Leverage in Predictions Markets

Key Takeaways

-

Four leverage models are emerging across prediction markets: the lending pool, the prime broker, the synthetic desk, and the perps exchange. Each differs in how it prices jump risk, manages liquidations, and sources capital. The lending pool socializes risk across depositors and uses calendar-based deleveraging ramps. The prime broker monitors account health at the venue level and uses Dutch auctions for large liquidations. The synthetic desk internalizes risk management by sitting between the trader and the underlying market as counterparty. The perps exchange applies the perpetual funding rate mechanism, though its mean-reversion assumption breaks down as prediction markets converge toward binary outcomes.

-

Financing revenue, not trading fees, drives leverage economics. Over 87% of modeled fee revenue comes from sustained open interest, so the winning model will be the one that keeps positions open longest. In the base case, a platform-wide leverage layer generates roughly $15M in annual fee revenue. The bull case reaches $50.7M, additive on top of spot.

-

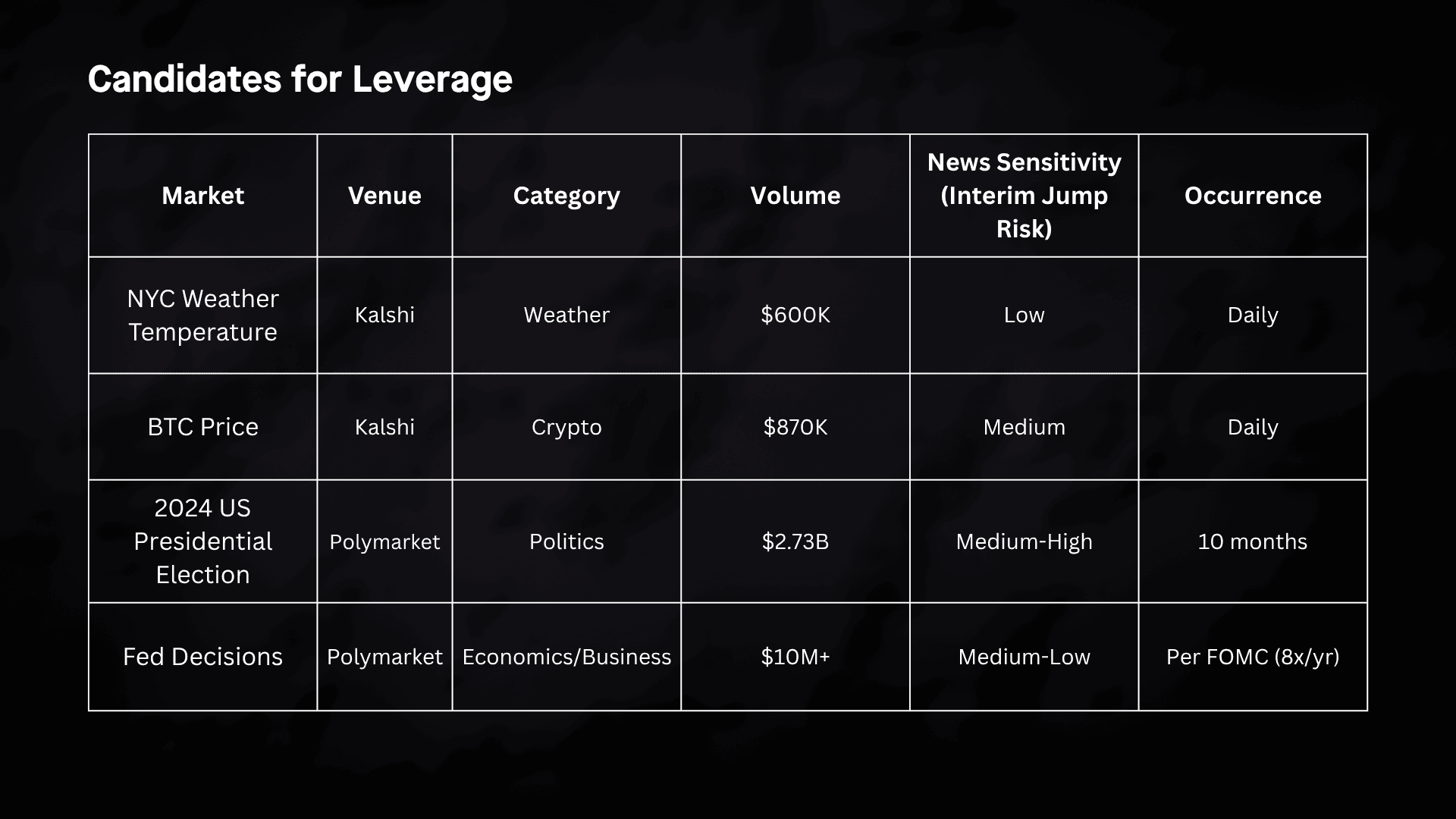

The institutional case for leverage extends beyond speculation. Weather markets on Kalshi have traded approximately $595M in cumulative notional volume with daily recurrence and a continuous underlying variable, making them a natural fit for hedging by energy companies, agricultural traders, and insurers. Leverage in that context amplifies capital efficiency on positions that already serve a risk-transfer function. The 2024 US Presidential Election, with $2.73B in Polymarket volume and a live leverage layer running on dYdX throughout, demonstrated that political risk markets can sustain leveraged activity at scale when duration and liquidity conditions allow it.

