An Overview of Real World Assets and Tokenization

Key Takeaways

- Tokenized assets reflect crypto's growth as a legitimate asset class and the adoption of blockchain technology by traditional financial players and markets.

- Adoption of tokenized assets will likely slow down amongst retail participants after the high interest rate environment ends and markets shift towards risk on. In the long run, growth will come from institutions, who are likely to adopt tokenization and blockchain technology as it increases efficiency, reduces costs and allows them to access more buyers.

- Stablecoins will continue growing as high inflation across the globe drives demand for tokenized USD. Tokenized commodities beyond gold will slowly expand, but face regulatory hurdles. Tokenized equities and real estate are underexplored areas with adoption risks from regulation and synthetic asset competition.

- Currently, token standards and permissioned chains are used to ensure regulatory compliance. As more permissioned chains are deployed by TradFi institutions, interoperability will become increasingly important.

- Regulatory, counterparty and smart contract risks all remain obstacles to tokenized asset adoption. Additionally, currently, illiquidity and siloed markets due to a lack of standardization is an issue.

Overview

RWAs are tangible assets with intrinsic value, such as stocks, bonds, real estate, commodities, and currencies, which are brought onchain through tokenization.

Tokenization is by no means a new trend and was attempted back in 2017 whenthe focus was on putting illiquid assets such as real estate, commodities, and art onchain in an effort to enable fractional ownership, improved security and fraud prevention, liquidity, and greater accessibility. Early tokenization efforts were largely unsuccessful, potentially due to the immaturity of blockchain technology.

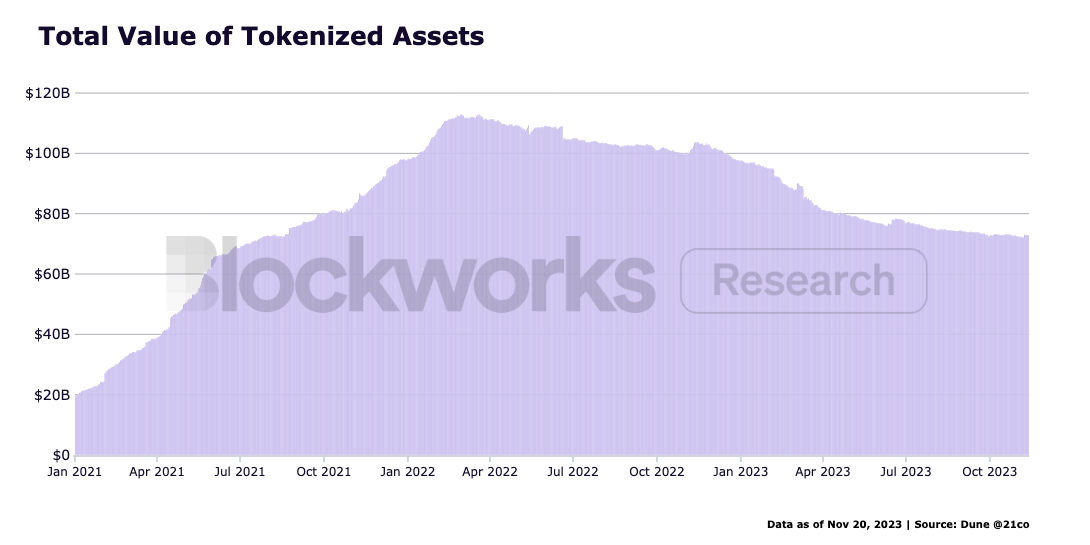

However, over the past year, RWAs and tokenization have grown dramatically, with the total value of tokenized products currently sitting at around $73B USD.

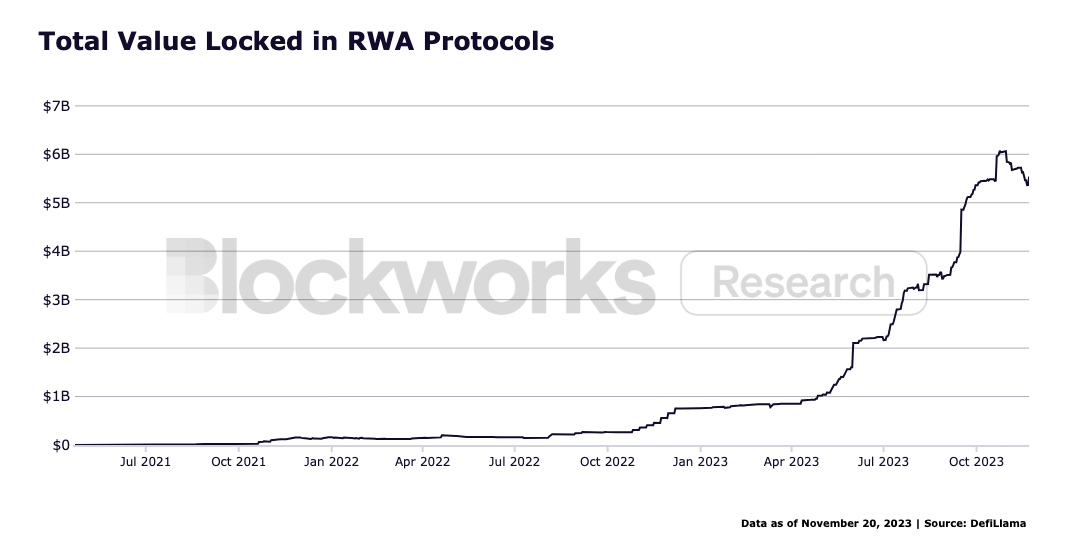

The majority of these tokenized assets are made up of stablecoins. However, there has also been drastic growth in non-stablecoin RWA products, as the total value locked in RWA DeFi protocols has reached more than $6B USD.

Overview of Tokenization Processes, Token Standards and Chain Architecture

RWAs take two different token forms:

- Non-native tokens that exist offchain and are managed by a custodian.

- Native tokens issued onchain as native RWAs and do not represent an offchain asset (i.e. if a bond was issued directly onchain).

To bring a non-native RWA onchain, the custodian must first validate the offchain value (determined by fair market value and other factors), ownership (based on legal jurisdiction via invoices, deeds, or other documents), and regulatory/legal (to disclaim liquidations, ownership etc.) backing. Information about the RWA is then moved onchain, where the ownership and backing data of the RWA is represented using smart contracts and the metadata of the token. Since tokenized assets require regulation, different legal frameworks and methods (KYC/AML rules, licensed token issuers etc.) to ensure regulatory compliance are used.

It’s important to note that regulation surrounding RWAs and cryptocurrencies in general is still immature, so claims on assets offchain vary from jurisdiction to jurisdiction. For example, while the US still has not developed a comprehensive framework for tokenized asset regulation, Switzerland introduced a regulatory framework with their amendments to the Swiss Code of Obligations, formally permitting the creation, listing and exchange of blockchain-based securities such as RWAs on ledger-based trading platforms.

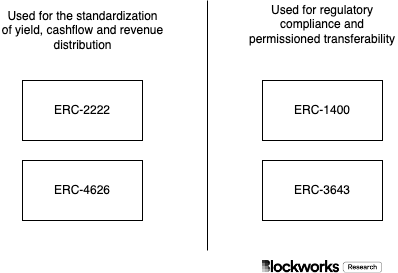

Token Standards

Tokenization of RWAs and of funds and their strategies require regulatory consideration, given that these assets are regulated as securities offchain. Unlike DeFi, most of the traditional financial instruments being brought onchain require users to be accredited investors or institutions that must comply with existing and evolving AML/KYC regulations.

Therefore, token standards for RWAs can be used to ensure KYC/AML compliance and provide permissioned transferability capabilities by enshrining certain constraints in the smart contract. However, different token standards for RWAs are not only used for regulatory purposes. For RWAs that are of a more decentralized nature, such as those developed by Frax, Centrifuge, MakerDAO, and others, token standards are used to standardize methods of passing on income to users safely.

ERC-1400

The ERC-1400 token standard is particularly suitable for regulatory compliance, as it can be programmed to only be transferable to certain parties or automatically comply with sanctions lists. ERC-1400 was developed prior to ERC-3643, and can be viewed as its predecessor. It is currently used by MatrixDock’s STBT, which offers short-term Treasury Bill exposure to accredited investors.

ERC-3643

ERC-3643s are permissioned tokens that have conditional transfer functions requiring approval from decentralized validators based on predefined rules. This permissioned structure suits use cases which enable compliance such as dealing with securities, while maintaining the standard ERC-20 functionality due to their underlying architecture.Unlike ERC-1400, ERC-3643 is able to freeze tokens, perform batch functions (leading to savings on gas), and provide token recovery processes.

ERC-2222

ERC-2222, the Funds Distribution Standard, can be used for payments such as dividends, loan repayments, fee, or revenue shares among token holders. Token holders are seen as fractional owners of future cash flow. ERC-2222 is an extension built upon ERC-20 and is therefore backwards compatible.

ERC-4626

ERC-4626 is a tokenized vault standard that makes it easier for applications to integrate with vaults. ERC-4626 was explicitly developed to standardize tokenized vaults to reduce errors, attack vectors, and integration time for developers. ERC-4626 is used by Frax and MakerDAO in their yield-bearing stablecoin designs, and by Maple Finance in their xMPL contracts to distribute revenues.

Chain Architecture

RWAs can be deployed and issued on either private or public chains. Similarly to token standards, different chain structures are utilized due to legal and regulatory reasons.

Private Chains

Private chains are permissioned distributed ledgers which enable regulatory compliance. For example, they allow only verified participants to validate the chain. Additionally, they offer more control and privacy as access is restricted and administrators determine visibility levels, faster transaction speeds and scalability, the ability to modify structure quickly through internal agreement, selectively revealing data to subsets of participants, and improved compliance capabilities such as granting regulator access.

However, they also come with drawbacks as less decentralized, with small groups controlling access and changes, have higher barriers to entry and smaller ecosystem participation, administrators become central points of failure, and innovation may be stifled without open competition. Furthermore, with the use of private chains, issuers forgo some benefits that come with RWAs onchain, mainly lowered auditing costs and increased liquidity (fragmentation due to many private chains can be resolved partially through interoperability).

Instead, private chains can comply with financial regulations without the use of token standards, as they are already only available to KYC'ed/allowlisted users. Additionally, many large institutions have opted to building their own private blockchains (such as J.P. Morgan’s’s Onyx) instead of using public chains, due to security, liveness, and privacy concerns associated with public chains, as well as the added benefit of feeless transactions that comes with private chains.

Public Chains

Public blockchains such as Ethereum, Solana, and Polygon are permissionless and allow for any user to access, validate and transact. They are battle-tested, composable, decentralized, and trustless. Additionally, public blockchains allow nearly complete disintermediation enabled by open participation, and collective innovation driven through competition in an open ecosystem.

However, they suffer from slower transaction speeds (compared to permissioned chains) and restricted compliance capabilities stemming from a lack of centralized authority. Furthermore, they can have issues due to network outages, smart contract exploits, and compromised keys.

