward earners include several infrastructure and utility services on the network. Denex Gas Station (previously 3Trade) provides bandwidth management. Cantara supports peer to peer billing. Fairmint enables onchain equity issuance as an SEC registered transfer agent. The Tie provides analytics services. 5North’s Loop is a wallet provider. Digital Asset’s DA Utility provides standardized infrastructure for tokenizing and administering assets using the Canton token standard.

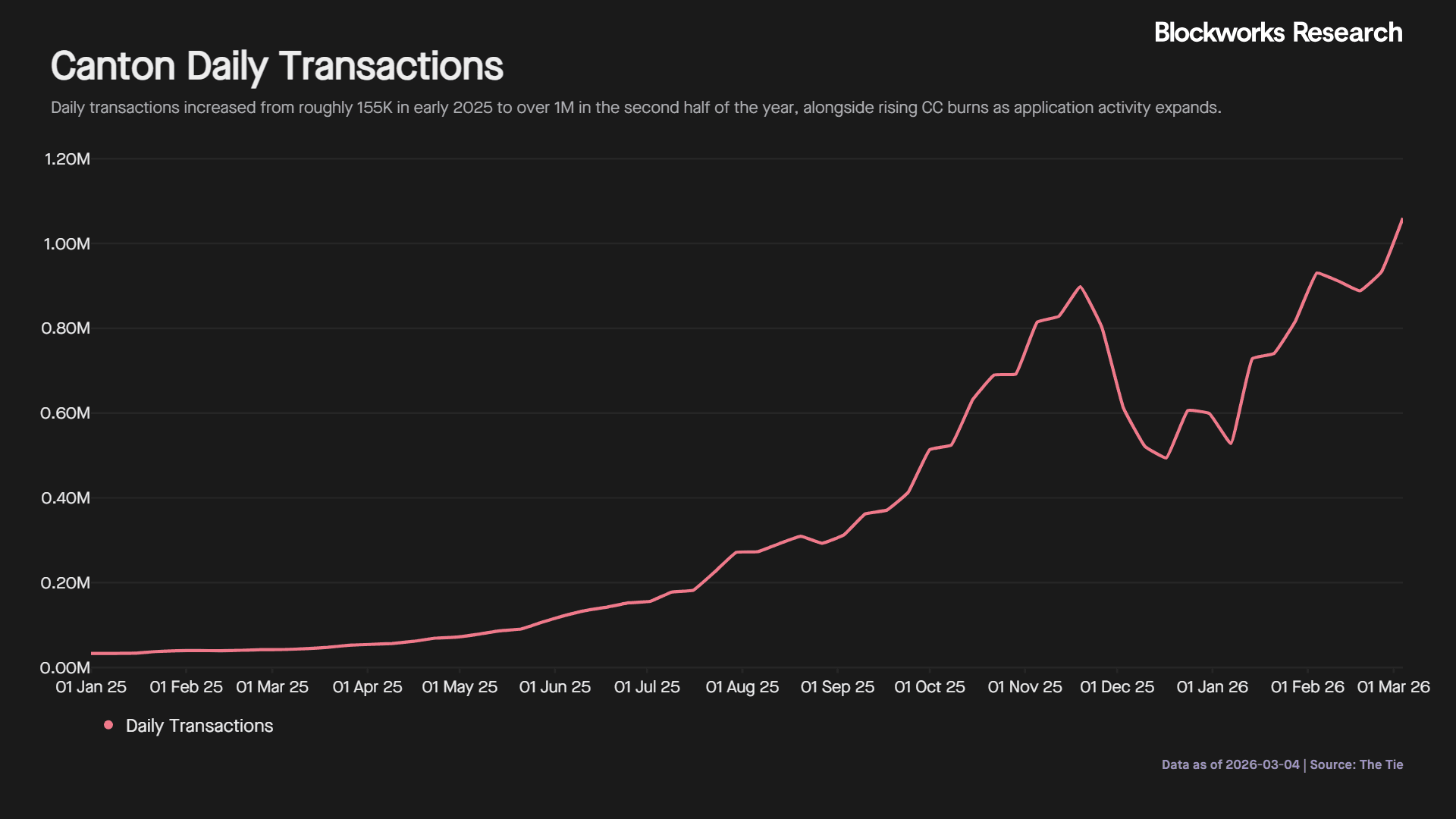

This expanding application base has coincided with a sharp increase in network activity. Daily transactions rose from roughly 155K in the first half of 2025 to more than 1M in the second half. This growth has occurred alongside rising CC burn, reinforcing the link between application activity and network economics.