-

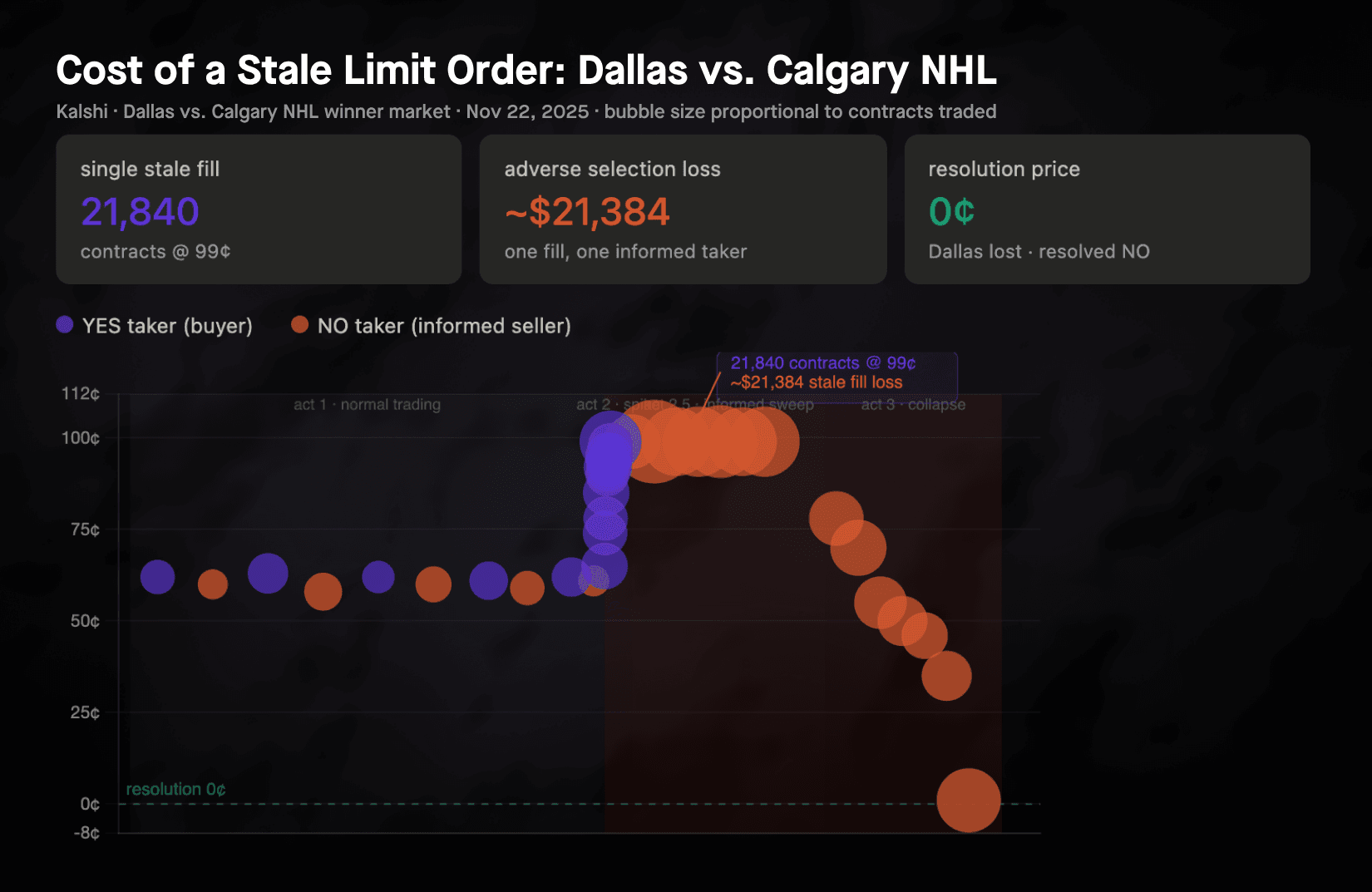

Every model inherits a shared dependency on CLOB venue structure. In the Dallas vs. Calgary NHL market on Kalshi, a single stale limit order at 99¢ resulted in a 21,840-contract fill and roughly $21,384 in adverse selection losses when the game shifted and the market resolved at 0¢ twenty minutes later. Stale limit orders during jump events create risk that no individual team can fully resolve.

-

The opportunity for structured products built on prediction market leverage is real but depends on venue reform. What a purpose-built prediction market venue could do differently, and how batch auction design could change the break-even economics for financiers and market makers, is the subject of the next report.

Why Prediction Market Leverage Matters

Leverage on prediction markets is a difficult problem. Not every market needs it, and often it may be more destabilizing than useful. But in the subset of markets where it can be supported well, the opportunity is significant. There are examples already in the wild: Polymarket’s ecosystem has seen third-party projects attempt to build leverage, while Kalshi recently gained access to margin through its regulated structure. Users are drawn to leverage for varying reasons. The prospect of larger returns with less upfront capital appeals to retail emotionally, while institutions value leverage for capital efficiency and hedging.

Leverage in prediction markets, however, is not simply a matter of adding margin to an existing venue. Its viability depends on three things:

First, market selection matters: the best candidates are liquid, recurring markets that are less exposed to constant repricing from breaking news.

Second, leverage provision must be priced properly relative to its risk. These risks are largely concentrated in jump risk (the risk that news sensitivity causes a market to gap in such a way where a proper liquidation cannot occur) and creep risk (price drift). Leverage provision as a result should be priced at an epoch level to segment these risks in a certain frame of time. More on this in a future report.

Third, and often overlooked, venue architecture matters. The way a market matches orders, handles liquidity, and processes liquidations can shape a financier’s risk in leverage provision.

Today, we already see markets where some form of leverage could be architecturally viable. Weather markets on Kalshi have traded approximately $595M in cumulative notional volume, averaging $2.8M daily in recent months, occur daily, and the underlying variable — temperature — is continuous and updates gradually rather than resolving on a single play or ruling. However, Kalshi's current bracket structure (e.g., "Will the high be 84–85°?") fragments this continuous outcome into a series of binary contracts, each carrying its own resolution risk. A continuous-settlement design, where payout scales with the actual reading, would better capture the structural advantage of the underlying and make weather a cleaner candidate for leverage. Retail demand for leverage in that domain is an open question, but the institutional case is fairly clear: weather derivatives are a natural hedging instrument for energy companies, agricultural traders, and insurers, for whom leverage would amplify capital efficiency.

Models for Leverage Provision

We currently see prediction markets developing new features either in-house or through ecosystem development teams, and leverage is the key feature that’s gaining the most popularity.