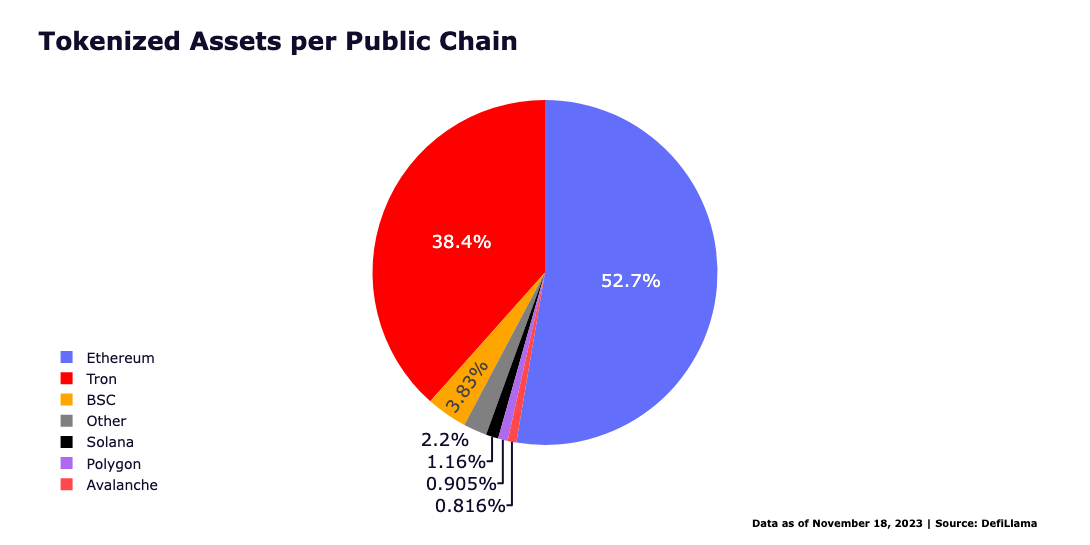

Ethereum is currently the most popular public blockchain for tokenized assets and currently holds more than half of the RWAs and tokenized assets on public chains. Tron is also a strong contender and holds more than $50B USD worth of tokenized assets. Tokenized assets on both chains are largely made up of stablecoins, especially Tron which has captured a significant portion of stablecoin market share across emerging markets thanks to their low fees, network effects and explicit focus on these markets. In contrast to Tron, Ethereum benefits from liquidity network effects, as well as being credibly neutral and highly decentralized, leading to many newer RWA protocols opting to build on Ethereum.

Some public chains have opted to leverage their infrastructure to accommodate both public and private chains. For example, Avalanche has developed Evergreen Subnet, a set of chain deployment tooling that allows for the creation of private/permissioned chains on Avalanche. Evergreen allows for geofencing, KYC checks, and gasless transactions.

The potential to bring in both permissionless and permissioned chains under its infrastructure could be highly rewarding and beneficial for Avalanche, as it will benefit from increased volumes, users. Additionally, it could lead to potential decreases in circulating supply and an increase in demand for AVAX, since Subnet validators must also validate on Avalanche C-Chain by staking a minimum of 2,000 AVAX.

Interoperability

Interoperability and cross-chain messaging allow protocols and products to be deployed and used across different chains, potentially reducing the inefficiencies that come with fragmented liquidity and increasing composability. Additionally, interoperability allows for users to interact with chains through a single interface, rather than separate implementations. This not only improves user experience, but also allows developers to save significant amounts of time and resources.

Interoperability between private and public chains is particularly challenging, since it comes with legal and regulatory risks on top of technical risks (such as infinite mint attacks and other smart contract exploits). Chainlink and Axelar are currently at the forefront of public-private chain interoperability and cross-chain messaging, as we see more and more institutions start experimenting with proof of concepts for cross-chain messaging between private and public chains.

Chainlink's CCIP can be used for interoperability between private and public chains. CCIP is a general cross-chain transferring protocol that allows messaging and token transfer between chains. Tokens are locked or burned on the source chain and minted on the destination chain.

Chainlink has recently partnered with the ANZ (Australia and New Zealand Banking Group) to explore how its customers can use CCIP to settle tokenized assets across public and private blockchains. The team has also partnered with SWIFT and large financial institutions including the ANZ, BNP Paribas, BNY Mellon, Citi, Clearstream, Euroclear, Lloyds Banking Group, SIX Digital Exchange (SDX), and The Depository Trust & Clearing Corporation (DTCC) to explore how existing SWIFT infrastructure can be leveraged to transfer tokenized assets across public and private blockchains using CCIP.

Axelar is an IBC-compatible general cross-chain communication network built using the Cosmos SDK. Axelar uses Proof-of-Stake consensus to validate messages between Axelar and destination chains.

Axelar recently partnered with JPM, Avalanche, and LayerZero to explore a proof of concept (POC) that explores messaging and asset transfers between private and public blockchains. As part of this POC, Axelar provided message validation and message passing by deploying a permissioned Axelar testnet and private offchain relayers.

In addition to the JPM Onyx-led POC, Axelar has also recently partnered with Ondo Finance, a tokenized debt protocol, to launch Ondo Bridge for native RWA token bridging assets from Ethereum to Mantle.

Similarly to Axelar, LayerZero took part of the JPM Onyx led POC, where they explored messaging and asset transfers between private and public blockchains. LayerZero provided an oracle and relayer to pick up an offchain message, and transmitted it to LayerZero endpoint contracts on Avalanche.

Despite Chainlink’s explicit focus on institutional adoption of CCIP, the participation of Axelar and LayerZero in the JPM Onyx POC shows that the playing field for interoperability providers is still very much even. Given that interoperability between private and public chains is still relatively underexplored and nascent, it’s likely that the ideal solution has not been implemented yet.

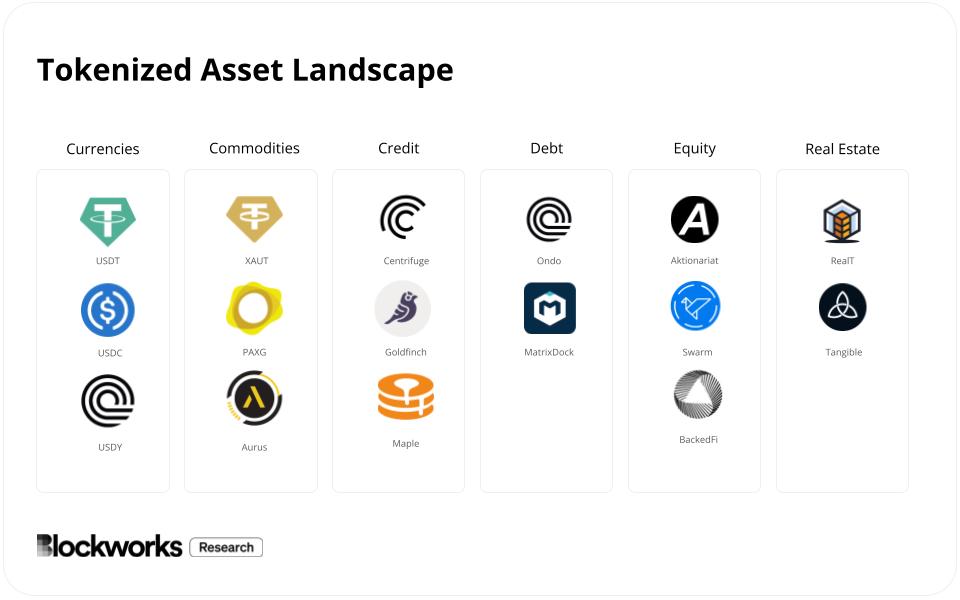

Tokenized Asset Classes

Tokenized Currencies

Tokenized currencies (stablecoins) are by far the most popular tokenized asset that currently exists in crypto. USDT and USDC combined have a market cap nearing $110B onchain, and $71B in EVM chains, which represents approximately 97% of tokenized assets on them.

The most popular tokenized stablecoin provider is Tether. USDT currently holds 70% of the market share for stables. Its dominance has grown recently, while USDC market share has declined. Part of the reasoning behind this is that USDT is used more commonly by users in emerging markets who are looking to access USD. In contrast, USDC is more DeFi focused, and utilized by crypto native participants.

The adoption of digital stables has mostly been led by countries with high inflation, such as Argentina, Turkey, and Lebanon, where citizens want to denominate their wealth in USD. In contrast to holding USD in a bank, USDT and other stables are easier to access, given that banks in these countries often set limits on how much USD can be withdrawn, and can be used to transfer internationally and for payments.

Additionally, participants who use USDT and other stables are often distrustful of their own banking system, and are more willing to trust Tether as a counterparty given that USDT is regulated by Bermuda and is backed by short-term bills rather than a portfolio of credit cards, mortgages, car loans of the local country.

Centralized stablecoins such as USDT and USDC allow issuers to capture the full yield of their underlying assets while passing on their risk to the customers. Newer stablecoins and stablecoin protocols, discussed below, instead have opted to pass on a large portion of the yield (less fees) from the underlying assets to holders.

Tokenized USD and stablecoin adoption will undoubtedly continue to grow. Even by crypto critics, they have been lauded as one of the few products that have found legitimate product market fit. They are a response to real needs and have genuine demand, which is to offer easier and more efficient access to foreign currencies.

