A Game of Volatility

Key Takeaways

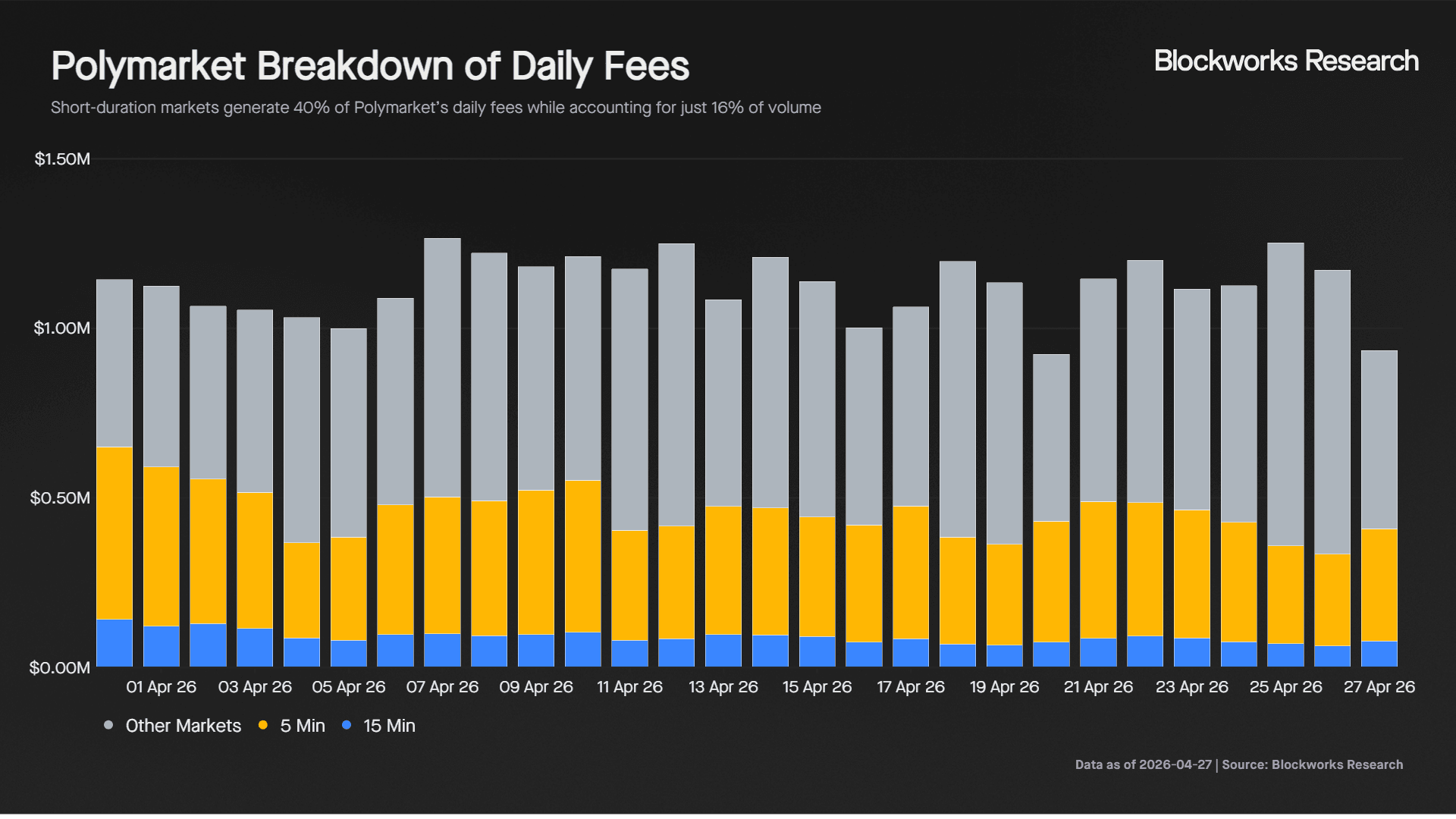

- Short duration markets have become a major driver of Polymarket activity. 5min and 15min crypto markets now account for roughly 16% of total Polymarket volume, while generating nearly 40% of the platform’s daily fees at around $400K per day.

- Retail traders are increasingly gravitating toward shorter duration products. 5min markets rapidly took share from 15min markets in the same way 15min markets displaced hourly products, reinforcing that users prefer volatility and faster feedback loops over predictability.

- Profits in these markets are highly concentrated among professional algorithmic traders. In 15min markets, just 19 addresses generated $11.4M in profits with every address profitable, while the average engaged retail trader lost roughly -$534. Similar patterns have already emerged in 5min markets despite their recent launch.

- Professional traders consistently rely on market neutral and latency sensitive strategies. High frequency paired YES/NO positioning, maker dominant execution and arbitrage focused trading allow professionals to systematically extract small edges while minimizing directional exposure.

- Volatility has become the product. Retail traders continue participating despite negative expected returns because short duration markets compress the possibility of outsized gains into extremely small timeframes.

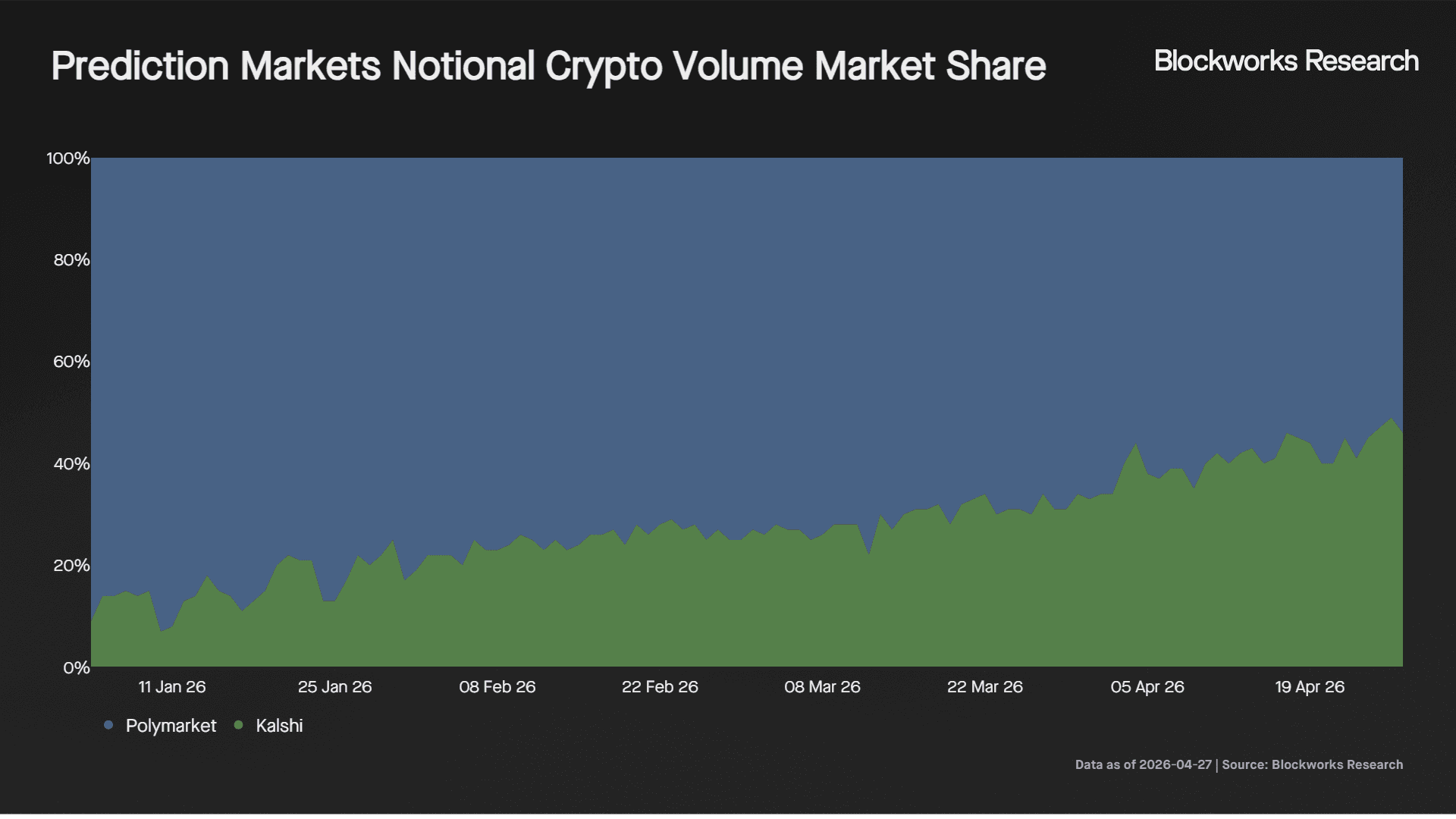

- Competition in short duration prediction markets is accelerating rapidly. Kalshi’s crypto market share has risen from 9% to 46% since the start of the year, while Hyperliquid is preparing to launch competing products.

