This research report has been funded by SKALE Labs, Inc.. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by SKALE Labs, Inc.. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

SKALE: The Chain Subscription Model

Key Takeaways

- SKALE is a modular network of EVM-compatible chains with pooled security. As the pioneer of the chain subscription model, its main value proposition is offering a gas-free blockchain experience for end-users.

- There are twenty SKALE chains as of October 2024. However, the majority of organic activity concentrates on the Nebula Gaming and Calypso NFT Hub, suggesting that the network has found a degree of product-market fit in the gaming sector.

- Chain pricing went live in January, yielding varied outcomes. Among the twenty SKALE chains, nine are fulfilling their monthly subscription obligations, projecting ARR to be near $389,000.

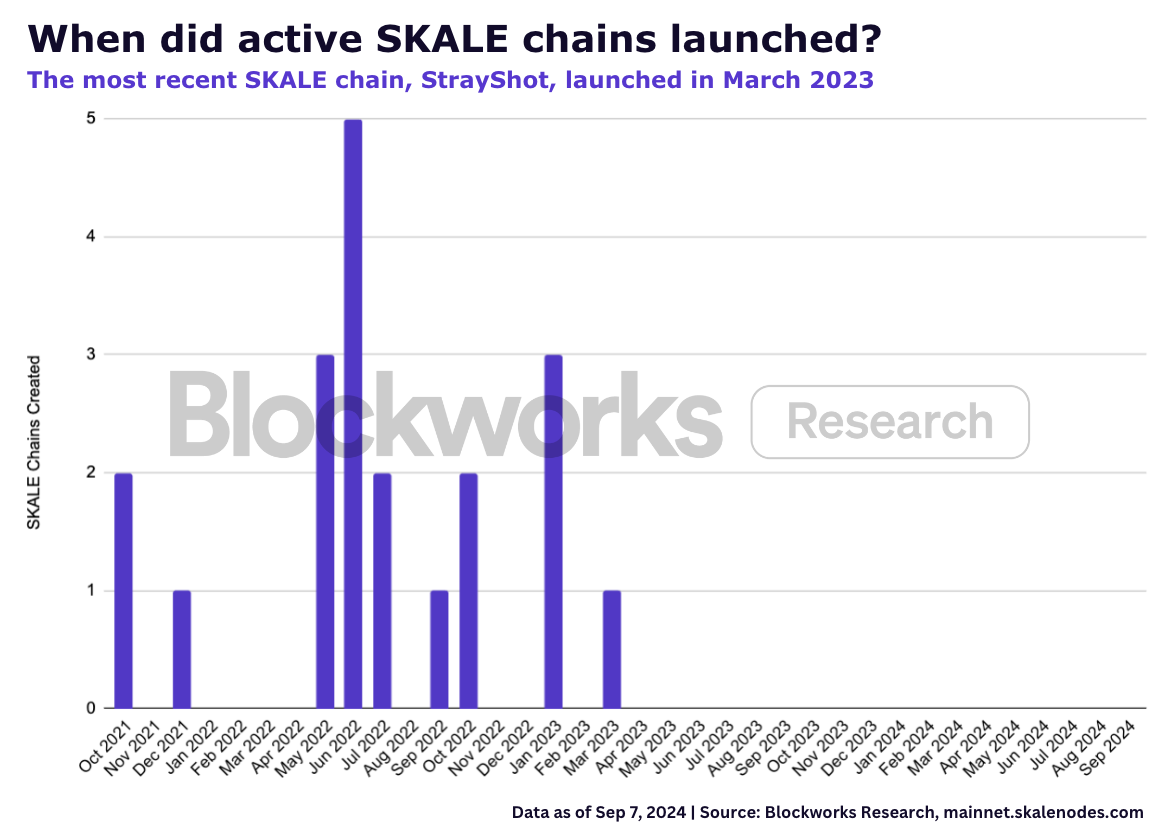

- The most recent SKALE chain launched in March 2023, meaning 19 months have passed since the last SKALE chain was created. SKALE chain growth will be a key metric as the network’s economic sustainability depends on new chains joining the network and paying their monthly subscription fee.

Overview

SKALE is a network of EVM-compatible chains with pooled security. SKALE chains are interoperable between one another and Ethereum mainnet. Although they share the same attributes technically, in practice, they can be divided into App and Hub chains. App chains are utilized by a single high throughput application, while Hub chains are shared by multiple applications within a broader sector, such as gaming or DeFi.

Ethereum's scalability issues have led to a modular era in blockchain design, and in a world with never-ending L1s and L2s, it's hard to differentiate from the herd. SKALE stands out by removing gas fees for end-users. SKALE is able to do this by shifting validator compensation to developers, who must pay a monthly subscription fee to maintain their chains. Later, we'll delve further into the implications of this business model and how an invisible blockchain experience makes SKALE particularly suitable for use cases like gaming.

