Solana DEX Winners: All About Order Flow

Key Takeaways

- Solana DEX dominance will remain bifurcated by asset maturity. Prop AMMs will continue to dominate short-tail, highly liquid markets, while passive AMMs will increasingly specialize in long-tail assets and new token launches.

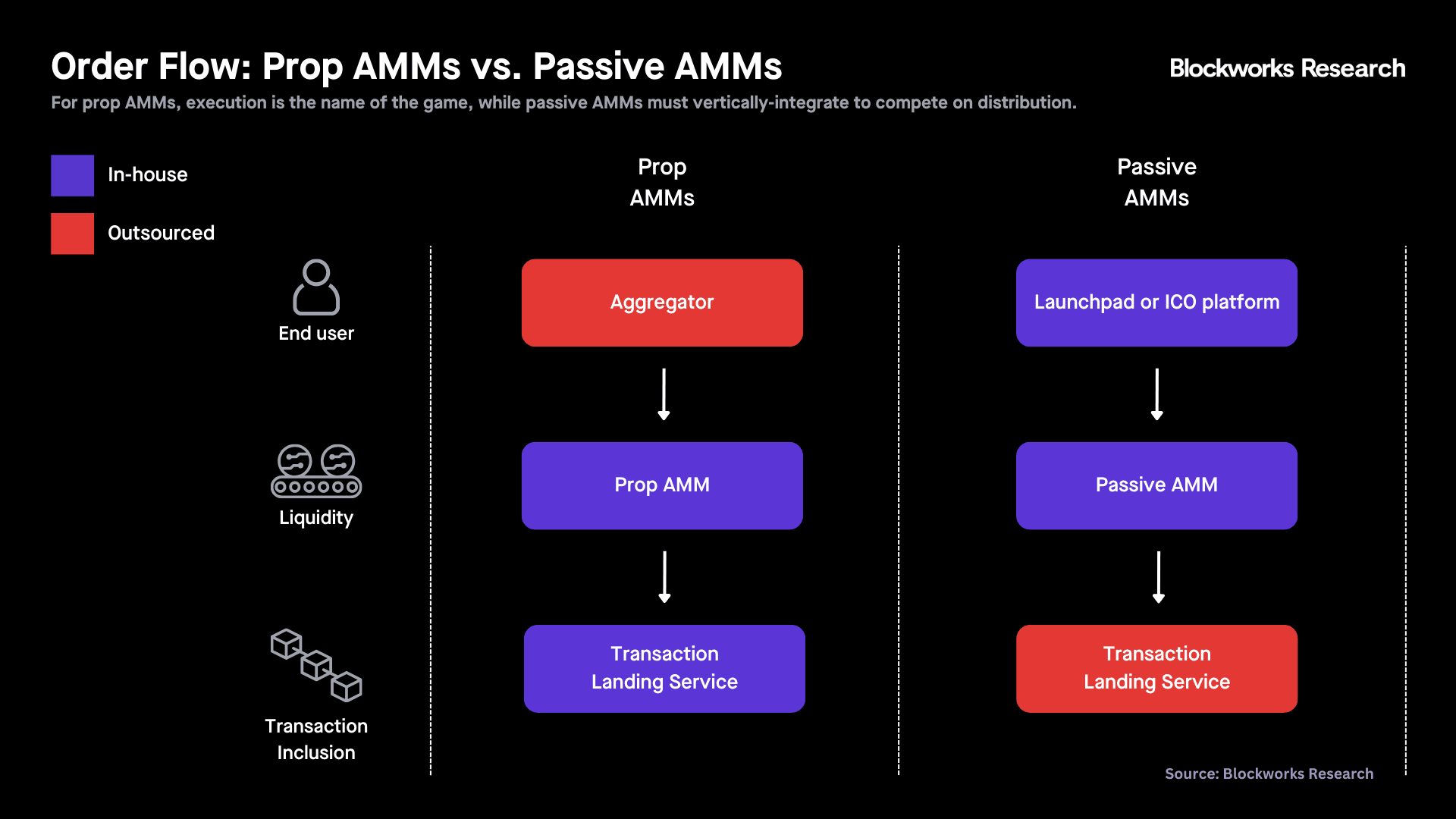

- Winning strategies differ by AMM type. Both prop AMMs and passive AMMs can benefit from vertical integration, but in opposite directions. Passive AMMs are moving closer to the user through token issuance platforms (e.g., Pump-PumpSwap, MetaDAO-Futarchy AMM), whereas prop AMMs are moving down the supply chain and focusing on transaction landing services (e.g., HumidiFi-Nozomi).

- HumidiFi leads the prop AMM category, commanding ~65% market share, with the majority of volume concentrated in SOL-USDC and SOL-USDT pairs. HumidiFi has the most optimized oracle-update instruction costs in the cohort and exhibits superior markouts relative to peers like SolFi and Tessera, as well as passive AMMs.

- The standalone passive AMM model is obsolete. Winning “passive AMMs” will no longer be perceived as AMMs, but as token issuance platforms (e.g., Pump as a launchpad, MetaDAO as an ICO platform) with vertically integrated AMMs serving as the monetization layer.

- DEXs that fit neither category face a structural growth decline. Protocols that are neither prop AMMs nor vertically integrated issuance platforms, most notably Raydium and Orca, are structurally disadvantaged and likely losers of this trend.

- Valuation should reflect both business quality and token value accrual. Multiples like P/S only matter in the context of growth prospects and credible tokenholder value capture. WET illustrates the tradeoff: it seems undervalued versus peers, yet still trades at a discount due to uncertainty around long-term token alignment.

Introduction

In February, we published a report on the competitive dynamics of Solana’s DEX landscape. At the time, DEX volumes were at all-time highs, and we (in hindsight) anchored too heavily to a trailing 90-day window that captured a uniquely frothy period: the Q4 2024 post-election rally, January’s TRUMP memecoin mania, and February’s LIBRA-driven burst of activity. Back then, Raydium was the leading DEX with roughly 50% market share, and the majority of Solana DEX volumes came from memecoins.

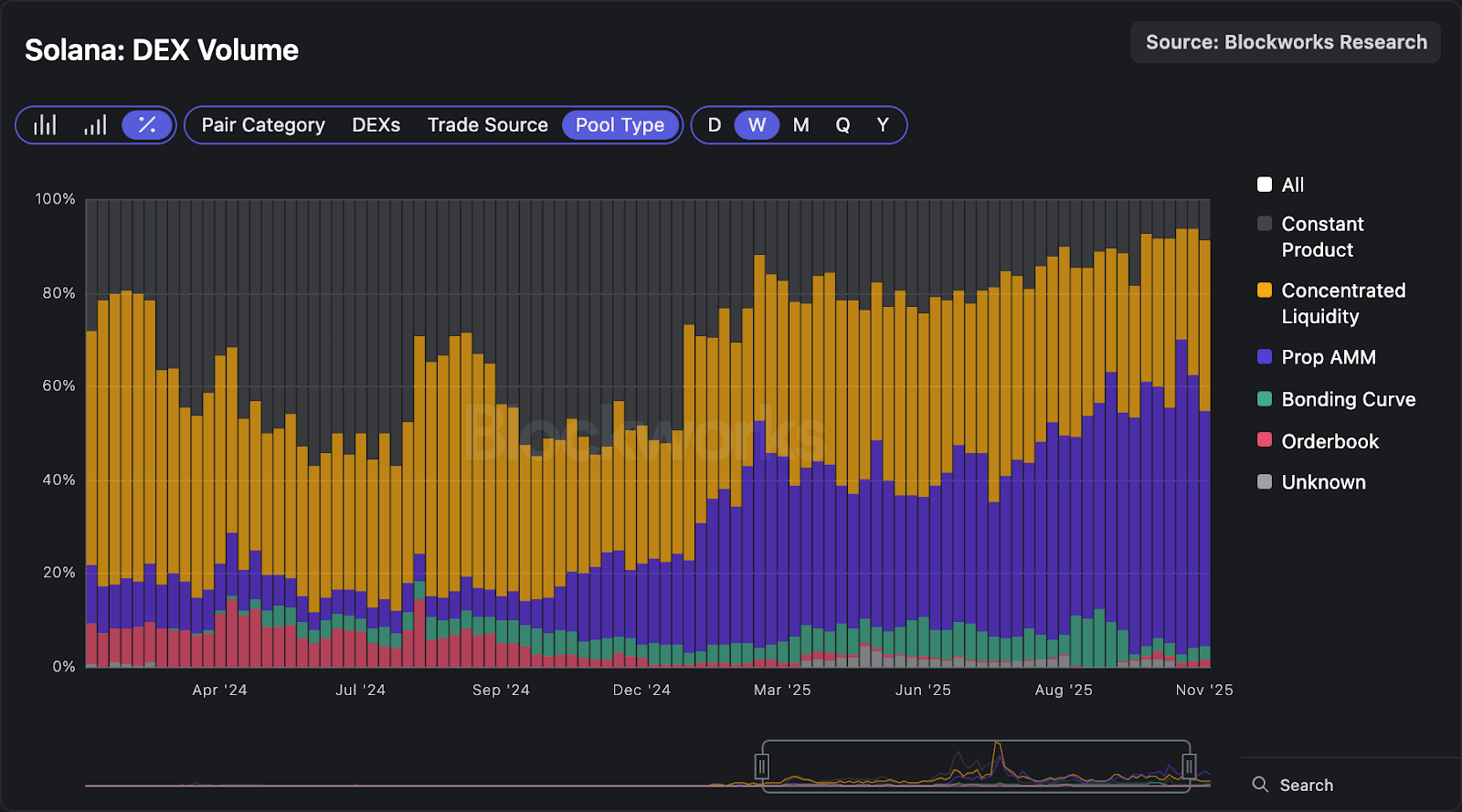

Today, the landscape looks fundamentally different. The rise of prop AMMs has reshaped market structure, and volume concentration has shifted from memes to the SOL-USD pair. While Lifinity pioneered the prop AMM model, it wasn’t until after the launch of SolFi in late October 2024 that prop AMMs began to proliferate and gain a meaningful share of trading volumes for highly liquid pairs.

As prop AMMs continue to dominate flow for the short-tail of assets, passive AMMs are left in a tough spot, increasingly pushed toward long-tail assets and distribution-dependent volume. Pump’s AMM launch in March 2025 demonstrated this dependence: once Pump redirected graduated coins to its own AMM, Raydium lost its largest source of volume and revenue, and has seen decreasing market share ever since. Since passive AMM liquidity is largely commoditized, the AMMs most likely to endure are those that control distribution and order flow.

This report revisits Solana’s DEX landscape with this new market structure in mind, updating competitive positioning, valuations, and our view on the protocols best positioned to win from here.

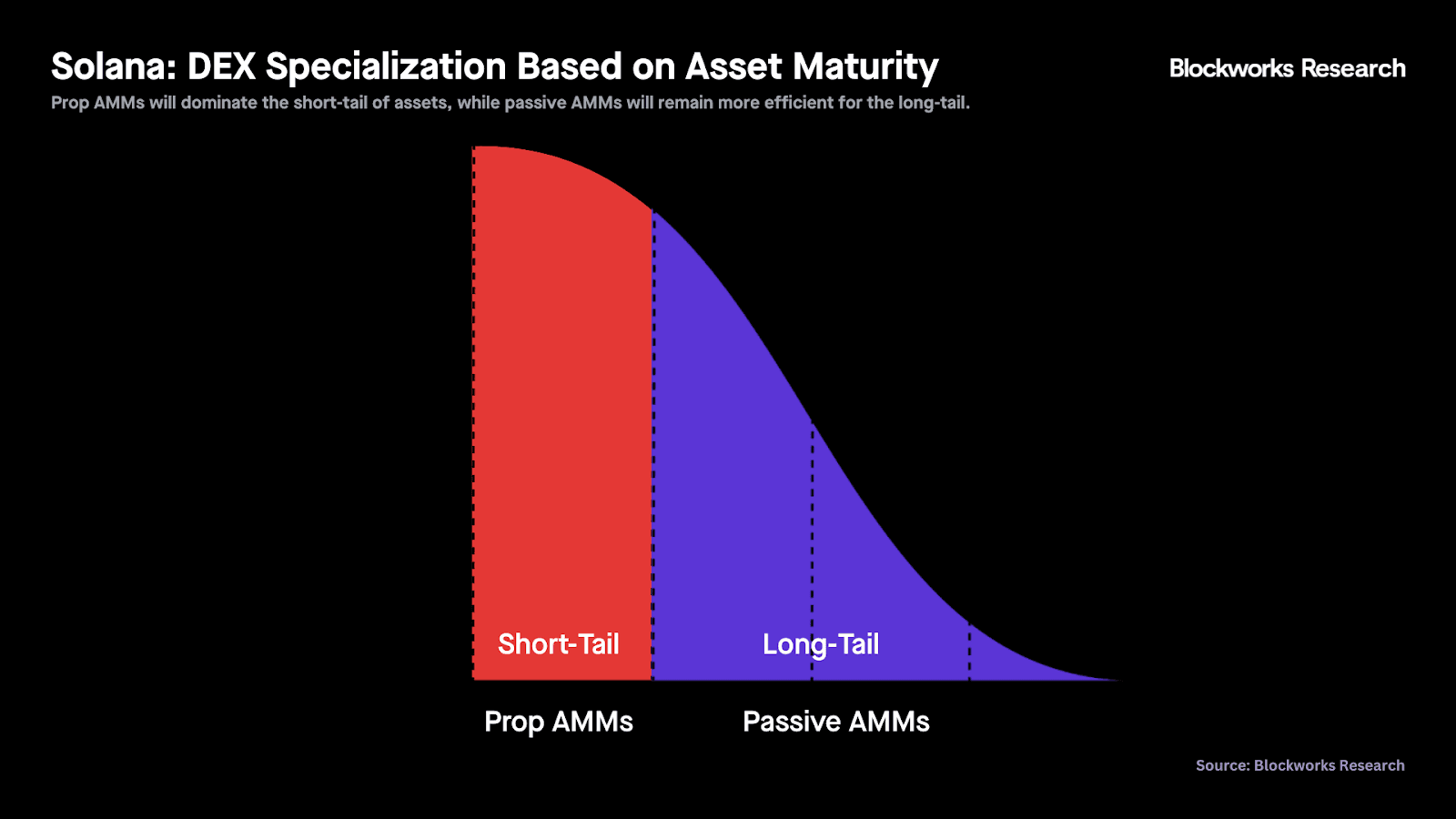

Specialization: Short- vs. Long-Tail

Solana’s DEX dominance will continue to bifurcate based on asset maturity. Prop AMMs will own the short-tail of assets (i.e., highly liquid markets), including SOL-stablecoin and stable-to-stable pairs. In contrast, passive AMMs like Meteora and Raydium will remain more efficient in handling liquidity for long-tail assets. Prop AMMs are virtually absent from this vertical because it’s too risky for them to actively manage liquidity for new assets, many of which don’t even have live oracle price feeds.