- Product and distribution will determine the winner. Maintaining leadership will likely require Polymarket to improve execution speed, deepen liquidity and refine order mechanics for market makers. A more gamified user experience alongside expansion into TradFi markets could also materially broaden the platform’s retail audience.

Introduction

Prediction markets are increasingly becoming a game of volatility rather than prediction. On Polymarket, short duration 5min and 15min up/down crypto markets have quietly become one of the platform’s largest drivers of volume and fee generation.

Retail traders are drawn to these markets for the same reason traders flock to memecoins, leveraged perpetuals and gacha mechanics. The shorter the duration, the sharper the price swings and the greater the potential to quickly multiply capital. Beneath the surface, however, these markets are increasingly dominated by professional algorithmic traders running latency sensitive and market neutral strategies at scale.

This dynamic has created one of the most active and monetizable segments across prediction markets. In this report, I revisit some of the findings from Dune’s recent study on short duration markets and dive deeper into the wallet level behavior, trading strategies and competitive implications driving this rapidly growing category.

Volatility Has Become Polymarket’s Growth Engine

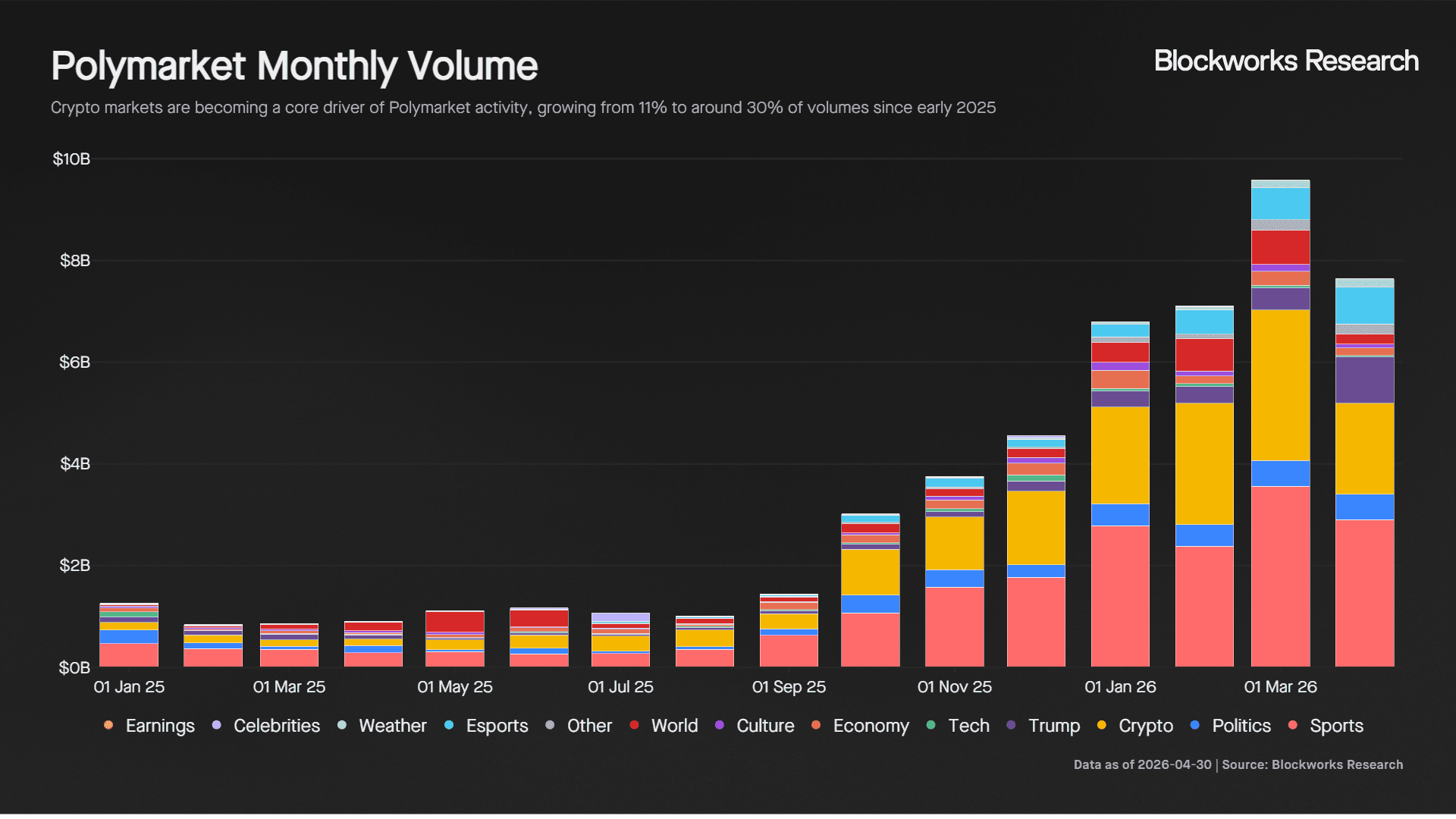

Short duration crypto markets have become one of the largest drivers of activity on Polymarket. Monthly platform volume has grown from $1.4B in September 2025 to a peak of $9.6B in March 2026 before pulling back around 20% in April, marking the first monthly decline in 7 months. Crypto markets have been a major contributor to that growth, expanding from 11% of total platform volume at the start of 2025 to roughly 30% today.