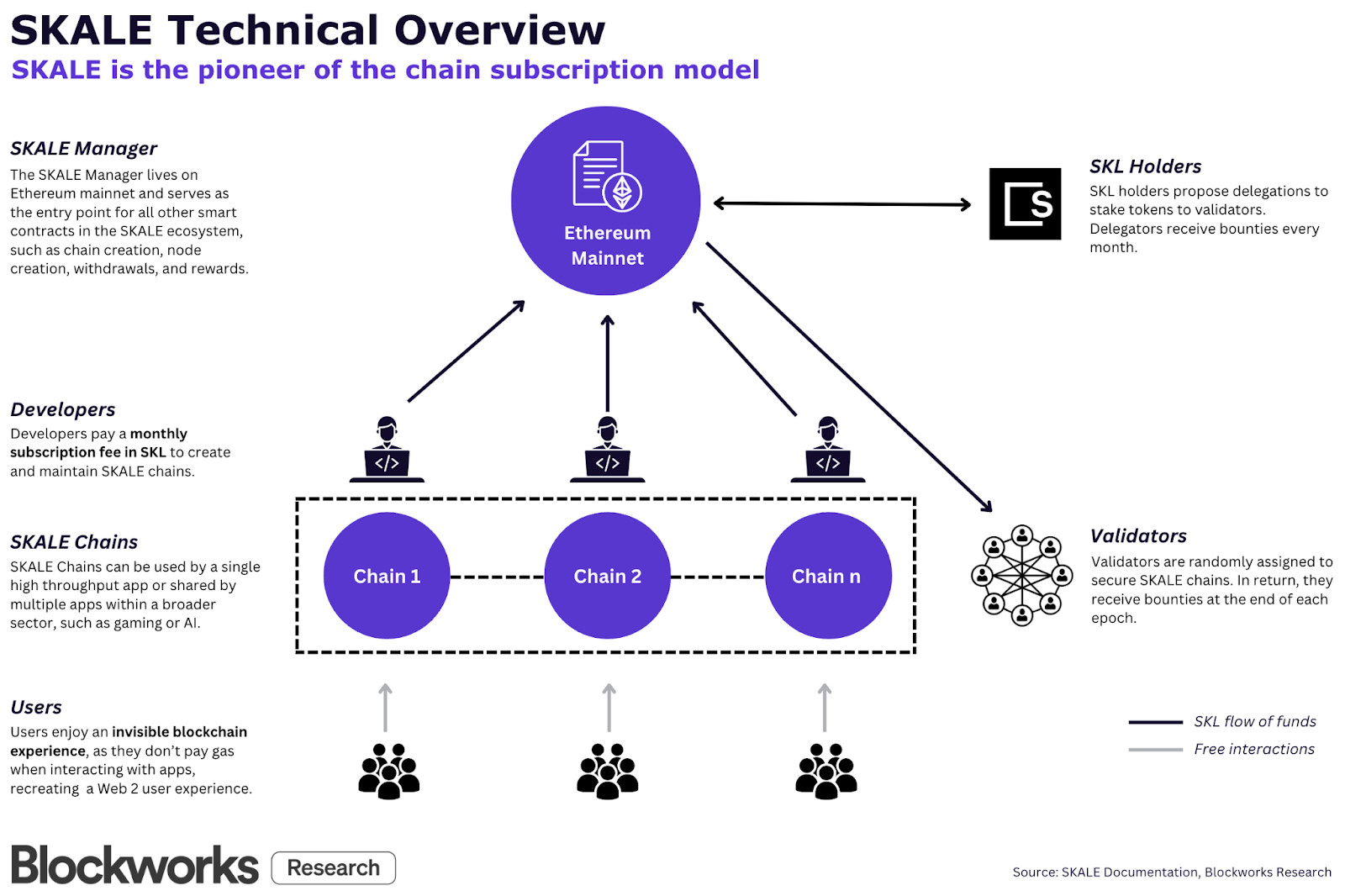

Network Architecture

SKALE is one of the pioneers of the appchain model, perhaps only preceded by Cosmos and Polkadot, and now adopted to some extent by popular L2s like Arbitrum's Orbit, Optimism's Superchain, or ZKsync's ZK Chains. Launched in June 2020, the network is composed of purpose-built chains for improved speed and customizability, depending on the desired use case. SKALE chains don't have to bootstrap a new validator set every time they are created as the network operates under a pooled security model. Every time a chain is launched, at least 16 random nodes from the validator set are randomly selected to secure it. A Distributed Key Generation (DKG) event occurs when the validators are chosen. The DKG algorithm generates a public key and a secret key, which no single party knows but has some share of. Each node gets a share of the secret key to participate in the consensus mechanism of a given SKALE chain.

At the center of SKALE's architecture is the "SKALE Manager," a set of smart contracts deployed on the Ethereum mainnet. The SKALE Manager controls nodes, validators, and the creation and destruction of SKALE chains. It also contains contracts for managing and staking of SKALE's native token SKL, Distributed Key Generation (DKG), and verification of BLS signatures. As such, SKL holders may propose delegations via the Manager to stake tokens to validators.

As crypto’s infrastructure landscape becomes increasingly saturated, it’s necessary for networks to meaningfully differentiate from the rest to attract a new cohort of developers and users. SKALE stands out by adopting a chain subscription model. Developers building a chain must pay a monthly subscription fee in SKL to “rent” their space. The result is that end-users of the network enjoy an invisible blockchain experience – free of gas fees – similar to how a Web 2 experience would feel. Below, we provide a simplified visualization of SKALE’s architecture.

Ecosystem Onchain Metrics

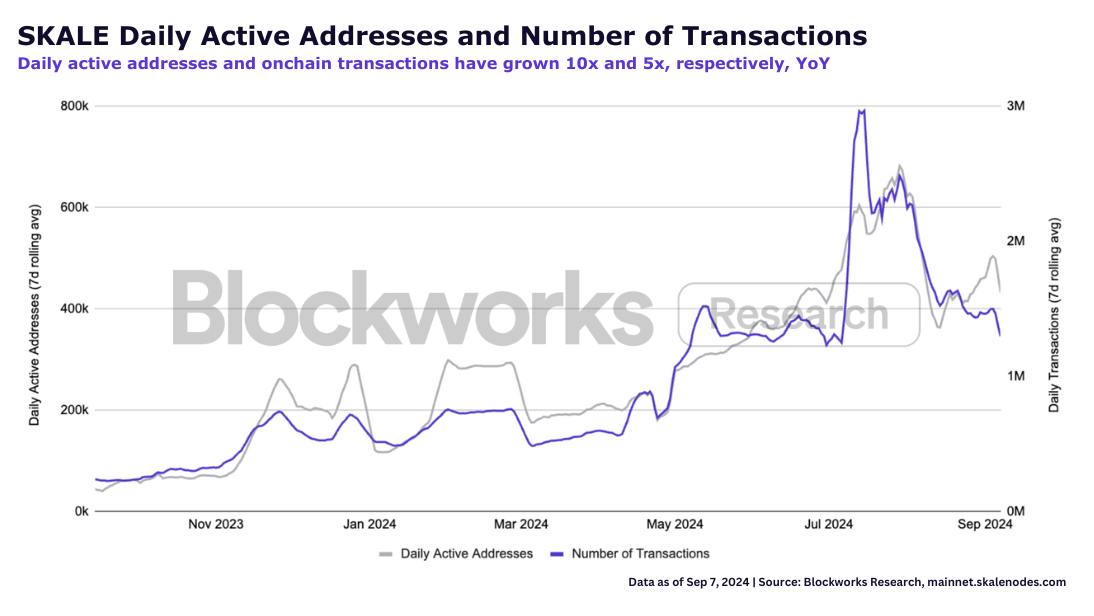

SKALE's onchain metrics point to an emerging but growing ecosystem. Daily active addresses (7d rolling average) have increased almost 10x in the past year, from ~44k in September 2023 to ~432k as of Sep 7, 2024. In addition, daily transactions have increased over 5x in the same period, from ~237k to ~1.30M. Though seemingly positive, these numbers don't reveal the whole picture. It's crucial to dive deeper into SKALE's ecosystem to understand where the growth is coming from and where it appears to be headed.