Order Flow: Execution vs. Distribution

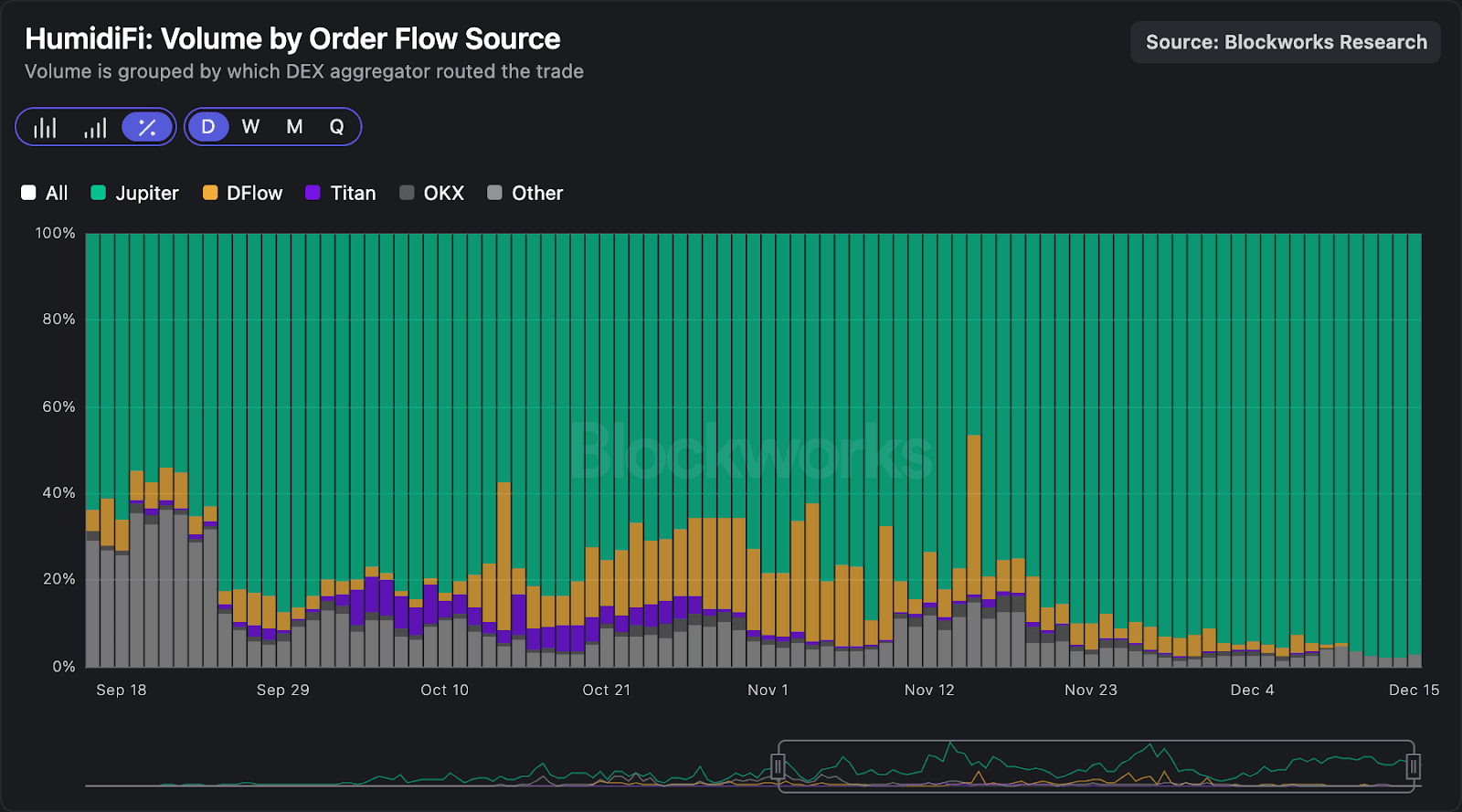

Prop AMMs don’t have a front end, and as such, rely on aggregators like Jupiter and DFlow to interact with their contracts and execute transactions through their pools. In other words, prop AMMs need aggregators for order flow. The chart below shows that HumidFi derives more than 95% of its volumes from DEX aggregators, with similar patterns observed for other prop AMMs like Tessera, GoonFi, and SolFi.

On the other hand, passive AMMs derive less than one-third of their volume from aggregators. Passive AMMs can’t compete with prop AMMs in price execution for major assets, and since liquidity for long-tail assets is largely commoditized, they must compete on distribution.

Putting it all together:

- Prop AMMs must compete on price execution, with aggregators routing to the venue offering the lowest slippage. As we’ll expand on later in the report, transaction ordering is crucial for prop AMMs (which can be viewed as market makers) as there is a race to update quotes before a taker can pick them off. As such, prop AMMs can benefit from moving down the stack and specializing in transaction landing services.

- Passive AMMs must compete on distribution, which means they need to vertically integrate or fade into irrelevance. In contrast to prop AMMs, passive AMMs need to move closer to the user through token issuance platforms (e.g., Pump-PumpSwap, MetaDAO-Futarchy AMM).

We believe passive AMMs that endure will not be perceived as AMMs at all. Instead, they will primarily function as token issuance platforms (e.g., launchpads or ICO platforms), with the AMM merely serving as the monetization layer for token launches. Meteora stands out as a possible exception, though its success still largely reflects its distribution through Jupiter. Below, we lay the most notable examples of this dynamic:

- Pump (launchpad) — PumpSwap

- MetaDAO (ICO platform) — Futarchy AMM

- Jupiter’s DTF (ICO platform) — Meteora

HumidiFi is the clearest example of a vertically integrated prop AMM, benefiting from Nozomi, a transaction landing service built by the same core team (Temporal).

The fundamental differences between prop AMMs and traditional AMMs warrant separate competitive analyses.

Prop AMMs: HumidiFi’s Dominance

Prop AMMs are spot exchanges with actively managed liquidity via oracle updates. Each prop AMM is operated by an individual market maker (no external LPs), who uses highly optimized transactions to update the oracle price, enabling quotes to be adjusted multiple times per second. With over ten prop AMMs now live on Solana, they now account for more than 50% of all spot trading volumes on the chain.

As mentioned in the introduction, Lifinity was the original prop AMM, pioneering the idea of protocol-owned liquidity and quotes adjusted based on oracle prices. Lifinity lost market share quickly after Ellipsis Labs (the team behind Phoenix) launched SolFi in late October 2024, seeing decreasing trading volumes ever since. Lifinity shut down operations on November 20, 2025, a decision that shows how competitive the prop AMM scene has become.

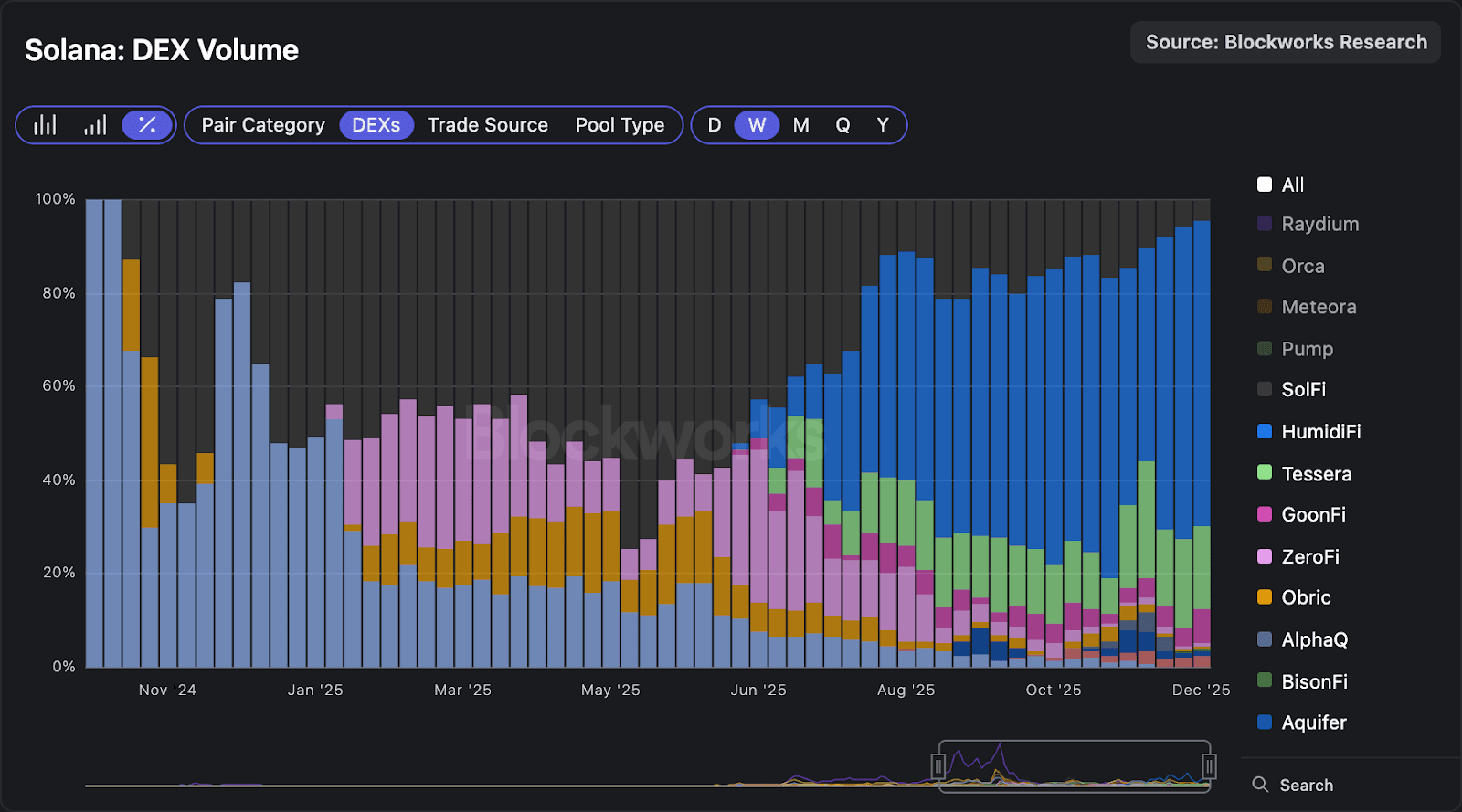

As seen in the chart above, SolFi accounted for nearly half of prop AMM volumes in Q1 and Q2 2025, but HumidiFi quickly rose to the top after its launch in June 2025. HumidiFi now leads prop AMM volumes with a 65% market share, followed by Tessera (18%) and GoonFi (7%).

The core engineering team behind HumidiFi is Temporal, one of the most technically talented teams on Solana. Temporal operates other products at the infrastructure level, including Nozomi (transaction landing service) and Harmonic (block building system aiming to compete with Jito). Aside from Temporal’s contribution, HumidiFi’s cofounder Kevin Pang, who worked at Jump, Paradigm, and Symbolic Capital Partners (SCP), has brought indispensable HFT expertise to the prop AMM.

HumidiFi exemplifies our view that, unlike passive AMMs that need to move downstream and own the end user to capture order flow, prop AMMs are better served by moving downstream into transaction inclusion and ordering infrastructure. Temporal’s infra stack is highly complementary to HumidiFi, improving its ability to optimize compute usage and transaction landing for oracle updates.

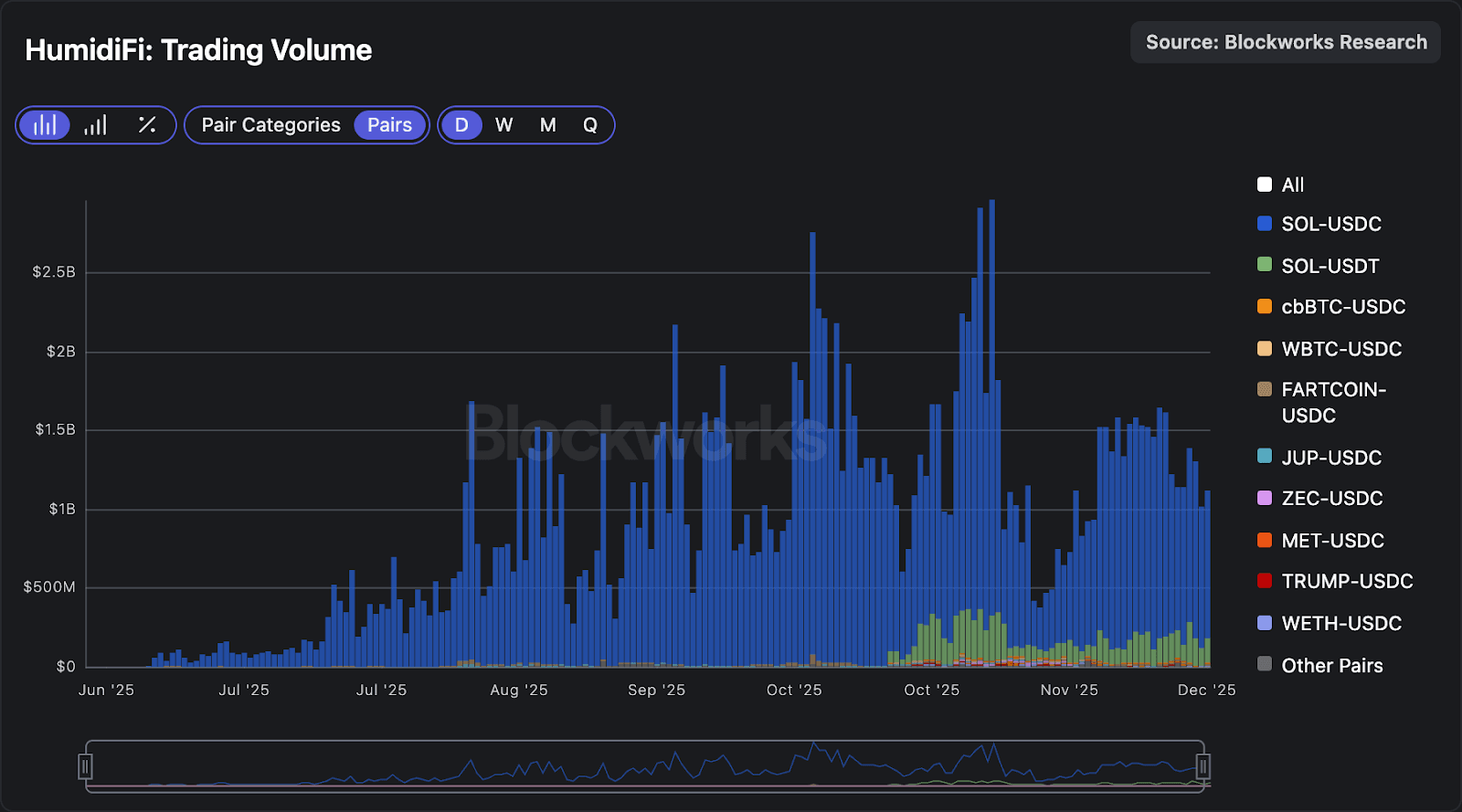

Although HumidiFi has 18 active pools, ~98% of its volume derives from the SOL-USDC (83.3%) and SOL-USDT (14.4%) pairs.

The CEX<>DEX Arbitrage is Moving Onchain

Per Dan Smith, head of data at Blockworks, one of the most interesting second-order effects of prop AMMs dominating SOL-USD volumes is the CEX leg of the CEX<>DEX arbitrage moving onchain. What used to happen:

- Onchain price is $120, Binance price jumps to $125.