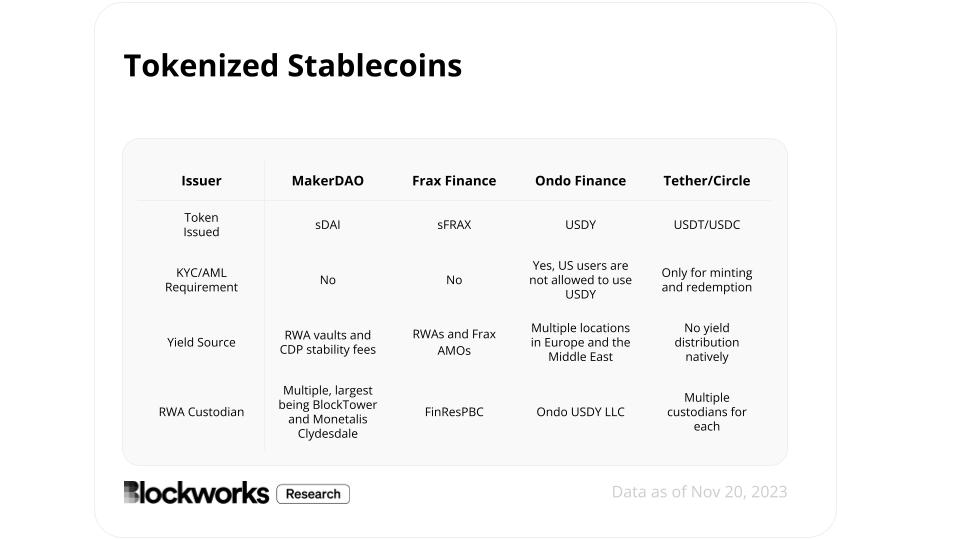

sDAI, MakerDAO

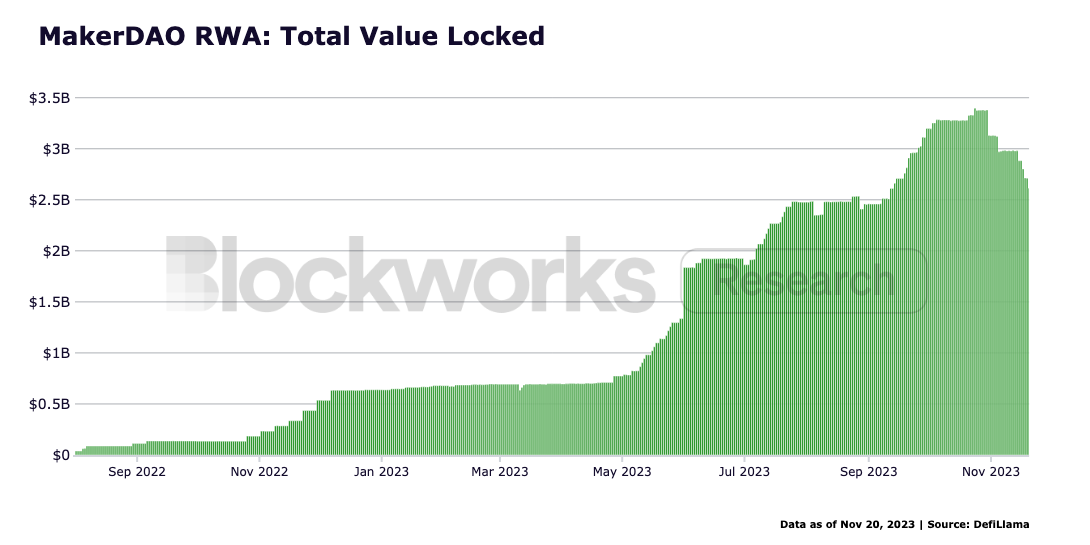

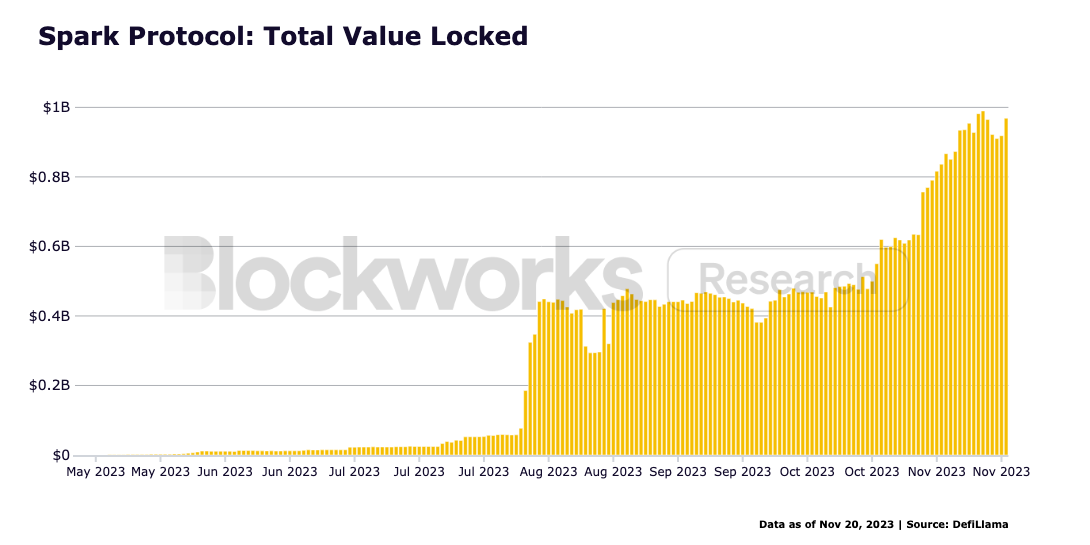

MakerDAO has launched sDAI under Spark Protocol, a decentralized, non-custodial liquidity market protocol that enables lending and borrowing in the DAI ecosystem. sDAI is a tokenized version of DAI deposited into the DSR (Dai Savings Rate). sDAI uses the ERC-4626 standard, and pays out yield (the DSR) through protocol-generated revenue, including stability fees and RWA investments, with the latter becoming an integral source of revenue for the protocol. The DSR is currently at 5%. MakerDAO currently utilizes third party asset managers to allocate to RWAs such as Monetalis Clydesdale and Blocktower Capital.

Maker’s RWA investments have quickly become an integral source of revenue for the protocol and have only relatively recently started being used to fund the DSR. Previously, and currently still, the DSR was funded out of stability fees paid by CDPs. Stability fees are paid by every CDP and are an annual percentage yield that is calculated on top of the existing debt of the CDP and has to be paid by the CDP

MakerDAO’s RWA investments have increased by more than 300% since the beginning of the year. As of October 2023, MakerDAO had $3.25B USD of exposure in RWAs through third party asset managers (MakerDAO has since had to draw down $250M from Coinbase Custody to DAI’s peg stability module (PSM)). MakerDAO’s two largest RWA vaults are RWA-007 representing $1.25B USD, with Monetalis Clydesdale, and RWA-015 representing $1.38B USD with Blocktower Andromeda. These two vaults combined represent nearly 81% of their total RWA exposure.

As MakerDAO’s RWA exposure has increased, so has Spark Protocol’s TVL. In just over 7 months, Spark’s TVL has reached $1B USD.

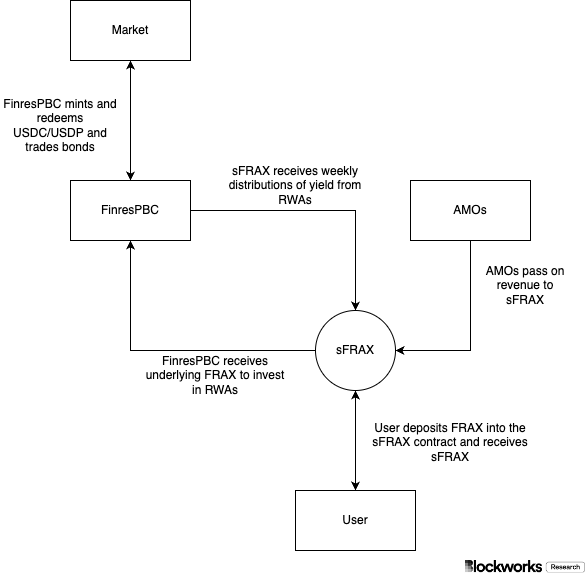

sFRAX, Frax

The Frax protocol issues decentralized stablecoins with four native tokens: its FRAX and FPI stablecoins, liquid staking token frxETH, and Frax Shares (FXS) governance token. With the launch of Frax v3, Frax introduced their first RWA product, staked FRAX (sFRAX). sFRAX offers yield to depositors by utilizing the ERC-4626 standard.

While sFRAX is designed to generate yield through both RWAs (US dollar deposits, T-bills, Federal Reserve repos and money market mutual funds) and Frax AMOs (lending, collateral investor and DEX AMOs), it currently generates its yield through sDAI - as they are currently prioritizing maintaining a 100% collateral ratio.

sFRAX's yield tracks the interest on reserve balances interest rate (IORB), which is approximately 5.4%. This is a soft target, and Frax’s main goal is to prioritize maintaining a 100% collateral ratio for FRAX before distributing yield to sFRAX.

For their RWA operations, Frax partnered with FinresPBC. FinresPBC is a not-for-profit C corporation based in Delaware. As Frax’s custodian, FinresPBC holds US dollar deposits in FDIC insured savings accounts, mints and redeems centralized stablecoins which back FRAX (i.e. USDC) and holds and trades US T-bills in brokerage accounts.

USDY, Ondo Finance

USDY is Ondo Finance’s yield-bearing stablecoin collateralized by short-term US Treasuries and bank demand deposits. In line with Ondo Finance’s mission to provide institutional-grade, blockchain-enabled investment products and services, USDY is the first tokenized note secured by treasuries, making its utility and accessibility on par with stablecoins. USDY holders receive the yield generated by the underlying assets in the form of increasing redemption value (i.e. 1 USDY is worth 1.04 USD when redeemed in one year's time if the APY from underlying assets is 4%.) USDY is a general access product, meaning that any user who provides KYC can mint USDY. Additionally, USDY can only be transferred to those on the Allowlist - i.e. KYC’d users.

USDY’s appeal comes from the fact that it can be redeemed relatively easily - given that often users have to OTC to redeem USDT, and USDC has started halting retail accounts. Additionally, it gives users yield corresponding to the risk that they assume, unlike USDC and USDT who pass off all risk to the consumer and keep the yield earned by underlying assets.

Gold & Other Commodities

Tokenized gold is one of the earlier tokenized products launched for users back in 2019 with Paxos. Its benefits are similar to those that come with tokenized currencies and stablecoins: it allows users to easily hold and trade gold using DeFi and without KYC, instead of traditional financial rails.

In terms of mechanics, the most popular tokenized gold products (Tether’s XAU₮ and Paxos’ PAXG) are structured similarly to how Tether's USDT and Circle's USDC works.

XAU₮/PAXG are ERC-20 tokens backed by 1 fine troy ounce of gold. Physical bars are stored in a vault in Switzerland (for Tether) or London (for PAXG). Only verified individuals or corporations, who have passed identification and financial statement checks, are able to mint XAU₮/PAXG. However, XAU₮ and PAXG can be traded by anyone as an ERC-20 token on Ethereum.

Aurus’ offering differs slightly in its implementation. Firstly, Aurus does not only offer users gold, but also access to tokenized platinum and silver. tGOLD (TXAU), tSILVER (TXAG) and tPLATINUM (TXTP) are backed 1 to 1 by 1 gram of physical gold, silver or platinum, unlike XAU₮/PAXG which are backed by an ounce of gold. Aurus also offers stakers to earn fee revenue, if they stake the native token AX. This revenue comes in the form of TXAU, TXAG or TXTP from tokenization, burning and transaction fees.

Gold is by far the most popular commodity onchain, with other options being dramatically underrepresented. Aurus’ tokenized silver and platinum products have only a combined $600K USD in market cap currently.

Recently there have been attempts to provide a larger variety of more exotic commodities available onchain, such as Uranium with Uranium3o8 (in partnership with Madison Metals). As the crypto and DeFi continue to mature, it's likely that additional commodities such as uranium, oil, natural gas, and lithium will become tokenized and gain popularity onchain. Tokenized commodities enable greater accessibility and liquidity for users and reduced volatility and improved transparency for commodities as an asset class. These come with additional custody and regulatory risk (especially for uranium), so will likely take longer to implement.

Credit

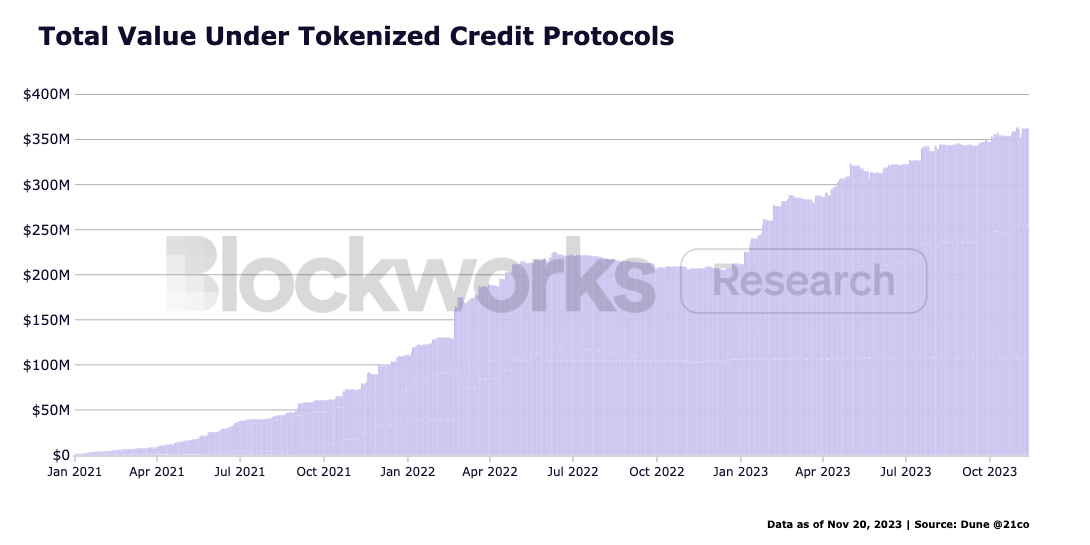

Tokenized credit protocols have grown significantly over the past year, with protocols such as Centrifuge amassing $250M in total assets under management.

Most tokenized credit protocols follow a similar structure:

- Borrowers are able to borrow from an individual pool if they pass checks and can agree on loan terms. The terms of the loan are agreed on by the borrower, the protocol, and often a third party credit underwriter.

- Lenders deposit capital into the pool and earn yield based on interest payments.

Tokenized credit protocols have found product market fit to an extent since they fulfill an important role. Unfortunately, they also come with greater risks than tokenized debt protocols. For example, following the collapse of FTX, multiple institutional borrowers, including Orthogonal Trading and Auros Global, defaulted or had to restructure their loans on Maple Finance as they had funds stuck on FTX.

This may be slightly detrimental to their adoption, as less sophisticated retail participants who are interested in tokenized debt will likely be attracted to AAA-rated tokenized bonds due to lower risks. Additionally, with the growth of the crypto ecosystem overall, there might be more institutional and sophisticated participants who are able to properly assess and participate in tokenized credit - potentially leading to increased efficiency for the terms of loans as well.

Versus other tokenized assets, tokenized credit protocols differ in the demographic that they attempt to attract. Currently, Centrifuge, Maple Finance and Goldfinch are three of the leading lending protocols.

Centrifuge is focused on connecting DeFi protocols with creditors. Maple Finance offers credit to market makers, and institutions,while also enabling access to tokenized Treasuries. Goldfinch focuses on lending to small businesses and borrowers, who may not have access to capital, and matching them with onchain lenders.

