This research report has been funded by ZKsync. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by ZKsync. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

ZKsync and Grvt: Enabling Composable Perpetuals

Key Takeaways

-

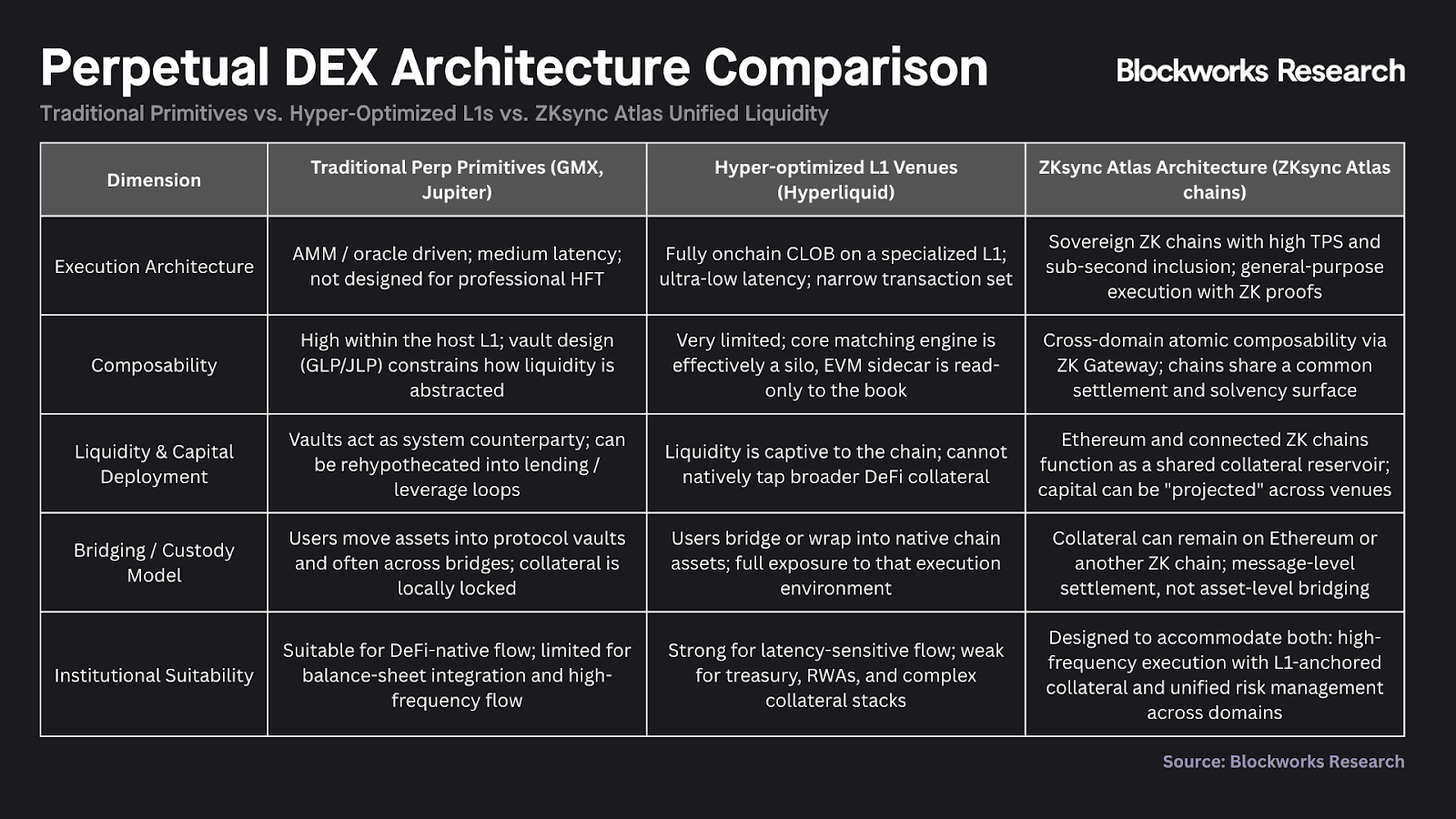

The performance vs. composability tradeoff defined first-generation perp DEXs. High-throughput execution required isolated app-chains that fragmented liquidity away from Ethereum's $122B in DeFi collateral, forcing users to bridge assets and reconstruct financial primitives in siloed environments.

-

ZKsync’s Atlas architecture has dissolved this constraint. Sub-second proving now enables real-time margin verification against L1 collateral without asset movement, allowing derivatives venues to access Ethereum's liquidity infrastructure while matching isolated L1 throughput.

-

Unified liquidity enables diversified revenue beyond transaction fees. Platforms can now monetize collateral yield, margin interest, and ecosystem fees, mirroring how Robinhood and Coinbase generate substantial revenue from interest and services rather than trading alone.

-

Ethereum-native platforms have a structural edge as tokenized assets scale. Ethereum already concentrates the capital and trust, but its base layer cannot support high-frequency, real-time markets. Built on ZKsync, Grvt aims to become Ethereum’s market layer: an execution venue that can reference Ethereum-secured collateral in real time. It starts with perpetuals, then expands into a broader onchain banking stack that keeps custody anchored to Ethereum while bringing high-performance trading to specialized execution.

-

Lighter has demonstrated that verifiable execution and zero retail fees can capture market-leading volume ($292.5B in Nov 2025) without sacrificing security.

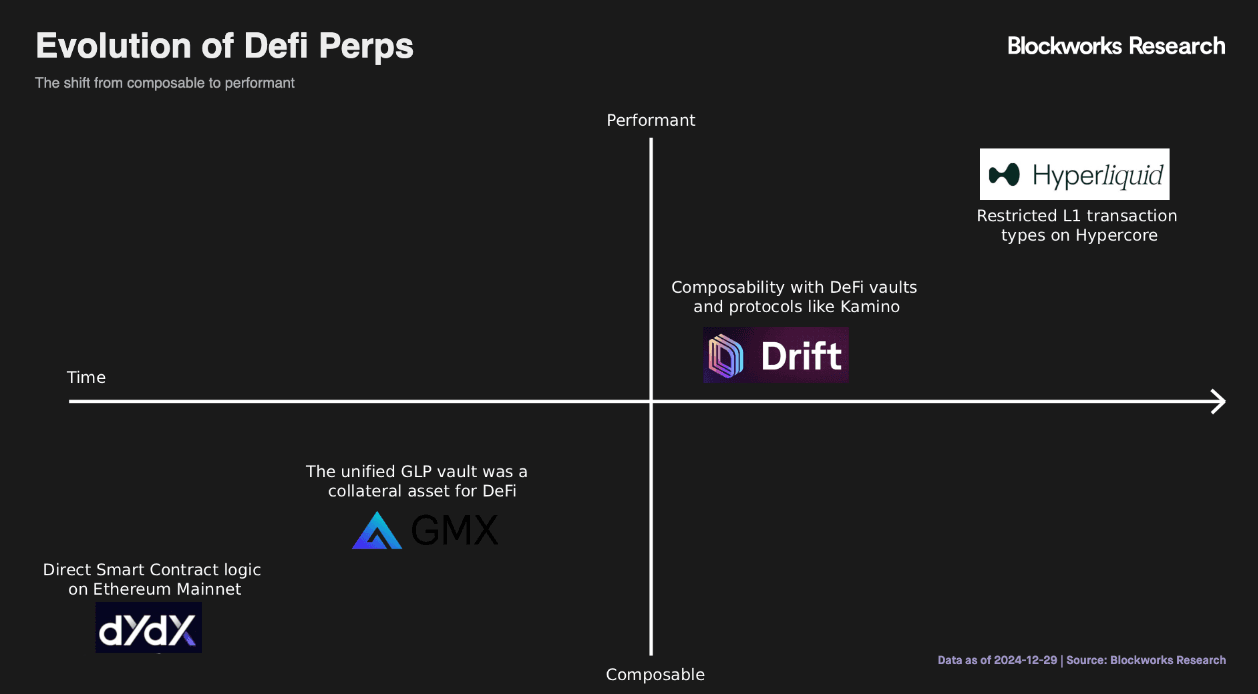

Decentralized Perpetuals: The Performance Trade-off

Perpetual futures began as offchain instruments on centralized exchanges, with BitMEX's XBTUSD launch in May 2016 establishing the funding-rate-pegged format that dominates crypto derivatives today. These venues executed matching and risk management on proprietary servers, creating unverifiable custodial risks that were highlighted in FTX's collapse. The resulting loss of over $8B exposed critical verification gaps in safekeeping customer funds, a far cry from the industry’s original ethos of self-custody and transparency. But it also catalyzed a gradual pivot toward onchain settlement.