A recent development is Circle’s launch of USDCx on Canton. USDCx is a privacy enabled stablecoin backed 1-to-1 by USDC held in Circle’s reserve. Only the transacting parties can view transaction details, addressing one of the main barriers to institutional stablecoin adoption. At the same time, USDCx remains interoperable with USDC on other chains through Circle’s bridging infrastructure, allowing institutions to access broader liquidity while maintaining confidentiality within Canton.

This capability unlocks real world financial workflows beyond trading. In February 2026, a multinational company executed the first private onchain payroll using stablecoins on Canton. The transaction was enabled by Toku, which manages global payroll logic, and Cantor8, which provides secure employee wallets. USDCx further simplifies this process by providing a native privacy preserving cash rail within the network.

Across these applications, a common pattern is emerging. Cash, yield bearing collateral, payroll, and repo activity are beginning to operate within the same privacy-preserving and interoperable financial environment. As more institutions move live workflows onto Canton, activity across payments, collateral, and settlement expands. This strengthens both network utility and token burn.

Valuation

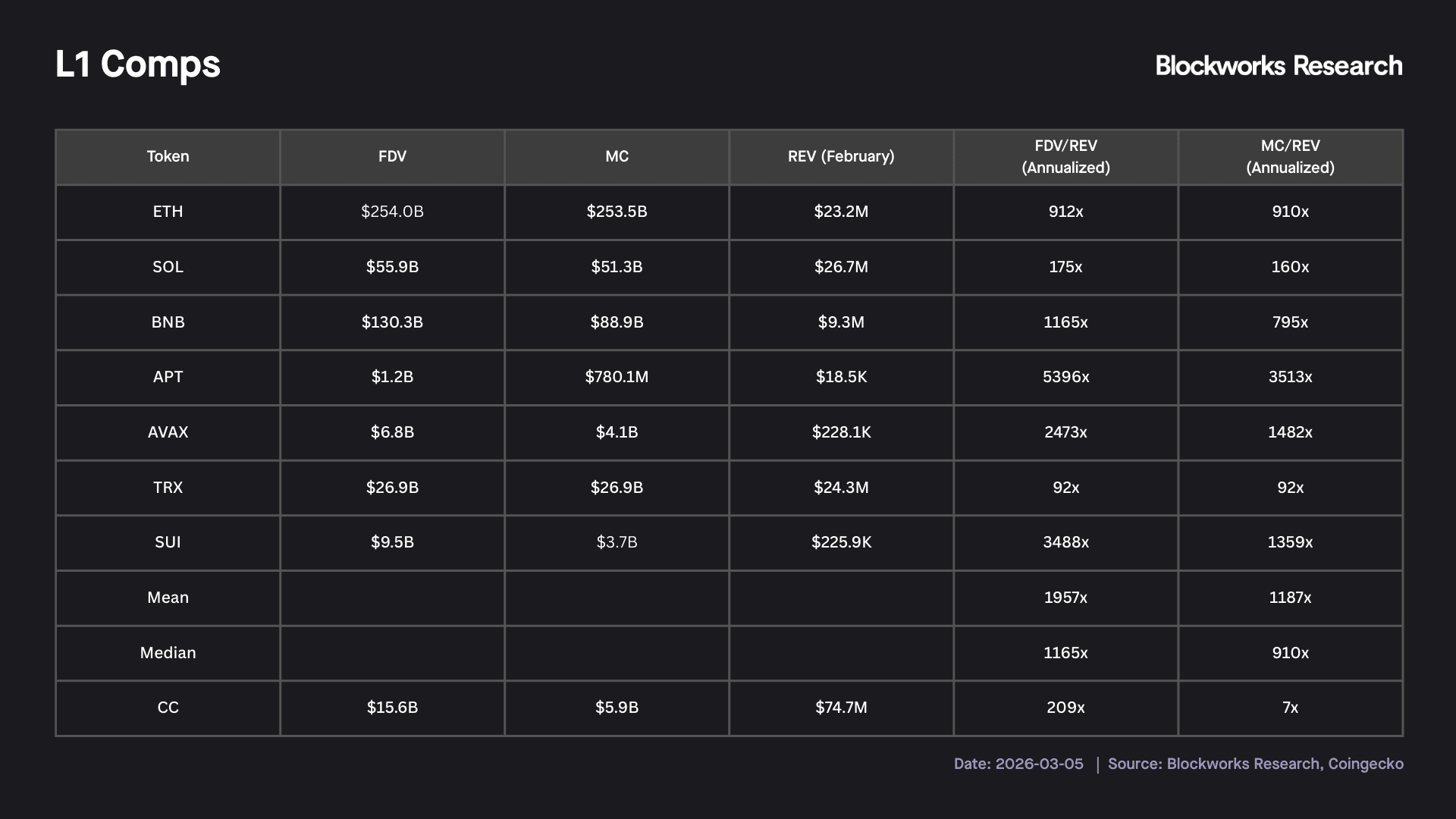

Looking at network REV, defined as fees paid for blockspace and settlement coordination, Canton generated the highest REV among major L1s in February at $74.7M, roughly 2.8x higher than Solana in second place. We estimate FDV using the 100B supply milestone reached around year 10, after which CC emissions continue at 2.5B per year in perpetuity. This approach is intended to account for the potential supply overhang often cited by investors when evaluating Canton.

In practice, Canton’s future supply is dynamic because tokens are continuously burned through network activity. This means circulating supply will ultimately depend on the balance between emissions and token burns rather than a fixed cap.

Even after applying this conservative adjustment to account for future supply expansion, Canton still trades at a significant discount to other L1 networks on both MC to REV and FDV to REV multiples.