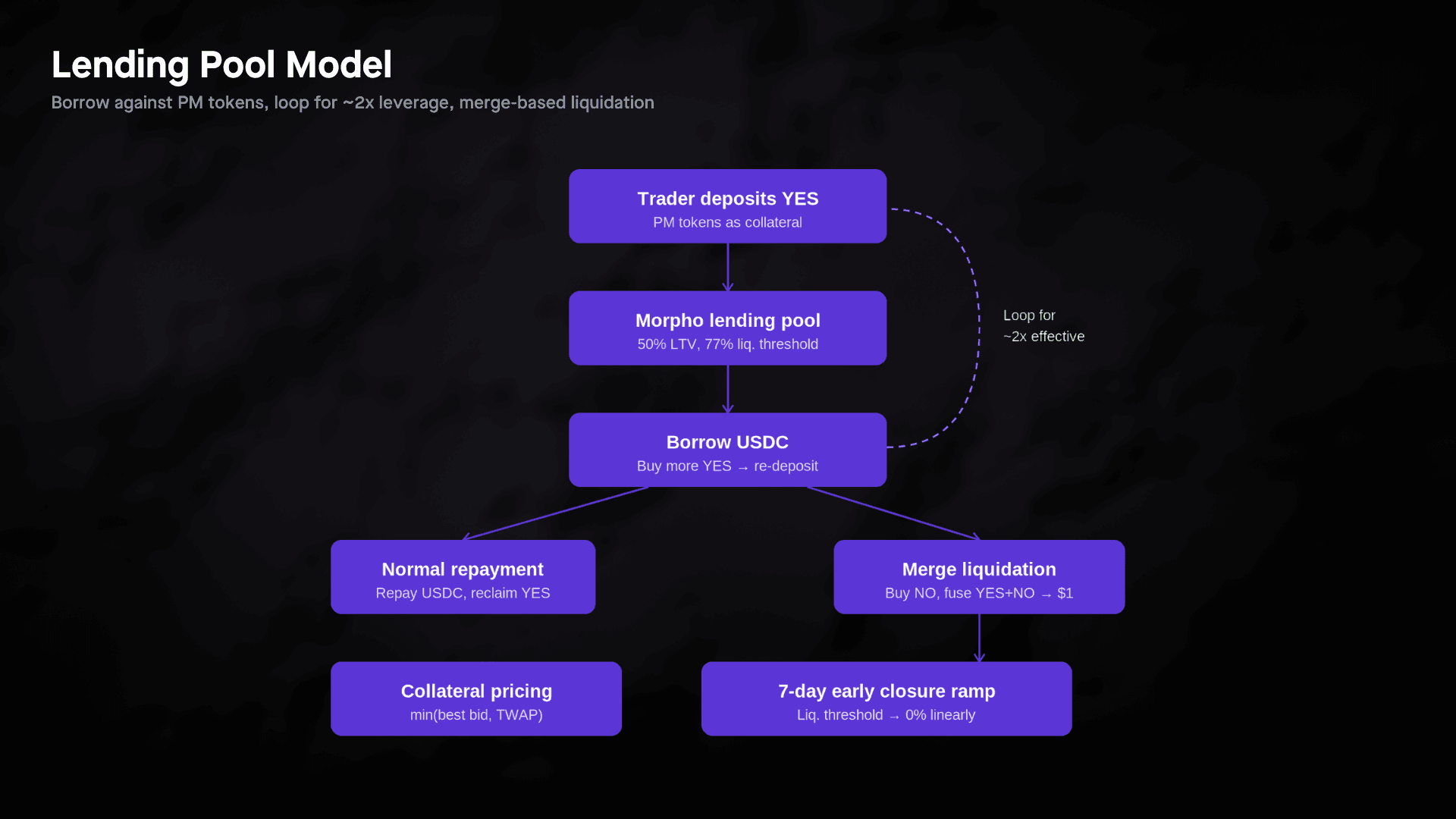

The Lending Pool

The lending pool model provides leverage in a manner similar to onchain lending markets. Just as Aave users deposit collateral and loop borrowed funds to lever up on the same asset, tokenized prediction market positions can in principle be used as collateral within lending vaults. Polymarket positions are tokenized as ERC-1155 NFTs, so they can be readily integrated into lending systems such as Morpho vaults. A similar framework may eventually emerge for Kalshi given its DFlow tokenization.

In this model, tokenized shares are treated as collateral. Traders deposit existing positions and borrow stables against them, and then increase exposure through looping: borrow, buy more shares, redeposit, repeat. The pool itself is the financier, while the risk of losses is socialized across users. This structure creates scalable leverage but also means that mistakes in risk management are weathered collectively. Existing protocols like Gondor manage jump risk, the danger that an asset’s price moves abruptly, by linearly reducing liquidation thresholds to zero over a fixed period before market-end. This forces positions to unwind gradually as the market approaches expiration. There are a few possible issues here: (1) the linear reduction does not necessarily address interim jump risk and (2) a toxic flow problem may be created if an actor knows a set of markets will have their leverage deflated by a set period of time, then this creates an opportunity.

The risk engine in this model is fundamentally LTV-based with PM specific safeguards. At its core are familiar lending parameters: a borrow cap and liquidation threshold.

From there, three additional controls are needed:

1. A collateral oracle for shares: Gondor uses minimum best bid and TWAP.

2. Per-market exposure caps to limit concentration and cascade risk.

3. An early closure ramp that pushes thresholds to zero as resolution arrives, where interest rates follow a standard DeFi utilization curve with caps by risk tier.