At the time, general-purpose L1s lacked the infrastructure and throughput for performant perpetuals. The first DeFi perpetual wave (2020-2021) deployed AMM-based designs to circumvent Ethereum's constraints; Perpetual Protocol v1 introduced a virtual AMM; Synthetix perpetuals used delayed oracle settlement; and GMX pooled liquidity against its GLP vault. These models concentrated counterparty risk on LPs and limited market breadth, prompting a natural shift back to order books as base-layer performance improved.

Hybrid architectures emerged next, pairing offchain CLOBs with onchain settlement to reconcile CEX-like latency with verifiable custody. Drift Protocol, for example, limited by Solana's blocktimes, decoupled matching from execution: a network of offchain bots rapidly pairs orders in local memory, triggering the blockchain only for the final, atomic settlement of assets. This design circumvents the structural incompatibility between block-time finality and high-frequency quoting, allowing hybrid exchanges to support professional market making while strictly preserving noncustodial security.

More recently, high-throughput chains have enabled fully onchain CLOBs, though this requires extreme specialization, at the expense of general computation. Hyperliquid, for instance, runs its entire book onchain by restricting its L1 to just essential transaction types, unlocking parallelized validation speeds unattainable on general-purpose chains. This pivot represents a fundamental architectural decision: the trade-off between atomic composability and raw performance.

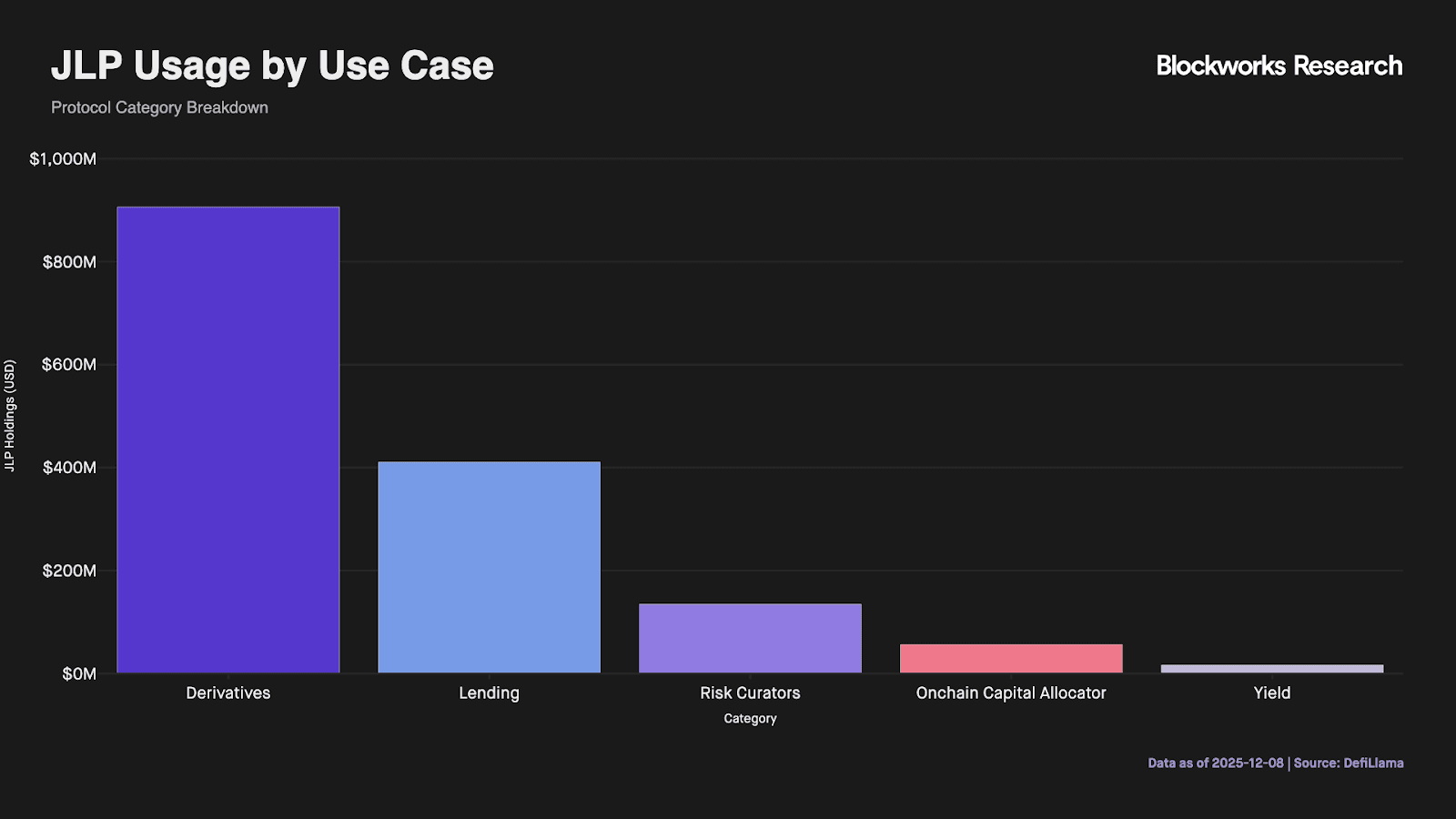

The evolution of the liquidity token illustrates this trade-off effectively. On Solana, Jupiter’s JLP emerged as the equivalent to GMX’s GLP, users deposit USDC, BTC, SOL, or ETH into the JLP which acts as the counterparty to $14B monthly perpetual volume.

However, due to the asset's composability beyond backing the derivative exchange, a massive secondary market has formed around the asset: approximately $400M — nearly a third of the total supply — is actively rehypothecated in lending markets like Kamino Finance. JLP is used for leverage loops, liquidity pairing, or trading fixed yields on protocols like Exponent. This capacity to rehypothecate capital by simultaneously backing trades, earning yields, and securing loans stands in contrast to siloed app-chains, where such secondary utility is structurally impossible.