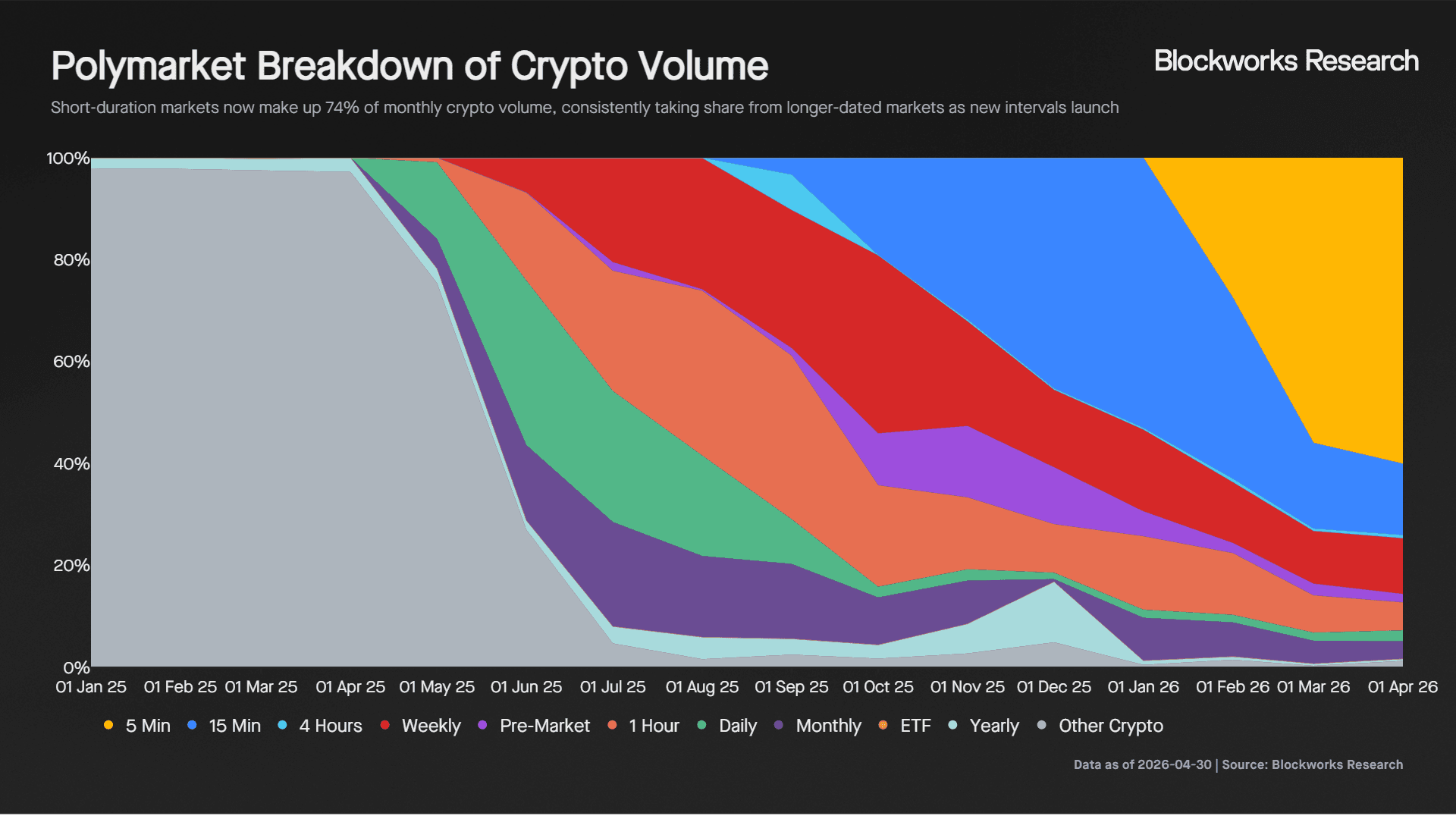

Within crypto, activity has become increasingly concentrated in short duration markets. 5min and 15min up/down markets now account for 74% of monthly crypto market volume. The recent Dune report highlights how dominant BTC markets have become within this segment, with BTC up/down markets alone accounting for 77% of weekly turnover.

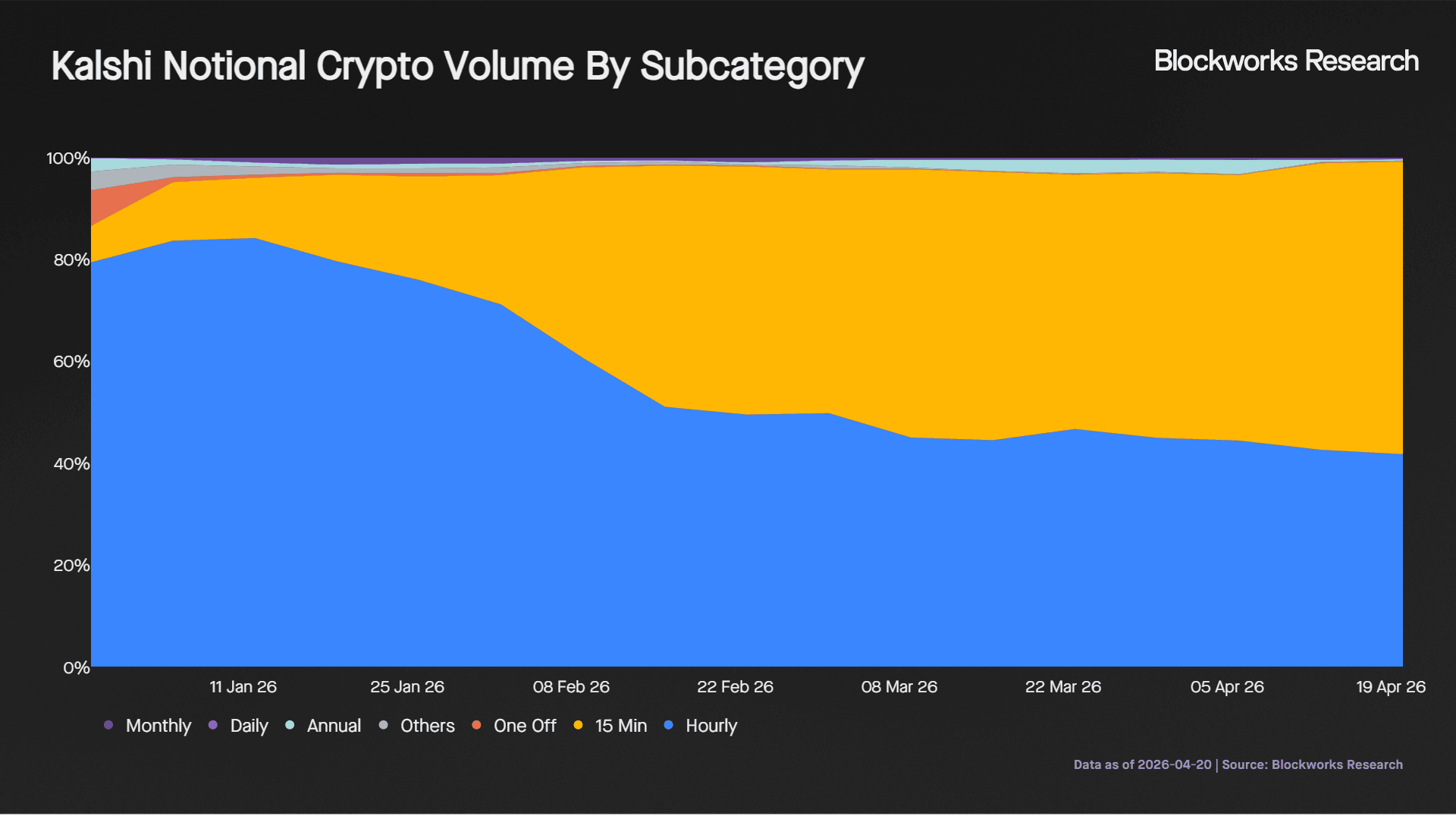

One of the more interesting trends is how each newly introduced shorter duration market rapidly cannibalizes the prior shortest duration product. 5min markets have steadily taken share from 15min markets in the same way 15min markets previously took share from hourly and weekly markets. Rather than seeking predictability, traders appear to prefer volatility and faster feedback loops.

To put this into perspective, 5min and 15min markets now account for roughly 16% of all Polymarket monthly volume. More importantly, these markets monetize exceptionally well. Despite contributing 16% of volume, they generate close to 40% of Polymarket’s daily fees, averaging around $400K in daily fee generation. Crypto markets also carry the platform’s highest effective taker fee rates, around 44% higher than the next highest category.

Retail Provides the Liquidity, Professionals Capture the Edge

Short duration markets are increasingly becoming a transfer of wealth from retail traders to professional algorithmic firms. Retail participants provide the liquidity while professionals systematically extract small but consistent edges through high frequency execution, hedging and market making strategies. The shorter the duration, the more pronounced this dynamic becomes.

As expected, a large share of short duration market activity comes from bots, with the recent Dune report estimating bot participation at 55% for 5min markets and 62% for 15min markets. The more interesting question, however, is who is actually making money.

To analyze this, I split traders into two cohorts. The first consists of addresses with over 1M fills, which are clearly professional algorithmic traders executing at high frequency with small sizing per trade. The second consists of highly engaged retail traders with between 1K and 9.9K fills.