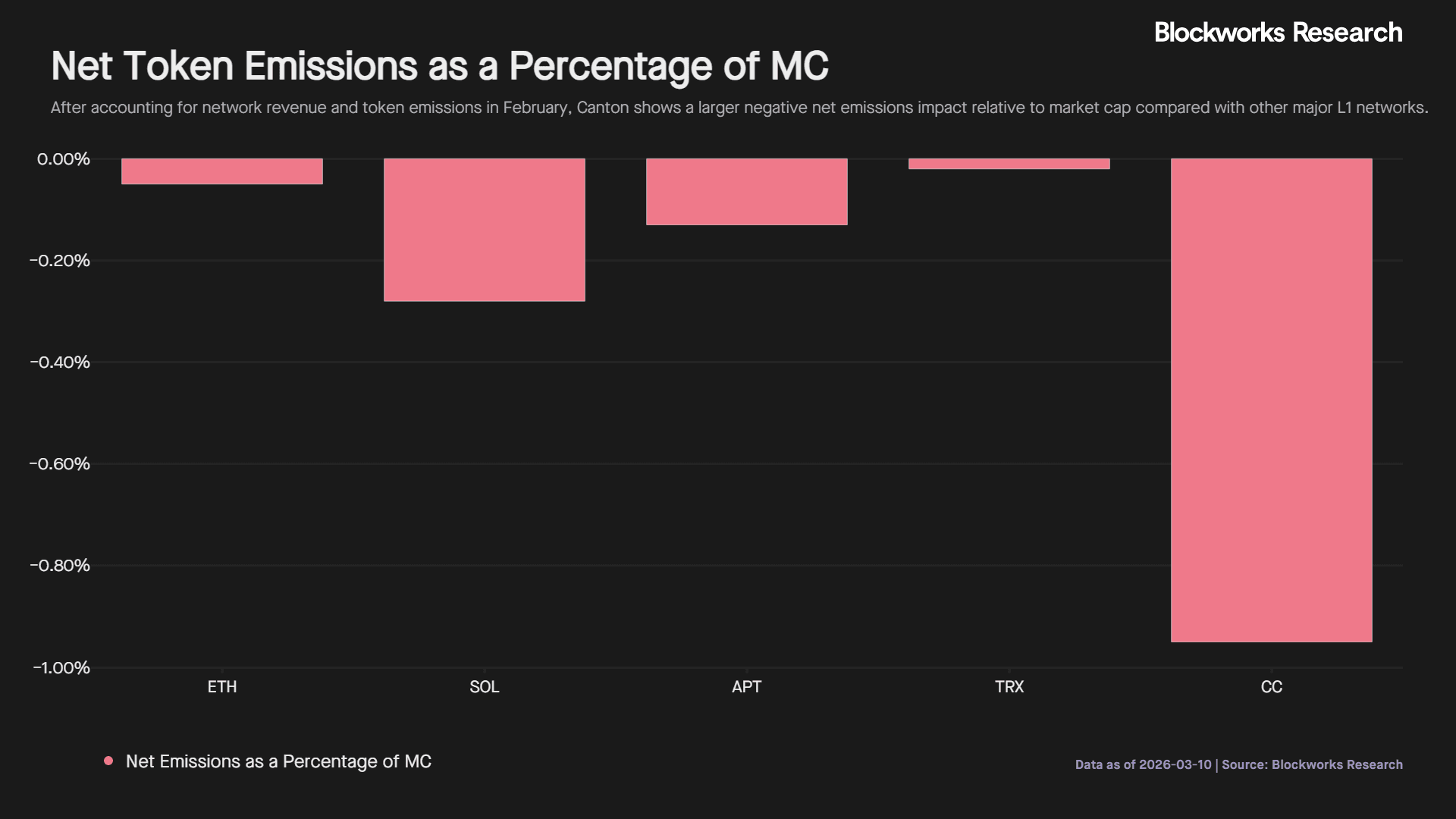

One reason for this discount may be Canton’s relatively high near term token emissions. Monthly emissions currently imply inflation of roughly 2.15% declining to 1.8% over the next twelve months, which remains higher than most L1 networks. A more relevant comparison is net emissions (REV-Emissions) relative to MC. On this basis, Canton’s net emissions represent a larger negative percentage of MC than comparable L1s. This suggests investors may be discounting the token to reflect the higher effective supply expansion despite strong revenue generation.

Another explanation may be how the market interprets Canton’s role within the financial stack. Most L1 networks primarily monetize general purpose blockspace used by DeFi and consumer applications. Canton today functions more as financial infrastructure used by regulated institutions. Much of the activity on the network relates to settlement coordination, collateral management, and tokenized asset workflows between financial institutions.