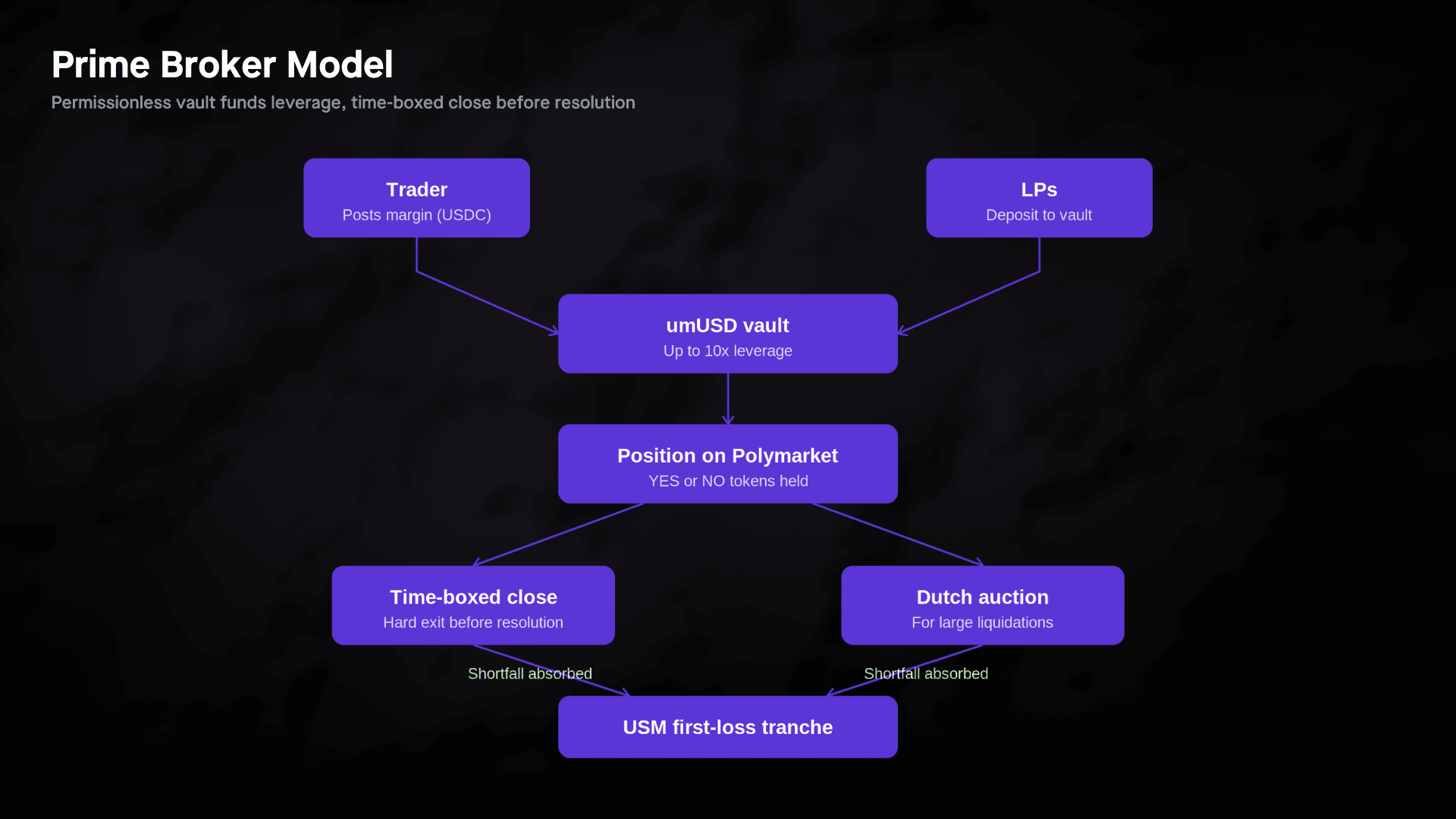

The Prime Broker

The prime broker model differs from the lending-pool approach in one important respect: leverage is managed natively by the venue rather than funded through a pooled credit vault. Instead of treating prediction-market shares as collateral inside a socialized lending pool, the platform monitors account health directly, sets risk limits at the venue level, and actively manages liquidation when positions become distressed. Therefore, it is better understood as a venue-native margin model than a pure lending protocol.

Ultramarkets is a good example of this design: positions are monitored using a health metric, and liquidation is triggered once that health falls below a fixed threshold. Where it diverges from the lending pool method is in three areas:

1. Leverage caps are set per market based on liquidity depth, volatility, and time-to-close;

2. Position limits have three levels: per-position, per-user, and per-market aggregate OI;

3. Market selection criteria prioritize predetermined resolution schedules.

The largest difference is the liquidation mechanism. Ultramarkets uses a two-phase system: direct market selling for small positions and Dutch auctions for large ones.

These are architecturally very different approaches to the same problem (minimizing creep risk during liquidation and causing a cascade event). Each has its own slippage profile. The lending pool’s approach has zero sell-side market impact but introduces buy-side slippage on the opposite outcome. The prime broker's Dutch auction has minimal order book impact but depends on liquidator participation which may not be developed as prediction markets are newer instruments.