Due to the nature of credit, protocols take on significant risk. Although all tokenized credit protocols are structured such that active auditors and other credit professionals assess the creditworthiness of borrowers, there have been historical instances where protocols have accrued bad debt, as has been the for Goldfinch due to a default involving a borrower company that provided an unauthorized intercompany loan to a subsidiary that eventually led to a loss of the entire $5 million loan. However, this is to be expected, given that credit is offered to firms that are not able to get credit through easy means - either due to a lack of access to the level of credit required or for other reasons such as a lack of developed credit markets.

Overall, despite their riskiness, tokenized credit protocols fulfill an important role that blockchain technology promises through tokenization by connecting borrowers offchain to capital and lenders onchain.

Centrifuge

Overview

Centrifuge provides the infrastructure to offer credit and financing for real-world assets natively on-chain. Centrifuge is built atop Centrifuge Chain, a RWA-focused Layer 1 built using Substrate. This infrastructure allows Centrifuge to create transparent and permissionless borrowing and lending markets in the form of pools, without intermediaries.

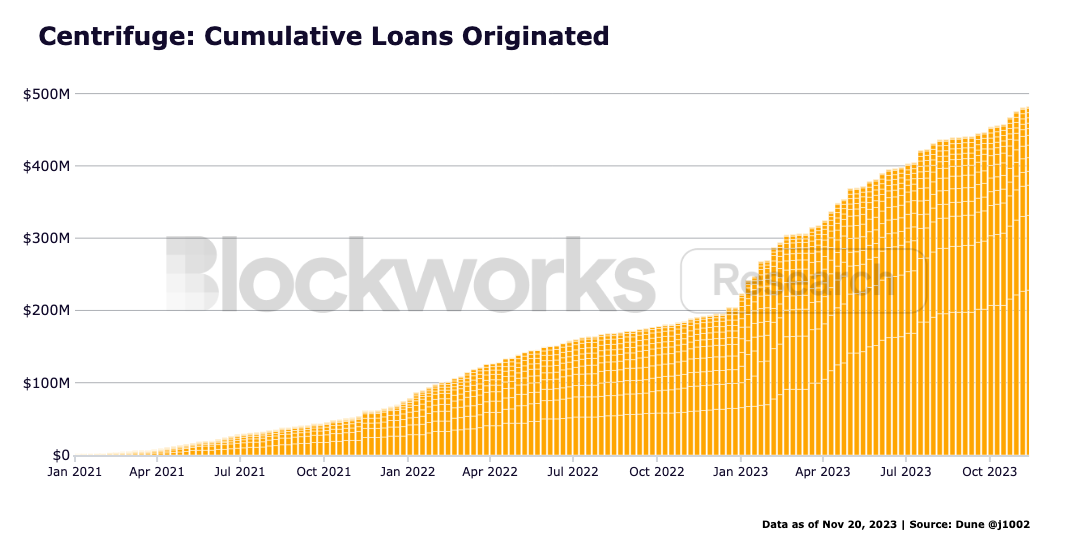

Centrifuge has originated a cumulative $482M USD onchain since their launch in late 2020, and has tokenized 1,341 assets in total.

Currently, approximately 47% of loans issued by Centrifuge are originated by BlockTower, and used by Maker to fund investments in real-world assets. BlockTower Series 3 and Series 4 structured credit pools hold $185M USD.

Centrifuge has partnered with Aave to use Aave's stablecoin treasury for RWA investments through Centrifuge Prime, by allocating $1M USDC to the Anemoy LTF, a short-duration US treasury bill pool on Centrifuge.

In addition, Centrifuge is exploring backing GHO, Aave's stablecoin, with RWAs. Their partnerships with DeFi protocols and DAOs are part of their newer product Centrifuge Prime, Centrifuge’s infrastructure and services offering for DeFi protocols and organization to onboard RWAs.

Mechanics

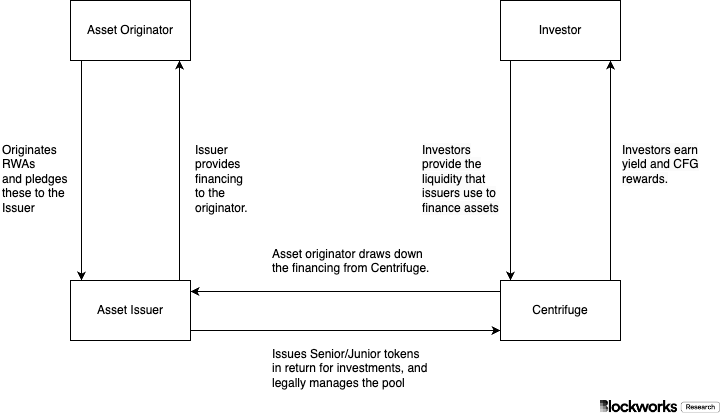

Centrifuge Pools allow asset originators to finance real assets like invoices and mortgages on the blockchain by tokenizing them as NFTs, which are then used as collateral:

- Investors provide the funds for financing by investing in Centrifuge pools, enabling originators to access liquidity. They earn yield and CFG rewards in return.

- Asset originators originate RWAs and pledge these to asset issuers.

- Asset issuers issue senior and junior tokens and legally manage the Centrifuge pool. Issuers also provide financing to the asset originator, by drawing down the financing provided by investors.

Asset pools are fully collateralized, and liquidity providers (investors) have legal rights. Pools are asset-class agnostic, and allow investors to access mortgages, invoices, micro-lending, and consumer finance.

Centrifuge pools use a tiered investment structure with different tranche tokens representing varying risk and return levels. The typical structure includes a senior token offering stable returns protected by a junior token taking first loss risk for higher potential returns. Mezzanine tokens with fixed returns exist between senior and junior tokens, in that they are subordinate to senior tokens and protected by junior tokens.

Tokenomics

CFG Token

CFG is Centrifuge’s governance token. The value of the CFG token is derived mainly from its use for transaction fees on Centrifuge Chain. Additionally, CFG allows holders to participate in network governance.

Goldfinch

Overview

Goldfinch is an onchain credit protocol that allows offchain entities to access credit without crypto collateral, but with real-world collateral.

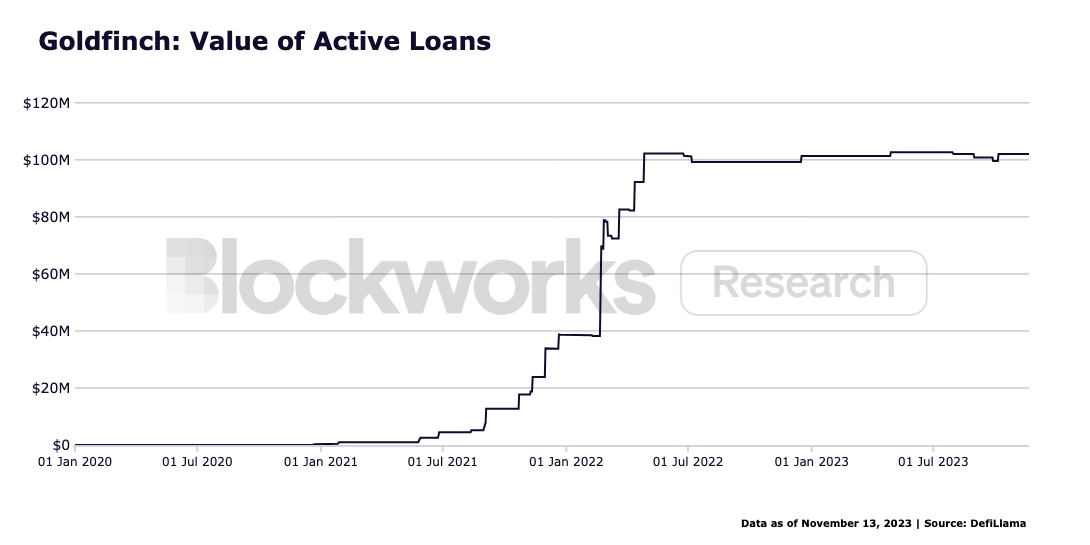

Goldfinch currently has over $102M USD in active loans with the majority of these being lent out to US, Mexico, and Kenya.

Unlike Centrifuge, whose focus has shifted towards building infrastructure to connect DeFi protocols with creditors, Goldfinch’s business model relies on lending to small businesses, who may not have access to capital, and matching them with onchain lenders. This has led to bad debt for Goldfinch creditors on multiple occasions.

Recently, $7M of a $20M loan for Goldfinch borrower Stratos has been written down, after Stratos invested in tech companies and cryptocurrencies. Back in 2021, Tugende, a motorcycle taxi financing company based in Uganda, had to restructure their loan terms with Goldfinch, after they defaulted on their loan of $5M USD.

Mechanics

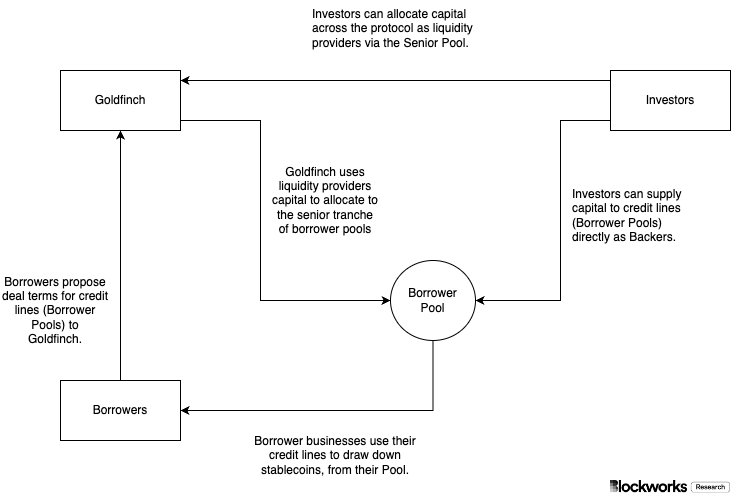

Goldfinch offers two ways for investors to supply credit - as a backer to junior tranches of individual pools, or as a liquidity provider to the senior pool.

Similarly to Centrifuge, Goldfinch offers different credit tranches where investors (backers or liquidity providers) can deposit into junior or senior tranches of borrower pools. Users who deposit into junior tranches earn additional returns due to the increased risk they take.

Backers take on additional risk and own the junior debt tranche. They receive NFTs to track deposits, and the interest is paid out pro-rata depending on NFT ownership. Additionally, the protocol incentivizes backers with GFI rewards for early due diligence and the extra risk they take on by investing in junior tranches.

Liquidity providers own the senior debt tranche across all pools. They earn diversified yields with lower risk. Additionally, as they own the senior tranche, they get repaid first in the event of a default. Liquidity providers deposit to the senior pool and receive FIDU tokens. Goldfinch uses a leverage model to determine how much capital the Senior Pool (which liquidity providers deposit to) allocates toward each Borrower Pool. More senior pool capital is allocated to pools with more backer deposits and a more distributed backer set.

One important difference between Centrifuge and Goldfinch is that Goldfinch is not a permissionless protocol. Borrowers have to go through KYC procedures to verify their identities and gain access to credit opportunities, both on the business and lender sides.

Borrowers are businesses that create “Borrower Pools”, smart contracts through which they borrow and repay capital. Borrowers must be approved by Auditors to create a Borrower Pool. Each Borrower Pool has an interest rate, borrow limit, payment frequency, term length, and late fee that Borrowers define.

Auditors perform human-level checks on Borrowers to ensure that they are legitimate and not fraudulent. Auditors earn GFI rewards for their work.

Tokenomics

GFI and FIDU

Goldfinch uses two native tokens, GFI and FIDU, as well as the stablecoin USDC.

GFI is the core governance token, and is used for governance voting, Auditor staking and rewards, community grants, staking on Backers, and protocol incentives. Additionally, it can be deposited into a Member Vault to earn Member Rewards in exchange for helping to secure the protocol’s growth.