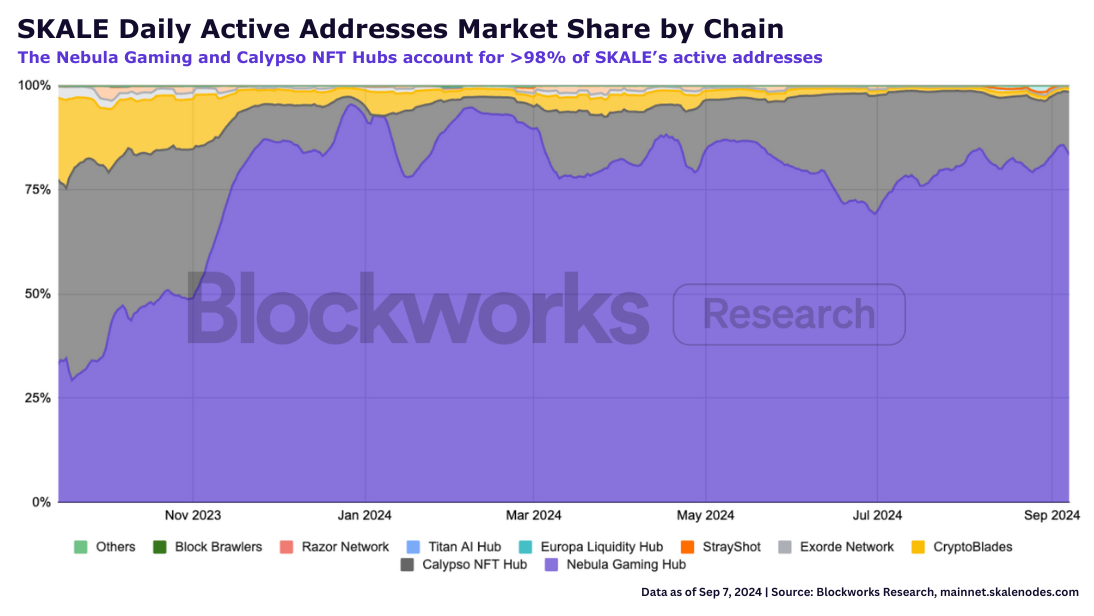

There are twenty SKALE chains as of September 2024, but most daily active addresses come from Nebula and Calypso. The Nebula Gaming Hub, home to over 50 games, represents 83% of SKALE's daily active addresses. Ten Nebula gaming apps have over 10k unique active wallets in the past 30 days, per DappRadar data. Some of the most popular include MotoDEX, World of Dypians, and EtherStrike. The Calypso NFT Hub sits in second place regarding active addresses, with a 15% share. Although Calypso started with a focus on NFTs, it now hosts a number of apps in the gaming and AI sectors. Its most popular app is Dmail Network, a decentralized communication protocol leveraging AI. All apps above, except for EtherStrike, have been deployed on multiple chains (i.e., they are not exclusively on SKALE). It's crucial to note that eleven of the twenty SKALE chains (55%) saw negligible activity in the past 30 days, with eight of them not registering a single transaction.

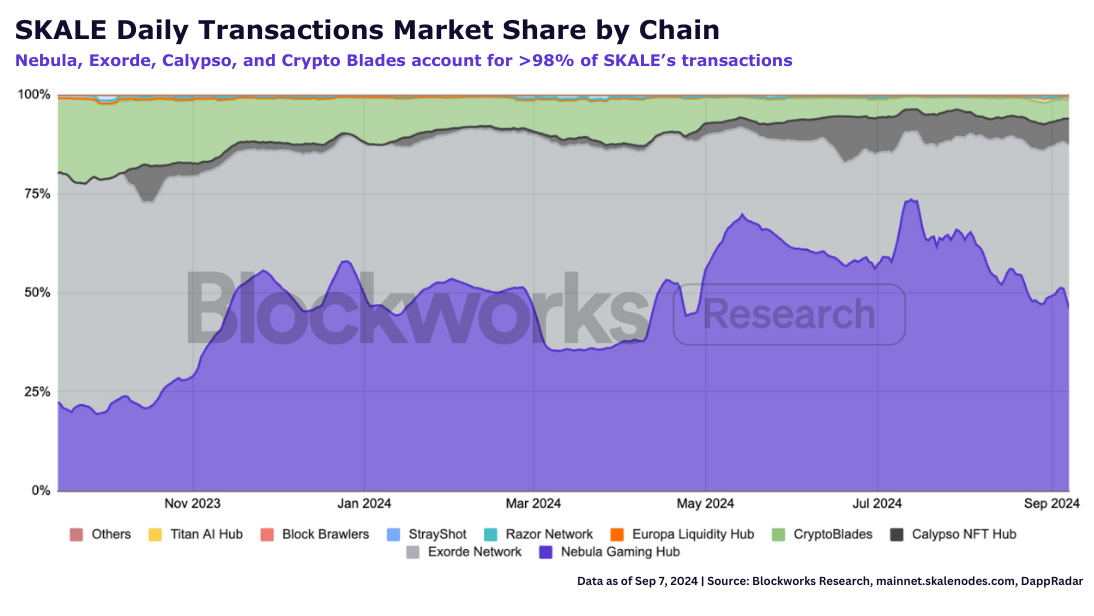

Regarding transaction volume, the Nebula Gaming Hub is also the clear leader, registering 46% of SKALE's daily transactions as of September 2024. Exorde – a protocol designed to collect and extract sentiment from social networks in real-time with the help of AI – is also a significant driver of transaction volume, accounting for 41% of SKALE's daily transactions. Exorde's activity comes from AI-powered bots that scrape the internet for information and publish it onchain, averaging 271 daily transactions per active address. It's interesting to note how SKALE's gasless offering toward the end user makes it particularly suitable for transaction-intensive use cases like gaming and data collection.