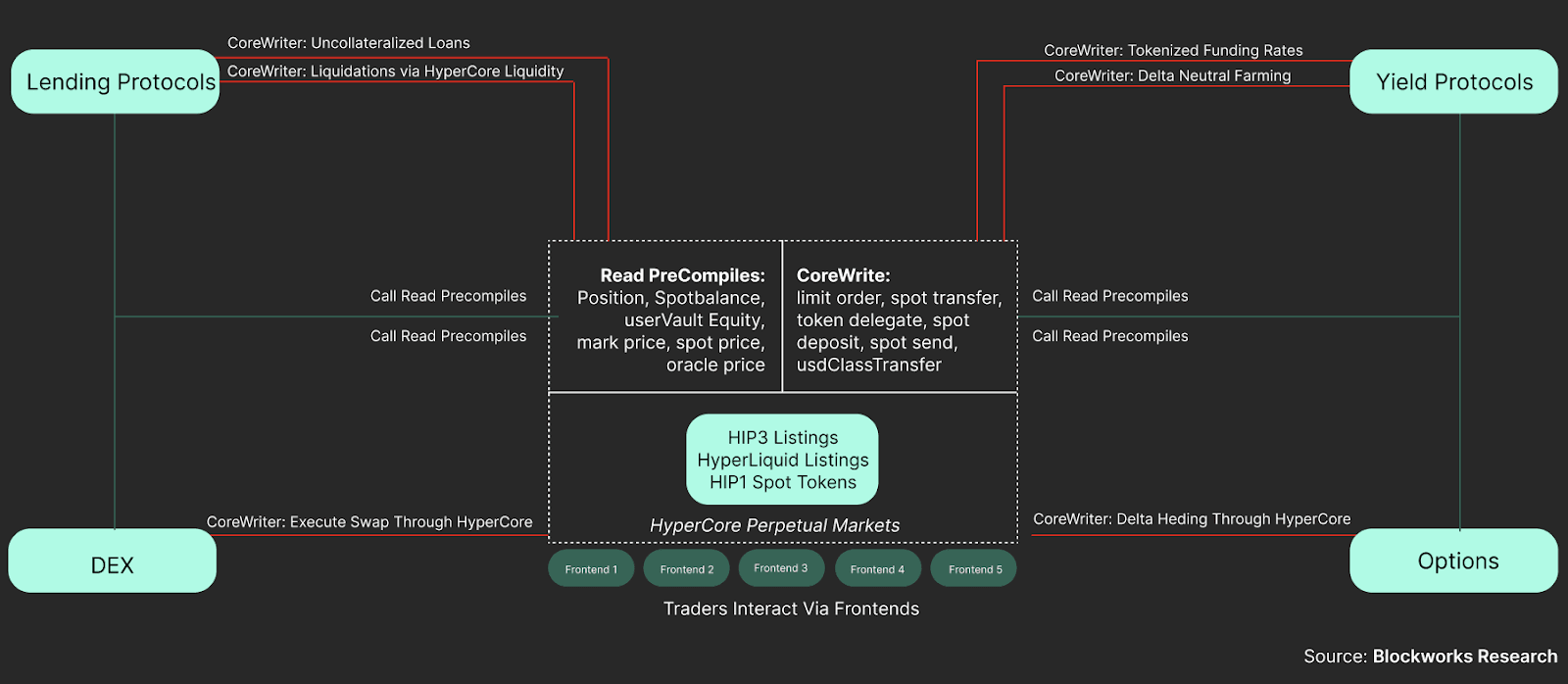

This constraint has prompted a necessary response. Hyper-optimized chains are now attempting to reclaim the composability they initially sacrificed for throughput. Hyperliquid exemplifies this approach through its dual-layer architecture: recognizing that HyperCore's restriction to specific trading primitives creates an isolated execution environment, the protocol introduced HyperEVM, a general-purpose execution layer designed to operate in parallel with the order book, reintroducing programmable functionality to a specialized matching engine.

Yet this approach introduces its own inefficiencies. Composability remains asymmetric: the EVM layer can read HyperCore state but cannot synchronously modify the order book or execute transactions, unless via a vault, resulting in disjointed execution. Liquidity fragments across layers, requiring capital to be wrapped into distinct collateral standards (e.g., UBTC) rather than drawn from unified pools. This effectively gates existing DeFi capital behind bridging infrastructure. Moreover, core financial primitives must be reconstructed on the HyperEVM; rather than integrating with established protocols like Aave, developers must build parallel infrastructure to service the isolated ecosystem.

Consequently, while such solutions represent progress toward functional reunification, they substitute the siloed liquidity of a core exchange for the fragmented liquidity of a parallel ecosystem. Still needed is infrastructure capable of delivering composability without compromising performance.

Unified Liquidity: The Transition to the Atlas Architecture

The fundamental constraint is a conflict of state topology. Ethereum L1 offers atomic composability through a single, shared state: swaps, borrows, and liquidations synchronize within a single block. However, its sequential processing model and approximately 12-second slot times are structurally incompatible with the low-latency requirements of high-frequency perpetual trading.

To resolve this, the industry adopted rollup architectures, migrating execution to secondary layers to maximize throughput. While this successfully scaled transaction volume, it introduced a fractured topology: execution became asynchronous, and liquidity fragmented across isolated domains.

Optimistic rollups compounded this fragmentation through their fraud-proof mechanism, which necessitates a seven-day challenge window before state transitions achieve objective finality. This latency effectively precludes trustless capital mobility. To exit or move capital rapidly, users must rely on third-party market makers to front liquidity, reintroducing the custodial risks and counterparty dependencies the architecture was designed to eliminate.

Early Zero-Knowledge (ZK) rollups replaced challenge windows with validity proofs, resolving the trust assumption but failing to address the latency constraints required for unified liquidity. Previous generations of ZK infrastructure suffered from immense computational overhead, with proof generation requiring computation and 15 to 60 minutes to finalize on L1. While this eliminated the seven-day wait, the resulting finality gap meant cross-chain interactions remained asynchronous. A user could not utilize collateral on one chain to margin a trade on another without incurring significant delays, driving the market toward isolated app-chains that prioritized raw execution speed over ecosystem-wide composability.

Resolving this tradeoff demands an architecture capable of delivering sub-second finality while preserving access to unified liquidity pools.

The ZKsync Atlas upgrade addresses this by re-architecting the stack into three integrated layers: Execution, Verification, and Settlement. This design decouples the demand for high-performance execution from the requirement for shared liquidity.

Execution Layer: ZKsync OS: Atlas

The foundation is a modular execution environment designed to eliminate resource contention. Unlike monolithic rollups that force all protocols into a single, constrained virtual machine, ZKsync OS allows for the deployment of sovereign chains with custom execution parameters. This architecture introduces a new sequencer model benchmarked at approximately 23,000 TPS for oracle-style high-frequency updates with approximately 250ms inclusion latency, sufficient to support dedicated perpetuals exchanges without the overhead of building bespoke L1 infrastructure.

The OS uses a unified compilation pipeline. The sequencer runs on native x86 architecture to maximize execution speed, while the code compiles to RISC-V for verification.

This design ensures that the execution trace matches the proven trace, reducing the audit surface. At the same time, it allows specialized chains to achieve sub-second inclusion and throughput exceeding 10,000 TPS — all without sacrificing EVM compatibility.

Verification Layer: Airbender

High throughput is insufficient for unified liquidity if verification latency disconnects the chain from the network. Previous proving systems faced high costs and latencies measured in minutes, rendering high-frequency market making unfeasible.

Airbender addresses this through a generalized RISC-V zkVM capable of generating validity proofs in under one second on commodity hardware and slashing proving costs to approximately $0.0001 per transfer. By collapsing the time delta between execution and verification to near-zero, Airbender ensures that the state of a high-speed derivatives chain is cryptographically finalized almost instantly, establishing a verification standard compatible with institutional-grade trading.