FIDU represents deposits to the Senior Pool from Liquidity Providers. Liquidity providers receive an equivalent amount of FIDU when they deposit liquidity into the Senior Pool. FIDU can be redeemed for USDC in the Goldfinch dApp at an exchange rate based on the net asset value of the Senior Pool, minus a 0.5% withdrawal fee.

Maple Finance

Overview

Maple initially started as an undercollateralized lending protocol. Following the decline of interest in undercollateralized lending after the collapse of FTX, the team shifted its focus to offer overcollateralized or secured lending for cash management and RWAs, while continuing to offer some undercollateralized lending options.

Maple currently offers four types of pools for lenders to deposit into:

- Cash Management: Offers lenders access to US Treasury bill yield, through Room40. Room40 is a fund which is the sole borrower from the Cash Management pool. They convert USDC to USD and invest in treasury bills through a brokerage.

- RWAs: Offers access to various different forms of offchain debt through secured lending to offchain originators and corporates. Currently offering investment grade debt and US Treasury Tax Receivables

- Overcollateralized Lending: Secured lending to institutions overcollateralized by digital assets.

- High Yield Lending: Unsecured lending to institutions for market making.

Maple has originated nearly $2.9B in loans since May 2021 and currently has 1.4K unique lenders.

Through its Cash Management Pool, Maple offers treasury bill yield. This pool has originated nearly $765M in loans and has paid out 4.76% in lifetime APY denominated in USDC.

Mechanics

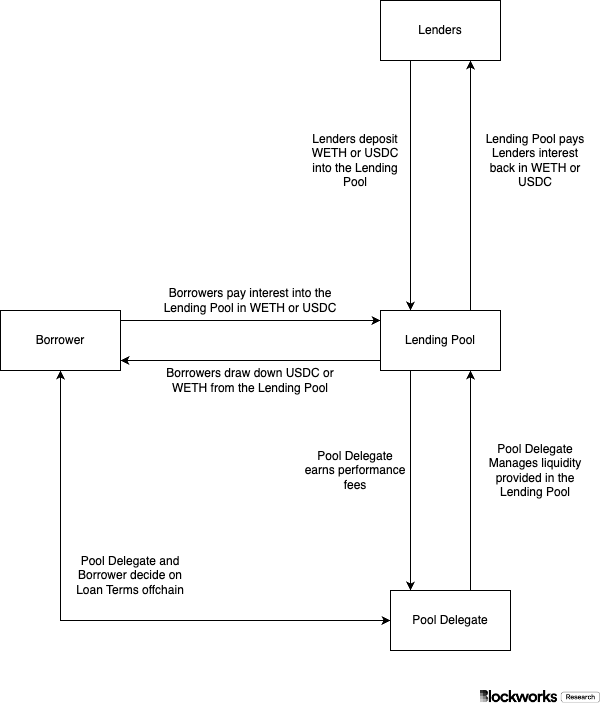

Maple Protocol provides a decentralized lending and borrowing infrastructure run by 3 key actors: Borrowers, Lenders, and Pool Delegates.

Borrowers must apply and be approved by the Maple team in order to create a pool. If approved, they can create an RFQ for a loan. Pool Delegates, (typically funds and professionals with credit experience) conduct due diligence on the borrower’s reputation, financial strength, and creditworthiness, and agree to loan terms with the borrower.

Once Delegates and Borrowers agree on terms, the Borrower will create an on-chain loan request and the Pool Delegate can approve a transfer of funds from their designated Lending Pool.

When pool delegates fund a loan, they will take idle liquidity from the lending pool and transfer it into a loan contract with the borrower.

Each Maple Pool is represented by a smart contract. Lenders deposit liquidity into pools and earn interest in the form of the pool’s liquidity asset (currently only USDC and WETH). . Lending to a pool calls the "Deposit" function, which accepts the lent assets and issues Pool LP Tokens in return. The pools use the ERC-4626 standard to determine how the LP Tokens gain value from loan repayments.

Aside from permissionless pools, Maple also offers permissioned, private pools, in case a borrower needs to ensure that all lenders in the pool are KYC'd and known.

Tokenomics

MPL

MPL is the native token of Maple, which enables users to participate in governance. Since MPL holders control the Maple Treasury, they are able to vote on MPL buybacks and fee distributions.

MPL can be staked for xMPL. xMPL holders receive MPL, which is bought from the open market using excess revenues by Maple Finance. As currently, revenues do not exceed operating expenses, no MPL is being distributed.

Tokenized Debt

Tokenized debt products and total value locked in them flourished under the high interest rate environment, as they managed to attract users with lower risk and higher, uncorrelated returns compared to DeFi - even those seen from bluechip protocols.

Protocols like Ondo Finance and MatrixDock, which provide access to US Treasury bonds, have seen rapid growth in their AUM. Since April 2023, MatrixDock's TVL has nearly doubled to $111M USD, and Ondo has reached $200M USD in TVL since their launch in February 2023.

Aside from protocols offering access to US debt, we've also seen Asian governments offer treasury bonds onchain. The Hong Kong government issued $800M HKD (worth approximately $100M USD) of tokenized green bonds earlier this year, under their Green Bond Program. The Philippines Bureau of the Treasury, the Development Bank of the Philippines and the Land Bank of the Philippines recently announced that they will be offering 10B pesos (worth $179M USD) in one year tokenized treasury bonds onchain.

In addition to treasury bonds, some companies have also begun to experiment with issuing corporate bonds onchain recently: for example, Siemens issued 60M euro in digital bonds on Polygon in February of this year.

The adoption of tokenized debt and bonds from onchain users and retail participants will likely stagnate as markets become more risk on and interest rates are lowered, leading to participants seeking higher returns through riskier investments. Additionally, their growth will depend on the financial sophistication of generally risk averse retail participants and demand from funds for foreign government and corporate debt. Retail participants are likely to find investing in tokenized debt more difficult than investing in yield-bearing stablecoins. Funds usually tend to invest in domestic securities, and if not likely already have convenient access to foreign debt.

As such, a primary catalyst for growth and long-term adoption for tokenized bonds will likely come from governments and large financial institutions, who can leverage the efficiency, reduced costs, liquidity, and broader access that tokenization offers.

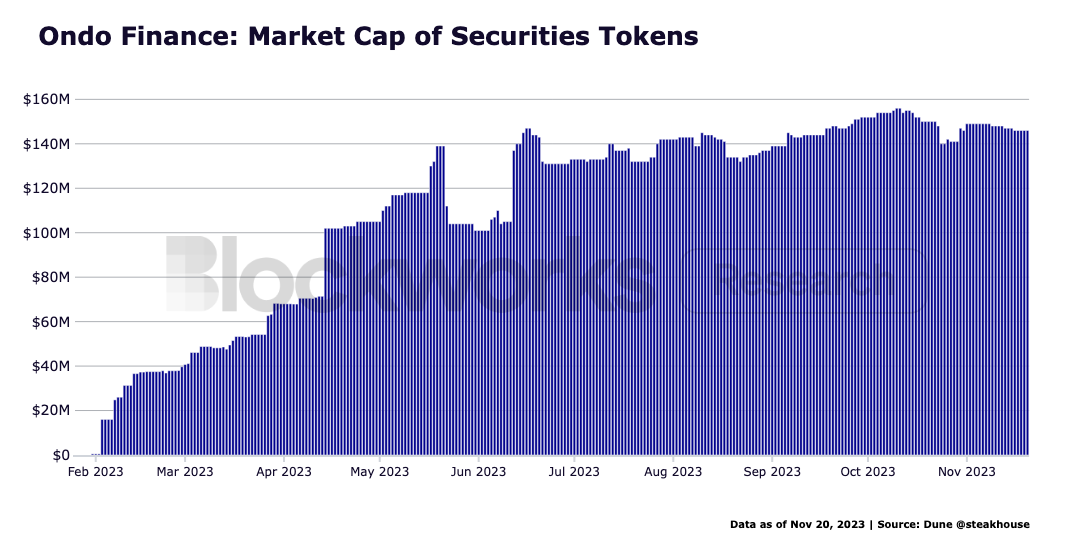

Ondo Finance

Overview

Ondo Finance offers a suite of regulated and KYC-compliant products and services onchain: USDY, a yield-bearing stablecoin; OUSG, tokenized exposure to short-term Treasuries; and Flux Finance, a lending protocol.

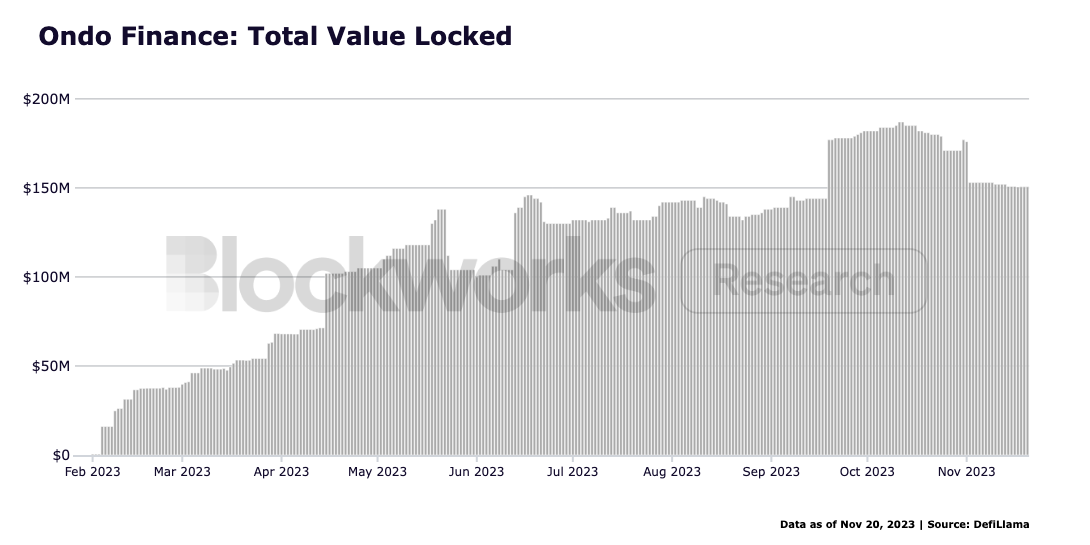

Since its inception in January 2023, Ondo Finance has seen rapid growth, surpassing $200M in total value locked in just over 11 months.

Ondo’s OUSG product currently has a market cap of $150M USD, which represents more than 40% of the total market cap of tokenized securities.

Despite most of Ondo’s tokenized securities existing on Ethereum (approximately 75%, with the rest spread between Mantle and Polygon), the team has recently partnered with Mantle to offer USDY on Mantle. Additionally, Ondo has partnered with Axelar to offer cross-chain issuance and bridging of OUSG and USDY across chains supported by Axelar.

Mechanics

OUSG

OUSG provides users with tokenized exposure to short-term Treasuries. Currently, OUSG tracks BlackRock’s SHV short-term Treasuries ETF. Unlike USDY, OUSG is only available to accredited investors or qualified purchasers.

Users can deposit USDC for access to OUSG, a tokenized representation of the assets managed by Ondo I LP, the entity that issues OUSG. The USDC is exchanged for USD and used to purchase short-term treasury ETFs or funds. Yield earned on underlying assets is reinvested to auto-compound.

Flux Finance

Flux Finance is a trustless, overcollateralized lending protocol, forked from Compound V2. It was originally developed by Ondo Finance to act as an onchain Treasury repo marketplace, where KYC’d users can borrow and lend stablecoins.

It supports both permissionless (USDC, USDT, DAI, FRAX) and permissioned (USDY, OUSG) tokens.