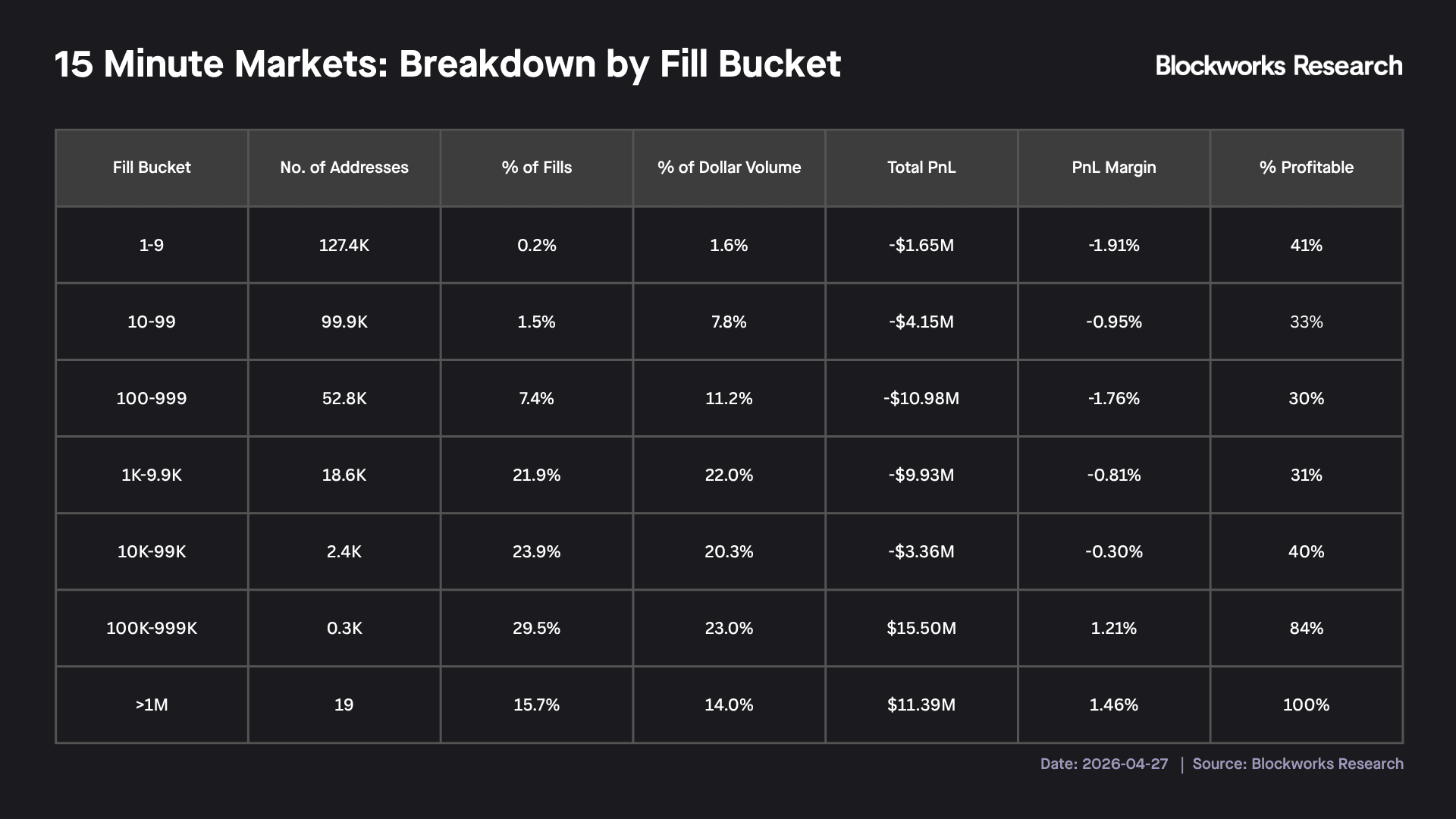

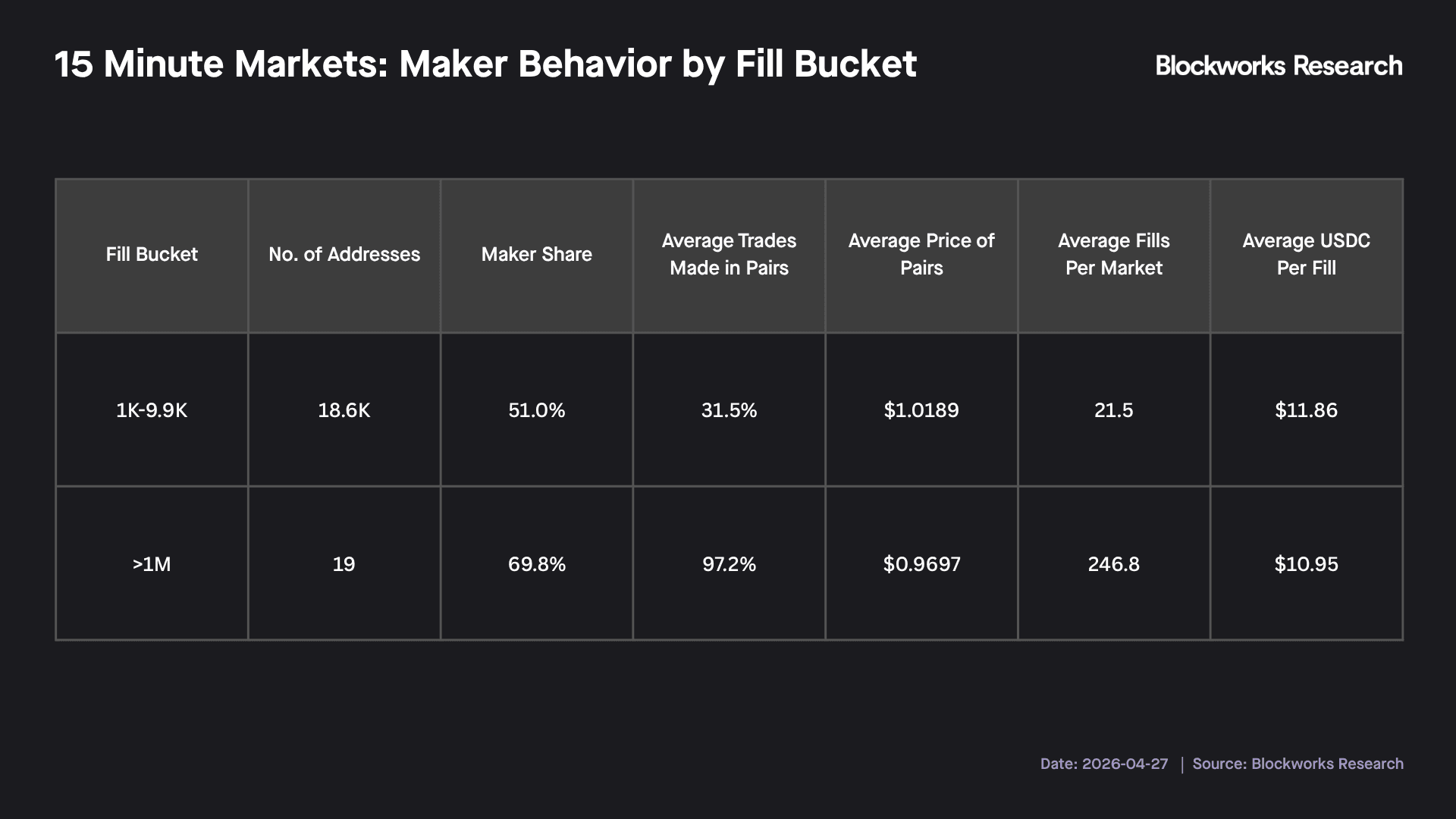

Professionals Dominate the 15min Markets

Despite there being just 19 addresses in the over 1M fills bucket, these traders accounted for 16% of all 15min fills and 14% of total volume. Every address in this cohort was profitable, collectively generating $11.4M in profits with an average margin of 1.46%. Profits in these markets are highly concentrated.

The picture looks materially worse for the engaged retail cohort. Despite contributing 22% of total volume and fills, only 31% of traders were profitable with the cohort posting an average margin of -0.81%. On average, each trader in this group lost roughly $534.

Execution behavior between the two groups differs sharply. Professional traders overwhelmingly trade paired YES and NO positions, with 97.2% of trades involving paired exposure versus just 31.5% for retail traders. Retail participants are far more directional with little hedging taking place. The ability to consistently fill both sides below a combined price of $1 remains one of the core drivers of professional profitability.

Professionals also skew heavily toward maker activity, with maker orders accounting for 70% of fills versus 51% for the retail cohort. This creates another structural edge as maker orders incur no fees on Polymarket. Despite similar average USDC per fill, professionals execute nearly 10x more trades per window than retail traders, extracting extremely small margins at scale.