Settlement Layer: ZK Gateway

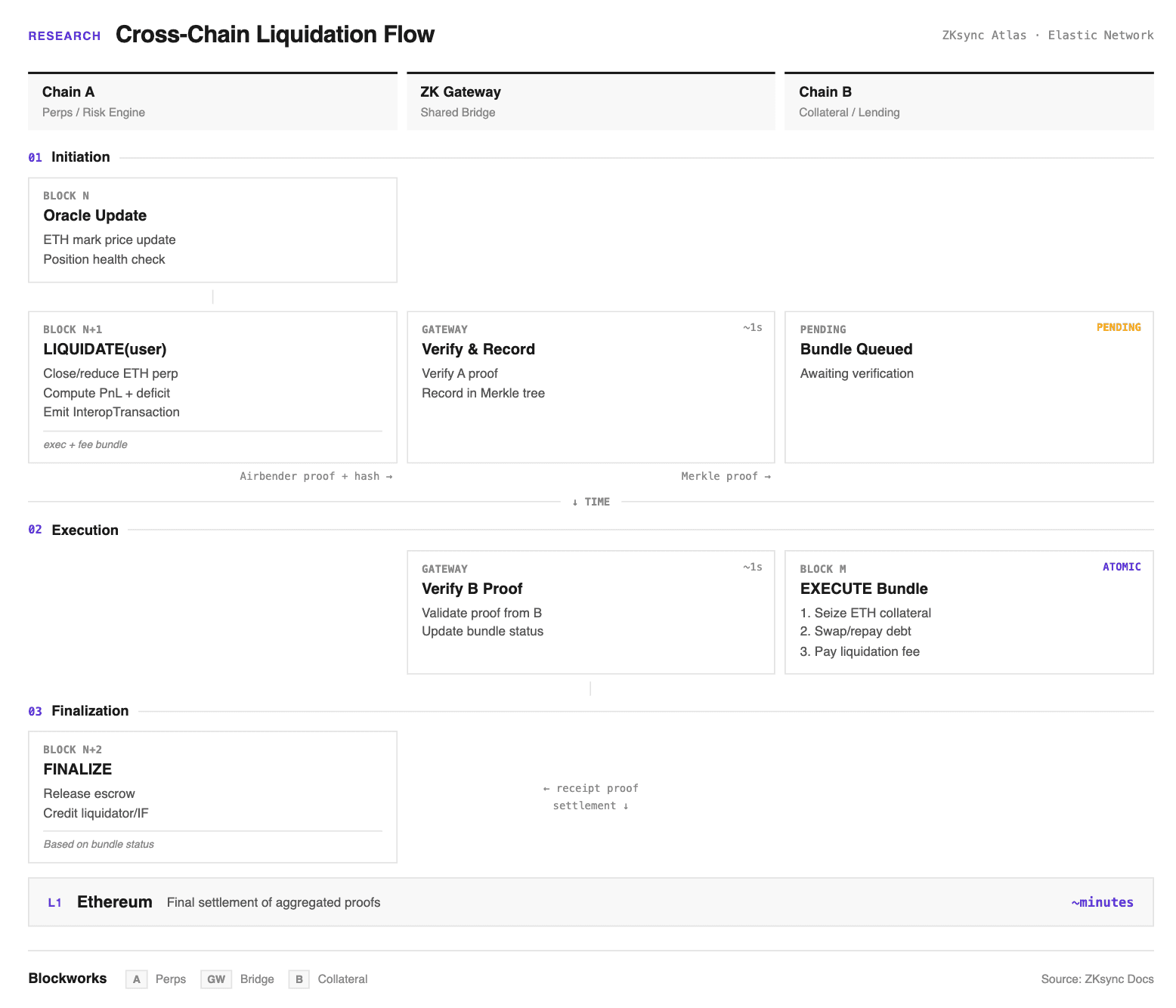

The ZK Gateway leverages these real-time proofs to function as a unified settlement layer, creating an elastic network of ZK chains. Previously, cross-domain settlement required naive L2-to-L1-to-L2 routes that incurred 30 to 120 minutes of latency. The Gateway changes this model by acting as a central router that aggregates one-second proofs from independent chains to facilitate trustless, atomic message passing. Because every state transition is verified instantly by Airbender, the Gateway can settle cross-chain transactions with approximately one-second network hops, eliminating the security assumptions and capital inefficiencies of traditional bridges. Rather than requiring assets to be bridged across domains, only state changes are communicated, enabling cross-exchange liquidity without capital migration.

The following figure illustrates this architecture in practice: a liquidation event executed across two ZKsync chains, where a perpetual exchange on Chain A accesses user collateral held on Chain B with sub-second finality.

This architecture restores atomic composability to high-performance environments. Rather than remaining isolated within individual domains, liquidity becomes accessible network-wide: a user can maintain collateral on a secure lending chain and execute a leveraged position on a separate high-frequency perpetuals chain in a single, atomic flow. The Gateway validates user solvency across both domains simultaneously, unifying liquidity across the entire network.

This represents a structural departure from both traditional vault-based primitives and hyper-optimized app-chains. The following table illustrates how these architectures diverge across execution, composability, capital deployment, custody, and institutional suitability.

The Strategic Unlock: What Unified Liquidity Enables

The maturation of the decentralized perpetual market suggests that the latency wars have largely concluded. Specialized venues like Hyperliquid have effectively solved the engineering constraints of high-frequency trading, establishing deep liquidity moats that leave little room for new entrants competing solely on execution speed. Similarly, protocols like Lighter have compressed fee structures to their economic floor. With raw performance and low costs now established as baseline commodities rather than competitive differentiators, the industry's focus is shifting. The next meaningful optimization is not in making the trade faster, but in making the venue composable with over $122B in DeFi collateral. By dissolving the boundaries between execution and settlement, the Atlas architecture addresses this saturation point directly.

The resulting capabilities build on one another: decoupling custody from execution enables access to unified markets, and adding entirely new collateral classes and primitives.

Decoupling Custody from Execution

The major unlock is synchronous cross-domain margin. Atlas enables native asset utilization, where collateral remains on Ethereum Mainnet while simultaneously backing positions on high-frequency ZKsync chains like Grvt. Unlike isolated app-chains, which force users to bridge and often wrap assets into fragmented liquidity pools, this architecture allows margin, funding, and risk updates to settle via ZK proofs against Ethereum's canonical state. This eliminates the opportunity cost of capital locked in bridges: a user can hold native ETH in a secure Mainnet vault and instantly leverage it on a high-performance derivatives exchange.

Accessing Unified Spot and Credit Markets

Once custody and execution are decoupled, the full depth of Ethereum's liquidity infrastructure becomes accessible from specialized execution layers. By treating Ethereum not only as a settlement layer but as a shared liquidity reserve, users on a ZKsync chain can instantaneously tap into Mainnet protocols such as Uniswap, Aave, or Euler. A user can borrow against their portfolio on Aave Mainnet and deploy that purchasing power into a high-frequency strategy on a ZKsync chain in a single, atomic flow. This merges the deep liquidity of the base layer with the aggressive performance of the execution layer, eliminating the fragmentation that typically constrains L2 ecosystems.

Activating Exotic Collateral

With access to unified markets established, passive assets can be transformed into active collateral. In siloed ecosystems, integrating complex instruments such as LP tokens, Liquid Staking Tokens (LSTs), or Principal Tokens (PTs) is structurally difficult due to cross-chain bridging risks. Under Atlas, these yield-bearing assets on Ethereum become directly composable with high-performance execution layers:

- Active LP Collateral: Uniswap V3 LP positions can margin perpetual trades, earning trading fees and market yield simultaneously

- Restaked Leverage: Liquid Restaking Tokens (LRTs) can serve as derivatives collateral, allowing users to stack restaking yield on top of trading PnL

- RWA Integration: Stablecoins backed by RWA, or Tokenized Equities on Ethereum can function as margin, enabling institutional-grade strategies where idle collateral generates yields while securing active positions

This capability addresses a specific constraint facing large allocators. Institutions are increasingly bringing high-quality, tokenized assets onchain, yet billions in capital currently sit idle due to the risks associated with bridging to experimental execution layers. Unified liquidity allows this capital to be activated without leaving the security perimeter of Ethereum Mainnet. By keeping assets anchored on the base layer while projecting their value into high-performance execution environments, Atlas provides an architecture capable of satisfying institutional demand for both extreme speed and custodial security.