MatrixDock

Overview

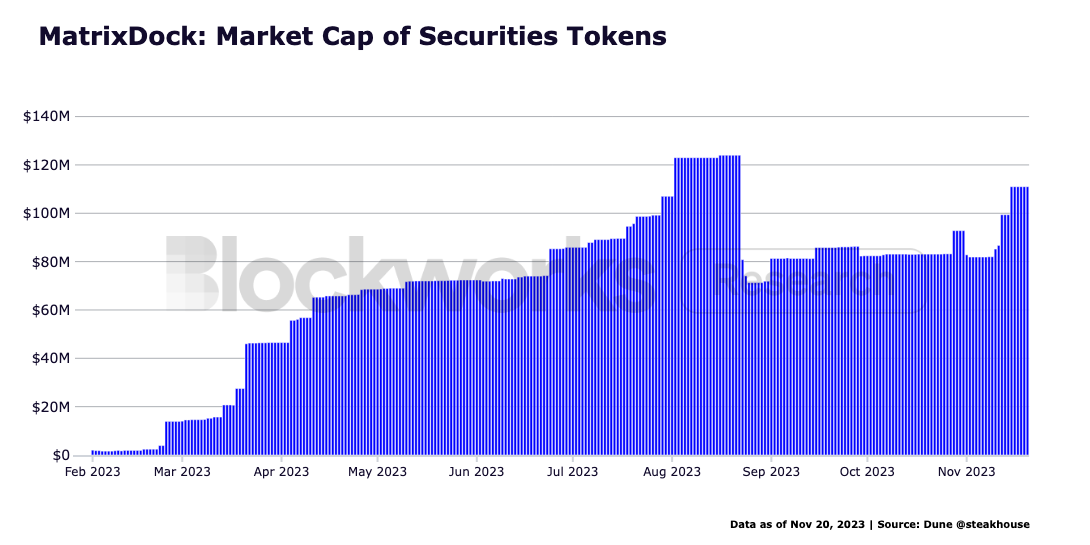

MatrixDock offers Short-term Treasury Bill Token (STBT) for accredited investors who are interested in T-bill yields. STBT, is pegged to 1 USD and backed by US Treasuries with maturities of less than 6 months and reverse repurchase agreements.

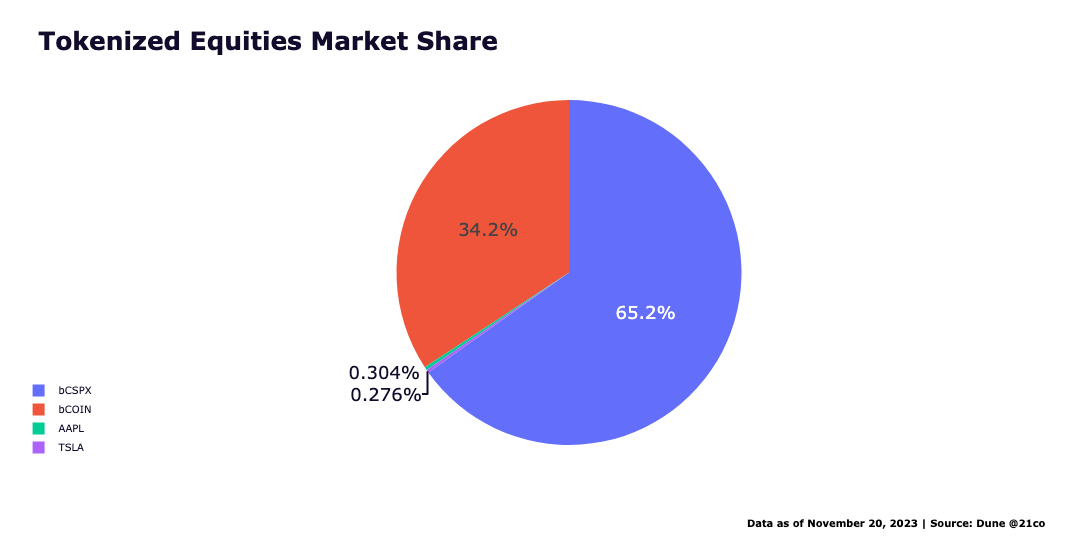

MatrixDock’s STBT currently holds nearly 30% of the market share of tokenized securities onchain, at more than $110M USD market cap.

Mechanics

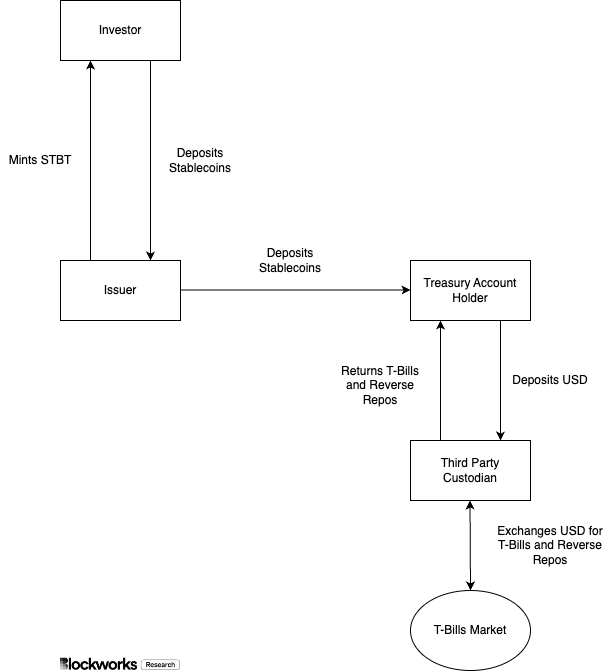

Accredited investors can deposit stablecoins to mint STBT. The stablecoin is received by a Treasury Account Holder, exchanged to USD, and deposited to a third party custodian. The third party custodian exchanges the USD for T-Bills.

Each STBT initially trades at 1 USD, and rebases with the interest accrued on each business day. Additionally, STBT is built using an ERC-1400 token standard.

Tokenized Equity

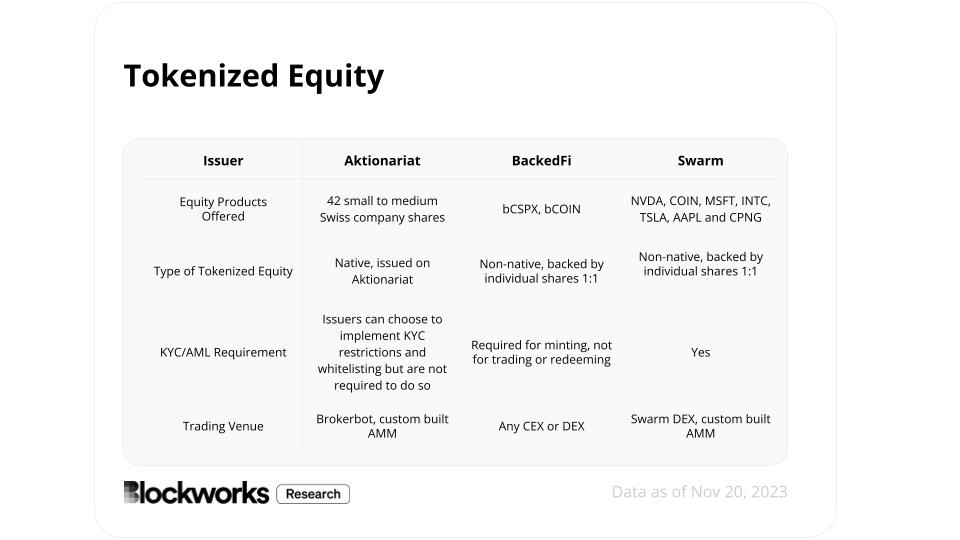

Tokenized equity is one of the least mature tokenized assets. Freely traded tokenized equity is available under Swiss laws, while others implement KYC/AML measures to trade equity.

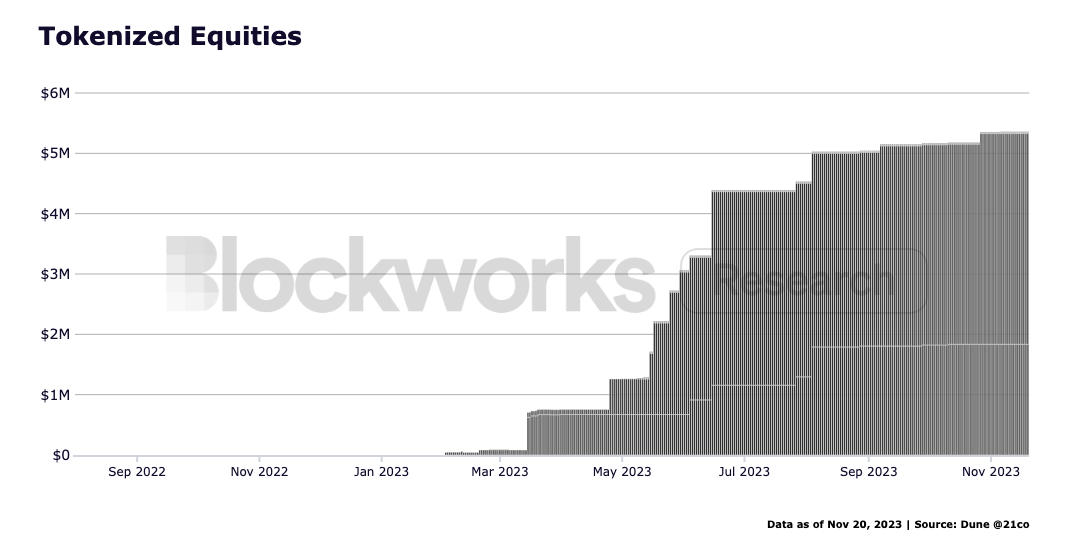

Notably, current adoption of tokenized equity is low and the available offerings are limited. Swarm has little to no usage and Aktionariat only provides access to Swiss small to mid cap equity issuers who decide to issue their shares onchain. Backed Finance, a hybrid tokenized debt and equity provider, has more assets under management compared to Swarm and Aktionariat, but only offers access to the S&P 500 and Coinbase (COIN).

BackedFi’s bCSPX token currently has the highest market cap amongst tokenized equities across DeFi, at $3.5M USD, likely due to Swarm and Aktionariat’s implementations not being particularly efficient. Swarm requires users to fully KYC to trade stocks, which disincentivizes many retail participants that may not value the benefits of tokenized equity as much as they value their privacy. Aktionariat does not necessarily require KYC and instead passes off the responsibility to issuers. Unfortunately, tokenized equity offered on Aktionariat is not attractive, since it comprises mostly of small to medium Swiss company shares. They are able to offer shares, which have the same rights as offchain shares, natively, thanks to the Swiss DLT Act which allows shares to be issued if permitted by the company to which the shares belong to. Unfortunately, as this law only applies to Swiss companies who permit to their shares being issued, their selection is limited, and the demand for their limited selection is low.

BackedFi follows a similar structure to tokenized stablecoins in how they implement tokenized equity. Only KYC’d users are able to mint Backed Tokens, but these tokens are freely transferable and redeemable by retail users. BackedFi offers more interesting, large cap stocks compared to Aktionariat, which are likely the reason that the platform is more popular compared to competitors.

We expect this trend to revert, and for tokenized equity to become more widely available onchain (depending on regulation), albeit likely without much usage. As the market environment shifts more risk on, providers may try and capture some stock trading volume onchain through tokenization. Their use case and product market fit is similar to that of tokenized debt: it aims to attract participants who may not have reliable access to foreign equity markets -- which tokenized equity can fix by offering cheaper access and lower fees. However, like tokenized debt, tokenized stock growth will depend on demand from funds and retail participants, who may not have demand for foreign equity, or may choose to use traditional financial rails due to convenience - despite the potential efficiencies and lower fees that come with tokenized equities.

Aside from traditional financial rails, tokenized equity also competes with synthetic stock trading platforms that track stock prices using oracles and are purely synthetic derivative products.

These synthetic products are strong competitors to tokenized equity products as earning yield is not as significant for tokenized equity as it is for tokenized debt. Additionally, the rights of tokenized equity holders have not matured as quickly as for tokenized debt holders. While tokenized debt holders receive the yield from underlying assets, current tokenized equity products do not distribute dividends, or allow for voting rights (aside from shares listed on Aktionariat - which are able to vote since they were issued onchain). Therefore, tokenized equity is much more susceptible to being used only for speculation, which is where synthetic products shine, since they have less regulatory complexity and allow for leverage.