- CEX<>DEX arbitrage bot would buy onchain and sell on Binance.

- Arbitrage bot captures the $5 difference.

What happens today:

- Onchain price is $120, Binance price jumps to $125.

- Prop AMMs quickly update their quotes to mirror the $125 on Binance.

- The arbitrage bot now atomically buys from the stale onchain venue and sells to the prop AMMs.

- Arbitrage bot captures the $5 difference.

Since both the onchain venue with a stale price and the prop AMMs are onchain, the arbitrage can now be captured atomically in a single transaction with less risk to the trader. There has subsequently been an uptick in the number of arbitrage bots that are now using flash loans to capture these opportunities.

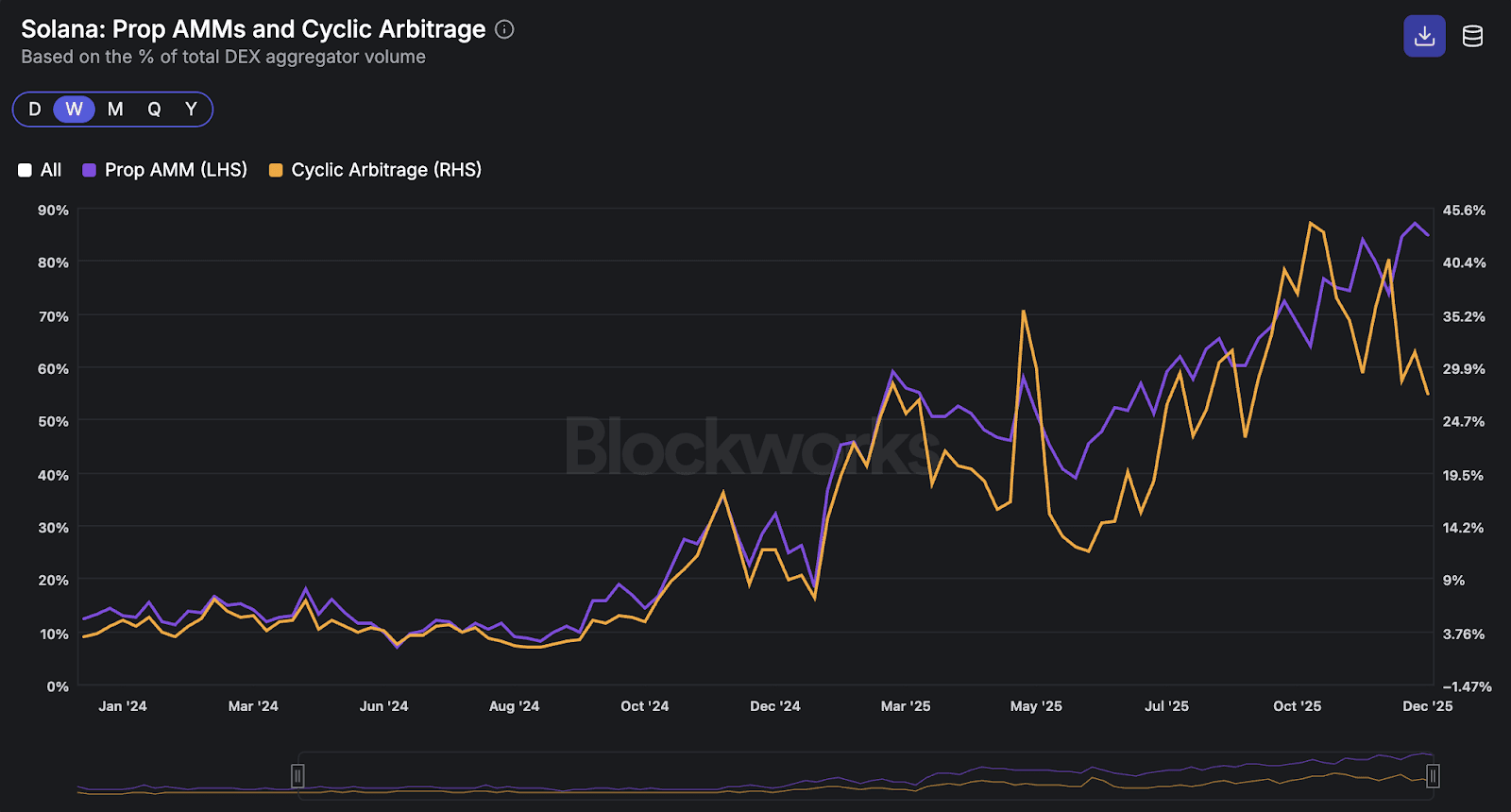

The chart below shows that there is an extremely tight relationship between the percentage of DEX aggregator volume that moves over prop AMMs (LHS) and the percentage of DEX aggregator volume that is cyclic arbitrage (RHS). Here, we define cyclic arbitrage as transactions that have the same input and output token, which captures the arbitrage transactions explained above.

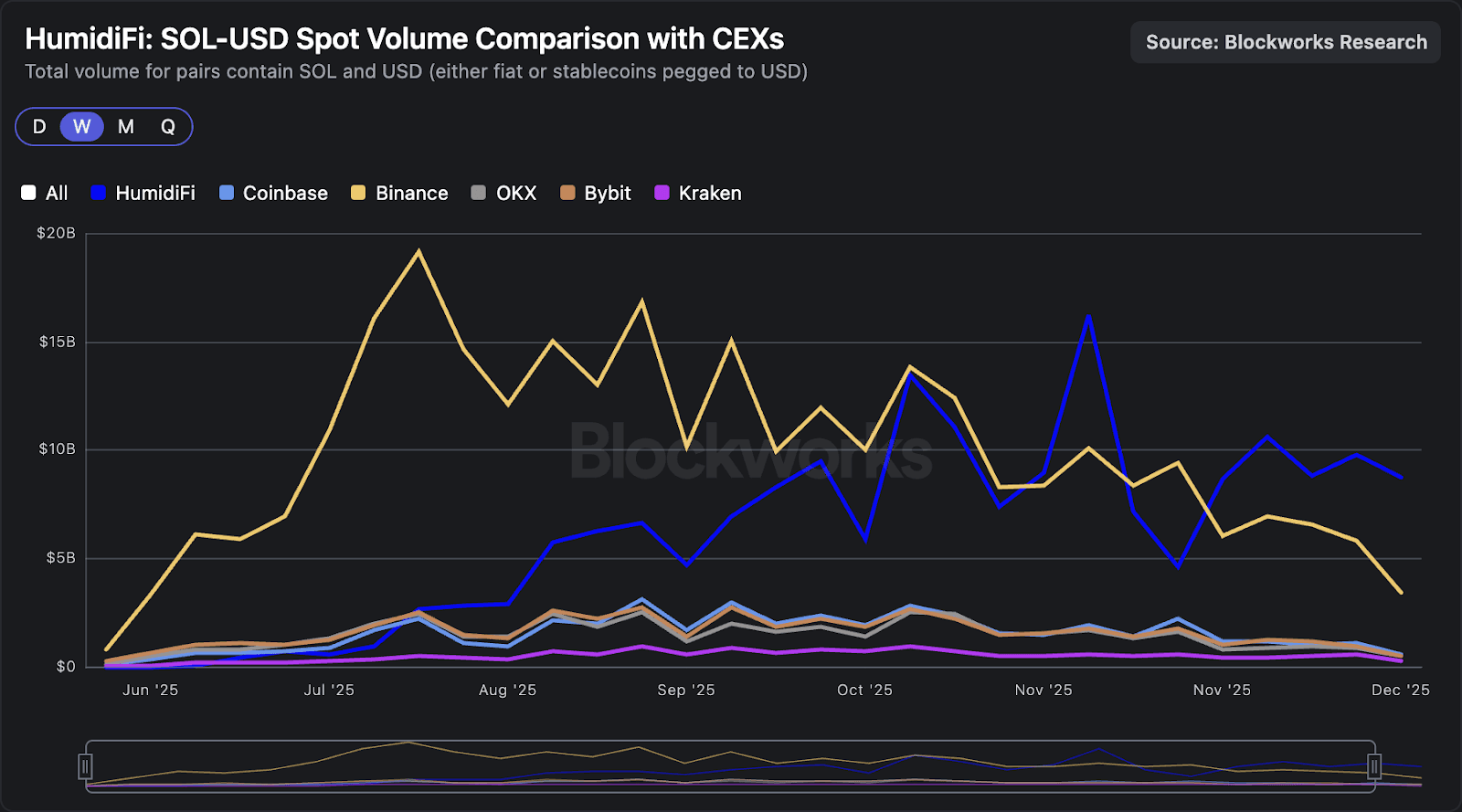

From this trend, prop AMMs now facilitate more trading volume on SOL-USD pairs than CEXs. The chart below shows that HumidiFi has averaged over $9B in weekly SOL-USD volume over the past four weeks, surpassing Binance as the top venue.

Oracle Updates

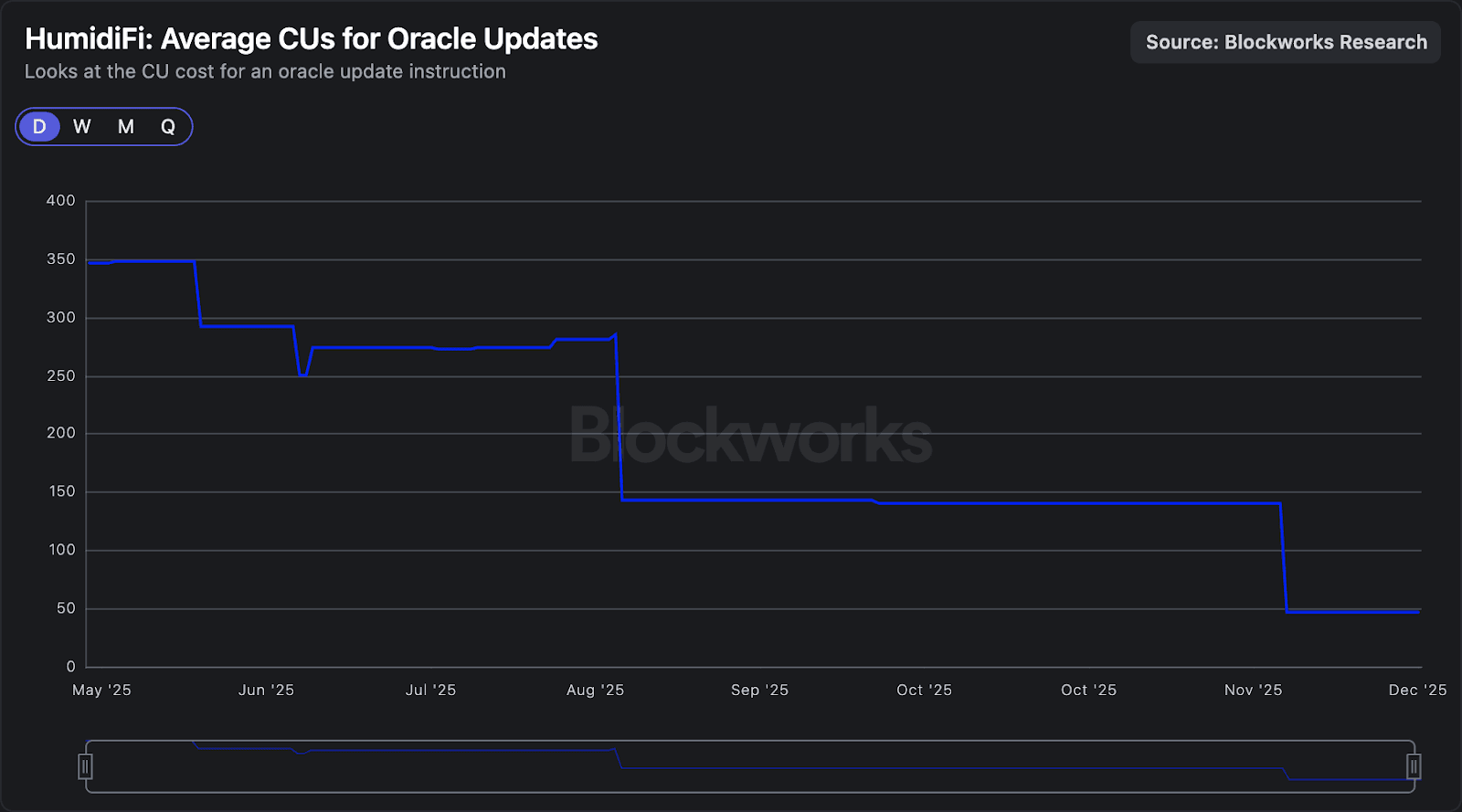

Prop AMMs update their pricing curve through oracle updates, allowing their quotes to be more "fresh" compared to passive AMMs. Since oracle updates are about 100x less compute-intensive than swaps, the market maker in a prop AMM can push quick updates to their internal pool parameters many times a second, enabling them to quote tighter spreads compared to passive AMMs with pooled liquidity.

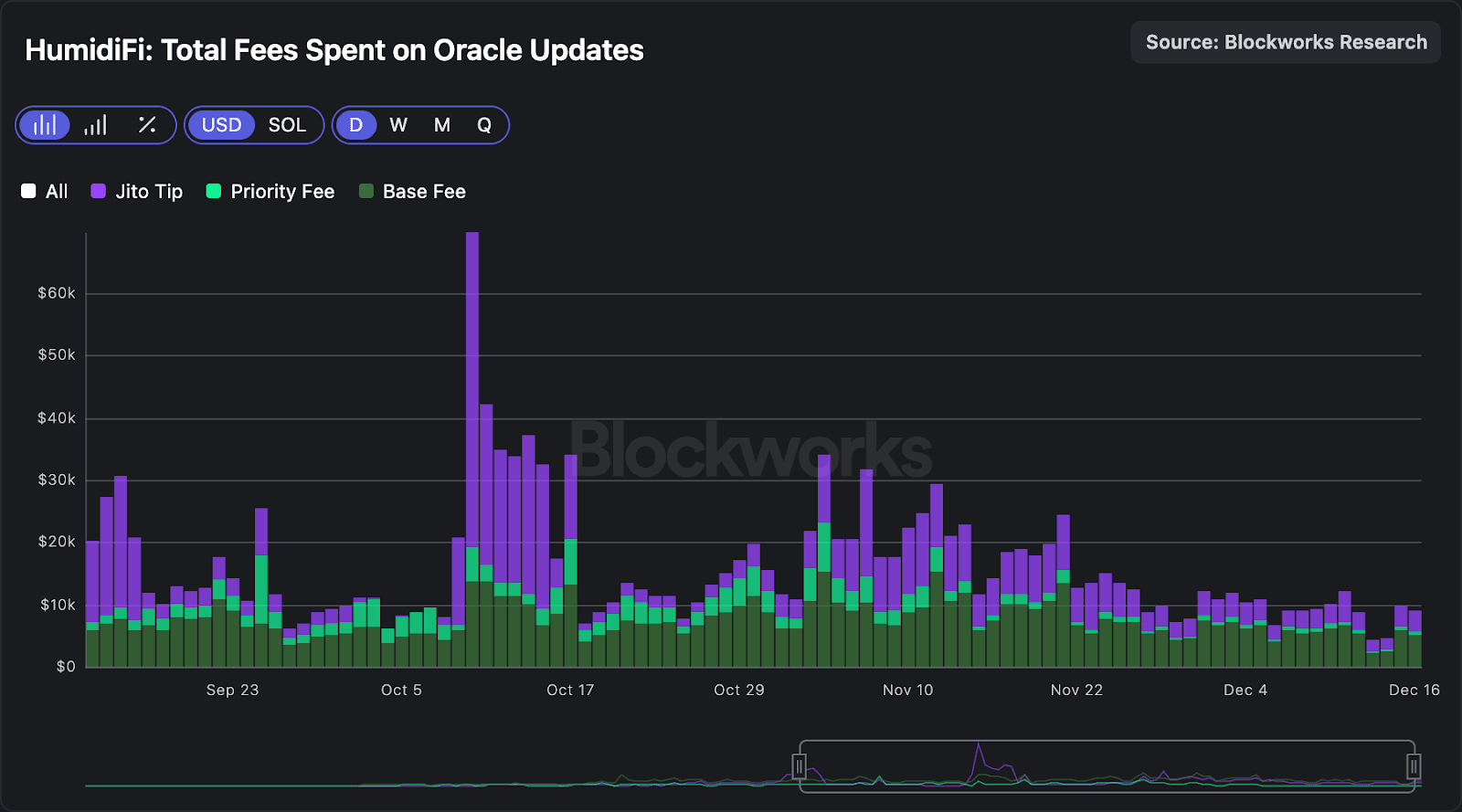

These oracle update transactions are highly optimized to consume as few compute units (CUs) as possible. Since transactions in a block are ordered by the priority fee paid per CU, a more lightweight oracle update enables the transaction to be ordered higher in a block with a lower total transaction fee. Transaction ordering is important as there is a race to update quotes before a taker can pick them off. The chart below shows HumidiFi has aggressively optimized its oracle-update instruction, reducing compute to 47 CUs, a >85% drop versus launch in June.