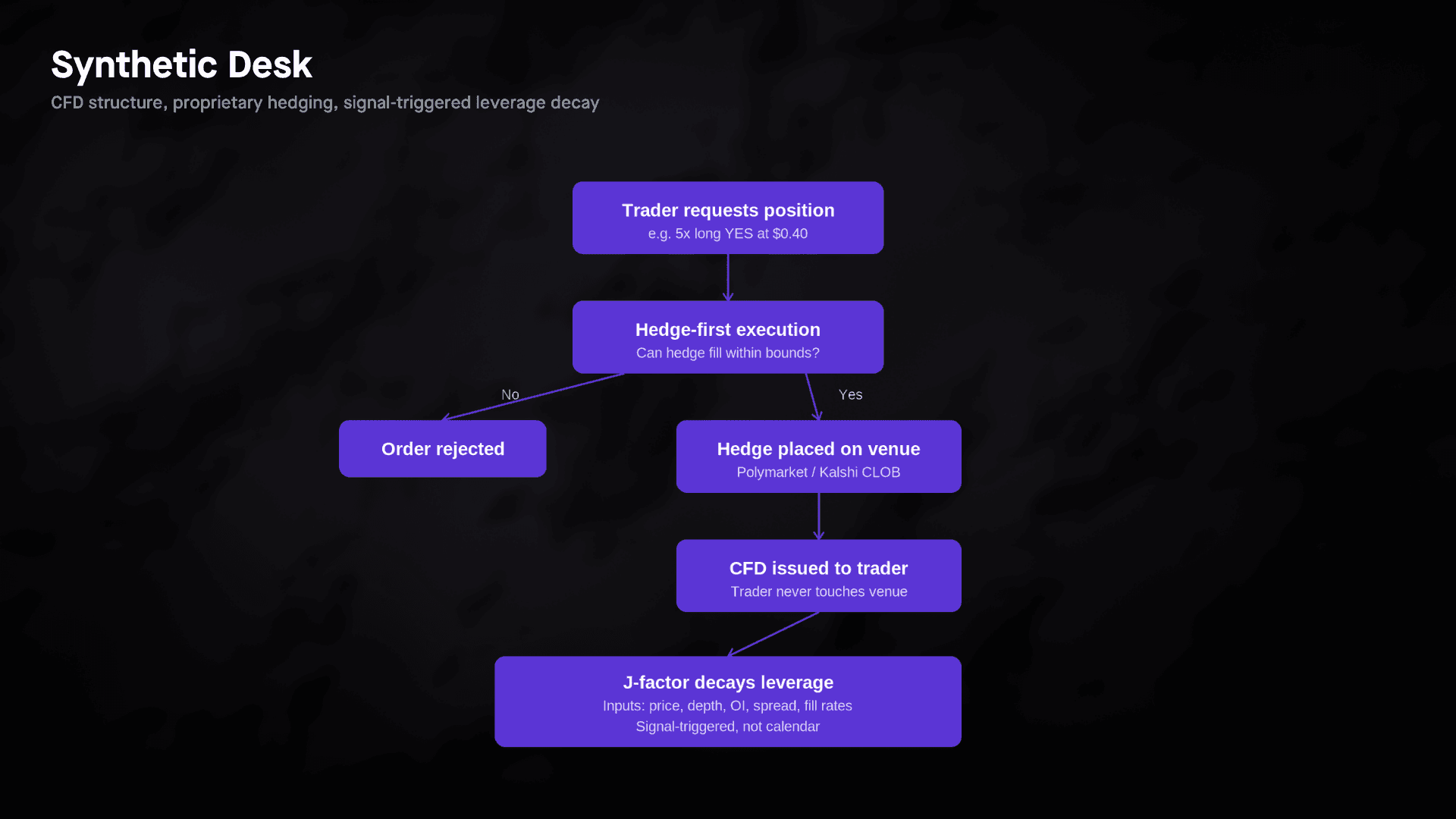

The Synthetic Desk

The synthetic desk model takes a different approach: the trader never directly touches the prediction market. Instead, the desk sits between the trader and the underlying venue as counterparty. The trader chooses a direction, leverage level, and collateral amount; the desk records a synthetic position and hedges it on the underlying market using its own capital. The trader’s PnL becomes a leveraged function of probability movement, while the hedge offsets that exposure. Structurally, this is a Contract for Difference (CFD): the trader holds a synthetic claim on price movement, not the underlying market position itself. Today, Dimes Multiply is the closest implementation of this model. Multiply is a middle-layer protocol that sits between onchain trading front-ends and Polymarket, extending credit on top of prediction market positions while managing all liquidity, hedging, and risk internally, offering up to 10x leveraged exposure without requiring front-ends to build any leverage infrastructure themselves.

Because the desk holds the hedge and the trader holds only a synthetic claim, the desk has full control over the position lifecycle. It can reduce leverage, accelerate unwinds, net exposures across users, and separate user liquidation from hedge execution on the underlying venue. That is what distinguishes the synthetic desk from the other models: risk management is internalized by the desk rather than embedded in the trader’s onchain position.

Within this structure, implementations can range from unopinionated to fully opinionated. An unopinionated desk is essentially a matching layer: it provides the CFD infrastructure, but independent capital providers determine which markets to support, how much leverage to offer, and at what price. Risk intelligence lives with the providers, who compete on underwriting and pricing. A fully opinionated desk does the opposite. It sources committed capital, runs its own risk engine, decides which markets to support, and sets all terms centrally, so the trader faces a single integrated counterparty. Dimes leans toward the opinionated end of this spectrum: rather than relying on pool-based TVL, Multiply uses a dedicated Underwriting Facility — an institutionally-sourced, pool of capital capable of underwriting millions in monthly volume — to finance hedges while handling jump risk.

In the more opinionated version, the desk can pair the CFD shell with a more sophisticated risk engine.

First, it selectively underwrites markets based on jump profile, resolution mechanics, and microstructure, refusing leverage where binary settlement makes jump losses unmanageable.

Second, it applies dynamic leverage decay: as time-to-resolution shortens or liquidity deteriorates, allowable leverage falls, and the desk automatically reduces both the synthetic position and its hedge.

Third, this decay can be asymmetric, preserving more leverage on winning-side positions while de-risking losing-side positions more aggressively. Fourth, while decay parameters may be set at entry, execution can still respond to live market conditions rather than fixed calendar dates alone, making the unwind less predictable and less easy to front-run.

The tradeoff is legibility versus sophistication. The unopinionated desk is more transparent: pricing is observable, capital providers compete openly, and no single entity controls the risk model. But it is less capable of complex portfolio-level risk management. The opinionated desk can net exposures, adapt deleveraging in real time, and manage the book holistically because it sees everything. The cost is trust: the trader is relying on a black-box counterparty whose risk engine is the product.