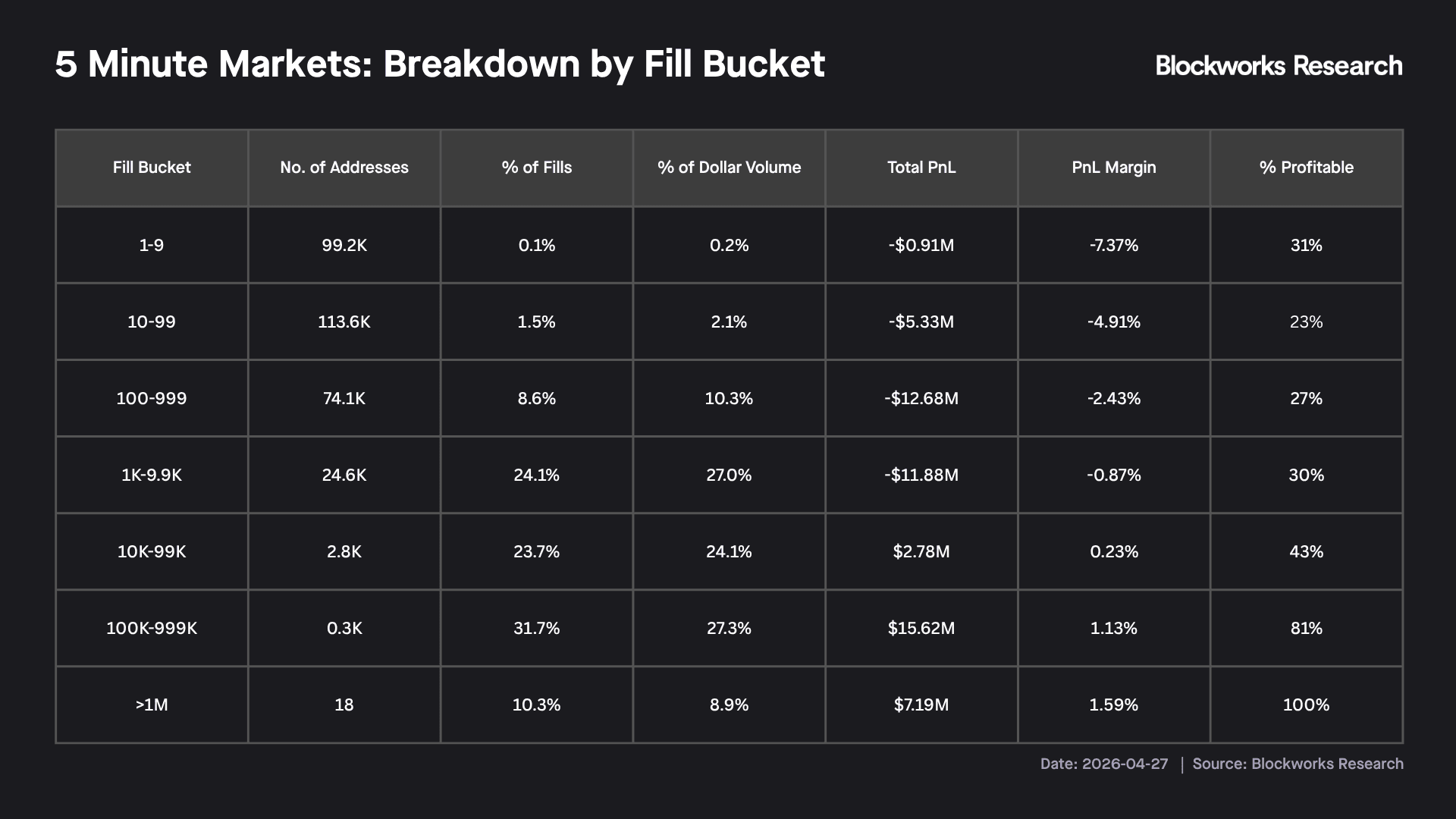

The Same Trend Is Emerging in 5min Markets

Despite launching only in mid-February, 5min markets are already showing similar structural patterns. Many profitable traders identified in the 15min markets have already migrated activity toward shorter duration products. The top 19 addresses from the 15min cohort shifted roughly 25% of their volume into 5min markets during April alone.

The larger shift, however, has come from retail participants. Traders in the 1K-9.9K fills cohort now execute 73% of their activity in 5min markets rather than 15min ones, reinforcing the preference for increasingly shorter duration trading.

The professional cohort in 5min markets remains small but highly profitable. Just 18 addresses were identified with over 1M trades, with 5 of those addresses also appearing in the 15min top bucket. Even so, profitability remains heavily concentrated with 80%-100% of addresses across the top cohorts remaining profitable with margins ranging between 1.1%-1.6%.

Retail performance continues to deteriorate in shorter duration markets. Only around 30% of retail addresses are profitable, with average trader losses in the 1K-9K bucket reaching roughly -$480.

Meanwhile, professionals have benefited materially from the increase in volatility and trading frequency. The top two professional cohorts have already generated $22.8M in profits from 5min markets versus $26.9M in 15min markets despite operating for less than half the time.

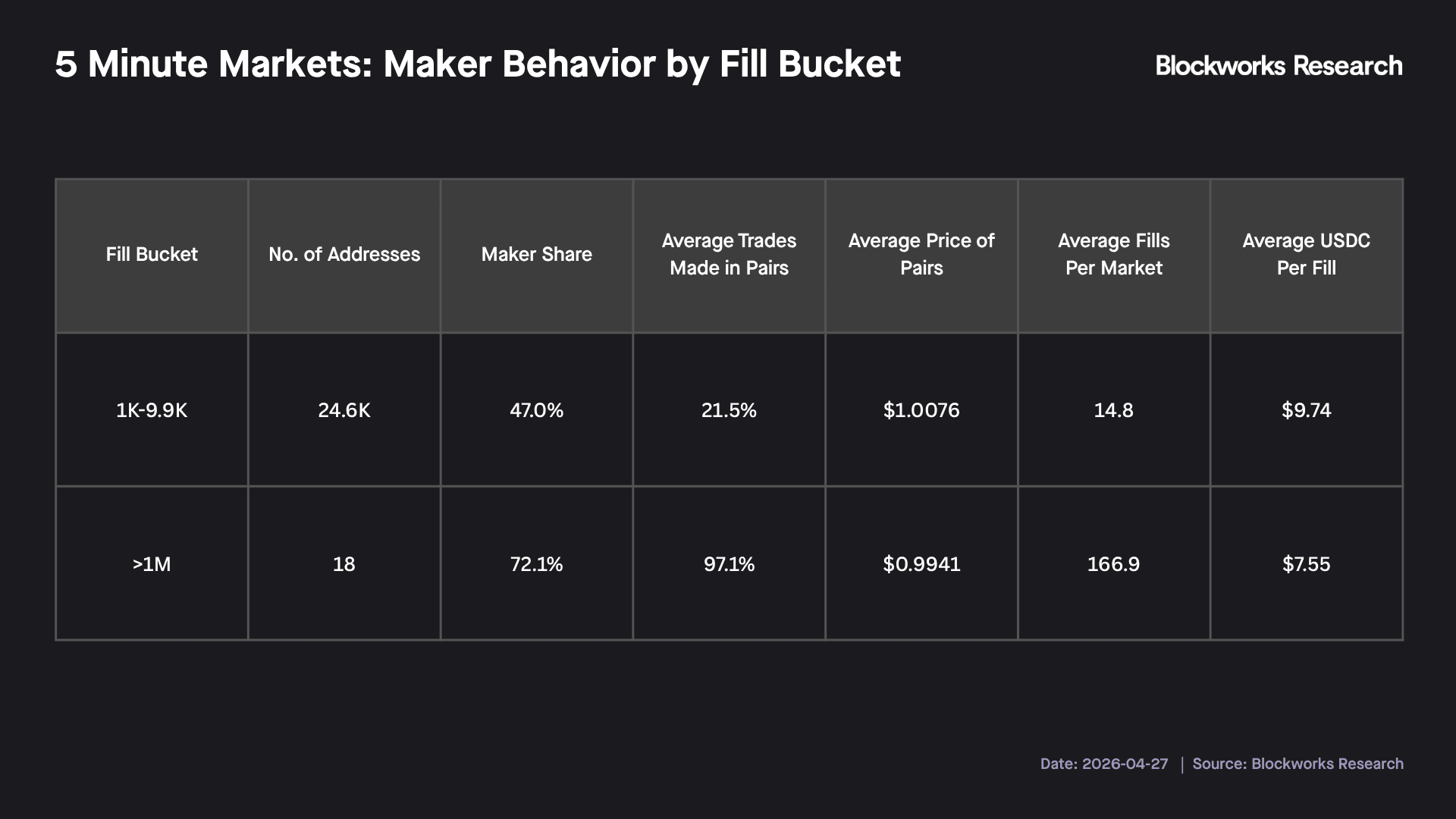

Professionals continue to favor paired YES and NO positioning, though average pair pricing is materially tighter at $0.9941 versus $0.9697 in 15min markets, reflecting increasingly efficient arbitrage conditions and faster repricing. The objective, however, remains the same: consistently extract small arbitrage opportunities while maintaining active hedges to minimize directional exposure.