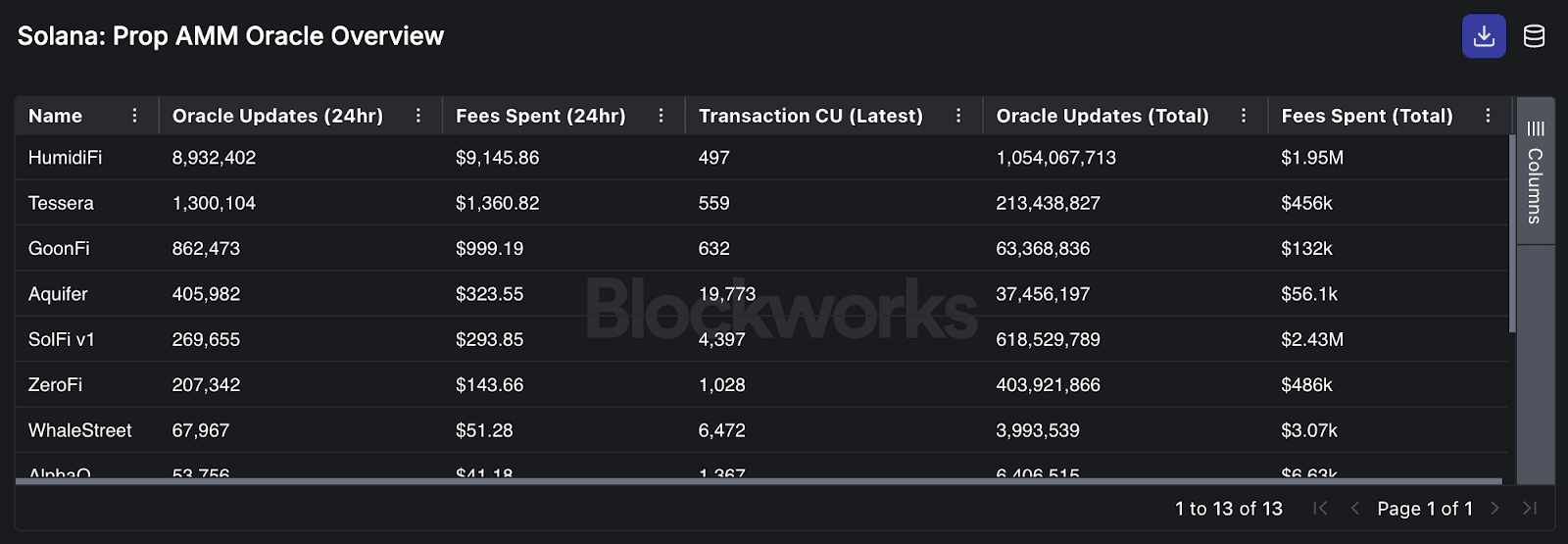

That said, the chart above only considers CU consumed by the oracle update instruction itself. The more relevant metric is total transaction CU, since a prop AMM can’t update the oracle without the full transaction, including any additional program calls and account-handling overhead required to execute the update.

The table below shows HumidiFi has reduced its oracle update transactions to <500 CUs, the lowest in the cohort. Aside from HumidiFi, only Tessera and GoonFi come in below 1,000 CUs.

Despite paying roughly $0.0016 per oracle update transaction, HumidiFi has averaged ~6M updates per day (about 70 updates per second!) since pushing total compute below 500 CUs. At that rate, HumidiFi is spending $9-10k daily on transaction inclusion fees (base fee + priority fee + Jito tip).

HumidiFi’s Revenue

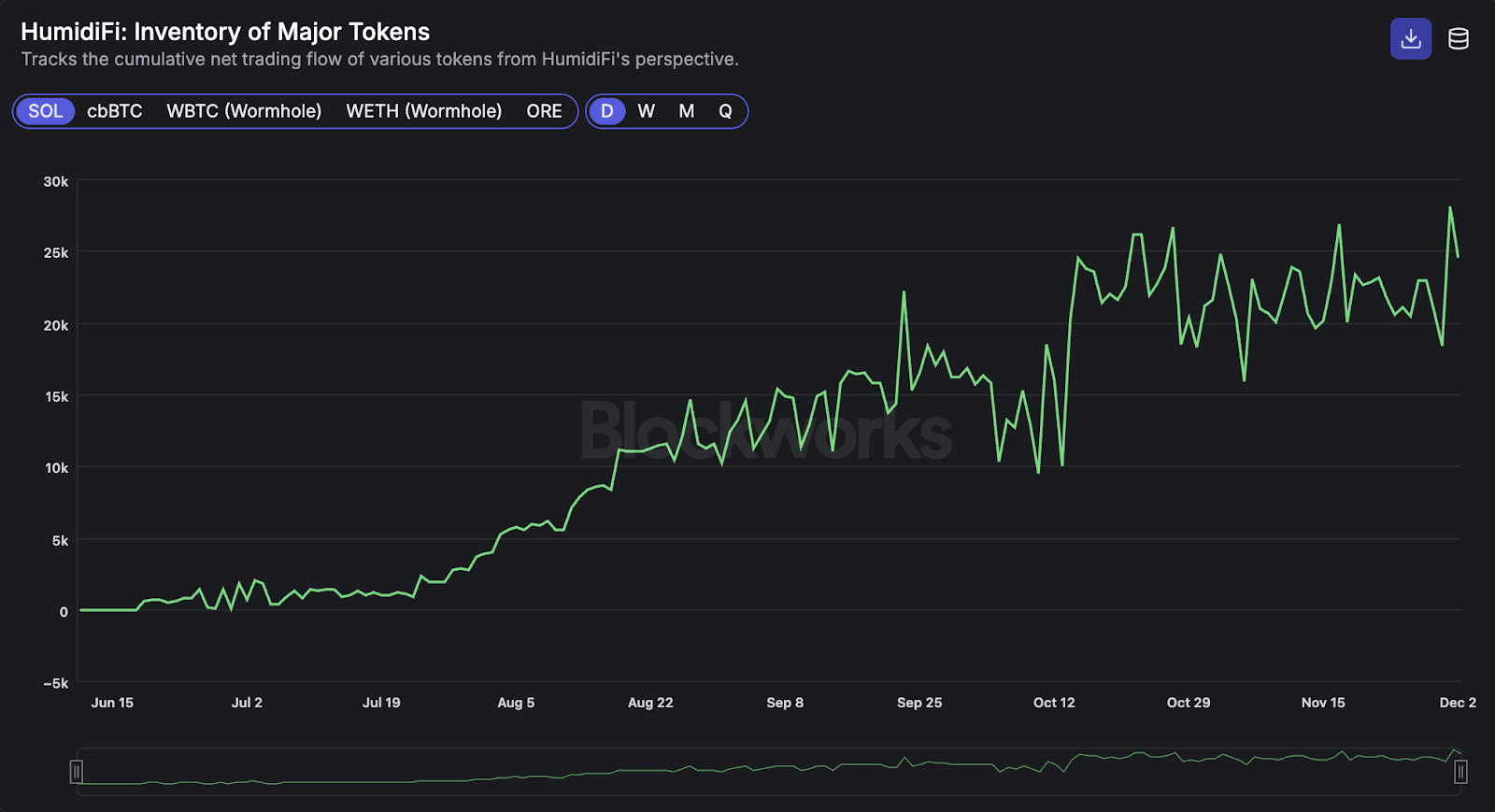

While HumidiFi’s revenue isn’t public, we can estimate it by looking at their token inventory delta since inception. The core idea is that, since HumidiFi effectively acts as a market making desk (there is a single LP in the prop AMM), every trade against it has a winner and a loser. Over time, the MM’s net inventory change reflects trading PnL. As such, we can track the cumulative net trading flow of various tokens from HumidiFi's perspective as a proxy for revenue.

The chart below shows HumidiFi’s cumulative net trading flow in SOL (where 98% of its volume comes from), which amounted to ~25k SOL as of Dec. 2, 2025. By measuring daily changes in HumidiFi’s SOL inventory and multiplying those balances by the prevailing SOL price each day, we estimate cumulative trading revenue of approximately $4.1M from inception in June through Dec. 2, 2025, translating to an average daily gross revenue of ~$24k.

The method above estimates onchain trading PnL, but it can diverge from true net revenue if HumidiFi is hedging inventory on CEXs, with funding, fees, and hedge PnL accruing offchain.

Another important caveat is that the estimate above reflects gross revenue. After subtracting the $9-10k per day in oracle update fees, HumidiFi’s implied net revenue is approximately $14-15k per day. Again, we must reiterate that this is just an estimate based on the available onchain data. A more accurate revenue estimate would require incorporating any offchain hedging activity, as we explained above.

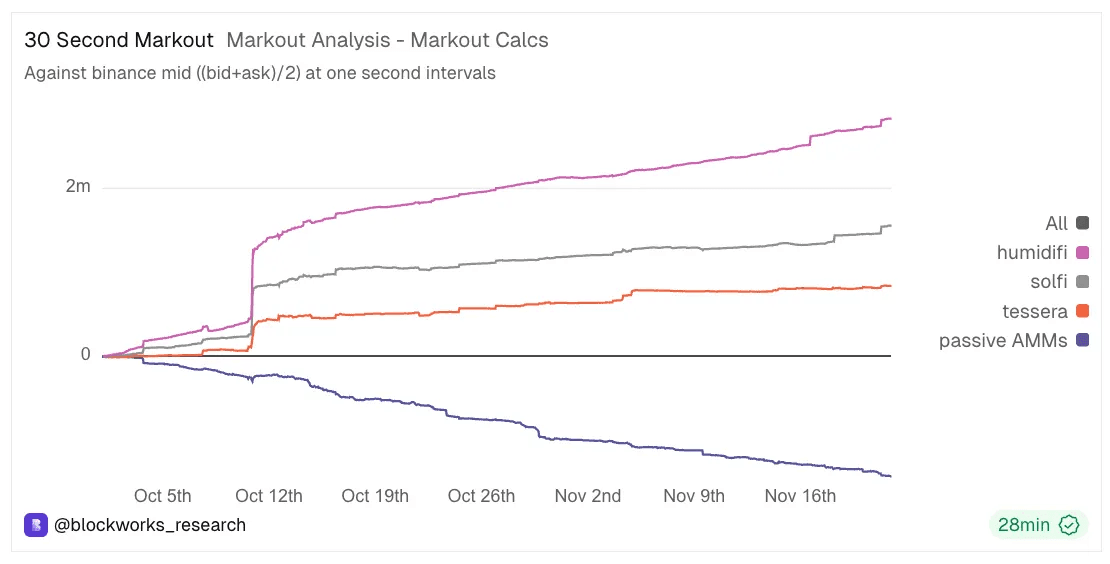

Markouts: Active vs. Passive Liquidity

Markouts are a measurement of execution quality and adverse selection for market makers, making it a useful assessment for prop AMMs who compete on the same strategy (provide delta-neutral top-of-book liquidity).

For this analysis, our data team focused only on the SOL-USDC pair trading on HumdiFi, SolFi, and Tessera. A 30-second interval post execution was used to benchmark the onchain fill prices against the Binance SOL-USDC mid-price ((best_bid+best_ask)/2) at 1 second book snapshots. PnL was then calculated as ((binance_mid_future - exec_price) / exec_price) * mm_side * volume_usd.

Here, mm_side is defined from the maker’s perspective: +1 when the prop AMM buys SOL (taker sells SOL into it) and -1 when the Prop AMM sells SOL (taker buys SOL from it). Additionally, we should note that using the Binance mid-price as the reference introduces potential cross-venue basis and timing mismatch versus onchain execution, so markouts should be interpreted directionally rather than as an exact decomposition of realized PnL.

The period analyzed covers Oct. 1 to Nov. 22, 2025.

A positive cumulative PnL indicates the maker is executing soft/non-toxic flow, and the price moved in the maker’s favor 30 seconds after the trade. In contrast, a negative cumulative PnL signals adverse selection, where the price moved against the prop AMM following the trade.

The chart below shows that prop AMMs ran positive 30 second PnLs over the period, which indicates these prop AMMs are successfully avoiding toxic flow and capturing spread from benign users. We also included an aggregate of passive AMMs on Solana, demonstrating that prop AMMs showcase significantly better markouts than their predecessors.

Passive Liquidity in SOL-USD: A Losing Game

Our markout analysis shows that active liquidity management protects the capital from being picked off by toxic takers looking to profit on mispriced assets.

What follows is that a majority share of SOL-USD volume on traditional, passive AMMs is not “organic” user flow, but arbitrage against stale quotes. Passive (whether CLMM or constant product) AMM curves will always lag fast-moving reference prices in prop AMMs. That lag creates a mechanical opportunity for arbitrage bots to step in and trade against the passive pool whenever there’s a mispricing.