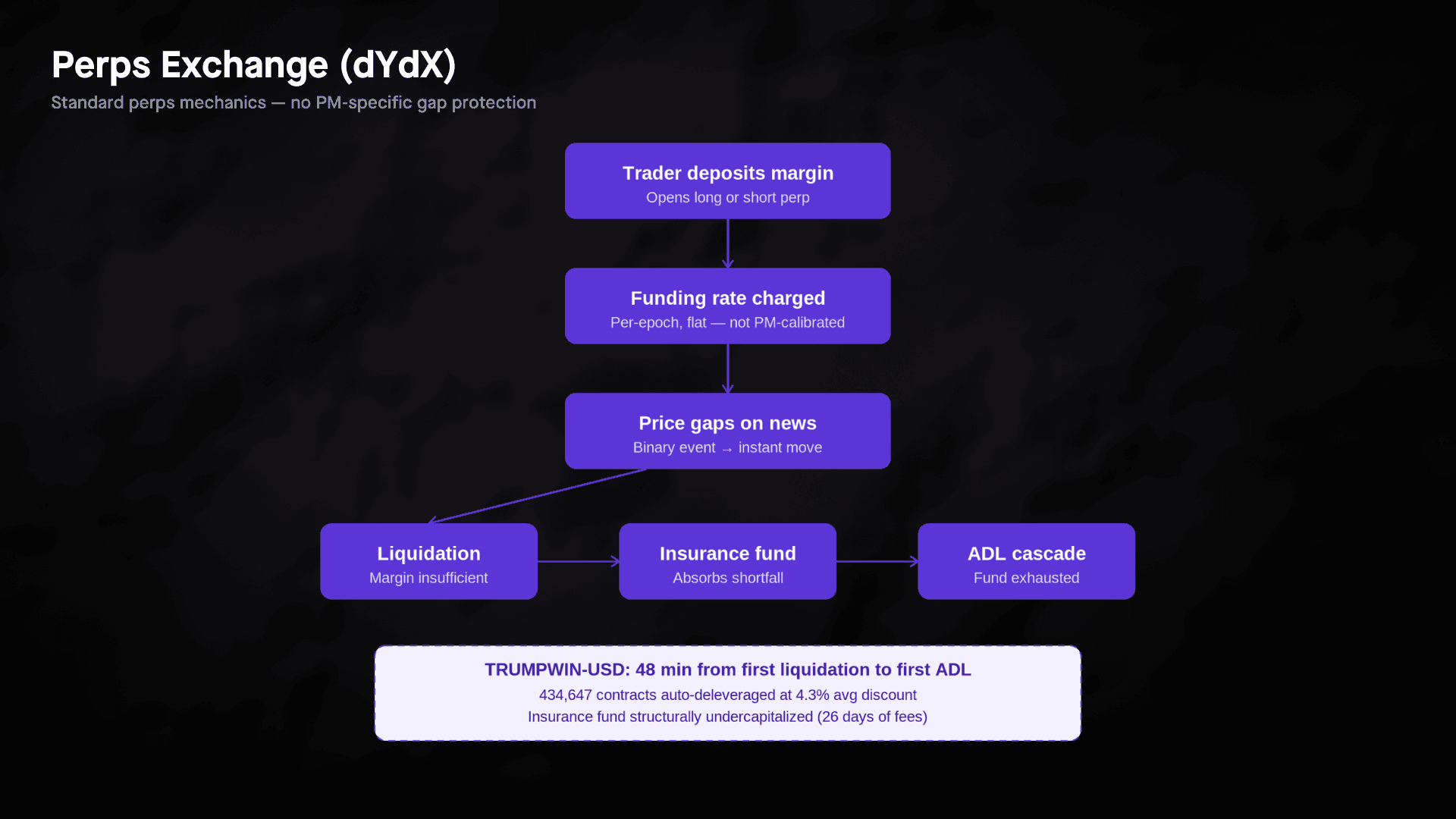

The Perps Exchange

Perpetual futures remove the expiration date from a standard futures contract and replace calendar convergence with a funding rate, a periodic cash transfer between longs and shorts that keeps the contract price tethered to spot. The mechanism self-corrects naturally as some traders simply cannot keep making these payments.

It’s been applied to prediction markets in a few cases, notably dYdX’s TRUMPWIN-USD leverage market, which tracked Polymarket's TRUMPWINYES contract directly. The oracle price was sourced from Polymarket, and funding rates operated identically to any other dYdX market.

The shortcoming is structural. A standard perp assumes a persistent, balanced fight between longs and shorts, the funding rate only works if both sides exist in reasonable proportion. Prediction markets violate this because of their convergence. As an outcome becomes probable, the price converges toward $0 or $1, and one side of the book collapses. The losing side has no incentive to hold; the winning side has no counterparty to pay them. Funding, designed for perpetual mean reversion, blows up exactly as the contract approaches its most important moment.

Market Sizing for Leverage: The 2024 Election

We can model the potential for leverage by using the 2024 election. Polymarket’s 2024 election is a decent example of what a leveraged prediction market could look like; it was highly liquid, long in duration, and only saw increased news sensitivity risk twice: upon Joe Biden’s exit from the race, and on the day it mattered most, election day. In fact, the 2024 election had a leverage layer built on top of the Polymarket Election Winner market in the form of TRUMPWIN-USD. This was a perpetual leverage market developed by the dYdX team specifically for whether Donald Trump would win or not. We will analyze this market on a later date in a note on prediction market microstructure and architecture.