The two biggest synthetic stock providers were FTX and Mirror (which had just over $2B in TVL at its peak before the implosion of the Terra ecosystem).

Aktionariat

Overview

Aktionariat is a tokenized equity protocol, which offers tokenized Swiss shares, with the same rights and obligations as traditional shares. Aktionariat currently offers 42 shares which can be traded on their platform. Shares offered were issued on Aktionariat by their respective companies.

Issuers can choose to implement KYC restrictions and whitelisting but are not forced to do so. Shareholders have no legal obligation to register unless their percent of share capital exceeds 25%.

Aktionariat currently has only $25M USD in total value locked. The shares traded on Aktionariat are small to medium Swiss companies that are able to access a broader demographic of investors and more capital through Aktionariat. The highest market cap for a share on Aktionariat is DAKS, Aktionariat’s own share, at $10.32M.

Mechanics

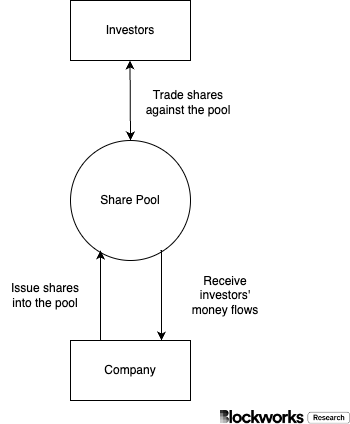

Aktionariat uses Brokerbot, a custom built AMM for the trading of shares. Brokerbot has two sets of functions: functions for investors to buy or sell tokens, and functions for issuers to manage their Brokerbot.

The most important difference between Brokerbot and other AMM designs is that Brokerbot is built under the assumption that all liquidity is provided by the issuer (the company). Companies who issue their shares through Aktionariat can hold up to 10% of their own shares, which can also be purchased by investors.

When a purchase is made, the investor's money flows to the Company, and they receive back shares. Issuers set the initial price and price adjustment (for both sales and purchases) of shares. For example, if the price is set to 10.00 CHF and the price adjustment is set to 0.05 CHF per share, buying 10 shares would push the price to 10.50 CHF, with the buyer having to pay 10.25 CHF on average. If an investor were to sell 5 shares while the price is 10.50 CHF, they would push the price down to 10.50 CHF, and would receive 10.75 CHF on average. When an investor sells shares through a Brokerbot, they are selling it back to the company, and receiving money from the liquidity pool.

Swarm

Overview

Swarm is a permissioned DeFi protocol which allows users to trade tokenized stocks and bonds onchain.

Despite their limited listings, Swarm is one of the only protocols that offers trading on large cap tokenized equities, including NVDA, COIN, MSFT, INTC, TSLA, AAPL, and more. However, Swarm still suffers from very limited volume and usage. Its two most popular stocks, AAPL and TSLA, have $30K USD in combined market cap.

Mechanics

The Swarm DEX is a fork of Balancer. It functions similarly to a traditional AMM, with one important change, compliance wrappers. Similarly to traditional AMMs, traders trade against a liquidity pool, while liquidity providers provide liquidity in exchange for SPT (Swarm Pool Tokens) to earn trading fees.

Swarm implements compliance wrappers so that only qualified users and digital assets can be traded on their DEX. Both liquidity providers and traders must verify their identity to ensure KYC/AML compliance. Users need to link their wallet to their identity and provide verification through their biometrics and documents.

Tokenomics

SMT is the native token of Swarm. SMT is a payment token on Ethereum, and is used for fee payments and rewards. Traders can get up to 50% in reduced protocol fees if they pay using SMT, while liquidity providers can earn SMT tokens for providing liquidity.

BackedFi

BackedFi offers composable, tokenized securities which track bonds, stocks or ETFs. Each Backed Token is backed 1:1 by the underlying asset and held by third party custodians. Backed Tokens are freely transferable ERC-20 tokens composable with DeFi protocols, and are ledger-based securities under Swiss law.

BackedFi’s products currently include:

- bIB01: Backed Assets Treasury Bond 0-1yr (USD)

- bIBTA: Backed Assets Treasury Bond 1-3yr (USD)

- bHIGH: Backed Assets High Yield Corp Bond (EUR)

- bGOVIES: 0 to 6 months Euro Investment Grade Bonds (EUR)

- bCSPX: Backed Assets Core S&P 500

- bCOIN: Backed Assets Coinbase Stock

Mechanics

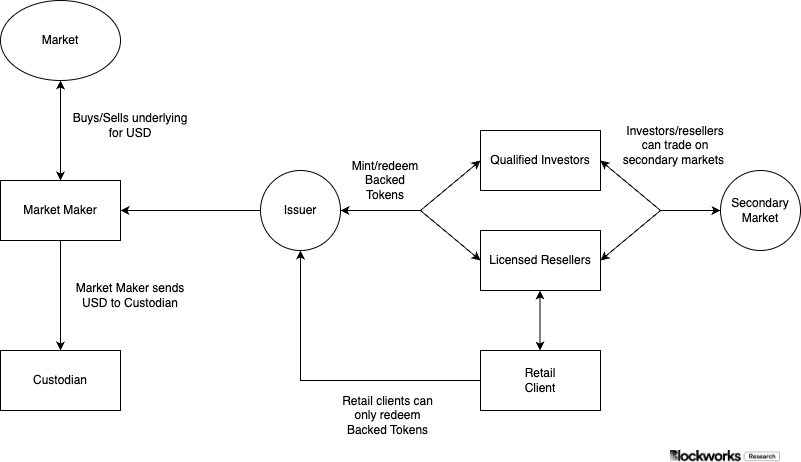

Qualified investors can purchase Backed tokens using USDC by sending USDC to a unique deposit address of the issuer of their desired Backed token. The issuer will convert the USDC to USD through market-makers. USD proceeds are custodied at Maerki Baumann & Co. AG, a Swiss private bank. The custodian purchases the underlying securities using the fiat received.

Backed tokens can only be bought directly from BackedFi (issuers) by qualified investors and licensed resellers to ensure KYC/AML compliance. Backed tokens can be sold to retail investors and on secondary markets.

Real Estate

Tokenized real estate products have over $110M USD in assets under management onchain, and is the only tokenized asset class where the majority of liquidity and assets are not on Ethereum, but instead on Gnosis.

Tokenization and fractionalization of real estate unlock retail investment in traditionally exclusive asset classes by splitting high-ticket, illiquid assets into affordable, tradable units. Additionally, protocols like Real T and Tangible improve transaction speed, for a typically slow process such as buying real estate -- as working with documents, approval procedures, and third party intermediaries can take up to 12 weeks.

Adoption for tokenized real estate is still low. Similarly to tokenized equity, its growth depends on markets becoming more risk on. Its growth is also threatened by synthetic real estate derivatives onchain, such as Parcl, who may capture more volume due to higher liquidity and more users due to incentivization programs.

Further, users interested in tokenized real estate may not be attracted by yield (from rent payments) but rather price speculation, in which case synthetic real estate derivatives outshine, since they allow leverage and are less complicated legally. Regulation for tokenized real estate is immature and therefore complications may arise due to non-enforceability.

RealT

Overview

RealT offers users tokenized investments in real estate, as well as protocols which enable swapping, borrowing, and lending tokenized real estate.

Ownership of real estate properties and their paper deeds are represented by tokens on Gnosis and Ethereum. Each token costs between $50 to $150 USD. Tokens are revalued once a year and rent is distributed to token holders every week. Rent can be received in the form of USDC on Ethereum and USDC or xDAI on Gnosis. Users will have to pay gas on Ethereum but are airdropped on Gnosis.

RealT operates under Real Token Inc., which is registered in Delaware. RealT has also separately created the entity Real Token LLC, to serve as an umbrella company. Since each property token is considered a securities offering, Real Token LLC established one private placement memorandum as an attempt to cover all offerings rather than separate documents. This umbrella structure aims to minimize legal costs and complexities when issuing new property tokens. RealT tokens are sold to US Accredited Investors and to non-US persons.

Mechanics

Each property deed is owned by a specific single-purpose LLC or Inc. Tokens on the RealT website represent ownership in the LLC or Inc. that holds the deed, and therefore the property. Property management is outsourced to local professionals.

Users can buy RealT tokens which represent properties on the primary market (the RealT site), or on the secondary market (various DEXs).

To buy property on the RealT site, users must first register and go through KYC/AML checks. They can then choose to buy property from the RealT site. Once a buy is initiated, users will receive a contract which they will have to sign. After the contract is signed, users receive their RealT tokens.

On the secondary market, users can buy RealT tokens, if they have first been whitelisted for the property (i.e. if they have gone through KYC/AML checks).

In addition to RealT tokens, RealT has built YAM and RMM:

- RMM is a lending and borrowing platform, forked from Aave V2. Lenders are able to earn interest on their RealT tokens while providing liquidity for borrowers.

- YAM is a decentralized exchange forked from SwapCat, where users can buy and sell RealT tokens. RealT tokens can also be bought and sold on LevinSwap and Uniswap (although liquidity is limited).

Tangible

Overview

Tangible offers a product suite which allows users to buy and sell real estate, wines, watches and gold. Tangible uses Real USD (a stablecoin backed real estate) to offer users access to tokenized and fractionalized RWAs. Notably, USDR recently depegged, following an exploit which drained its collateral DAI reserves.

Mechanics

Tangible allows users to purchase physical goods using Real USD. When an asset is purchased off Tangible, a TNFT is minted to the buyer's wallet, which represents ownership of the physical item. TNFT's are transferable, and can be sold on the open market.

Real Estate

Properties on Tangible are held in a local Special Purpose Vehicle, (SPV) a legal entity created solely for this purpose.

TNFT holders have beneficial ownership to the SPV, either in full or fraction. All properties are leased and rental yield is paid to the TNFT holder(s) in USDC.

Tangible Custody collects rent from the tenants, and pays the rent to the Tangible DAO. Rental yield is distributed from the Tangible DAO to TNFT owners (excluding the management fee and insurance costs). Fractionalized TNFT rental yield is split proportionally.

Wines

Tangible Custody uses Bordeaux Index as a service provider for wines on Tangible. Wine bottles are stored by Octavian, in a storage facility in England. Tangible customers pay $16 USD per year for 6 to 12 bottles at the facility.

Watches

The process for watches is similar to that of wines. Tangible works with Loomis International to store watches in London. Tangible users pay 2% of the watch's value at time of storage purchase per year.

RWA Adoption: HIRP Phenomenon or A New Regime?

The current high-rate environment has likely led to the growth boom in RWAs and the emergence of tokenized financial assets such as sovereign bonds, money market funds, and repurchase agreements. The Federal Reserve has hiked rates by 525 bps since March 2022, as part of the quantitative tightening cycle, and these rate hikes are the first rate hikes since 2018. Comparatively, in 2017 and 2018, the Fed had hiked rates only by 175 bps at a much slower pace than the current hiking cycle.