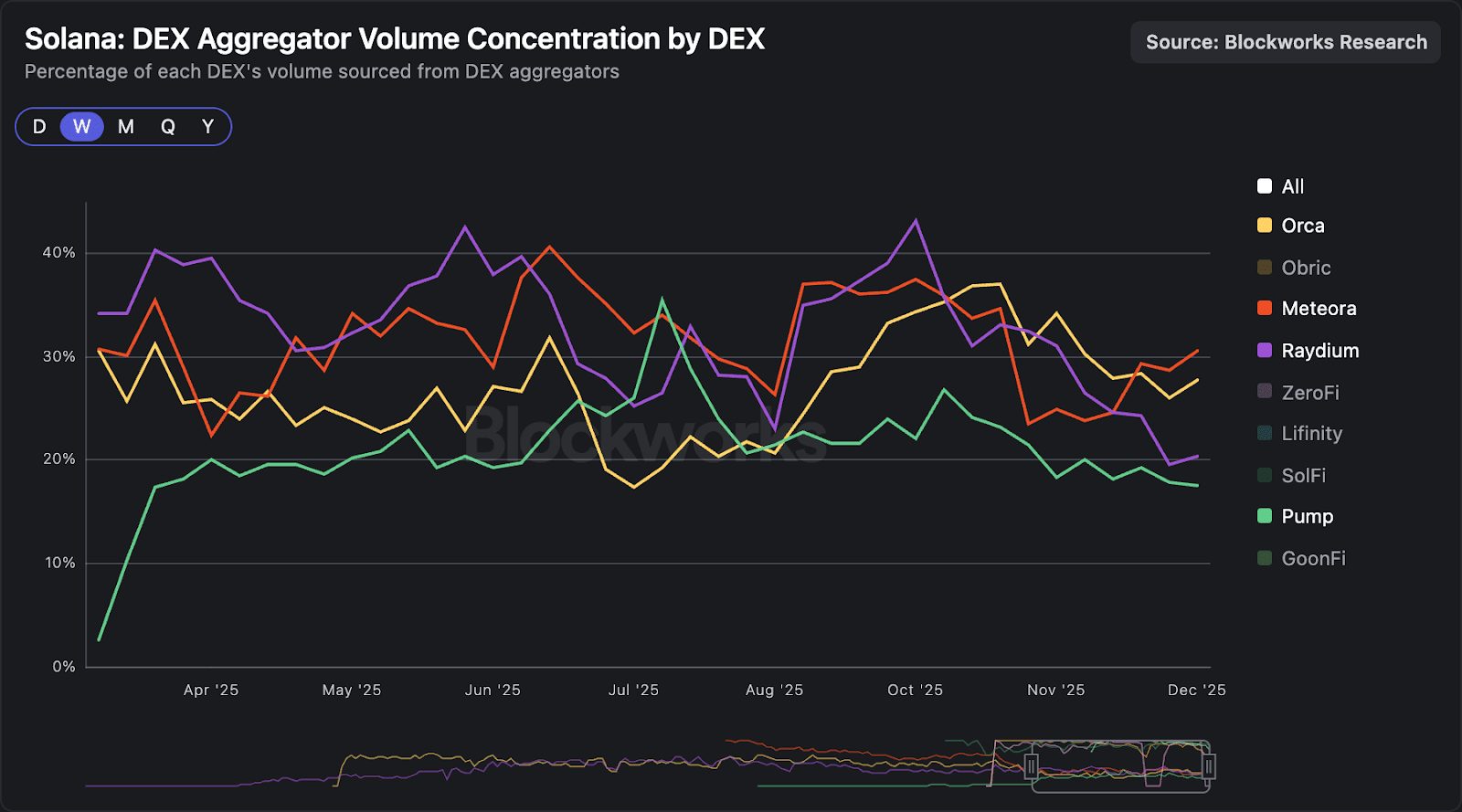

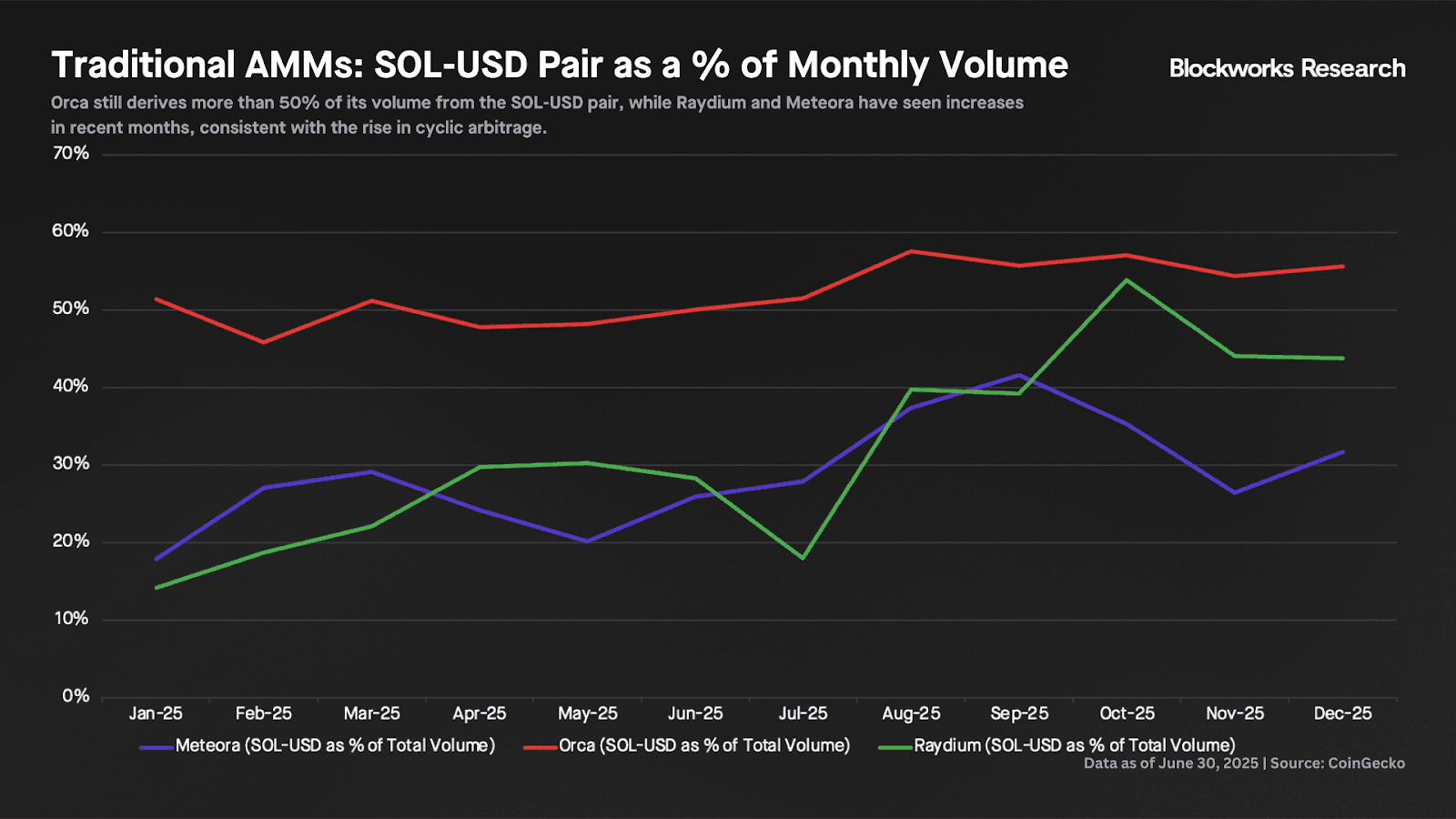

Looking at traditional AMM volume composition, Orca still derives over 50% of its volume from SOL-stablecoin pairs. Meanwhile, Meteora and Raydium (two venues whose activity had been heavily skewed toward memecoins) have seen SOL-stablecoin volumes rise in recent months, consistent with the growing share of cyclic arbitrage mentioned earlier.

Of note, newer AMMs like Pump’s PumpSwap or MetaDAO’s Futarchy AMM don’t have any active pools for highly liquid pairs like SOL-stablecoin.

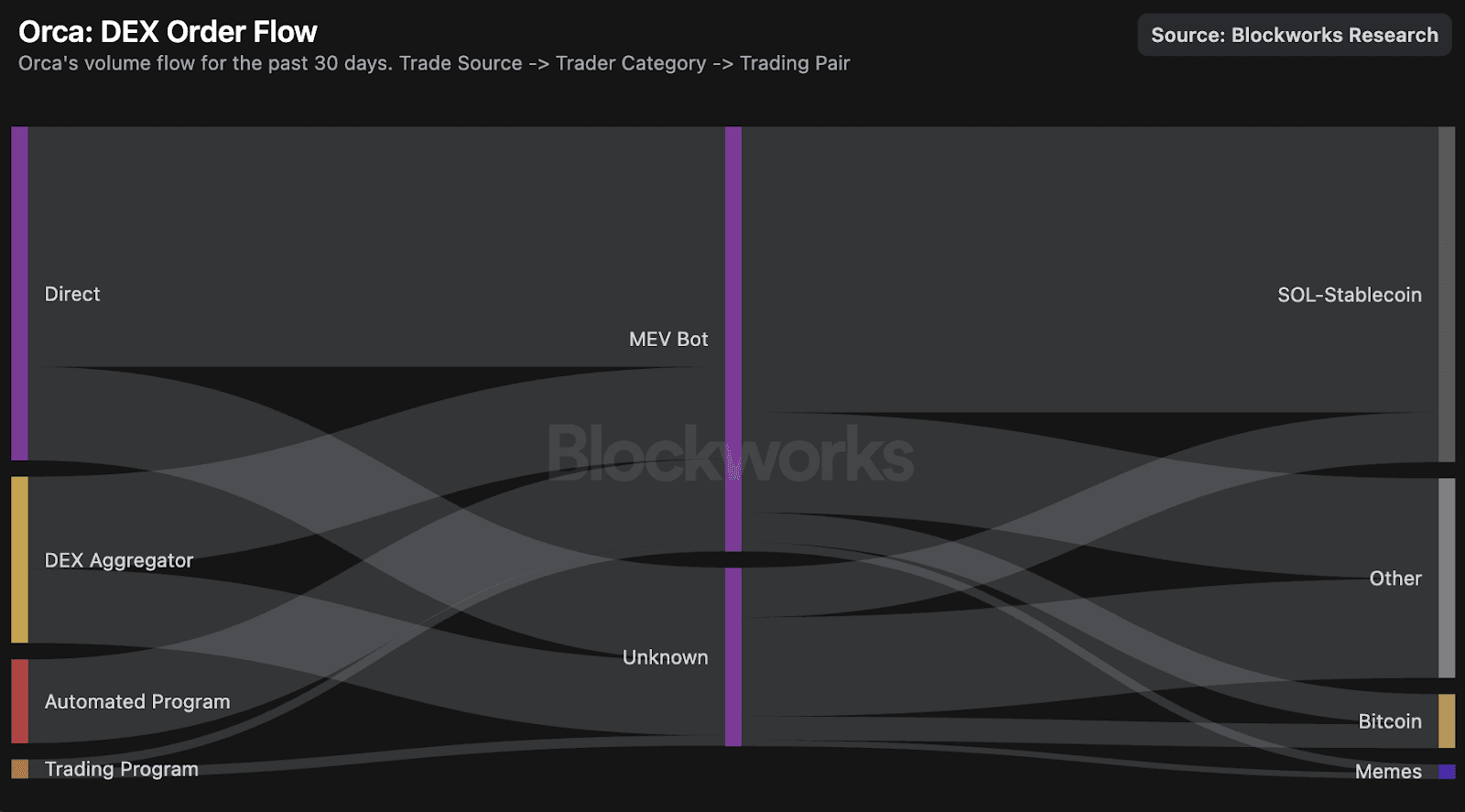

At a more granular level, the order flow diagram below shows that at least 85% of Orca’s SOL-stablecoin volume is attributable to “MEV bot” activity. However, most of this flow appears to come from Wintermute’s public market making bot rather than purely opportunistic arbitrage against stale quotes.

Absent incentives and assuming rational, profit-seeking actors, LP capital on traditional AMMs for highly liquid pairs (SOL-stablecoin, stable-to-stable, BTC-stablecoin, etc.) should naturally contract over the coming months.

That said, traditional AMMs can still retain an important role for the short-tail of assets. In particular, they act as fallback, always-available liquidity even if prop AMM liquidity pulls back during stress periods.

The End of the Standalone DEX

Even though this is a DEX report, one of the core ideas we want to transmit is that the standalone DEX model is dead outside of prop AMMs. Crypto investors have historically analyzed protocols in silos, in part because Ethereum historically produced a clear category winner: Aave in lending, Uniswap in DEXs, Lido in LSTs, and so on.

It was natural to apply the same mental model to Solana, but it doesn’t work. Firstly, Solana is incredibly more competitive than Ethereum, and it has been rare to see a protocol dominate in its vertical for a durable period. Second, as we have shown throughout the report, market structure on Solana has pushed traditional, passive AMMs towards long-tail assets, where they can be useful to support day one liquidity and enable onchain price discovery.

The problem is that DEXs have no moat, or at least not on their own. AMM liquidity is increasingly commoditized, and it is trivial to spin up a new AMM with constant or concentrated liquidity pools. To win order flow as a traditional DEX, you must sit closest to the end user, meaning you must own distribution, and hence become the token issuance layer.

Following this logic, we won’t think of the “winning spot DEXs” as DEXs at all, but as token issuance platforms. This model can take two forms:

- High-velocity launchpads for memecoins (e.g., Pump).

- ICO platforms that enable onchain capital formation for more legitimate projects (e.g., MetaDAO, Jupiter’s DTF).

Launchpads

We’ve covered launchpads extensively in the past (see here and here), emphasizing the importance of owning the consumer relationship through a prosumer-focused, mobile-first frontend. One idea we hadn’t explicitly formalized, however, is that the proliferation of launchpads has disrupted passive AMMs nearly as much as prop AMMs have, but through a different vector.

Prop AMMs have captured market share in the short-tail of assets. Launchpads, meanwhile, have become the token issuance layer for the long-tail, owning distribution and order flow for those assets. Evidence of this disruption is that the three largest passive AMMs on Solana (Raydium, Orca, Meteora) debuted a launchpad-related product in the past year.