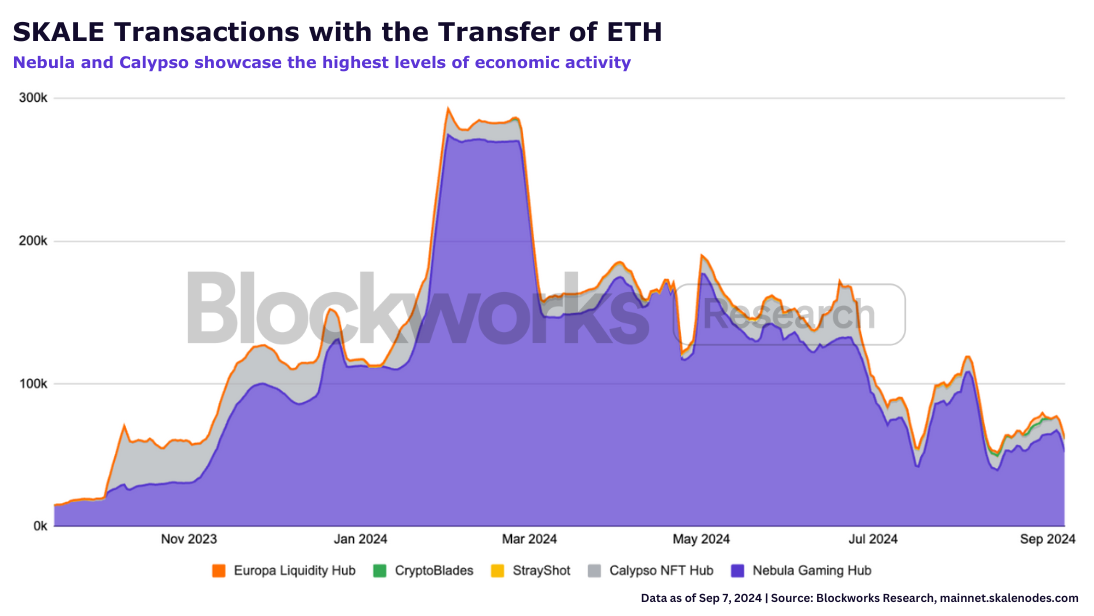

Intuitively, a network that doesn't charge any transaction fees can produce a lot of non-economic transactions, which lends itself to bot-driven activity. Thus, it's crucial to gauge what percentage of SKALE transactions carry economic value. The figure below shows the number of transactions of SKALE chains that included the transfer of ETH – though imperfect, it gives us a proxy for the level of economic activity in the network. As we can observe, Nebula showcases the highest level of economic activity in the SKALE ecosystem, with >50k daily transactions involving the transfer of ETH, followed by Calypso, with ~9k daily transactions. Looking at it from another perspective, over the past year around 18% and 24% of Nebula's and Calypso's daily transactions, respectively, have included an ETH transfer. This is a positive sign of organic traction on both chains and may indicate real economic activity, such as in-game purchases that turn these applications into sustainable business models.

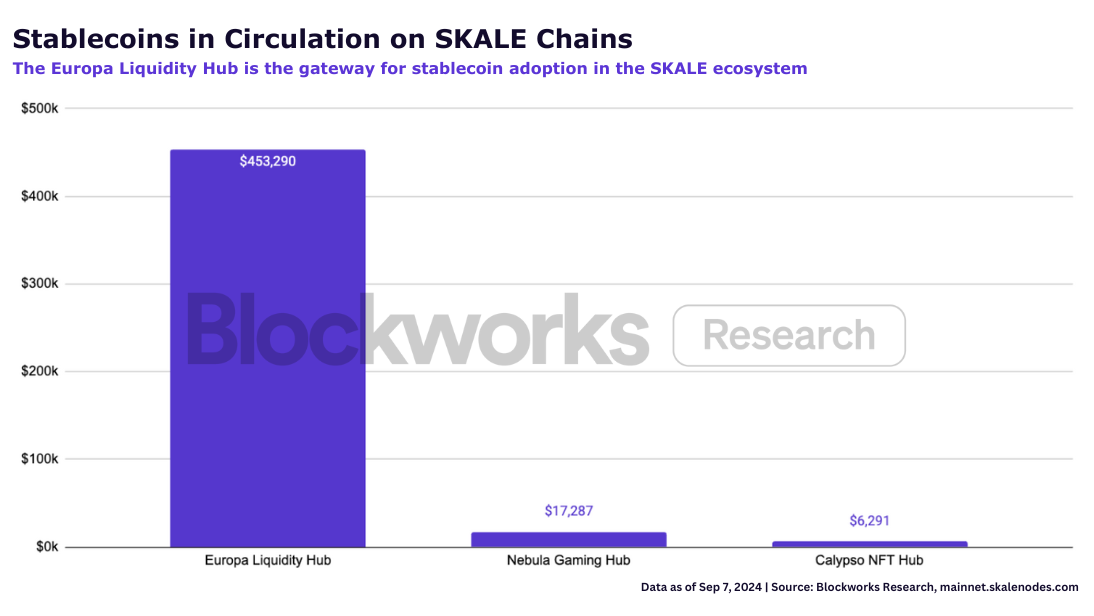

Another way of gauging economic activity in the SKALE ecosystem is by looking at stablecoin adoption. The Europa Liquidity Hub takes the lion's share with $453k worth of stablecoins in circulation. It's important to note that Europa is the liquidity gateway for other chains in the SKALE ecosystem, such that USDC circulating on Nebula and Calypso is bridged from Europa. Once again, the data suggests that Nebula and Calypso have achieved organic traction and some level of real economic activity. Still, Europa's traction is underwhelming compared to other DeFi ecosystems. Despite launching in 2022, it has only $377k in TVL, placing it 195th place of all chains by TVL as of Sep 10, 2024. In this regard, the only DeFi primitive that has emerged on Europa is Dexes, with SushiSwap at the helm. A plausible explanation for the lack of traction is that SKALE isn't competing with other blockchains for DeFi liquidity, which would be extremely difficult to accomplish due to the incumbents' network effects. Instead, it focuses on high throughput applications that need zero gas fees to operate economically. Still, it would be beneficial to the SKALE ecosystem for Europa to attract more liquidity as it can flow to other applications in popular networks like Nebula and Calypso.

SKL Economics

SKL has a circulating market cap of $199M and an FDV of $269M as of Oct 24, 2024. The SKL token serves four main purposes:

- **Staking: **SKL token holders may delegate and stake their tokens to validators, contributing to the network’s security.

- **Rewards for validators and delegators: **Validators receive a revenue stream in SKL at the end of each epoch, while delegators earn rewards on a monthly basis. SKL rewards come from monthly issuance of tokens (inflation) and developer subscription fees.

- **Developer subscription fees: **Developers “rent” their access to SKALE chains using SKL tokens.

- **Governance and voting: **SKL tokens are used for on-chain voting, giving holders control over the parameters of the protocol.