Professionals also continue to dominate maker activity with maker orders accounting for 72% of fills while maintaining significantly higher trading frequency than retail traders.

Inside the Bot Playbook

The profitability gap between professionals and retail traders raises an obvious question: what exactly are these bots doing that retail traders are unable to replicate, especially now that tools like Claude allow almost anyone to spin up algorithmic strategies?

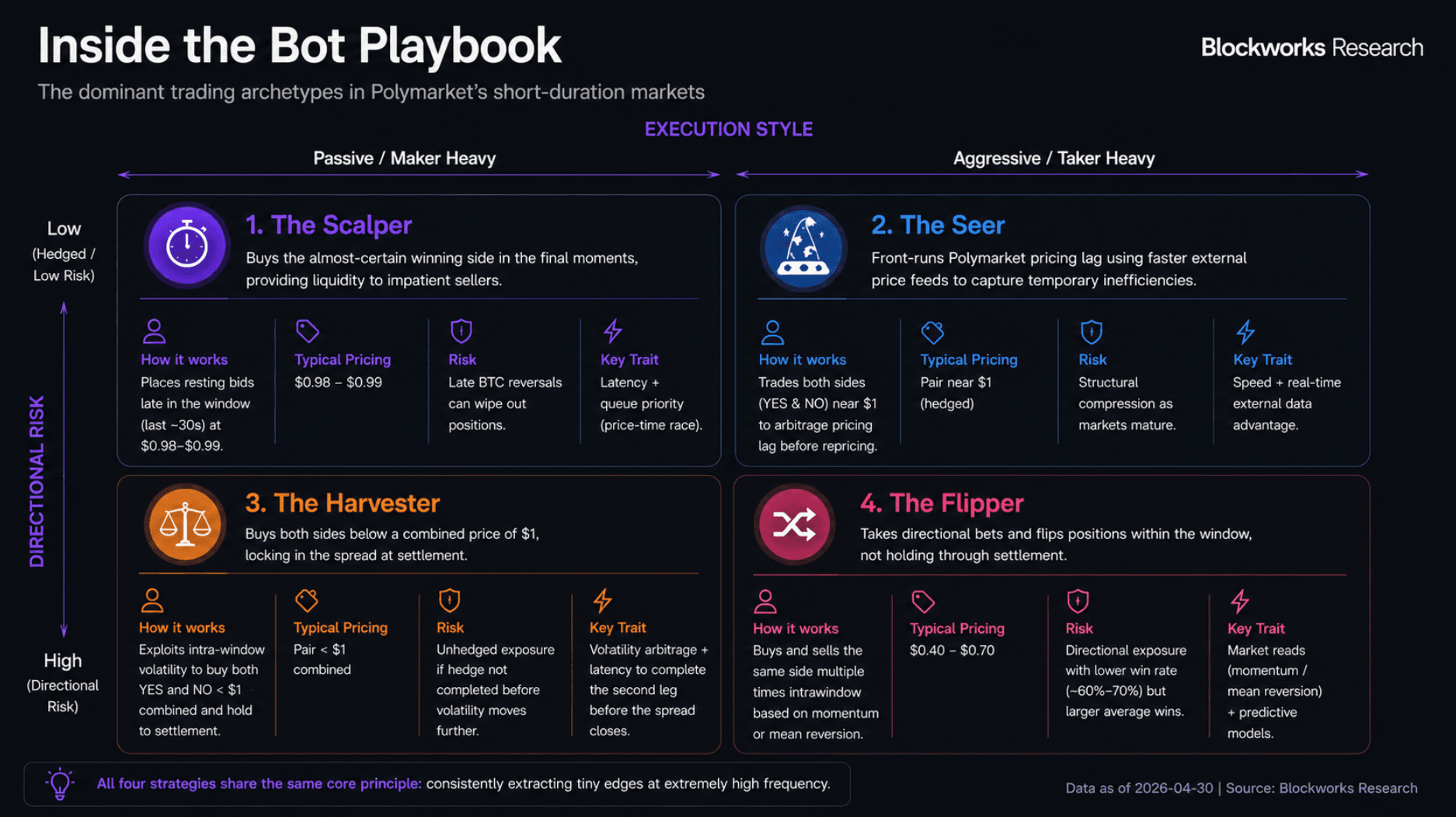

After analyzing the wallets in the top performing cohorts across both the 5min and 15min markets, most profitable activity could broadly be grouped into four strategies. While the execution differs, all four rely on the same core principle: consistently extracting tiny edges at extremely high frequency.

(1) The Scalper:

The Scalper waits until the final moments of a market, often within the last 30 seconds or during the post close settlement lag, before placing resting bids on the side whose outcome is almost fully determined. Average entry prices range between $0.98-$0.99 and are placed almost entirely as maker orders.

The strategy profits from traders on the winning side exiting early to lock in gains or recycle capital rather than waiting for settlement. Margins are extremely thin at roughly $0.01 per share, but the strategy scales because it provides liquidity to a constant stream of impatient winners. Position sizes can exceed $100K in a single market when enough late selling appears.

Their edge comes down to latency. Order priority is price time based, meaning even a slight delay in rebidding materially impacts fill quality. In practice, this has become a race for queue position.

The risk is that BTC can still violently reverse during the final seconds of the window. A $0.99 position can quickly become worthless if the outcome flips late. In one observed example, a trader lost roughly $82K in a single market after building a large position before a sudden reversal. One bad fill can wipe out profits from dozens of successful windows.

(2) The Seer:

The Seer uses faster external price feeds from exchanges such as Binance and Coinbase to front run lag within the Polymarket order book. Depending on urgency, these traders switch between maker and taker orders to capture temporary pricing inefficiencies before the market reprices.

Positions are typically hedged, meaning YES and NO exposure are both purchased within the same window with the combined pair price sitting close to $1. The goal is not directional speculation but small, near riskless arbitrage profits captured repeatedly throughout the day.

Their edge comes from faster external pricing data combined with execution speed.

Their risk is structural rather than directional. These opportunities were significantly larger when short duration markets first launched and order book inefficiencies were more common. As more professional firms entered the market, spreads compressed and the opportunities became increasingly difficult to scale.

(3) The Harvester:

The Harvester exploits sharp intra window BTC volatility to purchase both YES and NO contracts below a combined price of $1, locking in the spread at settlement. This appears to be the most common strategy among profitable traders identified in the cohort data.

These traders lean heavily on maker orders but will cross the spread when needed to complete the second leg of the trade. Multiple pairs are often accumulated within a single window and held through settlement.

Their edge lies in identifying moments where sharp BTC volatility temporarily pushes one side of the market out of line. The trader buys the cheaper leg first, then waits for further price movement to fill the opposite side below a combined price of $1. As volatility swings back and forth intra window, these pricing gaps can briefly appear before quickly closing. In practice, this has become another latency driven game as multiple bots compete to complete the second leg before the spread disappears.

The risk comes when volatility continues moving against the trader before the hedge can be completed. In these situations, traders can become trapped in unhedged directional exposure and are often forced to close at a small loss before the move accelerates further.

(4) The Flipper:

Unlike the previous three archetypes, the Flipper is taking genuine directional risk. These traders buy and sell the same side multiple times within a single market without holding positions through settlement.

The 5min version typically resembles momentum trading. BTC moves sharply higher, YES reprices upward, and the trader buys at $0.55 before exiting at $0.65 minutes later as momentum continues. The 15min version tends to resemble mean reversion trading where sharp moves are faded once pricing appears stretched.

Average entry prices usually range between $0.40-$0.70 with smaller sizing per trade given the higher turnover.

Their edge comes from reading short horizon BTC microstructure such as order flow imbalances, momentum clustering and mean reversion signals faster than the broader market. Unlike the other strategies, these traders rely far more heavily on predictive models rather than pure execution speed.

Their risk profile is materially higher than the other three strategies because they are carrying real directional exposure. Win rates appear lower, likely around 60%-70%, but successful traders compensate through larger average wins relative to losses.

Why Retail Keeps Coming Back

After looking at how professionals approach these markets, the obvious question becomes: why does retail continue participating despite consistently losing money?

The answer comes back to volatility. Short duration markets compress the possibility of large percentage returns into extremely small timeframes. A trader buying YES at $0.50 across 6 consecutive 5min windows could theoretically turn $10 into $640 within 30min. The probability of doing so is extremely low, but the possibility itself is what keeps traders engaged.