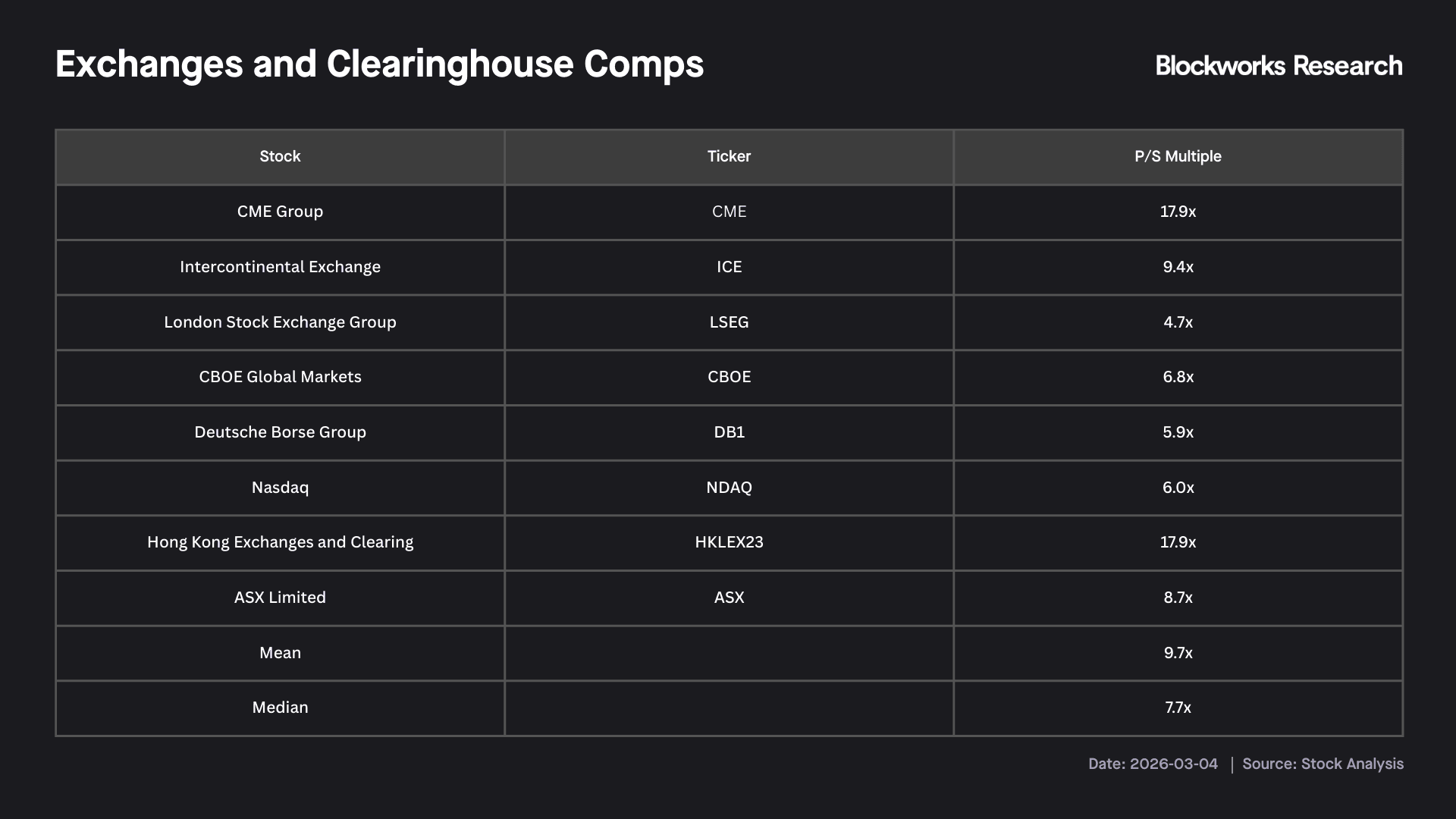

When compared with traditional financial market infrastructure providers, Canton’s valuation appears more aligned. Public exchange operators such as CME, Nasdaq, ICE, and LSEG trade between roughly 5x and 18x revenue, with a median near 8x. This range is closer to Canton’s current valuation multiples.

This suggests the market may be implicitly valuing Canton less as a crypto execution environment and more as a digital settlement layer for financial markets.

Additional upside could emerge if the network begins supporting applications that generate continuous onchain activity. These include prediction markets, perpetual futures trading, lending markets, and other financial applications where users trade, borrow, and manage risk. Such use cases could expand participation beyond institutions and bring a larger base of retail users onto the network. This could allow Canton to trade closer to valuation multiples typically assigned to other L1 networks.

Several applications in these categories are already being developed. ACME Lend is building an overcollateralized lending platform. Unhedged, the first privacy preserving prediction market on Canton, has already processed more than 10M CC in volume with over 11K traders participating across thousands of markets. CantonSwap is a decentralized exchange that already ranks among the top 25 applications by CC rewards received.

Additional assets and applications are also coming online. Franklin Templeton’s BENJI tokenized money market fund is now live on the network, while new lending applications such as Haven and Hello Moon are expected to launch soon. A Ledger integration has been completed and is expected to be announced soon, which will make it easier for users to interact with applications across the network.

Potential Catalysts

One potential catalyst from a regulatory perspective is passage of the Clarity Act. Much of Canton’s growth thesis depends on institutions moving regulated financial assets such as Treasuries, repos, and tokenized deposits onchain. Legislation like the Clarity Act would help define how digital assets and blockchain based infrastructure are regulated in the United States, reducing uncertainty for banks, exchanges, and clearinghouses. Current odds of the Clarity Act being signed into law in 2026 are around 60% on Polymarket.

Another near term catalyst is the rollout of DTCC’s broader tokenization platform. DTCC plans to launch a production platform in the second half of 2026 that will allow participants to tokenize and manage securities such as Treasuries, ETFs, and equities on approved blockchains. If Canton is used as a settlement environment, this could significantly expand the range of tokenized assets and financial activity on the network.