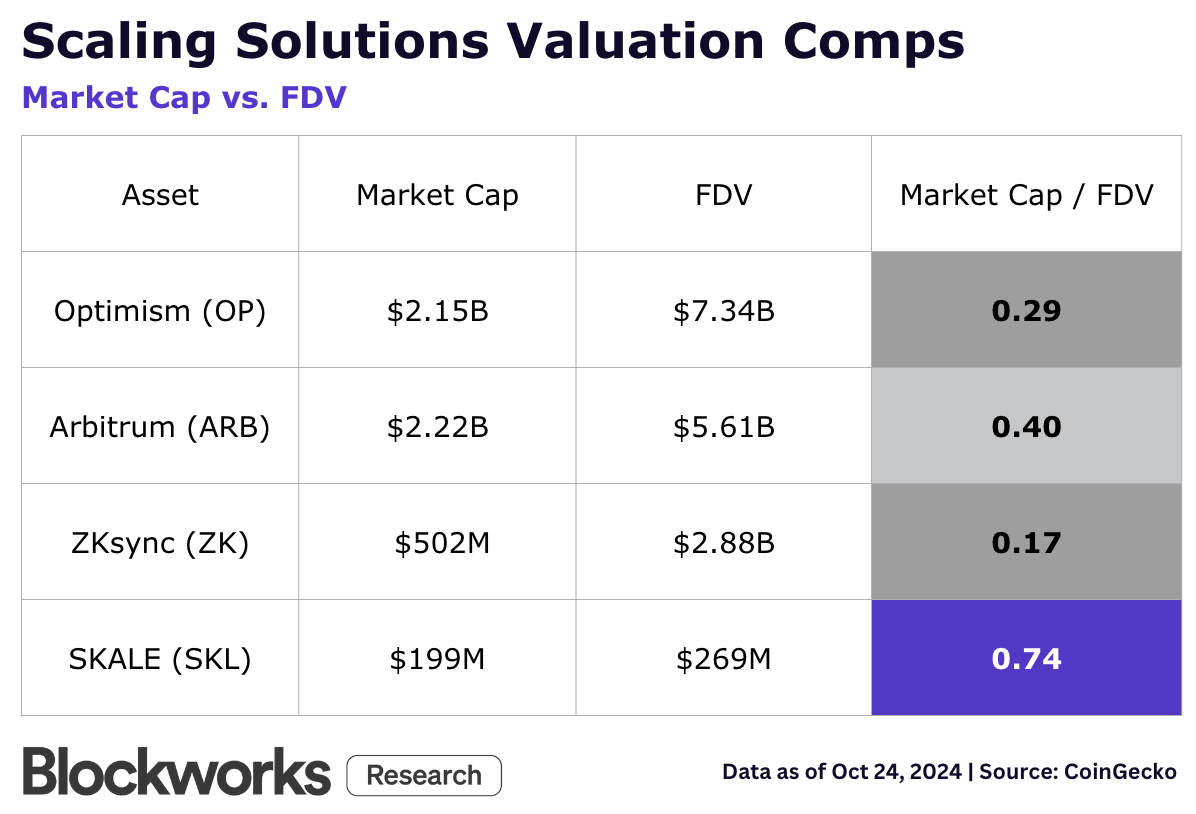

In terms of supply, SKL’s circulating supply is 5.18B, with a maximum supply of 7B tokens. In contrast to popular scaling networks suffering from the low float and inflated FDV problem, most SKL is already in circulation. The figure below shows that supply overhang isn’t as much of an issue with SKL as with other assets (OP, ARB, ZK) with much higher valuations and no supply cap.

Chain Pricing: SKL Inflation vs. Developer Subscription Fees

In January 2024, SKALE chain pricing officially went live on mainnet, with the first due date for payments being Feb 1, 2024. Pricing started at $3,600 per SKALE chain per month, with 100% of the proceeds going to validators. In this regard, the network has taken a loss-leader strategy with intentionally low pricing in the first year, with the goal of driving up price in the next 12-18 months based on a dynamic model.