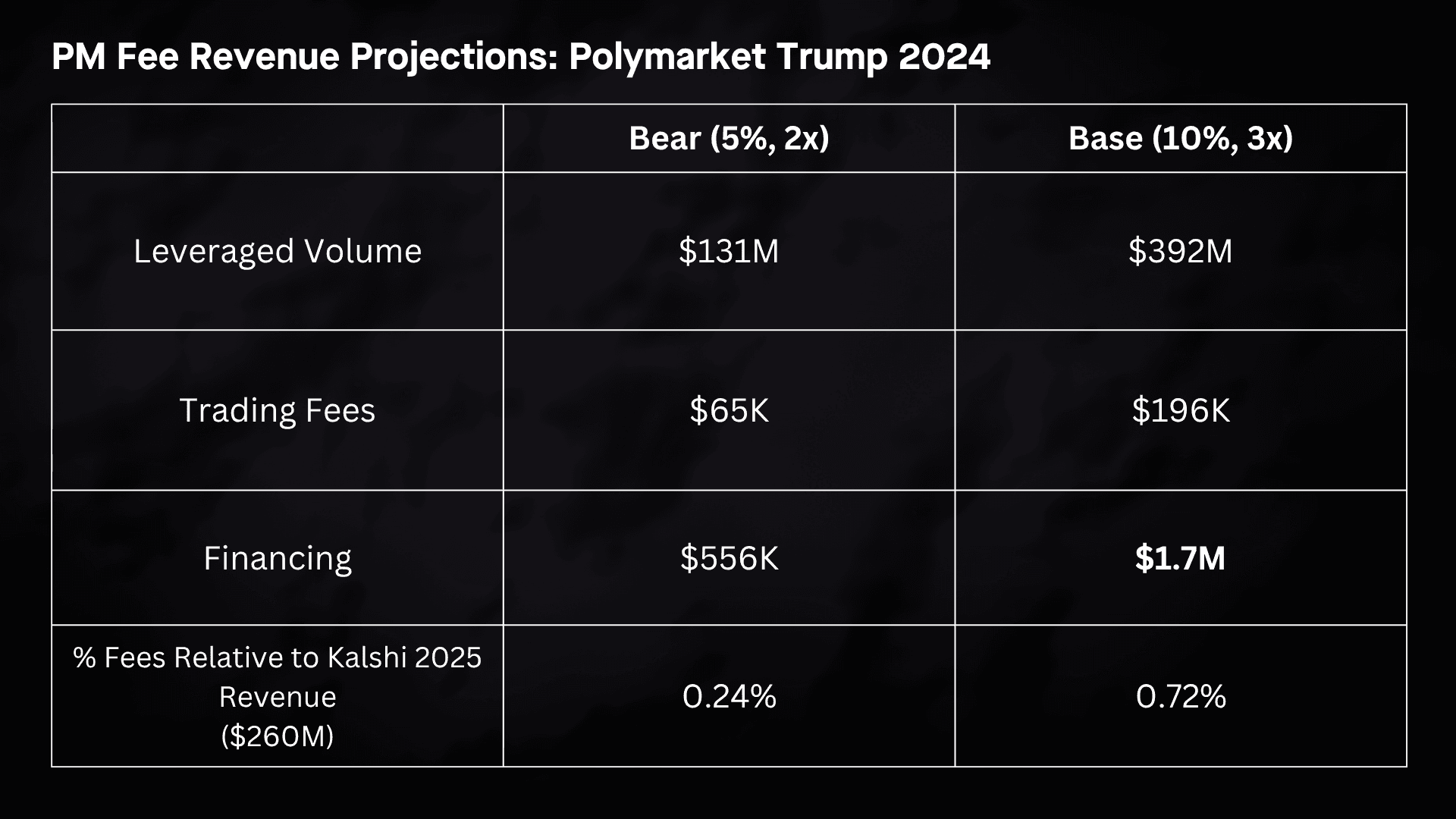

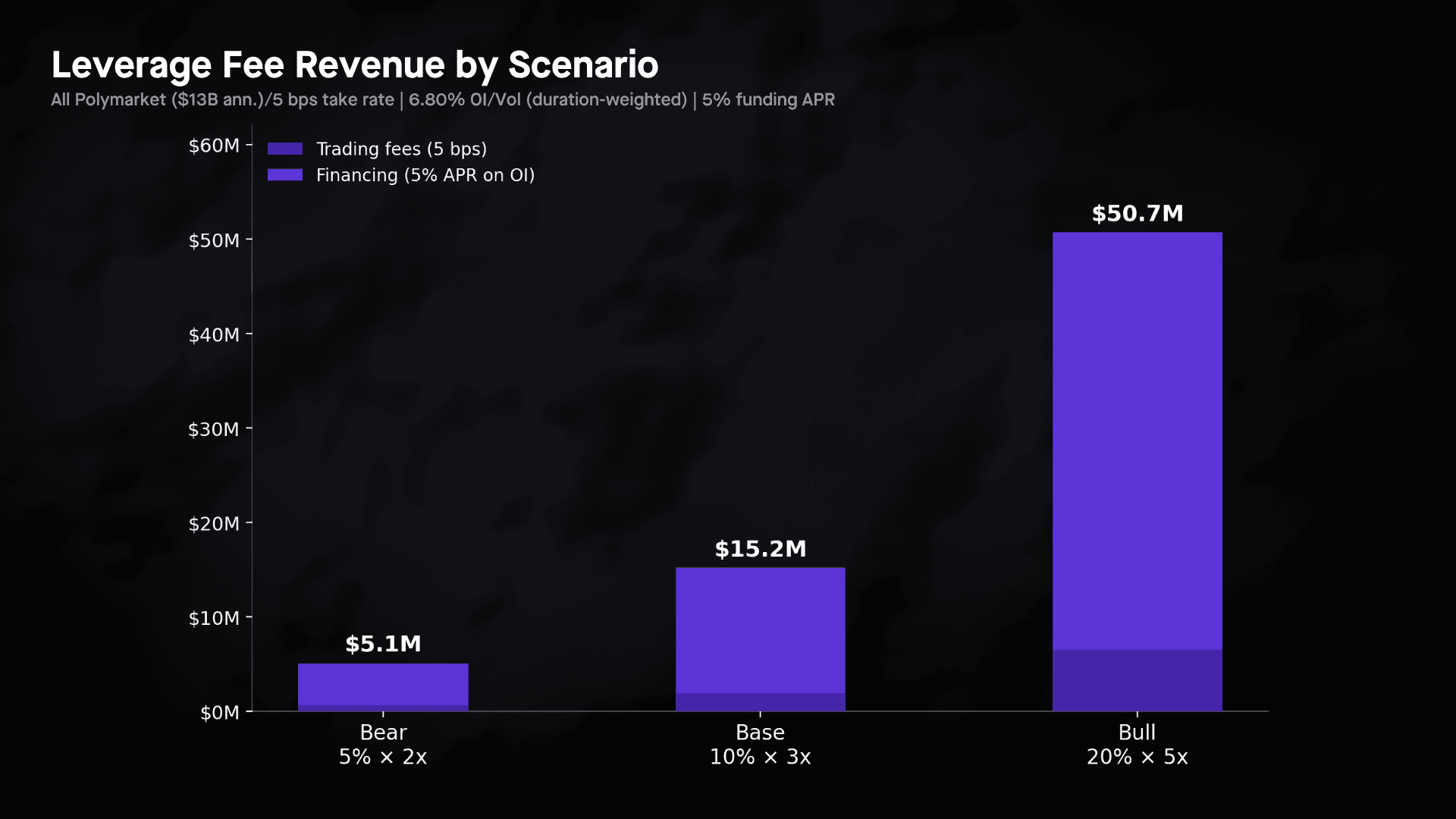

To size the leverage opportunity, we model gross fee revenue under three scenarios — bear, base, and bull — across two views: the full Polymarket platform ($13B annualized spot volume) and the 2024 US Presidential Election as a single-market case study ($1.3B spot, anchored to the dYdX TRUMPWIN-USD perp). This abstracted TAM model assumes leverage exists in a well-functioning form. It excludes protocol-specific risk costs, liquidation slippage, insurance fund requirements, and capital expenses.

Our revenue here has two components: trading fees (5 bps on leveraged volume, benchmarked against dYdX and Binance Futures) and financing revenue (5% APR on average open interest). The financing rate represents what a financier charges a leveraged trader for capital exposure, distinct from a perpetual funding rate, which is a peer-to-peer balancing payment between longs and shorts. Our 5% is conservative; for dYdX’s TRUMPWIN leverage market, the annualized funding rate ran at a default of 10.95% and spiked above 86% on election night, confirming that the market was willing to pay multiples of our assumption for leveraged PM exposure. Penetration and leverage multiple are decomposed explicitly. Bear assumes 5% of spot volume uses leverage at 2x average, base 10% at 3x, and bull 20% at 5x.