Platform Approaches to Unified Liquidity

For perpetual exchanges, unifying liquidity not only optimizes existing exchange architectures, it enables an entirely different category of platform. When execution, settlement, and collateral management can operate synchronously across domains, decentralized exchanges are no longer constrained to pure trading functionality. They can integrate lending logic, native yield generation, and RWA secondary markets into a single interface, mirroring the vertical integration that allowed fintech applications like Robinhood to consolidate brokerage, banking, and asset management under one platform.

ZK architectures have emerged as the requisite foundation for this unified experience. Against this backdrop, Grvt and Lighter represent interpretations of this vision, each proposing a unique path toward the endgame of unified liquidity.

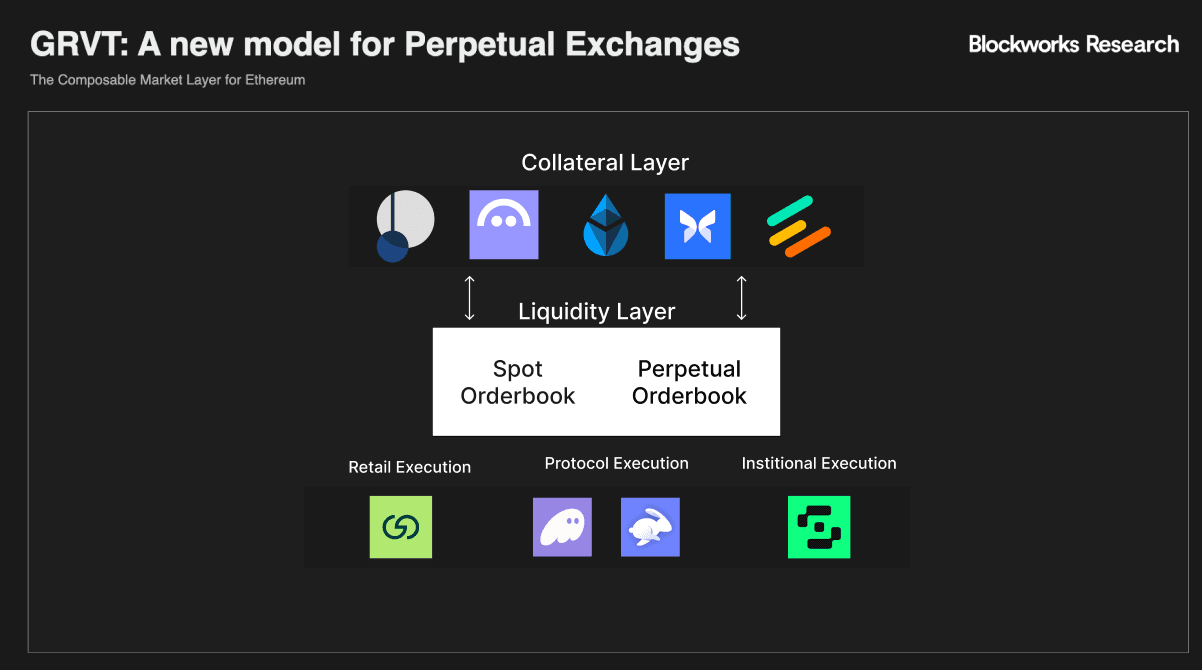

Grvt: The Unified Market Thesis

Grvt is positioning as an onchain private bank, built on a unified-liquidity market layer that starts with a professional-grade perpetuals venue. Grvt launched in late 2024 and is led by Hong Yea (ex Credit Suisse, Goldman Sachs). Backers include Flow Traders, Galaxy Trading Asia, and QCP Capital, with strategic support from the ZKsync Foundation. Within its first eleven months, Grvt hit peak weekly volume of $8.6B.

Its core architecture separates execution confidentiality from custody and settlement integrity. The platform uses a private offchain sequencer capable of 600,000 TPS, meaning live order book and position state are not published to a transparent ledger. This addresses a known vulnerability of fully onchain books, where observable margin buffers, stop placement, TWAP execution, and liquidation thresholds can be exploited to infer intent and structure adverse selection or position targeting. Execution remains private, while batched state transitions are verified via ZK proofs and settled to Ethereum L1.

As a ZK stack implementation, the margin framework is designed to reference L1-native collateral such as stETH or liquid restaking tokens, removing the requirement to bridge and reconstitute collateral inside a siloed environment.

The venue pairs this architecture with microstructure choices intended to broaden liquidity provision and improve execution quality for non-latency-sensitive flow:

- Retail Price Improvement (RPI): Retail-only, post-only limit orders that interact primarily with UI-driven flow, reducing exposure to latency-driven adverse selection while improving execution for retail takers.

- Incentive-Driven Bootstrapping: 22% of total token supply earmarked for ecosystem rewards tied to activity, deposits, and referrals.

- Builder Codes: Fee-sharing mechanism that allows integrators and front-end builders to capture a portion of trading fees from volume routed through their interfaces, incentivizing distribution.

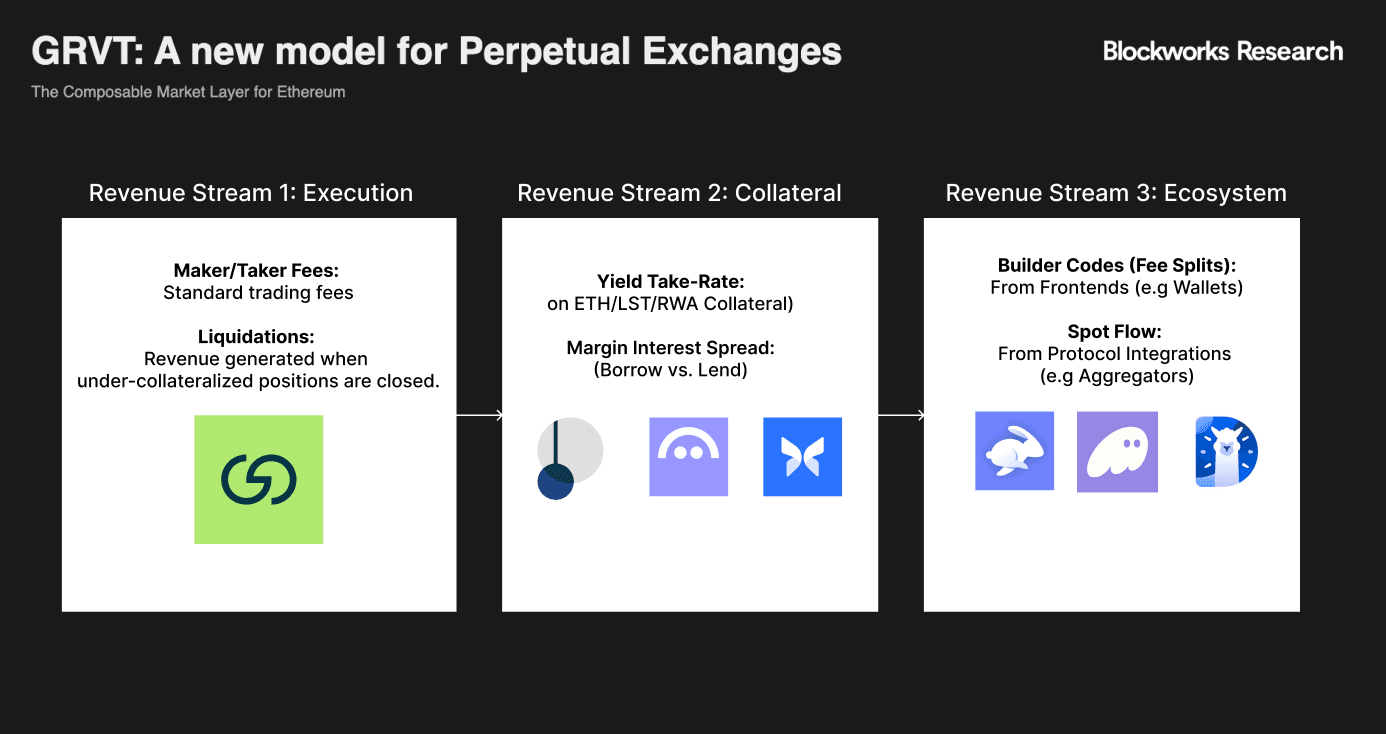

With execution and liquidity depth established, Grvt is utilizing ZKsync Atlas to expand from a standalone perpetual exchange into a broader market layer. This expansion addresses a structural limitation in most perpetual DEX business models: absent unified liquidity, monetization is typically dominated by transactional revenue because collateral is captive within the venue and economically inactive beyond margin.