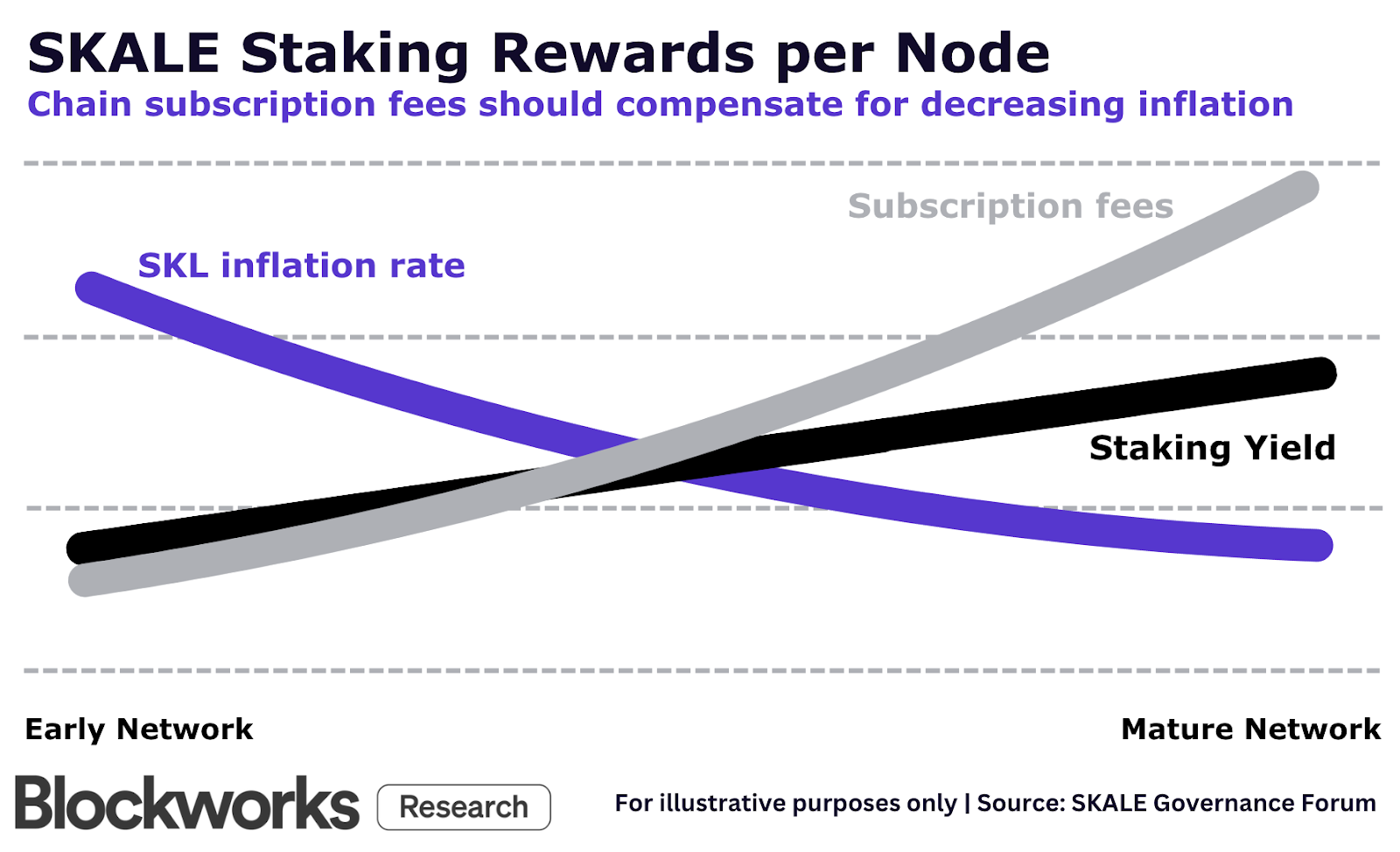

The idea of activating developer subscription fees is to achieve economic sustainability as SKL inflation trends towards zero. This idea was expressed best in the SKALE governance forum: “L1 blockchains operating with gas fees function similarly, where inflation subsidizes low gas fees in their network. Numerous high profile L1 networks generating tiny amounts of fees owe their short-term sustainability to this inflationary offset, which allows them to adopt a growth-first strategy. They however will eventually hit a crunch requiring them to increase fees or face the reality of running a perpetually subsidized economic model.”

Because SKALE’s main value proposition is offering a gas-free experience for end-users, developers must absorb the cost of incentivizing validators. Chain fees are supplemented by a descending inflation mechanism (hardcoded into the SKALE Manager contract), such that fees eventually surpass issuance rewards. The figure below illustrates the idea:

Chain pricing will be dynamic, increasing or decreasing in value based on the network utilization rate, defined as CA/NS where:

- C is the number of SKALE Chains live in the network

- A is the number of nodes in each chain, which equals 16

- N is the number of active nodes in the network

- S is the number of available slots on the node, which equals 8

As mentioned, chain pricing started at $3,600 per month and will rise to about $46,000 at the Target Rate of 50% network utilization and $84,000 at 70% utilization. Developers can pay up to two years in advance, which enables renters to lock in the price with a prepayment. This feature allows for predictable economic planning and a predictable path to revenue for applications in the ecosystem. In the event that a chain owner doesn't pay the monthly subscription fee, the chain is deemed non-compliant. After a two-month grace period, chain renters lose their chain autonomy, and ownership transfers to the SKALE Network multi-signature wallet on the Ethereum Mainnet. Additionally, as a last resort of "no payment," the chain's final month of rent will be utilized to support the transfer of state and assets from that chain to the SKALE collective community chain to protect end-user assets from chain default.

Finally, it’s crucial to emphasize that there are active discussions to change the dynamic pricing model so it’s not based solely on network utilization. Instead, it would also be based on the number of validators, storage size, and compute instances required by each chain. The practical implication of this change is that Hubs will cost dramatically more than App chains. In addition, validator resources will also be assigned dynamically such that App chains will require less nodes from the validator set and therefore pay less fees. Although this proposal is being actively discussed in SKALE’s governance forum today, the technical specifications have been in production in a test environment since 2019. The goal with dynamic pricing long term is for Hubs to generate over $2M per year in SKL fees, which is reasonable considering 50-200 apps per Hub. For instance, the more than 50 games in the Nebula Hub would contribute toward the “monthly rent” based on their size and activity level to pay for the Hub’s total cost.

Revenue Analysis

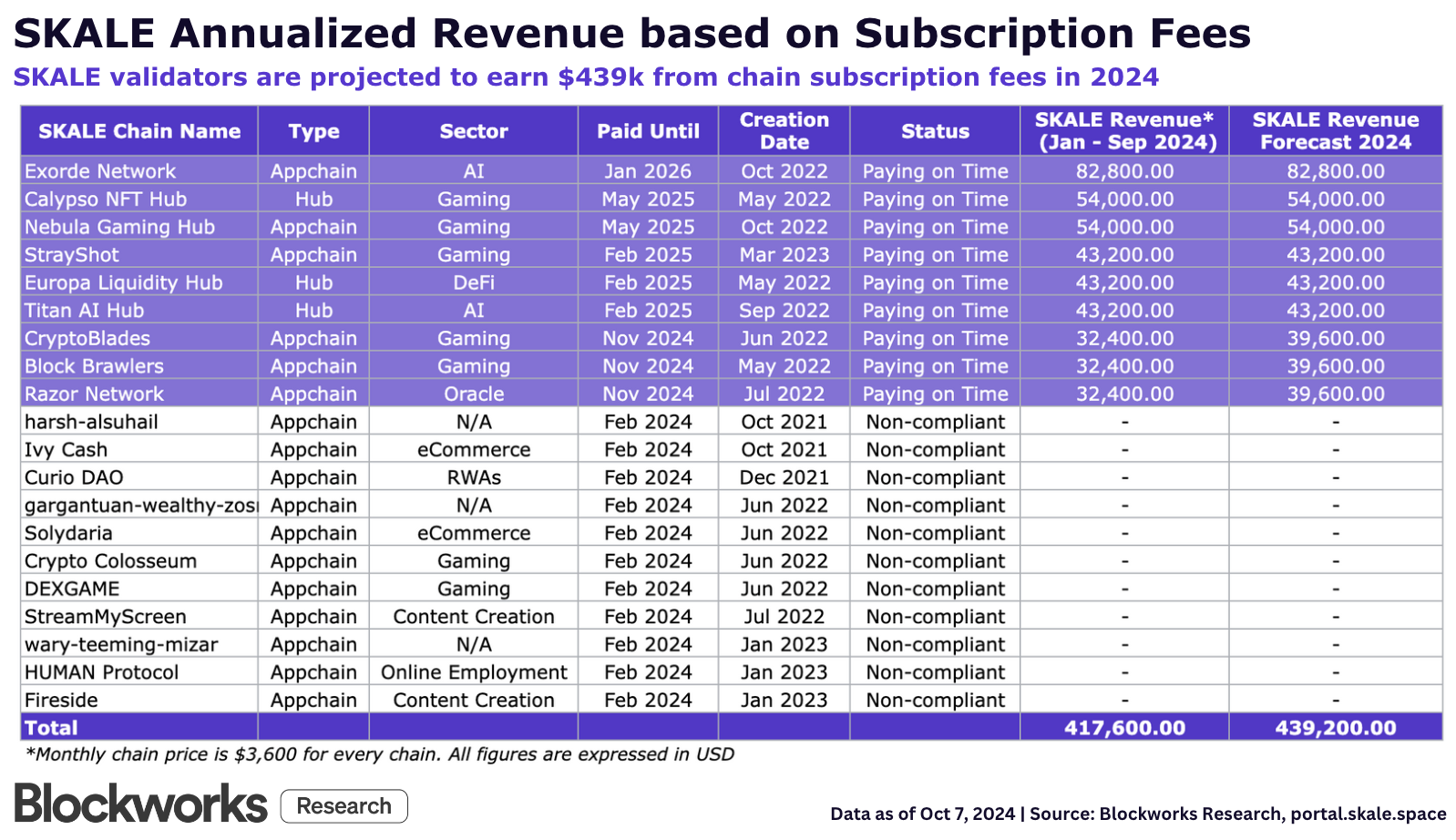

Now that we've discussed the chain pricing mechanism let's look at the actual revenue data SKALE has generated thus far. Out of the 20 SKALE chains, 11 (55%) are non-compliant. This data is not surprising, considering that these chains had minimal to no onchain activity to begin with. The table below shows the revenue generated by each chain.