Potential Risk

A potential risk is the concentration of CC ownership among a relatively small number of network participants. Based on current onchain balances, the largest recipients of CC rewards collectively account for approximately 54% of circulating supply. If a small number of large holders were to realize profits or reduce exposure, it could create meaningful sell pressure on the token.

Market liquidity also remains relatively limited. Spot market depth is currently around $350K at -2% on Bybit, which means relatively small trades can move the price materially and amplify volatility if large holders were to reduce positions. However, additional exchange listings may improve liquidity over time. Since the beginning of the year, exchanges such as OKX and Robinhood have listed CC, which could gradually expand trading depth and market access.

This concentration also requires context. The largest balances belong primarily to core contributors, infrastructure providers, application operators, and the Canton Foundation. These tokens were earned through network participation rather than pre-allocations or speculative purchases. As a result, a meaningful portion of these balances is operational in nature and used to support application activity, pay network fees, and bootstrap ecosystem growth.

The Canton Foundation has also recently approved a proposal under which Super Validators may lock a portion of their lifetime earned rewards to maintain validator weight. Super Validator weight determines how much influence and rewards they receive from operating the Global Synchronizer. Over time, this mechanism could help strengthen long term alignment among major network participants and reduce the likelihood of large scale selling.

Conclusion

Canton represents one of the most credible attempts to bring traditional financial infrastructure onchain. Its architecture is designed around institutional requirements, and early adoption from organizations such as DTCC, Nasdaq, and Broadridge suggests the network is gaining traction.

Much of this activity remains in early stages, and the network will need to continue to demonstrate sustained application growth and broader participation to close the valuation gap with other L1 networks.

Ultimately the investment case depends on how quickly financial activity moves onchain. Institutional workflows such as settlement, collateral management, and repo financing represent a large opportunity, but the network is also seeing growth in privacy focused financial applications such as trading infrastructure and prediction markets. As both institutional and application activity expand, Canton could increasingly serve as a coordination layer for financial markets.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.