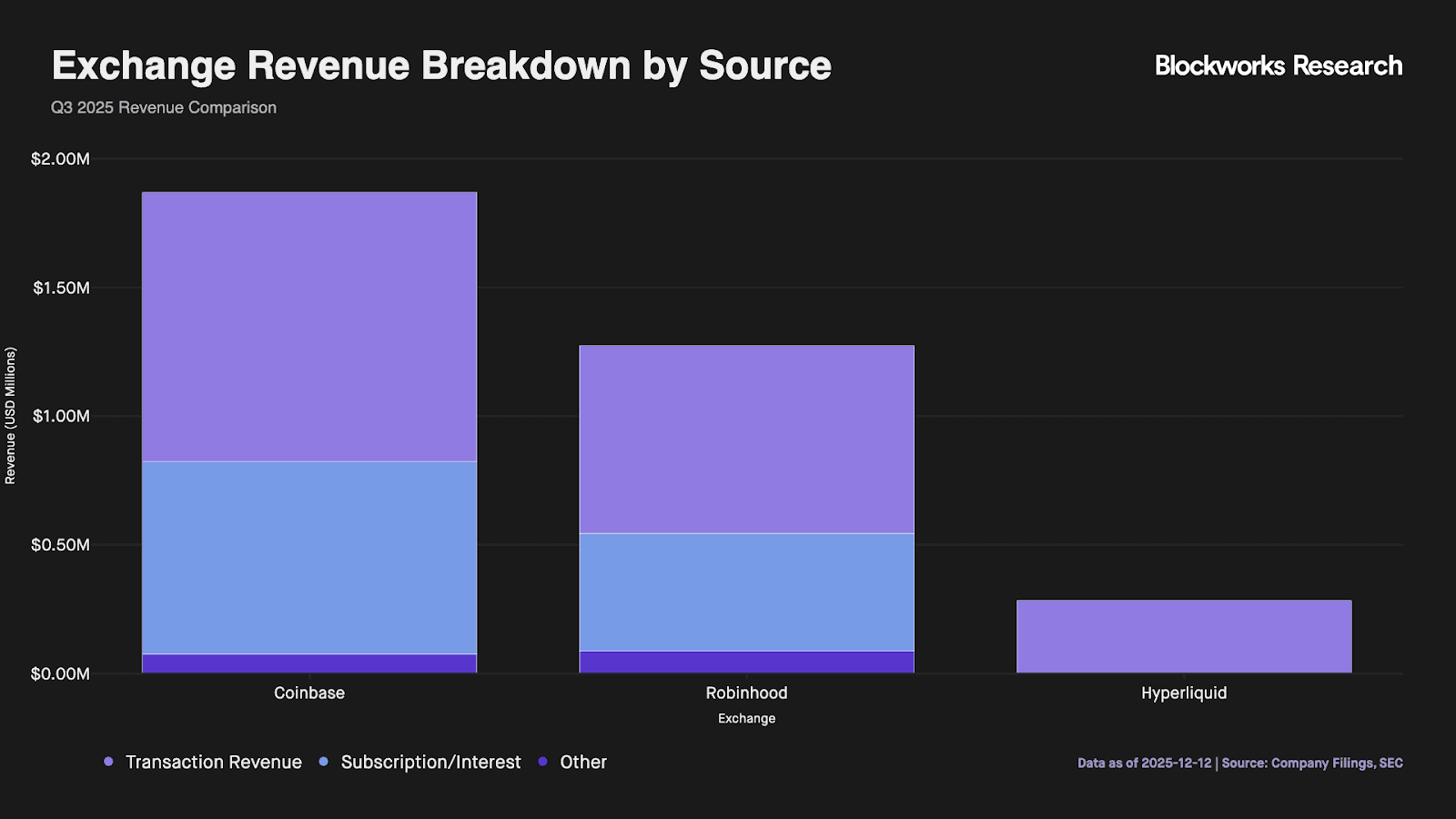

Unified liquidity expands the monetizable surface by allowing collateral to remain productive on Ethereum while satisfying synchronous risk checks on the derivatives venue. This is significant because it unlocks a new revenue lever: collateral productivity. Scaled centralized peers demonstrate the strategic importance of diversifying revenue beyond transaction fees. Robinhood generated $456M in net interest revenue on $1.274B of total net revenues in Q3 2025. Coinbase generated $746.7M in subscription and services revenue on $1.87B of total revenue in Q3 2025, including $354.7M in stablecoin revenue and $64.8M in interest and finance fee income. Hyperliquid, by contrast, remains almost entirely dependent on transaction fees, illustrating the revenue concentration that unified liquidity is designed to overcome.

Grvt is positioning to capture this same diversification onchain. The platform's ambition extends beyond operating a perpetual venue to becoming a full market layer for Ethereum, monetizing the infrastructure stack from collateral through trade execution.

By owning the complete stack, Grvt can monetize multiple touchpoints rather than capturing value solely at the trade. Execution revenue flows from maker/taker fees and liquidations. Collateral revenue derives from yield take-rates on ETH, LST, and RWA deposits, plus margin interest spread on borrow/lend activity. Ecosystem revenue captures value through builder codes and spot floor fees from protocols routing through the platform.