We can derive some interesting observations and conclusions from these numbers:

- Six chains have paid for months in advance: Six chains have taken advantage of the price lock mechanism, paying anywhere from 12 to 24 months in advance.. This feature allows for better financial planning and a more predictable revenue path for these applications, as monthly pricing may change as new chains join the network or the number of nodes increases or decreases.

- Gaming dominates as a sector: 55% of chains that are up-to-date with their payments belong to the gaming sector, suggesting that SKALE may have found product-market fit in this particular sector. This data point also reinforces what we observed in the onchain metrics section, where Nebula and Calypso clearly showed the most traction.

- SKALE annual revenue for 2024 is projected to be around $439k. SKALE has generated $418k in revenue as of October 2024. Assuming CryptoBlades, Block Brawlers, and Razor Networkcontinue making their monthly payments until year-end, we can forecast that SKALE’s revenue for the calendar year will be $439k.

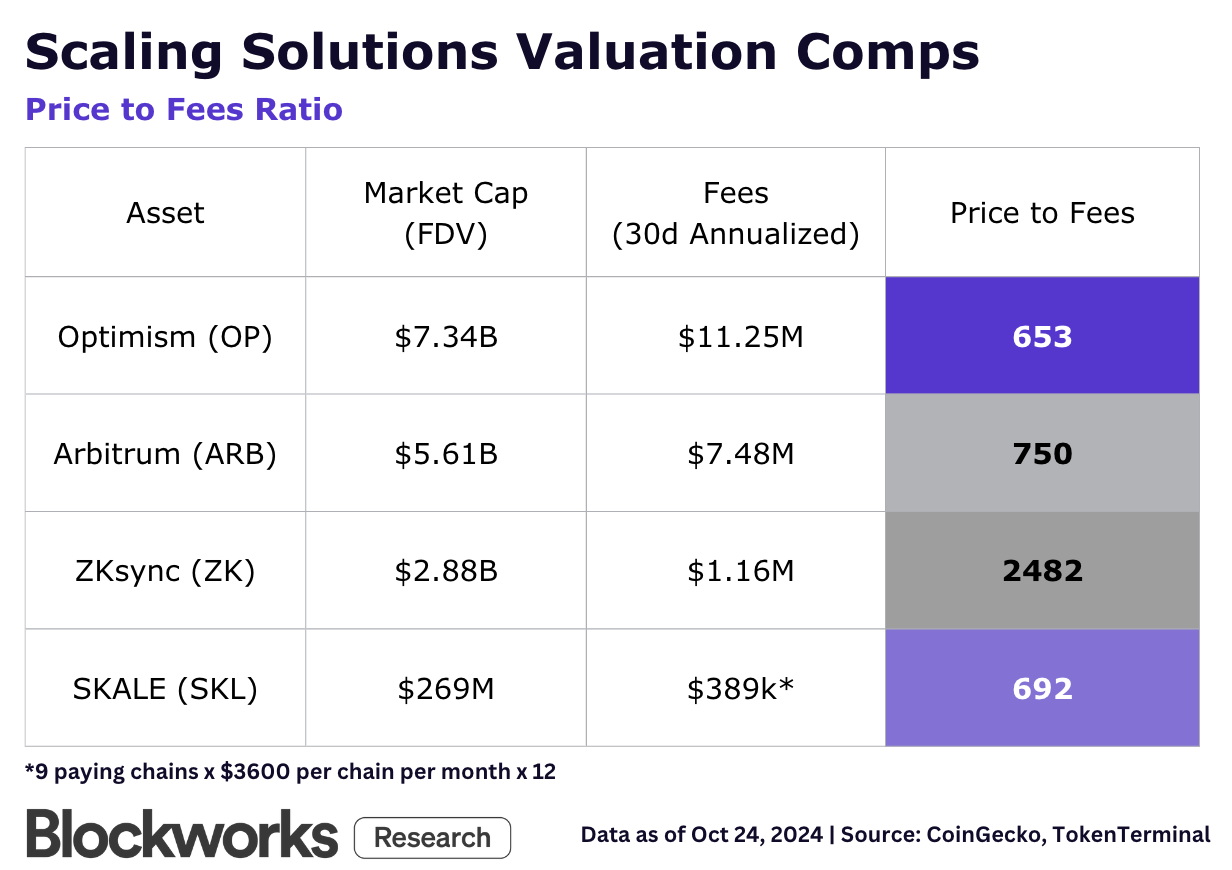

How is SKL priced based on its revenue compared to other modular networks? The table below shows that SKALE revenue is still relatively low compared to some of its competitors. Optimism, Arbitrum, and ZKSync generate about 29x, 16x, and 3x higher fees than SKALE on an annualized basis. However, it’s crucial to note that SKALE is priced the cheapest on a price-to-fees basis.

Investors should be aware of the inherent limitations of this analysis. Namely, we are only looking at current revenue when, in reality, investors also price assets based on expected future cash flows. Still, it is useful to gauge where SKALE sits today in terms of fee generation. Based on SKALE's business model today, increased activity won't necessarily translate to increased revenue. For instance, the Nebula Gaming Hub is home to many games, but no matter how many users or games the Hub hosts, the monthly subscription fee paid to SKALE will remain the same ($3,600). However, as mentioned previously, a novel dynamic pricing model will likely go live in the next 12-18 months, which means that Hubs like Nebula will require larger validator resources and hence will pay substantially more subscription fees than today.

Finally, it's crucial to remember that SKALE's pricing depends on the network utilization rate today. The number of active nodes on the network as of Oct 7, 2024, was 112. The CA/NS equation shows that the current utilization rate is (20*16)/(112*8) = 35.71%. Based on the current number of active nodes, it would only take 28 chains to reach a 50% network utilization rate, increasing SKALE's chain pricing to $46,000 per month. It seems unlikely that all chains are willing to pay that much based on the activity they are generating today, so it will be crucial for the dynamic model based on validator resources required to go live. In this scenario, Hubs like Nebula would pay substantially more than App chains like CryptoBlades. Assuming Nebula has 100 playing games in the future with in-game purchases, $46,000 per month translates to only $460 per game, which is not significant compared to what games pay for cloud computing services like AWS. Effectively, SKALE fees paid by game developers can be interpreted as buying smart contract compute, similar to cloud computing in Web 2.