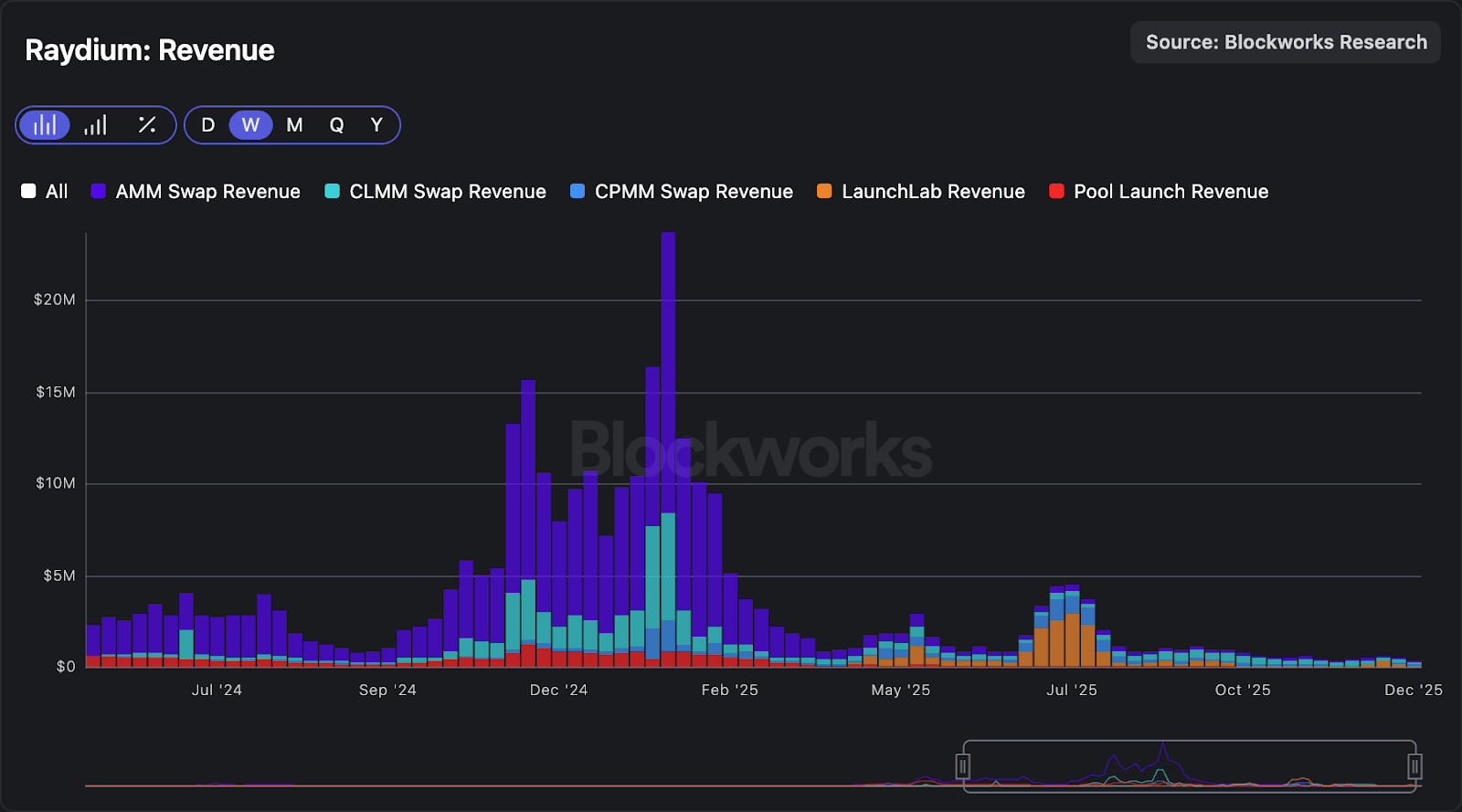

Raydium

After Pump introduced the PumpSwap AMM and cut Raydium out of the graduation flow, Raydium responded with LaunchLab, a whitelabel solution for integrators to easily spin up their own launchpads. Raydium takes a 25bps program fee on volume from any third party launchpad built using LaunchLab, with graduated tokens redirected to Raydium’s AMM. Raydium’s most notable customer has been Bonk.

Despite a brief surge in LaunchLab’s share in July 2025 via Bonkfun, Pump has remained the dominant launchpad, sustaining >90% market share. LaunchLab had reclaimed some share in recent days, but absent a clear structural catalyst, historical patterns suggest these gains are more likely to be sporadic than durable.

Orca

Orca has historically struggled to capture a meaningful share of memecoin volume. Since 2023, it has derived over 50% of monthly volume from the SOL-USD pair, with the remainder increasingly split across project tokens, stablecoin swaps, BTC-USD, and composite tokens (e.g., JLP). That positioning has left Orca in a difficult spot for more than a year: it ceded share to Raydium as Pump-driven memecoin issuance accelerated in Q1 2024, and the protocol’s main bull case (dominance in SOL-USD and other highly liquid pairs) has since been undermined as prop AMMs took over all short-tail liquidity.

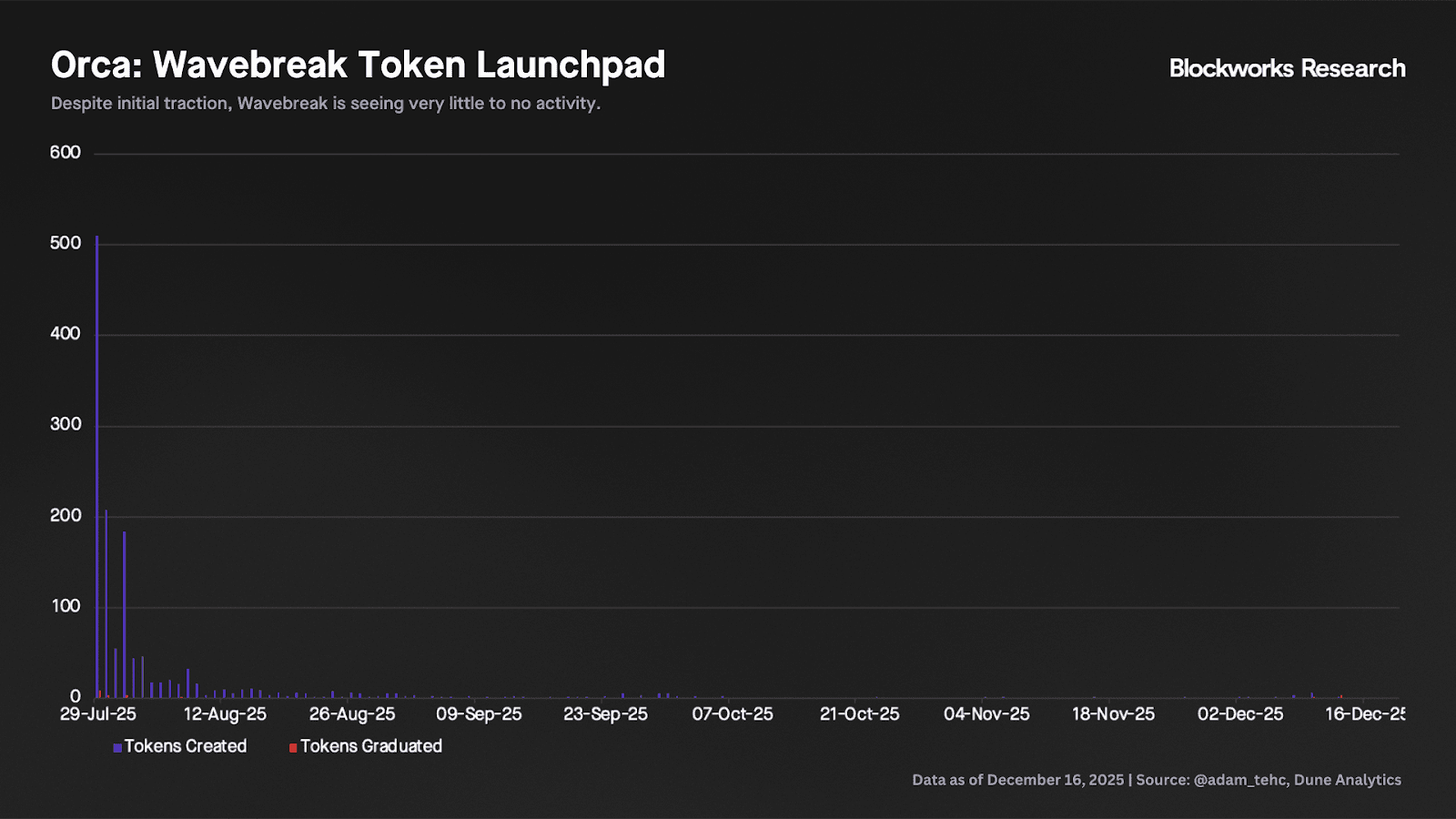

In July 2025, Orca introduced Wavebreak, a launchpad marketed around “proprietary anti-bot technology,” with DeFiTuna’s TUNA serving as the first launch. However, aside from initial traction following the launch, Wavebreak has seen almost no activity since late August 2025.

Meteora

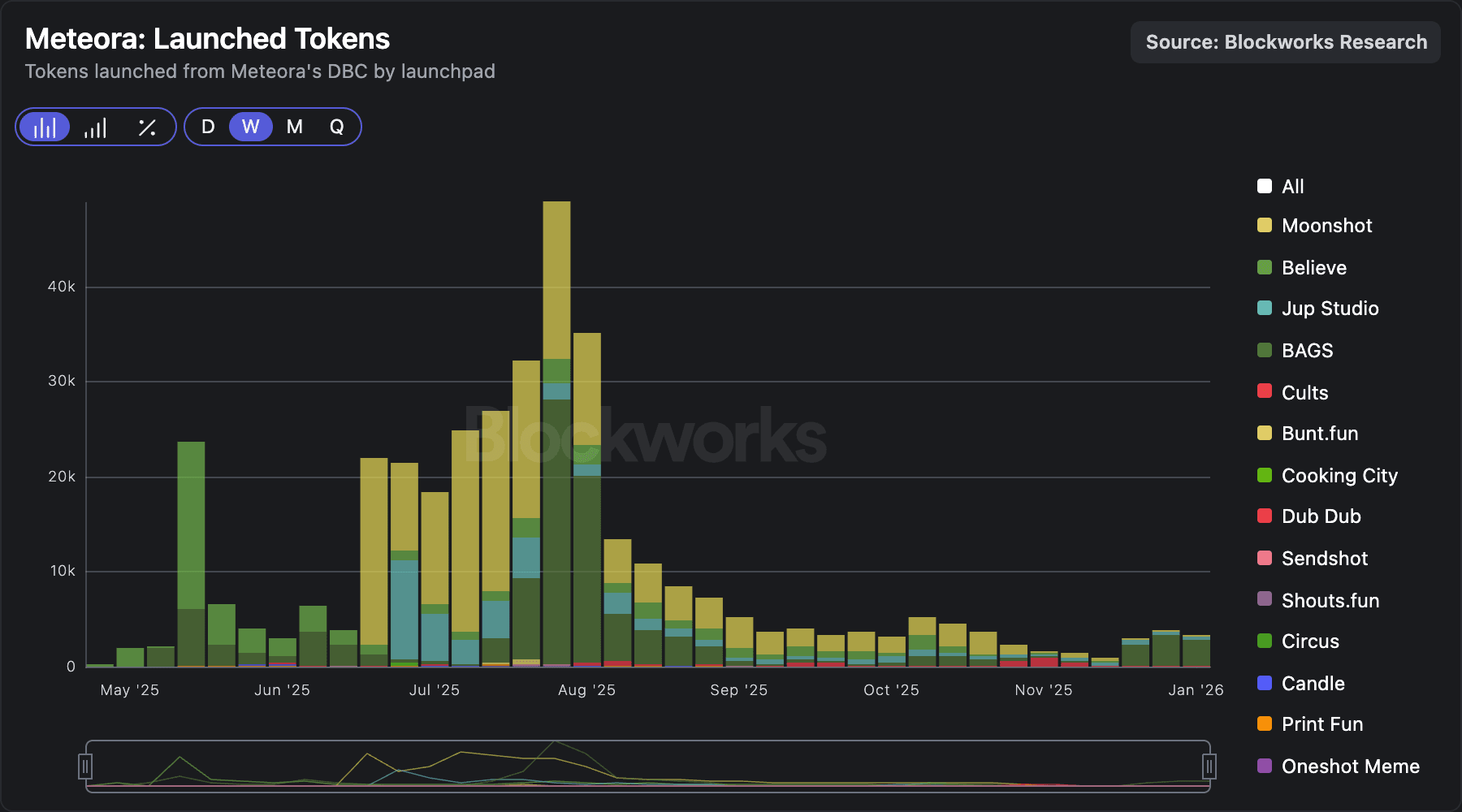

Meteora is operated in close partnership with the Jupiter team, which has become the gateway for most retail users to trade onchain. To expand its product offering beyond its AMM primitive, Meteora partnered with Moonshot in August 2024 to introduce a launchpad. In April 2025, Meteora launched a Dynamic Bonding Curve (DBC), with the protocol capturing 20% of trading fees from launchpad activity. The team has onboarded new partners since, including Believe, BAGS, and Jup Studio.

That said, Meteora’s launchpad activity appears to be following the same pattern as LaunchLab and Wavebreak. Despite a pickup in token launches through Q2 and Q3 2025, usage has rolled over, with activity declining sharply since September.

Pump

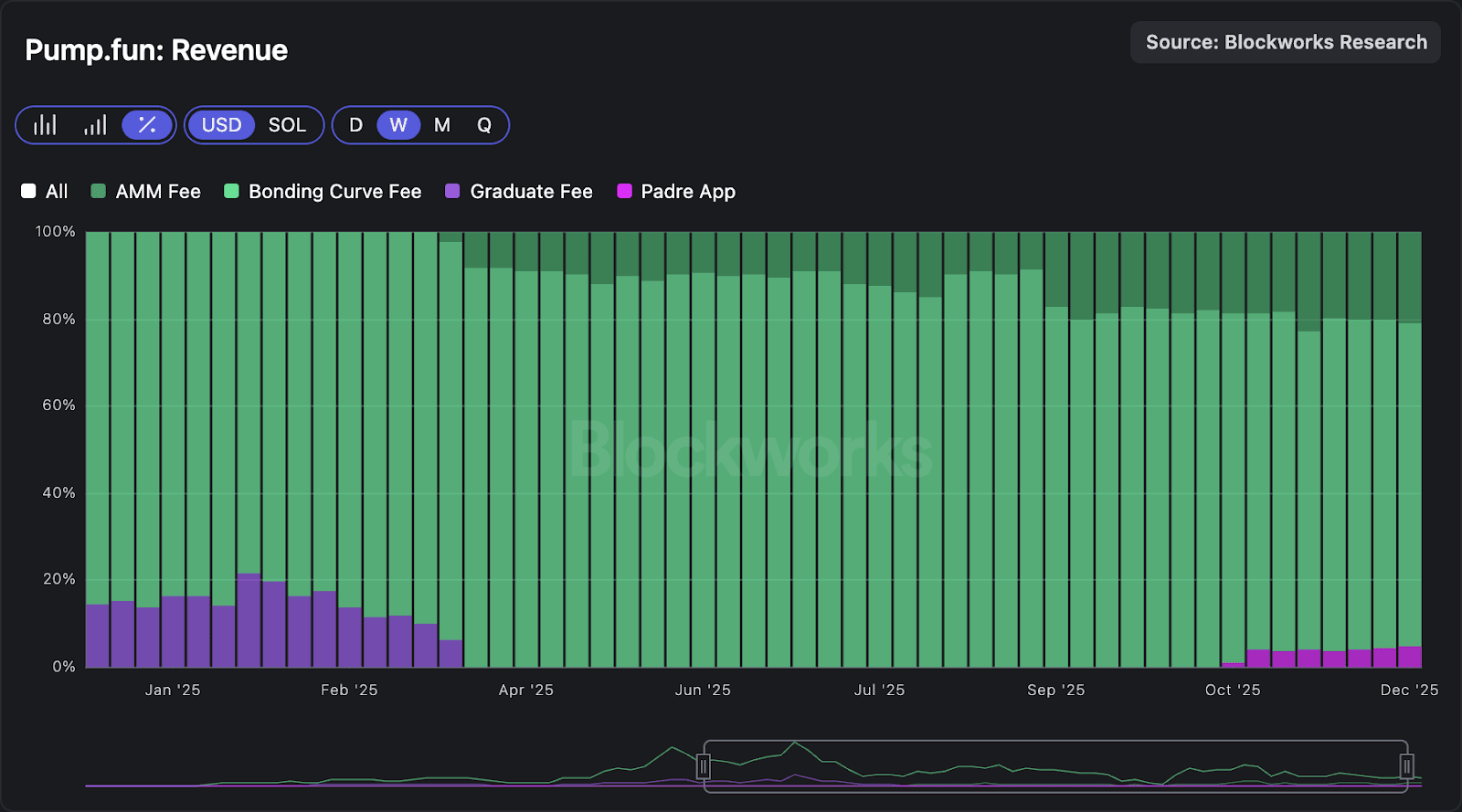

As noted above, Pump remains the dominant launchpad by a wide margin, something we’ve extensively discussed in prior work, so we’ll focus on what’s most interesting here. Pump was arguably the first embodiment of the vertically integrated DEX thesis, built top-down from issuance, instead of the other way around. After securing distribution and order flow through its launchpad, Pump introduced its passive AMM to capture downstream trading activity.