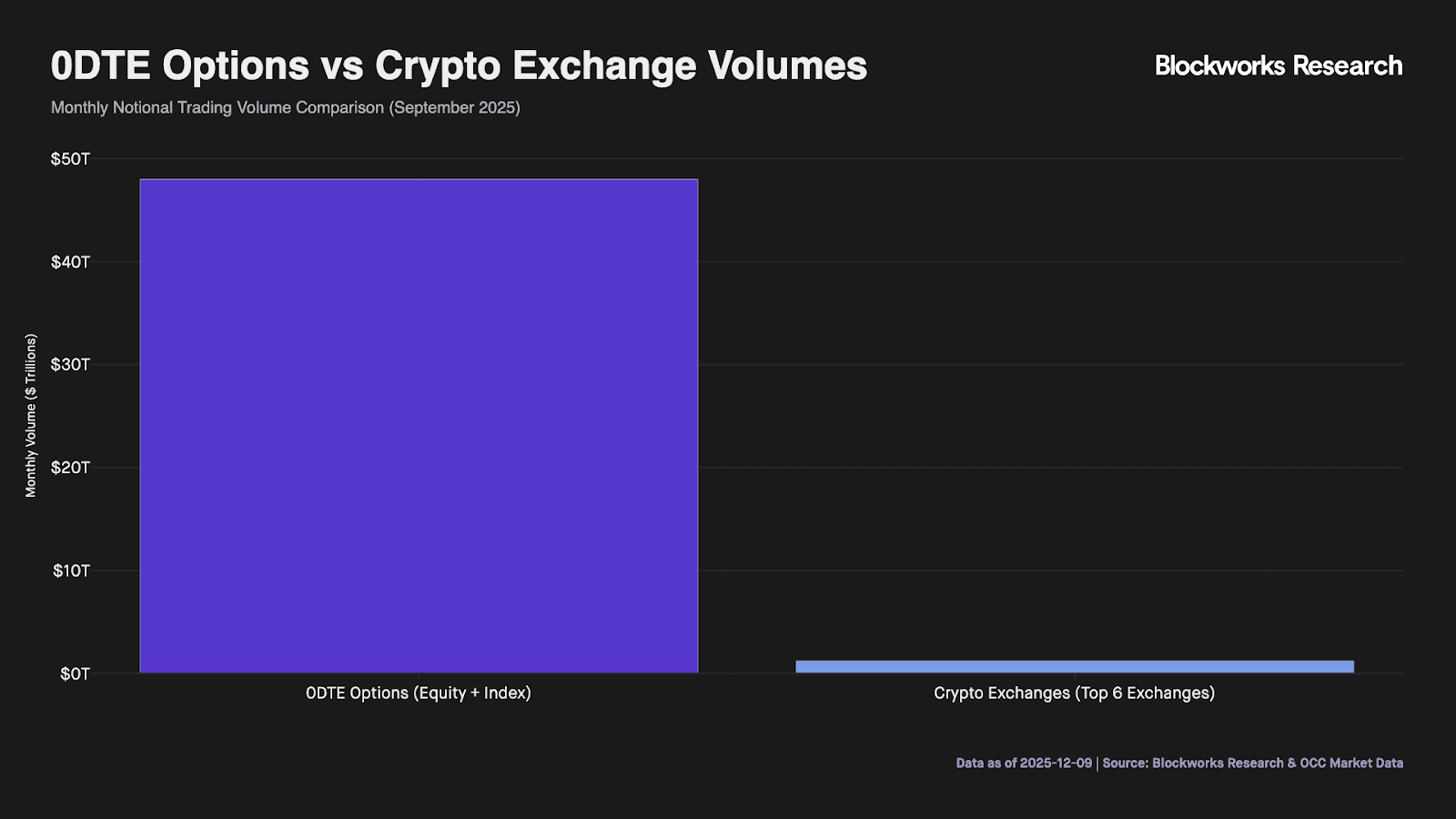

This structure also positions Grvt to expand beyond crypto-native assets into tokenized equities and traditional financial instruments. Listed equity derivatives already clear at scale materially exceeding crypto perpetuals, with the OCC reporting approximately 1.4 billion US options contracts in September 2025 and Cboe indicating 2025 volume is on track to exceed 13.8 billion contracts. Comparing Notional volumes, Equity options 0DTE estimated at $48T, roughly 40x the $1.2T traded across all perpetuals on centralized crypto exchanges in September 2025.

Accessing this market onchain, however, requires solving frictions that have historically made equity perpetuals unviable. The primary constraint for market makers is fragmented capital: hedging inventory sits on one venue while margin collateral sits on another, requiring stablecoin buffers and creating conversion drag. Unified liquidity addresses this directly by allowing tokenized equities to serve as eligible collateral. A market maker can post their hedge inventory as margin, collapsing buffer requirements and enabling tighter spreads. With direct access to Ethereum liquidity, including tokenized securities from platforms like Ondo Global Markets, Grvt will allow institutional market makers to utilize this inventory to quote on the exchange without leaving the security of L1.

Grvt's roadmap sequences toward this vision. Near-term priorities through 2026 focus on RWA perpetuals, extending the book to FX, equities, and commodities. The following phase introduces unified margin and coin margin, enabling vault tokens and broader Ethereum assets as collateral, alongside a spot CLOB and ZK interoperability. Options are positioned as a longer-term extension once the underlying infrastructure matures.

This evolving infrastructure will directly enhance existing wealth management features like Earn on Equity and Grvt Strategies, allowing them to tap into deeper liquidity and more sophisticated yield sources. For users, this means passive offerings will grow in tandem with the platform, enabling non-active traders to participate more fully in Grvt’s yield flywheel.

As unified margin scales and builder activity expands, growing platform revenue will create new avenues for value sharing with the community, completing the transition from a professional venue to an integrated onchain wealth destination.

Lighter: Verifiable Execution and Ethereum-Native Composability

Lighter represents a different interpretation of the unified liquidity thesis: rather than privacy-preserving execution, the platform prioritizes verifiable fairness. Every order match, liquidation, and margin call is proven by custom ZK circuits and verified on Ethereum, mathematically guaranteeing price-time priority execution. This addresses a fundamental trust problem in derivatives trading: users can cryptographically verify that no orders were front-run, skipped, or manipulated.

The platform launched in January 2025, founded by Vladimir Novakovski (formerly Citadel, Harvard). In November 2025, Lighter raised $68M at a $1.5B valuation led by Founders Fund and Ribbit Capital, with participation from Haun Ventures and Robinhood, bringing total funding to approximately $90M.

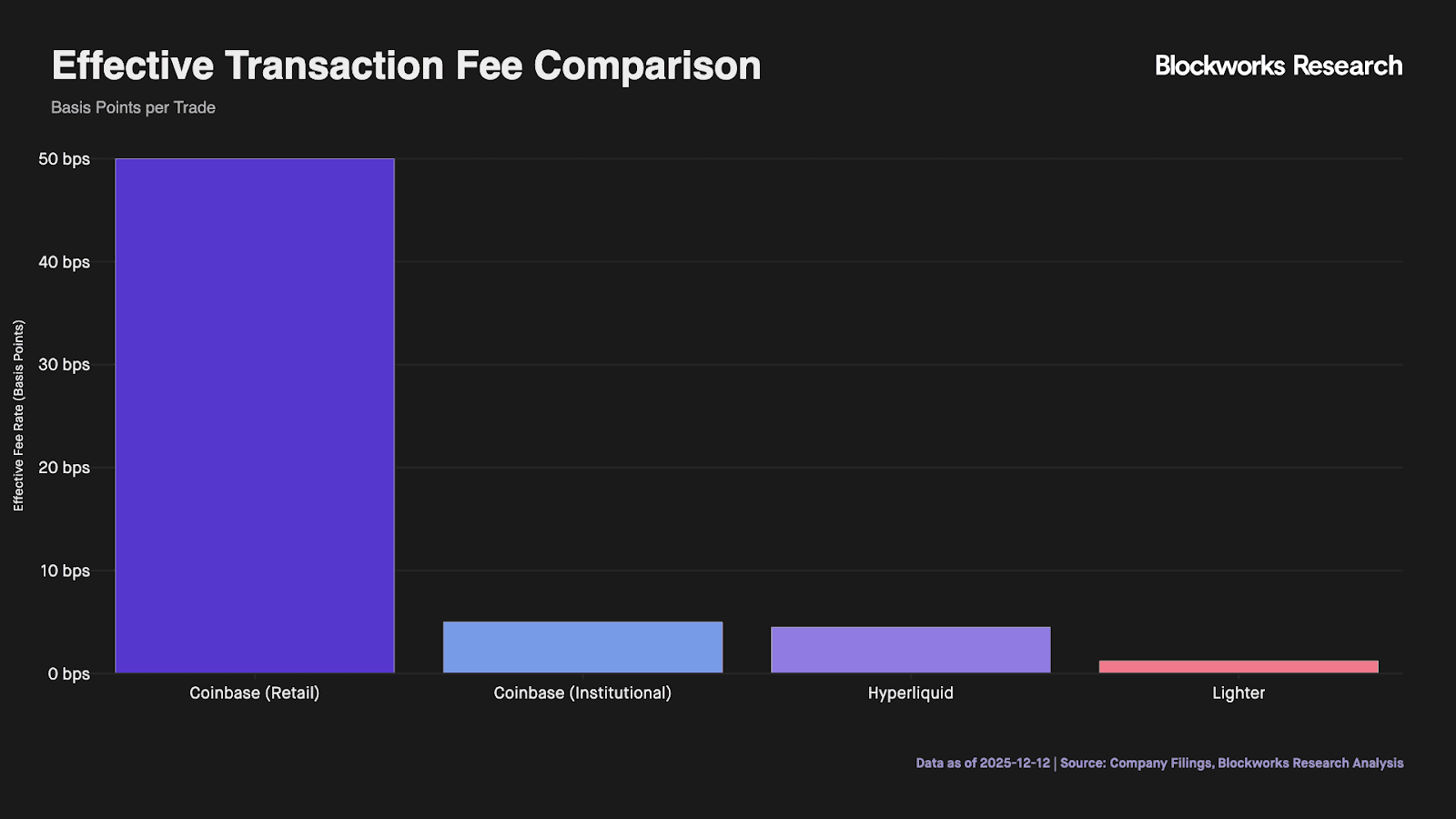

The most visible difference from other venues is Lighter's fee model: retail traders pay zero maker and taker fees. This is not a temporary incentive program but a structural feature enabled by the application-specific rollup architecture. Because Lighter's custom ZK circuits eliminate per-trade gas costs, the platform can sustain zero fees for retail while charging minimal fees (0.002% maker / 0.02% taker) to API and high-frequency flow.