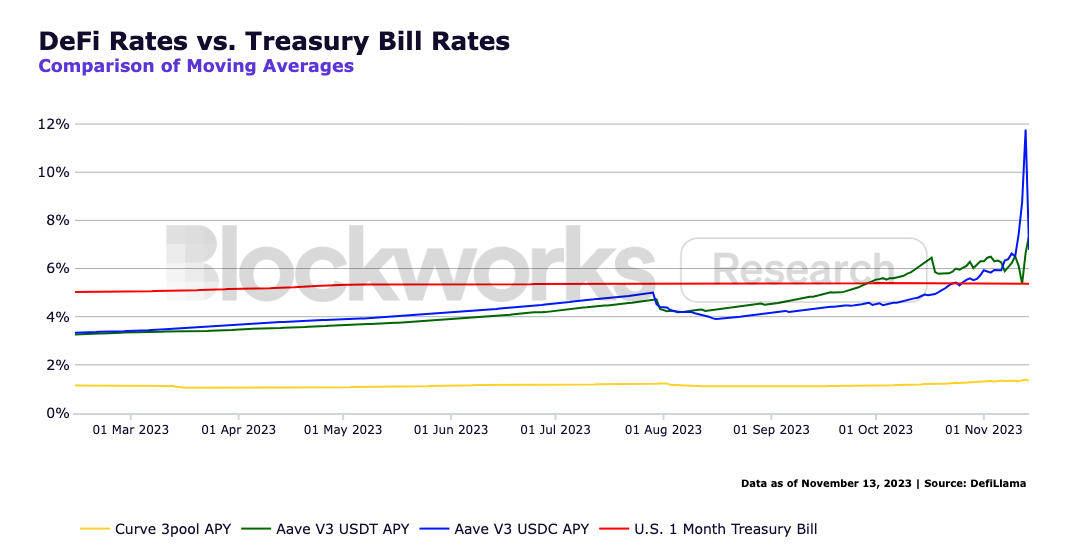

In addition to the high-rate environment, DeFi rates plummeted across the board following the collapse of Anchor and Luna and the subsequent decrease in demand for leverage across crypto. Therefore, unlike in 2017, the current cycle of RWA adoption has been spearheaded by treasury bonds and bills, which have garnered increased demand and inflow of capital due to the higher yield. The “safest” method to generate income onchain has been depositing into money markets (such as Aave) or providing liquidity for stablecoin pairs at unusually low rates – both of which yielded lower than the US T-bill rate up until September 2023. Additionally, compared to the US T-bill rate, chasing yield onchain is evidently much riskier due to smart contract risks, which can lead to drainage of funds and infinite mint attacks, which can lead to total loss of value. Even bluechip protocols come with significant risk: for example, Curve Finance faced a reentrancy exploit on July 30th, and Aave recently found a critical bug that could have led to the loss of funds.

However, the rapid growth of RWA adoption can be attributed to several factors beyond the high-rate environment as well. The development of the broader crypto ecosystem has played a significant role. As more institutional money and more sophisticated participants have entered, and the tech stack has been battle-tested over years, blockchain technology has become increasingly attractive and acceptable. Institutions are increasingly drawn to the potential efficiencies offered by tokenization - and are comfortable with the technology behind it. Additionally, another influential factor has been the adoption of stablecoins by participants in emerging markets for their daily payment and banking needs.

Notably, the rise in RWA adoption isn't solely driven by crypto native participants. It has surged because it appeals to a different, wider demographic as well, including TradFi participants and retail investors in emerging markets. Typically, crypto has attracted a relatively small group of people with interest in a niche financial market who have a somewhat strong tech background. The appeal to TradFi and emerging market retail investors introduces a new avenue for growth, potentially expanding the overall market significantly.

Institutional Adoption: Seeking Liquidity, Fractionalization and Improved Transaction Times

The efficiencies that tokenization offers could lead to institutional adoption. Tokenization can reduce transaction times: smart contracts have predefined functions that are triggered and can instantly complete transactions and reduce settlement times. In addition, tokenization allows for 24/7 trading and transactions, unlike traditional finance, which has comparatively restrictive trading hours.

Kevin Miao, Head of BlockTower Credit, gives a strong illustration of how tokenization can make securitization processes more efficient, in his article Everything is Broken.

In traditional finance, the process of securitization requires many intermediaries: custodial agents track loan performance, calculation agents determine payouts, paying agents debit the securitizations bank account, DTCC distributes payments, prime brokers pay investors, auditors review the entire process, trustees aggregate monthly reports. Smart contracts and tokenization remove most of these intermediaries, instead simplifying the process: NFTs track payments and terms of the loan, smart contracts calculate and distribute payments.

Additionally, since blockchains provide an immutable audit trail, as transactions are ledgered onchain with chronological timestamps, auditing is simplified and auditing costs are lowered. According to an estimate by Figure Technologies the collective benefit of onchain securitization to parties over the lifecycle of a loan is over 100 basis points. Additionally, according to the IMF’s 2022 Global Financial Stability Report, DeFi’s approach to financial markets can lead to large cost savings due to lower labor and operational costs, since complex intermediary systems in traditional financial systems can be replaced by a public ledger and automated smart contracts.

One of the largest benefits of tokenization is increased fractionalization. In traditional financial systems, there is a limit to how much an asset can be fractionalized. However, when an asset is tokenized, this limitation is removed, and users can own and trade tokens representing fractions of ownership.

This is particularly beneficial for assets that are illiquid. Pooling assets can reduce costs, especially in developing countries with a lack of securitization infrastructure. Additionally, pooling assets can increase liquidity. RWAs are often illiquid and can have long maturities, which can make investing difficult as investors do not always want to hold all the way to maturity, and in the current paradigm, have no liquidity to exit early if they wish to do so. By pooling multiple assets together, investors can provide financing for a pool instead of individual assets.

Pooling multiple assets together would also change risk profiles for these assets. Similarly to how securitization works in traditional banking, combining different tokenized assets into a single stream of income could mitigate the risk of default, therefore making it easier to sell products and tap into more buyers. For example, even though Sovereign bonds and treasuries can be liquidated immediately offchain, small- to medium-sized bonds can be illiquid. Pooling tokenized assets would improve liquidity for these bonds.

Retail Adoption: Emerging Markets and Broader Access

Broadening access to DeFi through tokenization encourages capital inflows from new retail participants, especially those in emerging markets. For emerging market participants, tokenized assets grant access to US debt and equity that they otherwise are not able to access - at least without high costs. For example, Interactive Brokers charges commission fees, electronic communication network and/or specialist fees, regulatory fees, clearing fees, exchange fees and pass-through fees - many of which are paid to intermediaries, who can be cut out using smart contracts.

Cheap and broad access to tokenized assets is particularly important for retail participants from emerging markets. According to Consensys’ The State of Web3 Perception Around The World report, participants from emerging markets, such as Brazil, Argentina, Mexico, Philippines, and Nigeria are more likely to view cryptocurrencies as the “future of money”. Access to stablecoins (particularly US Dollars) is particularly important in certain countries, where citizens may choose to use stablecoins to combat inflation, have access to their savings, or to seek safety incase as there is geopolitical instability in their region or country. Similar to stablecoins drawing in both crypto native participants who seek to reduce market risks and individuals from high-inflation economies, tokenized securities broaden DeFi participation beyond a niche group of participants.

Investing offchain is less affordable due to high ticket sizes for certain asset types, such as fine art and real estate. For example, in recent years, there has been a notable rise in real estate prices, making them inaccessible for many retail investors. Notably, between 2012 and the second quarter of 2023, the average value of US real estate surged by 131%. Fractionalization, enabled by tokenization, can allow retail to gain exposure to asset classes, such as real estate, with high barriers to entry - leading to a new set of investors gaining access to diversify their investment portfolios into asset classes they were previously unable to invest in.

DeFi Adoption: How RWAs Can Transform DeFi

In traditional finance, RWAs are a valuable form of collateral for loans. Similarly, crypto protocols want to bring these same advantages to DeFi. Products like tokenized treasuries, stocks, and loans can help grow DeFi, by attracting new capital and users, if they are built to be interoperable with DeFi infrastructure. By replicating traditional opportunities onchain, RWAs bring real world yields to DeFi, and appeal to those who want the benefits of DeFi (decentralization, anonymity, transparency) without certain risks (unbacked assets, “fake” yield).

Additionally, rising risk-free rates should affect lending markets, as investors expect certain returns over time. As risk-free rates rise, DeFi interest rates should also be higher to remain competitive. The risk-free rate sets a hurdle that DeFi markets must exceed to justify additional smart contract and protocol risks. Unfortunately, this has not been the case thus far, as funds often have allocation restrictions, and it is costly and cumbersome to move between chains.

RWAs also benefit protocol treasury management and support ecosystem maturity. In bull markets, protocol treasuries grow quite significantly, while in the bear market, protocols want yield to grow reserves. Currently, they often buy governance tokens and lock for low yield, concentrating price risk, or take on smart contract risk while earning low yield on bluechip protocols.

Often governance tokens move similarly to ETH and BTC. In bear markets, due to high correlation between assets, protocol treasuries lose significant value, which affects operations. RWAs provide uncorrelated yields to offset volatility and sustain growth. However, this would require protocol treasuries diversifying into stablecoins away from crypto-native assets, something that many large protocols have not managed to do successfully.

Adoption Risks

RWAs and tokenization come with many risks for adoption:

- Regulatory risks: Compliance and legality of asset tokenization varies greatly from jurisdiction to jurisdiction, and is still immature. This can lead to ownership, liquidation, and backing disputes, since there is no standardized tokenization framework and legal recourse.

- Counterparty risks: Tokenized assets need to be custodied, which leads to redemption risks. Assets which are tokenized may not be claimed by users if the storage and protection of assets are not handled properly. RWA lending protocols are particularly at risk, since they are susceptible to bad debt if they’re lending to offchain entities.

- Smart contract and technical risks: Smart contracts carry risk and can result in total loss of funds.

- Lack of standardization: Tokenized assets may see lower levels of adoption due to illiquidity if there is a lack of standardization in tokenization protocols and structures, leading to a lack of interoperability. However, there is significant work being done on this front with something such as the ERC-4626 tokenized vault standard.

Additionally, one important risk to consider is that the current set of RWAs were a high interest rate phenomenon. As markets become more risk on, or as interest rates come down, tokenized debt protocols may not continue to do as well, since retail participants will be interested in higher returns. In this case, it will be important to see if more risk on RWAs, such as tokenized stocks, real estate or fine art, become popular.

Final Thoughts

Tokenized assets reflect crypto's growth as a legitimate asset class and the adoption of blockchain technology by traditional financial players and markets. They appeal to a different vertical beyond niche crypto circles, by allowing institutions to increase efficiency and lower costs and emerging market retail users to access foreign debt, equity, and currencies. As such, their adoption is likely to continue and develop, even if this growth comes at potentially a relatively slower pace than it has over the past year.

A significant portion of growth for RWAs over the past year has come from tokenized debt instruments and stablecoins. Although it’s easy to dismiss this as a high interest rate phenomenon, tokenized debt will likely continue to grow, as it’s adopted by large institutions and governments, who seek efficiency, liquidity, and more buyers. Adoption of stablecoins will continue to grow, as emerging markets experiencing high inflation rates will continue to drive tokenized USD adoption, and as more onchain use cases emerge. It's likely that stablecoins that share yield with users from their collateral assets (sDAI, stUSDT, sFRAX, USDY) will have increased adoption with retail participants - over traditional stablecoins, such as USDC and USDT. Tokenized commodities have the second highest rate of adoption amongst tokenized assets, and work similarly to traditional tokenized stablecoins. Gold is by far the most popular tokenized commodity, however, efforts have begun to diversify the range of commodities available on-chain. Initiatives like tokenizing uranium aim to introduce a more extensive variety of commodities onchain, and we are likely to see tokenization of more popular commodities like oil, natural gas, lithium, etc. Adoption levels for these will likely be low and they will be difficult to implement due to regulatory complexity.

A risk on market regime could potentially lead to increased demand for tokenized equities and tokenized real estate. Tokenized equities and real estate have important use cases. Tokenized equities, like tokenized debt, appeal to emerging market retail participants, who seek cheaper access to large cap stocks. Tokenized real estate could be an ideal fit for retail who are not able to afford illiquid assets with high ticket sizes. However, they also come with significant adoption risk, due to more complex regulatory requirements. Additionally, synthetic stocks are strong competitors to tokenized equity, given that ownership of the underlying asset is not necessary (in contrast to how it is with tokenized debt) since demand mainly comes from speculation. Adoption will likely be slower than adoption has been for tokenized debt, which was accelerated by high rates. However, it’s likely that over the next 2 to 3 years protocols who offer tokenized debt will also build towards offering tokenized equity, and that newer protocols and products will be built following wider spread adoption of tokenized assets onchain. Adoption may be low for these products over the next few years, but in the long run, significant adoption of tokenized equities and real estate are likely to be made, especially for settlement processes, if regulatory clarity is achieved.