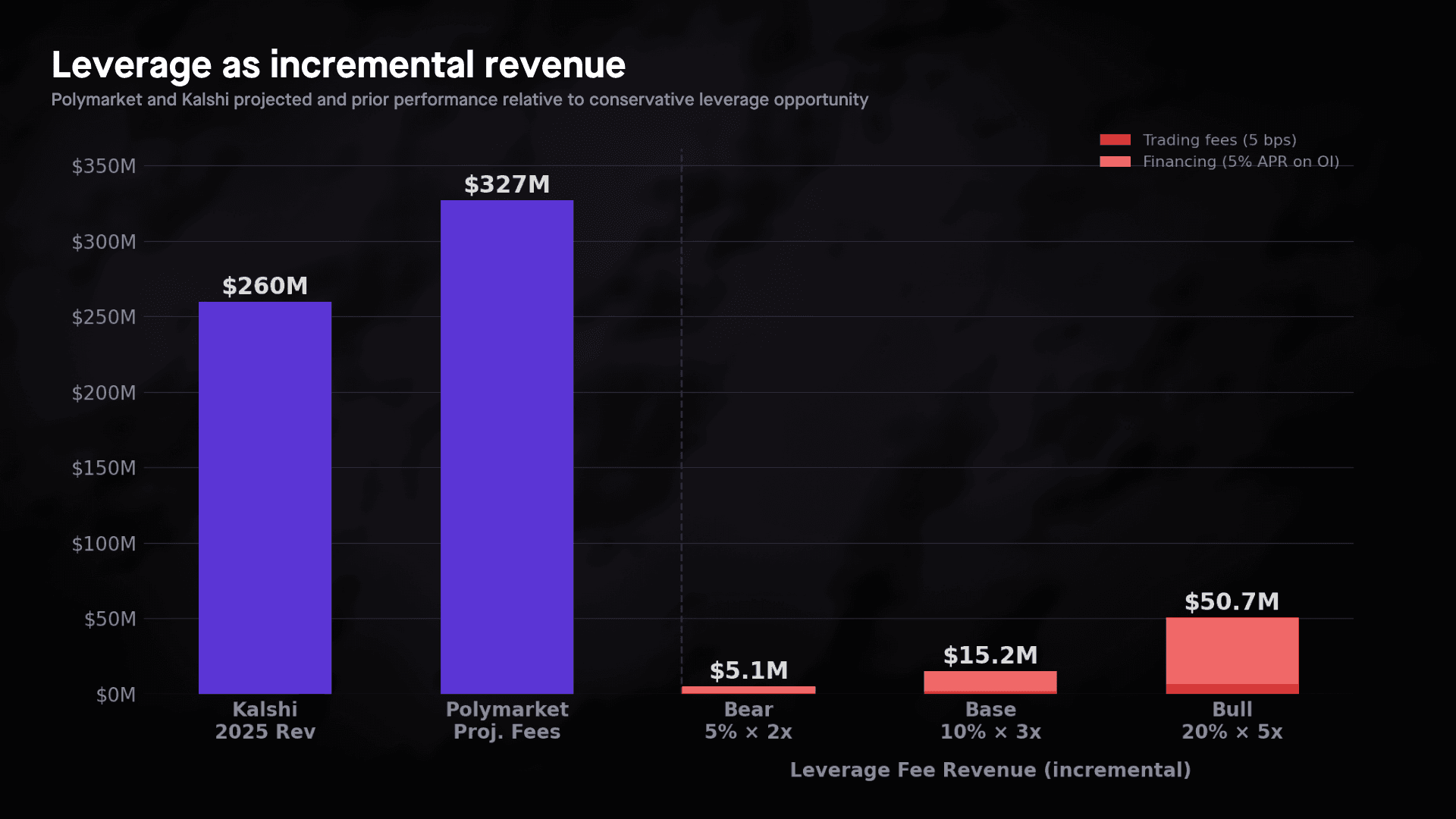

In the base case, the platform view generates approximately $15M in annual fee revenue. The bull case reaches $50.7M. Financing revenue accounts for over 87% of the total in both views, and the leverage feature's economics are driven almost entirely by how much open interest it can sustain, rather than transaction volume. That has implications for which model wins long-term: the one that keeps positions open longest.

Leverage fee revenue in the base case represents roughly 6 cents of incremental earnings for every dollar Kalshi generated in 2025 ($260M), additive on top of spot. Polymarket's own recent introduction of taker fees this month project $290-$365M annually at current volumes reinforces this position. Nevertheless, this model is very conservative, especially at the 5% APR assumption, and makes other assumptions, like a fixed financing rate across all markets. It also doesn’t attempt to create a mix of different leverage positions (2x, 3x, etc) and show them all in tandem.

The Shared Dependency

Ultimately, prediction markets will see leverage in some form or another. The question is how scalable it can be, and for that we need to address the elephant in the room: venue structure. Centralized limit order books, or CLOBs, are not the perfect structure for prediction market contracts. Today, both Kalshi and Polymarket largely treat all events the same, and the CLOB architecture used across different markets leaves vulnerabilities for market makers — vulnerabilities that flow directly downstream to every leverage protocol built on top of them.

Gondor illustrates this clearly. Its collateral oracle prices positions using the minimum of the best bid and a TWAP, a sensible manipulation-resistance choice, but one that's only as reliable as the order book beneath it. When market makers pull liquidity during a jump event, the best bid can become stale or disappears, and the oracle can degrade when accurate collateral pricing matters most. The seven-day early closure ramp, linearly reducing the liquidation threshold to zero before resolution, is, in part, a calendar-based workaround for a microstructure problem Gondor cannot fix on its own. Every model in this paper has a version of this constraint baked in somewhere.

On Nov. 22, 2025, Kalshi had a market for the Dallas Stars vs. Calgary Flames NHL winner, trading around 60¢ with genuine uncertainty. During the shootout, a wave of YES buying drove the price to 99¢. When the game shifted, informed NO sellers swept 37,239 contracts against resting YES limit orders that had not been cancelled with stale limit orders reflecting a game state that was essentially determined. The largest single fill was 21,840 contracts at 99¢. The market resolved NO twenty minutes later.

Note: The large orange cluster at 99¢ in the shaded yellow region represents 21,840 contracts filled against a resting YES limit order at 99¢. The contract resolved at 0¢ twenty minutes later, an adverse selection loss of approximately $21,384 on a single fill.

This is a consequence of running a continuous limit order book on a market where information arrives discretely and not all participants see it at the same time. The four models examined in this report, the lending pool, the prime broker, the synthetic desk, and the perps exchange, each represent a serious attempt to solve the leverage problem. They differ in how they price jump risk, manage liquidations, and source capital. None of them are broken, though each one, in its own way, works around a structural problem it cannot fix by itself.

The opportunity ahead is significant. The 2024 US Presidential Election alone traded $2.73B on Polymarket with a live leverage layer running on top of it in real time. Gondor raised $2.5M in December 2025 specifically to build lending and leverage infrastructure on Polymarket. As recurring high-volume markets mature across politics, economics, and sports, the total surface for leverage provision grows with them. As a base case, a well-functioning leverage layer across Polymarket generates approximately $15M in annual fee revenue, reaching $50.7M in the bull scenario. Over 87% of that comes from financing revenue, not trading fees, meaning that it's entirely driven by how much OI the feature can sustain. But capturing that opportunity at scale means addressing venue structure directly, not pricing around it. What a purpose-built prediction market venue could do differently, and how batch auction design could change the break-even economics for financiers and market makers alike, is the subject of our next report.