That integration has meaningfully diversified Pump’s revenue away from the bonding curve mechanism. The chart below shows that Pump now monetizes activity across the entire token lifecycle, with AMM fees now contributing over 20% of its total revenue.

ICO Platforms

The combination of low-float tokens getting punished in liquid markets and a more favorable regulatory environment has sparked a revival in ICOs over the past year. Unlike memecoin launchpads, where success is driven by high-velocity throughput of token launches, curated ICO platforms still want consistent launch volume, but place far more weight on founder quality, credibility, and longer-term retention of both founders and investors.

MetaDAO

We continue to maintain our thesis on MetaDAO as the protocol best positioned to win this market. As we concluded in our September report, “MetaDAO was built from first principles and is meaningfully different from every other solution in the market. Notably, MetaDAO aims to solve one of the industry’s most important problems today: enforceable tokenholder rights.”

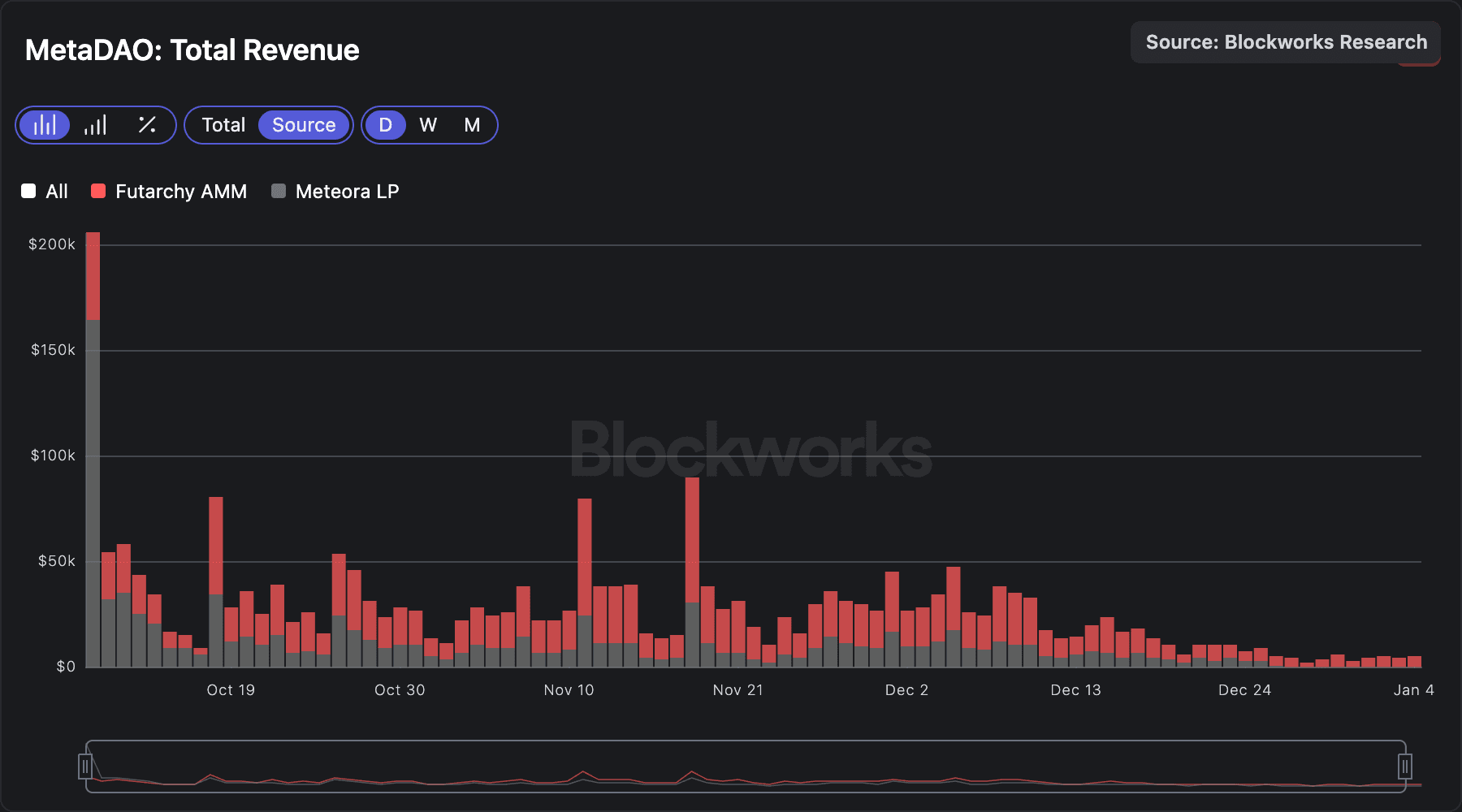

Unlike launchpads, MetaDAO doesn’t have a bonding curve. Instead, it monetizes ICOs through swap fees on its Futarchy AMM and its LP position on Meteora. The Futarchy AMM charges a 0.5% fee on volume, which was originally split evenly between MetaDAO and the project raising (e.g., 0.25% to MetaDAO, 0.25% to Avici). On Dec. 28, after mutual agreement with teams, the split was retroactively adjusted so that the full 0.5% now accrues to MetaDAO.

Since the Futarchy AMM went live on October 10, MetaDAO has generated $2.4M in revenue, with roughly 60% coming from the Futarchy AMM and 40% from its Meteora LP position.

MetaDAO is perhaps the clearest expression of our “death of the standalone AMM” thesis. Nobody thinks of MetaDAO as an AMM. Still, the Futarchy AMM functions as the protocol’s main monetization layer, enabled by MetaDAO’s control of the token issuance layer and the distribution that comes with it.

Jupiter and Meteora

On December 3, Jupiter debuted its Decentralized Token Formation (DTF) platform with HumidiFi’s WET. Projects launching through DTF must undergo a vetting and selection process by the Jupiter team, underscoring the difference in approach between high-velocity launchpads and curated ICO platforms.

WET’s sale was conducted on a first-come, first-served basis across multiple phases (whitelisted addresses, JUP stakers, and public sale), with the first two phases priced at $50M FDV and the public sale at $69M FDV. Of note, Jupiter has indicated that future launches may experiment with other sales mechanics. After the sale concludes, any remaining allocations are locked transparently using Jup Lock, and a liquidity pool on Meteora is immediately provisioned from a portion of the sale proceeds, to ensure liquidity for the tokens.

Although Meteora’s launchpad efforts didn’t pay off, we think it is better positioned than Raydium and Orca due to its relationship with Jupiter, with far better distribution and BD. For example, Meteora was chosen as the go-to venue for high profile launches, such as TRUMP or WLFI, though the volume and revenue generated by these types of tokens is highly cyclical.

Valuation Framework

While it is tempting to value Solana DEX tokens on a trailing price-to-sales basis, doing so in isolation is of limited practical value. A simple comparison that labels one asset as “cheapest” within the cohort ignores the fact that the Solana spot trading landscape is still evolving rapidly, and forward-looking growth will be determined by where volumes consolidate rather than where they have historically accrued. As a result, understanding the direction of market structure is a prerequisite for any meaningful valuation exercise. Moreover, not all tokens are created equal, and some have stronger tokenholder guarantees than others.

For investors looking to capture upside from Solana’s spot trading landscape, we see two primary paths:

- Prop AMMs, which should continue consolidating share in the short tail of assets. Although the SOL-USD pair drives the majority of volume today, we expect prop AMMs to also dominate other categories that will become meaningful for Solana in the months ahead, such as tokenized stocks (xStocks).

AlphaQ is an interesting example of a prop AMM starting to specialize beyond the SOL-USD pair. It operates as a “stableswap” prop AMM and has been gaining market share alongside a new Solana CLOB, Manifest. That said, exogenous demand for volatile asset pairs beyond SOL-USD remains limited today, so the market likely needs more time to mature before prop AMMs can realistically capture meaningful volume in xStocks, wrapped BTC, etc.

Over time, we expect prop AMMs to translate their innovations from just spot trading to derivatives via perps platforms. Ellipsis Labs already announced Phoenix Perpetuals, and it is likely that others such as HumidiFi will enter this market if Phoenix sees traction.

- Token issuance platforms with vertically integrated AMMs, where the AMM is primarily a monetization layer for launches. Depending on investors’ desired exposure, this bet can be expressed through high-velocity launchpads like Pump, or ICO platforms like MetaDAO that enable onchain capital formation. Given the current market environment, we are more constructive on the growth prospects of ICO platforms for legitimate projects.

Against this backdrop, we find it increasingly difficult to justify a long-term bullish view on DEXs that do not fit into either of these categories, with Raydium and Orca being the clearest examples.

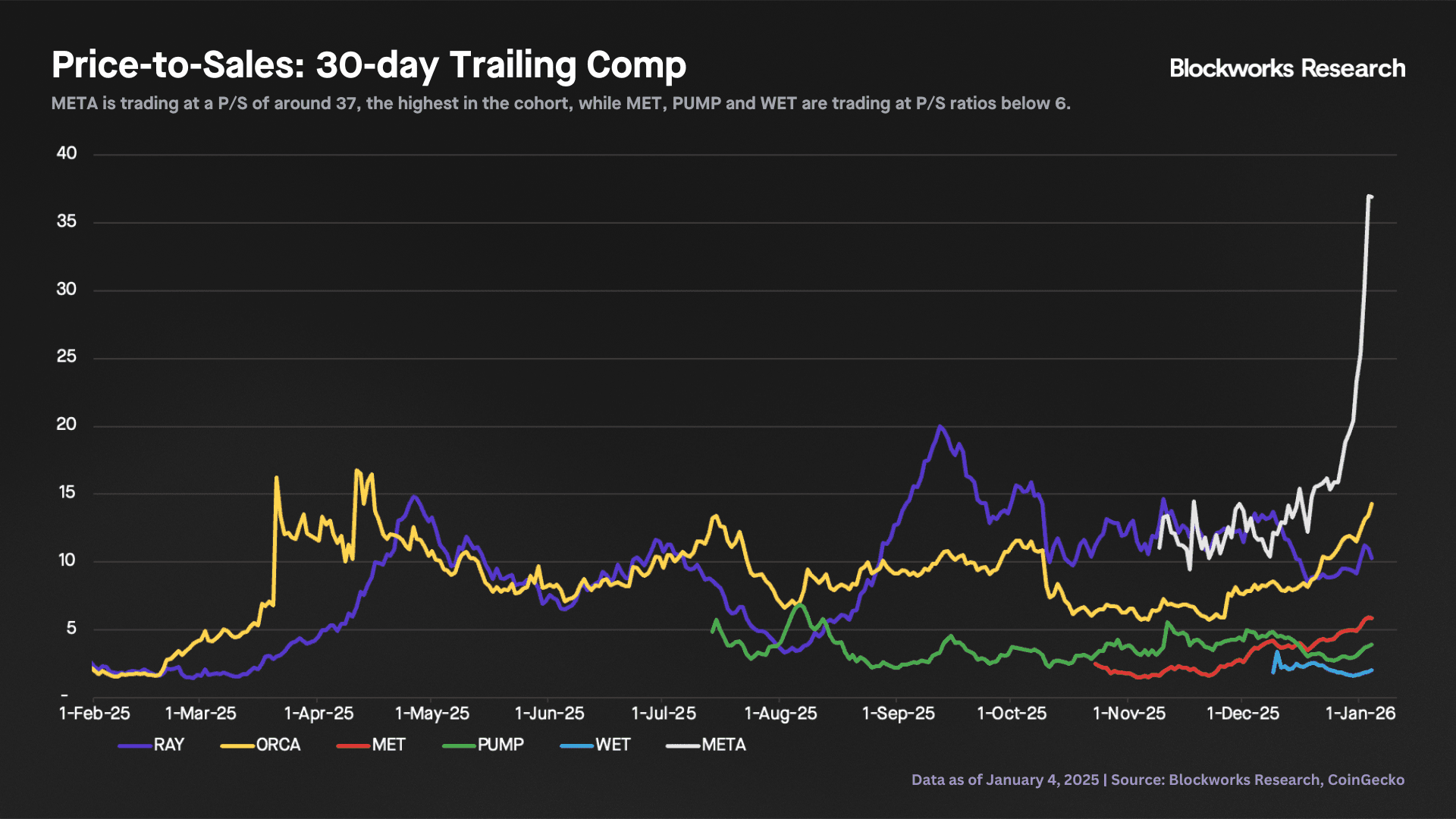

Price-to-Sales

The chart below shows the circulating price-to-sales multiples for the assets discussed throughout the report. The first notable takeaway is that RAY and ORCA have become more expensive over time (revenues have declined faster than valuations), leaving them at current P/S ratios of 10x and 14x, respectively. In contrast, PUMP and MET trade at around 4x and 6x P/S, respectively, despite being better positioned from a distribution and growth standpoint (Pump via its launchpad, and Meteora via Jupiter).

To calculate WET’s P/S, we estimated HumidiFi’s revenues by applying a 0.5 bps (0.005%) take rate to volume. While this assumption is directionally useful for cohort comparisons, it’s not fully accurate given that HumidiFi’s spreads can vary meaningfully with market conditions. Under this framework, HumidiFi would trade at roughly ~2x P/S.

Finally, META screens as the most “expensive” name in the cohort at ~36x P/S, which is precisely why we cautioned against treating trailing multiples as decisive on their own. We believe META can justify a premium to non-ownership coins, given its explicit guarantees around tokenholder rights and its forward-looking growth prospects. We previously published a forward-looking valuation model for META here.

That said, META’s current ~36x P/S sits well above its historical ~15x average, suggesting the market is frontrunning a series of near-term catalysts. The multiple expanded as META rallied ~40% over the past week while trailing revenue has dipped over the past month amid a temporary pause in ICO activity. Looking ahead, several developments should support a rebound in forward revenues:

- The Futarchy AMM fee split doubled from 0.25% to 0.50%.

- The migration of ~90% of META liquidity from Meteora DAMM v1 into the Futarchy AMM under the Omnibus proposal.