This creates the same psychological feedback loop seen in memecoins, leveraged perpetuals and gacha mechanics. Sharp price swings, fast outcomes and the chance to quickly multiply capital create a powerful dopamine effect for retail traders.

That retail flow is ultimately what makes these markets so attractive for professionals. Retail participants provide the volatility and liquidity while algorithmic traders systematically extract small edges through execution speed, hedging and market making strategies.

In many ways, short duration prediction markets are becoming less about prediction and more about trading volatility itself.

Competition for Short Duration Markets Is Heating Up

Polymarket is no longer the only platform aggressively targeting short duration crypto markets. Kalshi’s share of crypto prediction market volume has climbed from 9% at the start of the year to 46% by April 27th, highlighting how quickly competition in the category is intensifying.

Much of Kalshi’s recent growth has come from hourly and 15min crypto markets, products that closely resemble Polymarket’s own offering with similarly competitive fee structures and maker incentives. With Hyperliquid also preparing to launch 15min BTC markets following the introduction of daily BTC contracts, volume fragmentation across platforms is likely to accelerate further.

HIP’s cheaper fee structure could eventually pressure both Polymarket and Kalshi to compress fees, though doing so would be painful given how important short duration markets have become to Polymarket’s overall fee generation.

Where Polymarket Should Go From Here

If Polymarket wants to maintain its lead in short duration markets, it needs to focus on three areas: expanding the number of markets, improving distribution and refining the product experience itself.

More Markets

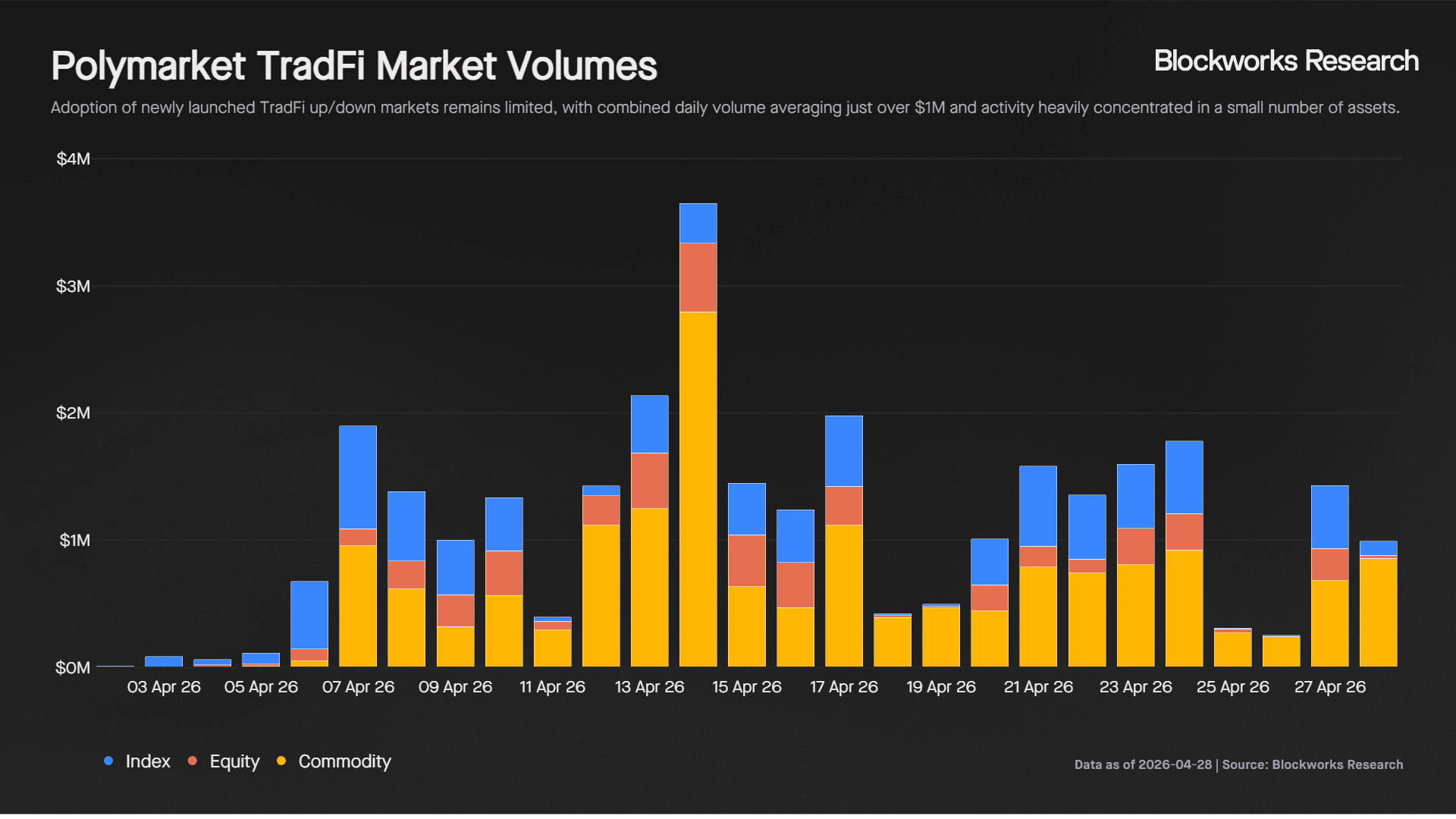

Competition within crypto up/down markets is already becoming crowded, but the broader opportunity extends far beyond BTC. The most obvious adjacent category is TradFi.

Polymarket recently introduced daily close markets for assets such as the S&P 500, Gold, Silver, Oil and several single stock names. So far, traction has remained limited with combined daily volume averaging just over $1M.

Volume is also heavily concentrated. The S&P 500 accounts for roughly 90% of index volume, WTI Crude represents 95% of commodity volume and Mag 7 names drive 62% of single stock activity.