Catalysts and Risks

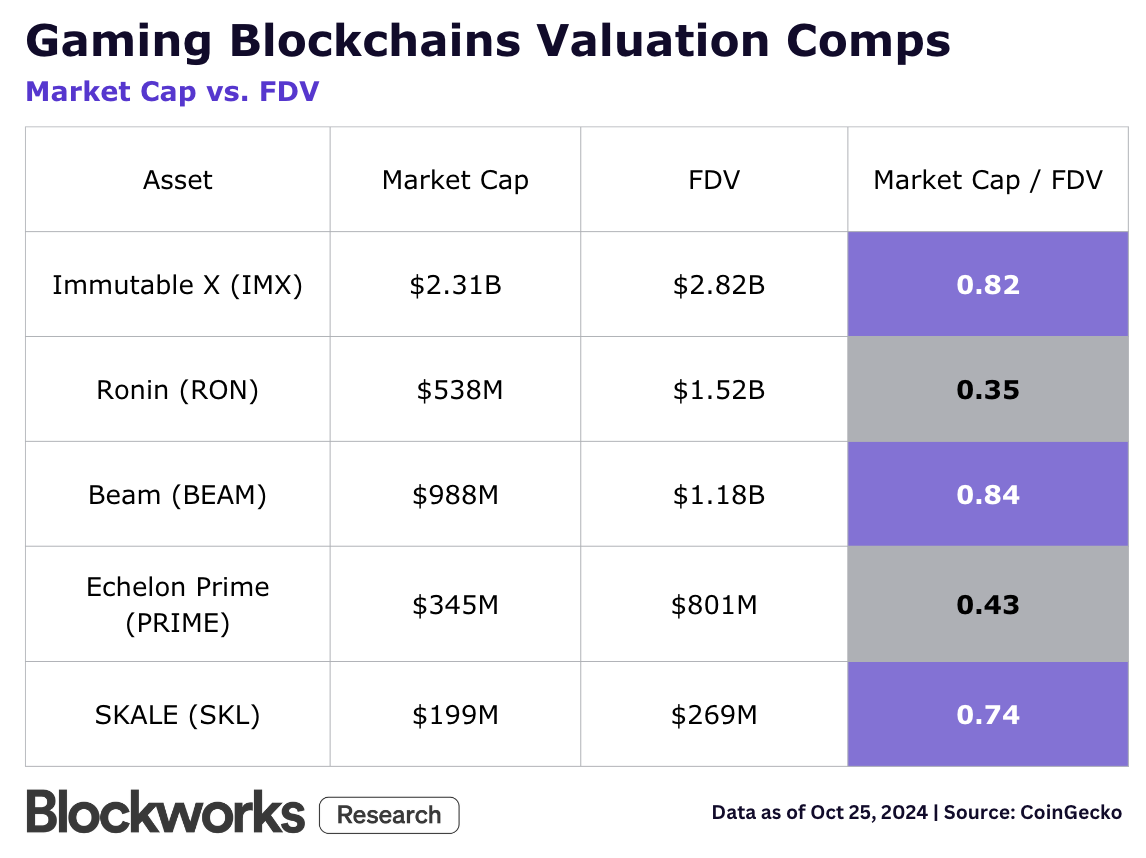

Gaming has emerged as an ideal use case on SKALE due to its invisible blockchain experience and zero gas fees for end-users, as proven by the dominance of Nebula and Calypso in onchain activity. Thus, SKALE has continued its gaming sector efforts to catalyze chain growth. In early 2022, SKALE announced a $100M fund managed by the Network of Decentralized Economics (N.O.D.E.) Foundation to support and onboard projects to the network. The ecosystem fund is still ongoing, with recent grant programs focusing exclusively on gaming. SKALE announced a $2 Million SKL token grant opportunity for game projects and developers attending the Game Developers Conference (GDC) in March of this year. Besides a robust grant program, SKALE has recently attained remarkable partnerships in the gaming sector. For instance, SKALE joined Unity's publisher support program in June 2024 – as one of the world's leading platforms of tools for creators to build and grow real-time games and applications, this could be beneficial for developers looking to build on SKALE. In sum, SKL could emerge as an overlooked bet on the gaming ecosystem, especially compared to other gaming blockchain valuations.

A clear risk is the lack of traction in the network's liquidity hub, Europa. Despite launching over two years ago, stablecoin adoption is minimal, and the only application that has some usage is SushiSwap. It should be noted that SKALE is not competing on DeFi but has instead shifted its focus on gaming and high-performance applications. Still, increasing liquidity in the Europa Hub could benefit the entire ecosystem via stablecoin adoption for in-game purchases, lower slippage for swaps, native asset issuance, and more. In the coming months, there will be an initiative to revitalize Europa with token incentives to promote activity.

Another risk for SKALE is its ability to find a credible path to economic sustainability with its current business model, which is dependent on new chains joining the network. The chart below shows that the most recent SKALE chain launched in March 2023, with most chains launching in 2022. In other words, 19 months have passed since the last SKALE chain was created. In this regard, once SKALE pricing shifts to a dynamic model charging more to Hubs than App chains, this risk will be minimized as the network will no longer depend on new chains being created to increase its revenue. Instead, Hubs will accrue the majority of applications and activity, hence requiring larger validator resources and paying more SKL fees to the network.

Final Thoughts

SKALE implements a novel business model, differentiating itself from other networks by offering a gas-free blockchain experience for end-users. The network is at a critical moment in its lifecycle, as it's the first year in which developer subscription fees have been active. Previously, the network relied solely on SKL issuance rewards (inflation) to incentivize validators, a bootstrapping strategy employed by virtually every L1 and L2 in the industry. As the network matures and SKL inflation trends toward zero, monthly fees for SKALE chains should take a bigger portion of validator rewards and generate a real positive yield. With only six paying customers (chains), SKALE's path to profitability seems to be very early. It will be crucial for the team to focus on use cases where it has found a semblance of product market fit, such as gaming. With its unique value proposition for end-users, robust grant program, and recent partnerships, SKALE could be an exciting player to watch out for in crypto gaming.

Disclosure: This research report has been funded by SKALE Labs, Inc. dba SKALE. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by SKALE Labs, Inc. dba SKALE. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek the advice of a qualified financial advisor before making any investment decisions.