- The upcoming Ranger ICO (launching Jan. 6, 2026).

These catalysts, along with permissionless launches and STAMP, should help stabilize the P/S multiple lower in the coming months as revenues re-accelerate.

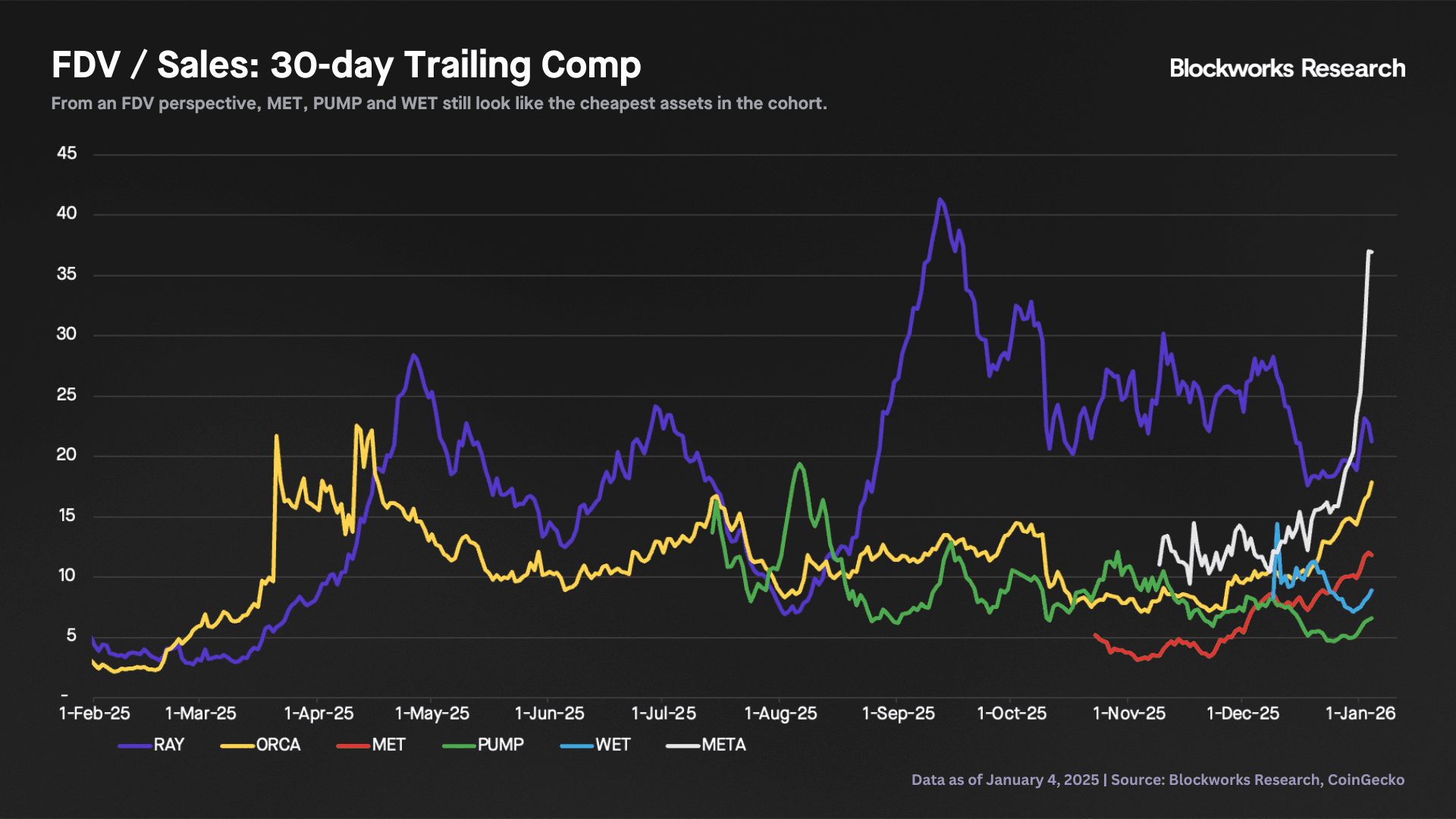

FDV to Sales

On a fully diluted P/S basis, META and RAY are the most expensive of the cohort. In Raydium’s case, we struggle to justify a premium given its more challenged forward volume trajectory and lack of durable control over the issuance layer. By contrast, MET, WET and PUMP have the lowest multiples in the cohort, at 12x, 9x and 7x, respectively.

Adverse Selection in Liquid Tokens

Across the board, we observe a median P/S of 8x and FDV/Sales of 15x. While these multiples may seem low at face value, the discount is primarily explained by uncertainties around tokenholder rights and supply dynamics.

Investors want exposure to fundamentally sound businesses, but they also want confidence that owning the token provides ownership rights over that business. Specifically, they want assurance that the team will act in the best interest of both the project and tokenholders, and that the token has a credible claim on residual cash flows, assets (e.g., the treasury), and legal recourse.

In our view, META trades at a premium relative to the cohort because it is one of the few assets that meets both criteria: fundamentally sound business and investable token with credible value accrual. That said, we expect the current ~36x P/S to compress toward ~20x over the coming weeks as revenues re-accelerate. Absent that, the recent price appreciation becomes harder to justify on fundamentals alone.

RAY is also an investable token. Raydium scored 38/40 on the Token Transparency Framework, indicating that the project has fully disclosed its revenue streams, equity to token holder rights, advisory service providers, and executive team personnel. It also has a high float, and the team uses 12% of swap fees to programmatically repurchase RAY.

The problem with Raydium is that its high multiple relative to the cohort shows a fundamental divergence to its growth prospects. Revenue has declined at a faster rate than its valuation, and absent a clear structural catalyst, it’s hard to make the case as to why that trend would reverse. Of note, Orca faces a similar structural issue to Raydium; while you can make the case for ORCA as an investable token, its growth prospects are similarly constrained.

An interesting observation is that, aside from ownership coins, the only credible signal for teams to tell the market that they care about the token has been buybacks (RAY, PUMP, ORCA, MET) – even though it is not the most optimal use of capital. Pump has spent roughly $230M to repurchase ~17% of PUMP’s circulating supply, yet the token still trades at ~3x trailing P/S (or ~5x on a fully diluted basis). Meanwhile, Meteora has spent approximately $12M to repurchase nearly 3% of MET’s total supply, with the token trading at a slightly higher circulating P/S ratio of 5x.

Even if you make a compelling growth case for Pump and Meteora as businesses, both tokens face challenges that could justify discounted multiples. Regarding Pump, it remains unclear for public market participants how value is split between token and equity, and if tokenholders have a right on Pump’s treasury. Regarding Meteora, ~7.2M MET tokens unlock monthly as part of the team’s and ecosystem reserve allocation, which could materialize into sell pressure. For example, at the current $280M valuation, these unlocks would translate to $2M in potential sell pressure per month.

That being said, while both tokens face challenges that could justify discounted multiples, the fact that RAY and ORCA trade at more than 2x the multiples of PUMP and MET with lower growth prospects could suggest a potential market mispricing and an attractive setup for a relative-value pair trade.

Finally, HumidFi’s WET presents similar issues. HumidiFi is the dominant and fastest-growing DEX on Solana and, on paper, WET represents the only liquid way to gain exposure to prop AMMs. That said, investors have to trust (somewhat blindly) that the team won’t rug the token.

In terms of token utility, users will be able to stake WET to earn fee rebates, with the team explicitly noting that “WET is not and should not be viewed as an investment.” If the team is long-term aligned with the token, then you can make a very easy case as to why WET is currently undervalued, despite having a low float. However, that’s the issue: public market participants have no way of telling if WET is a meme or an investable token with credible value accrual. As a result, it trades at a discount to where it otherwise could.

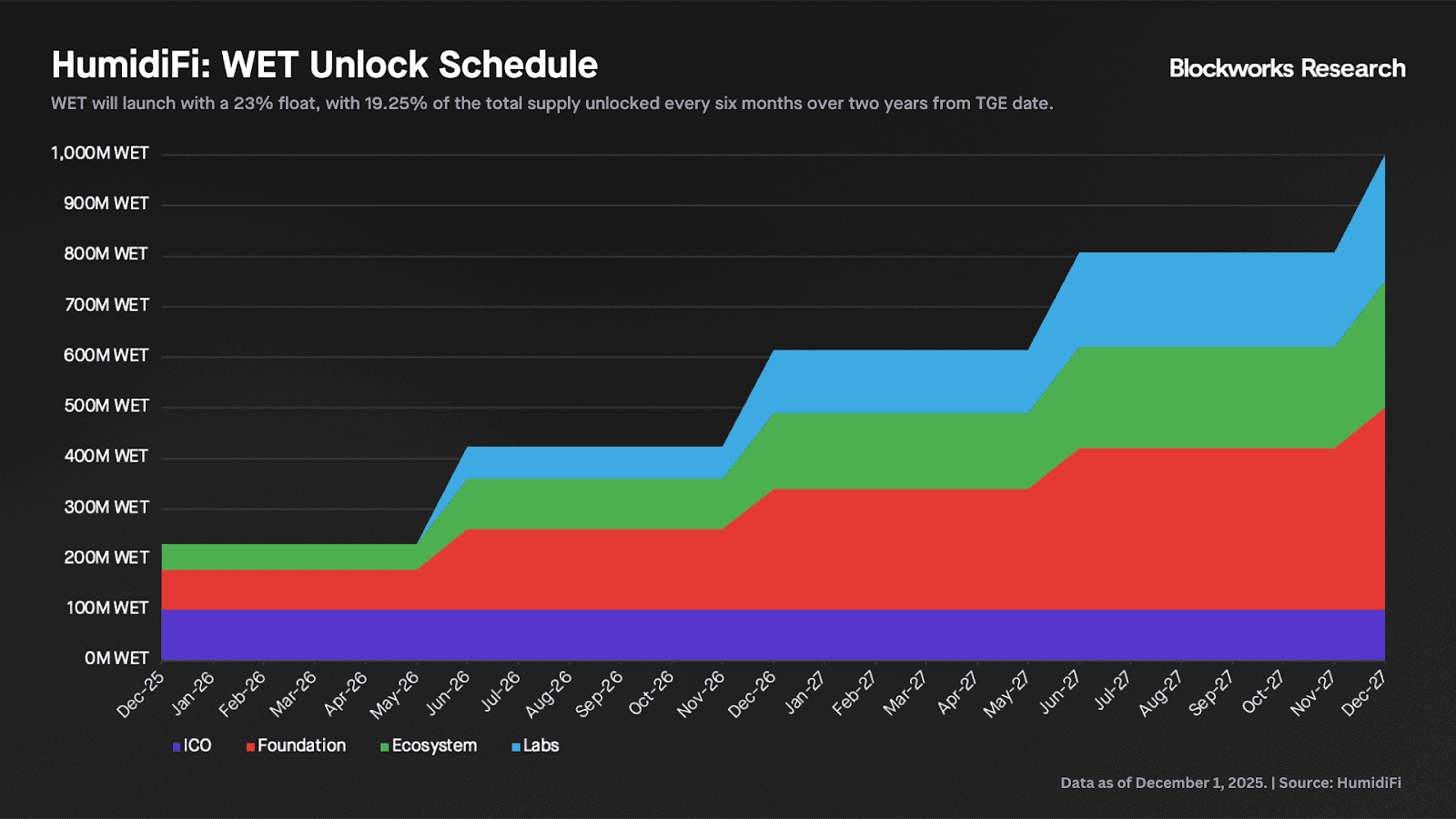

That said, given Temporal’s quality and track record as long-term builders in the Solana ecosystem, we assign a higher probability that the team will pursue growth and value accrual aligned with WET. This is ultimately a subjective judgment and should be taken with appropriate caution. Even so, on a risk/reward basis, we think WET presents more upside than RAY, ORCA, PUMP and MET, at least in the near term, before unlocks begin in June 2026.

Risks

Each of the projects for which we’ve taken a constructive view carries its own set of idiosyncratic risks, which we outline below.

HumidiFi

As noted earlier, the primary investment risk remains the lack of clarity around value accrual for WET. Beyond token design, there are also competitive risks to HumidiFi’s position within the prop AMM landscape. To date, HumidiFi has benefited from Temporal’s deep technical expertise and vertical integration at the infrastructure layer (e.g., HumidiFi benefits from Nozomi for transaction inclusion). However, one of the defining advantages of prop AMMs today is onchain composability: because both the stale-price venue and the prop AMM are onchain, arbitrage can be executed atomically in a single transaction, materially reducing execution risk. In this regard, Titan’s recent introduction of a composable RFQ product could narrow the gap between RFQs and prop AMMs, potentially pressuring prop AMM market share over the coming months.

Pump

Setting aside the token concerns discussed previously, Pump’s dominance in the high-velocity launchpad category is undisputed. The more relevant question is the durability of its revenue, with a common concern being that memecoins may be in secular decline. Onchain data suggests revenue has remained resilient, hovering near ~$900k per day in the past few days despite broader market weakness. However, this has also raised questions around data quality and sustainability. Current bonding curve activity still appears healthy, with roughly 1-2M transactions per day. That said, there is growing skepticism around whether some portion of this demand could be externally subsidized, a claim that remains speculative but nonetheless contributes to uncertainty around long-term revenue prospects.

MetaDAO

While we remain bullish on META and view MetaDAO as the most differentiated ICO platform, execution risk remains, especially around launch cadence. In our September base case, we assumed roughly five ICOs per month. As of writing, it has now been over a month since the last launch (Solomon), and MetaDAO ended December 2025 without any ICOs. That said, the Ranger ICO (launching Jan. 6, 2026) should re-accelerate revenues.

MetaDAO has debated both internally and in public comms whether to preserve a fully curated (permissioned) model or experiment with permissionless launches. We believe the latter, despite the risk of lower-quality projects, is a necessary experiment to increase throughput and validate the platform’s scalability, and is likely the direction the team ultimately pursues.

We also believe that Colosseum’s STAMP will bring consistent, high-quality launch volume to MetaDAO, complementing permissionless launches.

Meteora

While Meteora clearly benefits from Jupiter’s distribution, an important nuance is that the two protocols maintain separate tokens (MET and JUP). As a result, it is not obvious how much of Jupiter’s frontend-driven growth ultimately accrues to MET versus JUP. Even with strong team alignment, a lower multiple for MET may be justified if Meteora remains positioned primarily as backend liquidity infrastructure, while Jupiter captures the majority of user flow and interface-level value.

Final Thoughts

This report has outlined the current spot trading landscape on Solana. The key takeaway is that we expect the market to remain bifurcated: prop AMMs will continue to dominate short-tail, highly liquid markets, while passive AMMs will increasingly specialize in long-tail assets and new token launches.

Both prop AMMs and passive AMMs can benefit from vertical integration, but in opposite directions. Passive AMMs are moving closer to the user through token issuance platforms (e.g., Pump-PumpSwap, MetaDAO-Futarchy AMM), whereas prop AMMs are moving up the supply chain and focusing on transaction landing services (e.g., HumidiFi-Nozomi). The losers of this trend are legacy AMMs with limited end-user control and no durable, launch-driven source of order flow.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.