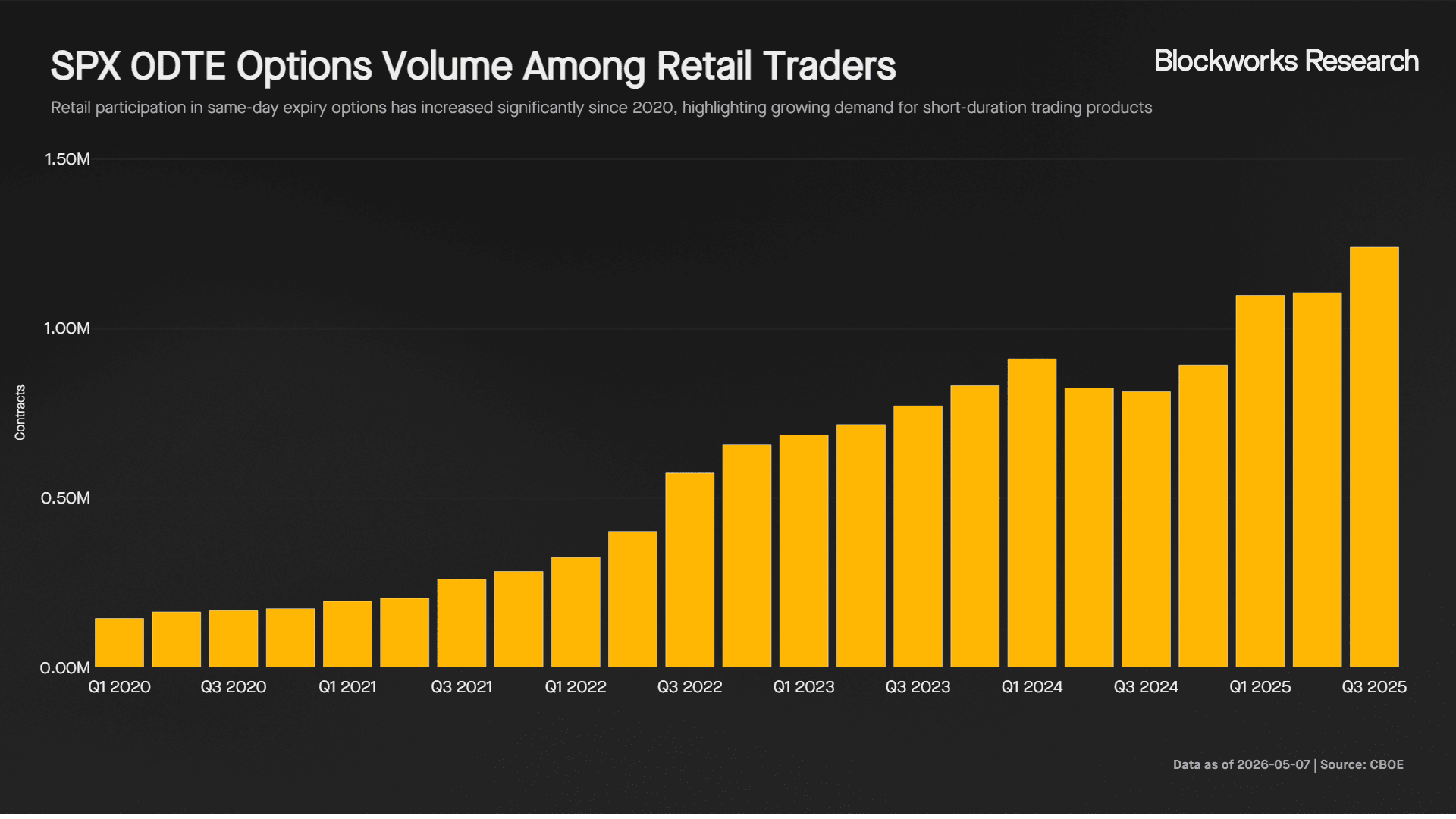

The larger opportunity may lie in bringing short duration formats to more volatile assets. High beta AI stocks, Korean equities and earnings driven names regularly experience sharp intra day swings that are naturally suited for hourly and 15min prediction markets. This would also allow Polymarket to expand beyond crypto native users into a broader TradFi audience. The demand for short duration speculative products already exists, with 0DTE option volumes continuing to trend sharply upward since 2020.

Short duration markets could also work well in sports. Instead of predicting the final outcome of a game, users could trade shorter windows within the match itself. The faster feedback loops and rapidly shifting odds could create a similarly engaging experience for retail traders. The first platform to successfully expand short duration markets beyond crypto will likely gain a major advantage in the next phase of the volume race.

Better Distribution

Retail participation remains the core driver of these markets. A trend increasingly visible across the industry is the popularity of gamified trading experiences. Platforms such as Rainbet and Stake generated roughly 23.4M and 86.4M monthly visits respectively last month and are frequently featured across TikTok, Instagram and influencer content.

That is the same direction platforms like Euphoria are pushing toward by making trading feel more game like and entertainment driven.

Polymarket recently introduced one tap trading for 5min and 15min markets which improves the user experience, but the platform still feels structurally closer to an exchange than a consumer entertainment product. A more gamified frontend could become an effective onboarding funnel for a much broader retail audience.

Improved Product

Polymarket’s product experience still suffers from issues that become increasingly important in short duration markets where latency is critical. Slow UI updates, settlement delays, failed transactions and discrepancies between displayed prices and the live order book continue to impact execution quality.

What has been encouraging is that the team has openly acknowledged many of these issues and already begun rolling out infrastructure upgrades. The launch of CLOB v2 on April 28th was designed to improve throughput and reduce ghost orders, with additional performance upgrades expected over time. Chain migration also remains on the roadmap, which should allow for faster settlement and lower latency.

Order execution mechanisms are also likely due for further improvement, and Polymarket could take a page from Hyperliquid’s playbook. Features such as cancel priority, where cancellations are processed before new trades, could better protect market makers from being picked off. Priority fees that reduce latency could also emerge as an additional revenue stream given how important execution speed has become for algorithmic traders.

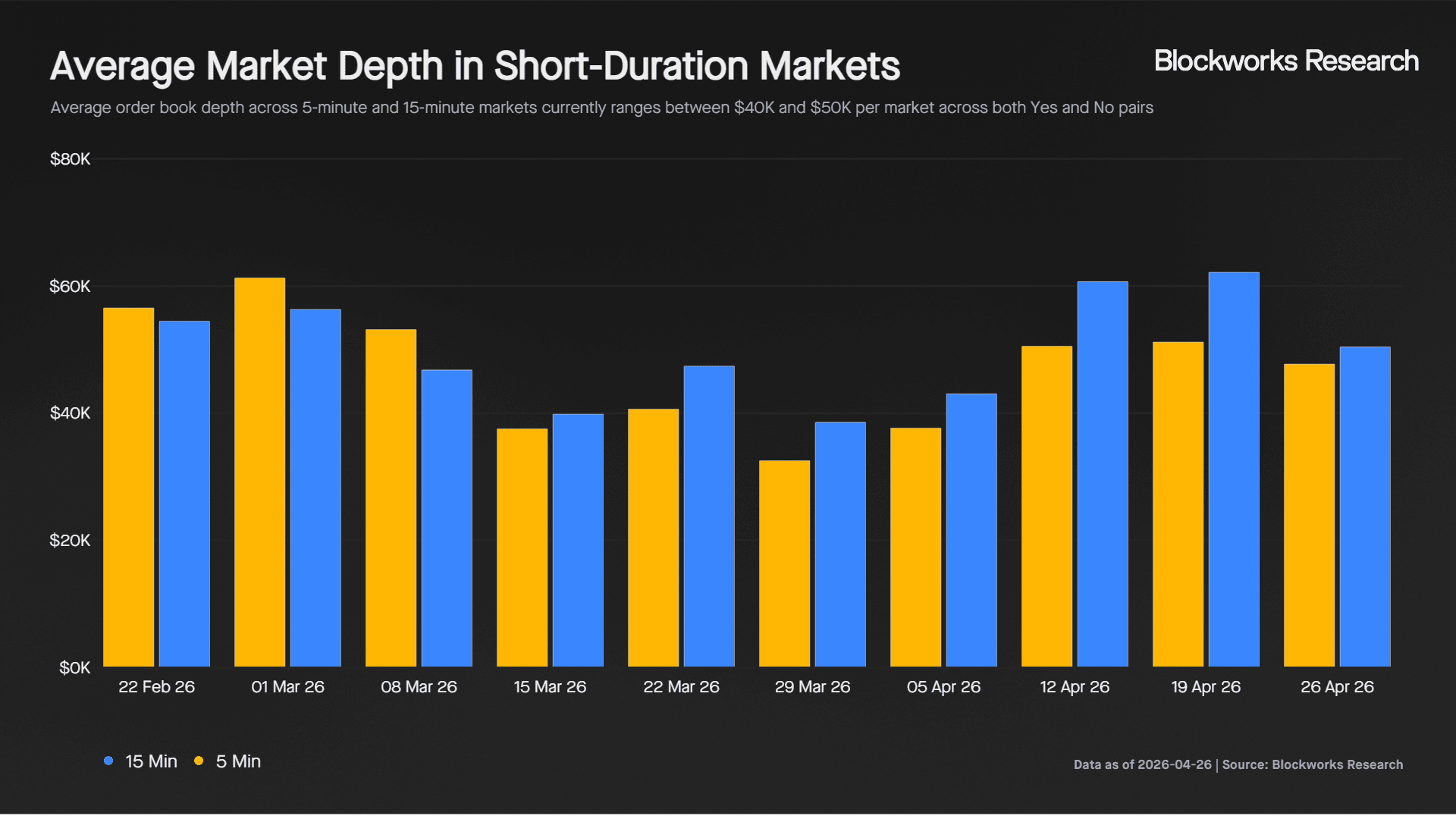

These improvements matter because market depth in short duration markets remains relatively thin with average depth per 5min and 15min market still sitting around $40K-$50K. Improving execution quality and market maker protections should help deepen liquidity over time.

Conclusion

Short duration markets have quietly become one of the most important drivers of activity on Polymarket. What initially looked like a niche product is increasingly evolving into a high frequency volatility marketplace where retail traders chase sharp returns while professional firms systematically extract small edges through speed, hedging and market making.

The opportunity for Polymarket is significant. These markets generate disproportionately high fees, strong engagement and naturally lend themselves to gamified trading behavior. But competition is accelerating quickly, and maintaining leadership will require faster execution, deeper liquidity and expansion into new categories beyond crypto.

Ultimately, the success of short duration prediction markets may have less to do with prediction itself and more to do with creating highly liquid environments for trading volatility. Right now, that appears to be exactly what users want.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.