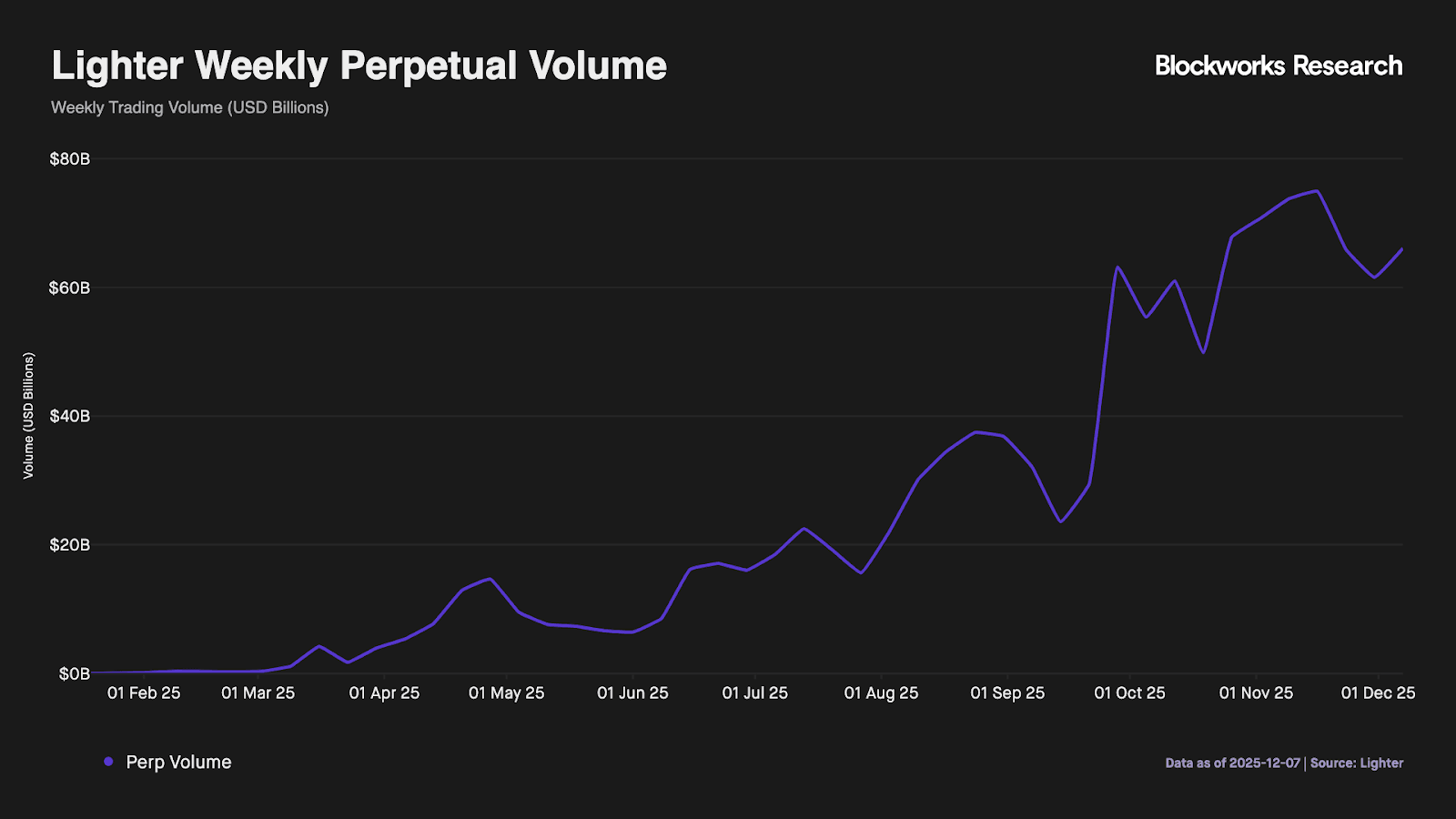

This mirrors the model that disrupted traditional brokerage. Robinhood eliminated retail commissions by monetizing order flow from market makers who valued access to smaller, less directional trades. Lighter applies similar logic onchain: retail flow is less toxic to liquidity providers, making it valuable at scale even without explicit fees. Lighter's version monetizes through professional tier fees, LLP yield, and spread capture against retail counterparties. Since launch, the platform has generated approximately $34M in cumulative fees while processing over $280B in volume, implying an effective fee rate of roughly 1.2 basis points, substantially below competitors.

Additionally, Lighter launched spot trading on Dec 4, 2025, starting with ETH. The move highlights a structural advantage of Ethereum-native architecture, users trade native ETH/USDC pairs directly, without the friction of bridged or wrapped assets. On Hyperliquid and other isolated L1s, traders must convert to chain-specific representations (UETH, UBTC), introducing bridge risk, conversion costs, and capital fragmentation. Lighter's spot markets inherit Ethereum's existing token standards and liquidity infrastructure, eliminating this overhead entirely.

Lighter has demonstrated that verifiable execution and zero retail fees can drive meaningful volume: $292.5B in November alone, surpassing Hyperliquid to become the highest-volume perps protocol that month. The platform also proves that choosing Ethereum's security no longer means compromising on performance. With Universal Cross Margin planned for Q1 2026, enabling any Ethereum asset as collateral, Lighter is positioned to deepen integration with Ethereum's existing DeFi infrastructure rather than rebuilding it in isolation.

Conclusion

The first generation of perp DEXs faced a binary choice: optimize for execution speed on isolated chains, or accept Ethereum's latency constraints to preserve composability. Venues that prioritized throughput built standalone L1s capable of matching CEX performance, but at the cost of fragmenting liquidity away from Ethereum's existing DeFi infrastructure. Users bridged assets into siloed environments, capital sat idle behind custodial choke points, and core financial primitives had to be reconstructed from scratch.

ZKsync's Atlas architecture has collapsed this tradeoff. Sub-second proving enables derivatives venues to verify margin against L1 collateral in real time, accessing Ethereum's $122B liquidity infrastructure without bridging risk or asset movement. Collateral can remain on Mainnet while simultaneously backing positions on high-frequency execution layers, eliminating the opportunity cost that defined earlier designs. Grvt and Lighter represent two expressions of this capability.

Grvt is evolving from a unified market layer into an accessible onchain private bank. It integrates collateral custody, lending, spot, and derivatives execution into a single infrastructure stack with diversified revenue across each touchpoint.

Lighter has demonstrated that verifiable execution and zero retail fees can capture market-leading volume while settling on Ethereum.

Both are positioning for a market where tokenized assets scale onchain and institutional allocators require verifiable custody, a market where composability with Ethereum's liquidity layer becomes the primary competitive axis rather than raw execution speed.