Meta-Analysis on Incentive Programs

Key Takeaways

This report distills Blockworks Advisory’s research on incentive programs and their analysis, offering a foundation for designing future initiatives and advancing industry-wide standards. By highlighting key lessons and methodologies, we aim to empower protocols to make informed, data-driven decisions.

- A successful incentive program achieves a net inflow of capital that exceeds the value of rewards distributed, while also reshaping the protocol's dynamics to sustain benefits even after the incentives are withdrawn.

- Well-designed incentives can trigger a self-sustaining flywheel effect, where liquidity attracts trading volume, and trading volume draws more liquidity, leading to long-term gains in TVL and market share even after incentives end. However, success depends heavily on precise pool selection, efficient resource allocation, and the ability to adapt to diminishing returns.

- A foundation is laid for improving strategies to better understand and optimize incentive programs, focusing on approaches to normalize against market dynamics, selecting the right metrics and analyzing user behaviour.

- The focus should shift to productive metrics—those tied to revenue-generating activities and reflective of protocol quality and usability. To address this, a new metric, Volume-Adjusted TVL Growth, was developed and put into action. This metric penalizes TVL growth when the Volume-to-TVL ratio decreases and amplifies growth when the ratio increases.

- By balancing simplicity and complexity, methodologies can reduce bias and ensure actionable insights. Advanced techniques, such as Synthetic Control, highlight the importance of leveraging robust data to isolate program effects and evaluate causal impacts.

- Successful incentive programs require a balance of careful design, active management, and adaptability. Incentives are most effective when they target sustainable behaviors, such as improving price execution or bootstrapping underutilized pools, rather than mercenary activities like trade mining.

- Pool selection is critical, and programs benefit from dynamic, data-driven adjustments to maximize efficiency and returns. Flexibility in structure and duration, alongside active community engagement, ensures better alignment with user needs and market conditions.

- A continuous feedback loop—monitoring, analyzing, and iterating incentive strategies is key to foster long-term protocol growth.

Introduction

Incentives are the foundation of any decentralized system. For such systems to thrive, agents must be motivated to act in ways that benefit both the system as a whole and its users. This underscores the critical importance of designing well thought-out incentive mechanisms. In the crypto industry, incentives play a pivotal role across multiple levels. At the blockchain level, to achieve consensus and deter malicious actors or at the application level and beyond, for example, enabling efficient cross-chain intents and solvers.

Incentives can either be built directly into the system—such as through Byzantine Fault Tolerance algorithms—or layered on top of ecosystems and applications as targeted incentive programs. These programs often aim to enhance competitiveness and attract users to the system. This report focuses specifically on incentive programs at the application layer, targeting individual protocols. At their core, these programs aim to drive growth. A successful incentive program achieves a net inflow of capital that exceeds the value of rewards distributed, while also reshaping the protocol's dynamics to sustain benefits even after the incentives are withdrawn.

In recent years, we’ve seen incentive programs both succeed and fail. This case study aims to consolidate the best research on incentive programs, focusing primarily on DEXs while drawing relevant insights from other verticals. Rather than attempting to be exhaustive, this study highlights the most significant and unique lessons learned, and discusses some of the current well-documented methodologies of the industry for design and analysis. Based on extensive internal research, this report offers a glimpse into the work we’ve been doing to better understand incentive program dynamics and to help protocols make more informed, data-driven decisions.

The first section explores the overarching impact of incentive programs and their significance as well as theory behind it in the context of DEXs. The second section examines the approaches used to create and assess incentive programs. It addresses common challenges, such as accounting for market trends, selecting appropriate metrics, and the necessity of deep market and protocol understanding before program design. The final section summarizes what has been proven to work (and what hasn’t) based on the analyses reviewed, distilling actionable insights for future programs.

Effectiveness of Incentives

At the DEX level, incentives have proven effective in jumpstarting a positive flywheel effect. While it’s widely acknowledged that liquidity is mercenary—flowing to where incentives are most abundant—properly designed programs can leave a lasting impact. Under the right conditions, overall engagement levels often remain higher after the program ends, even if they don’t match the peak levels achieved during the incentives.

The core theoretical idea is that liquidity facilitates volume bootstrapping, enabling incentives to create long-term effects on TVL and trading volume. Here’s how it should work: incentives in a specific pool attract an initial influx of liquidity from yield-seeking liquidity providers. Increased liquidity improves price execution for the trading pair, drawing more trading volume to the pool.

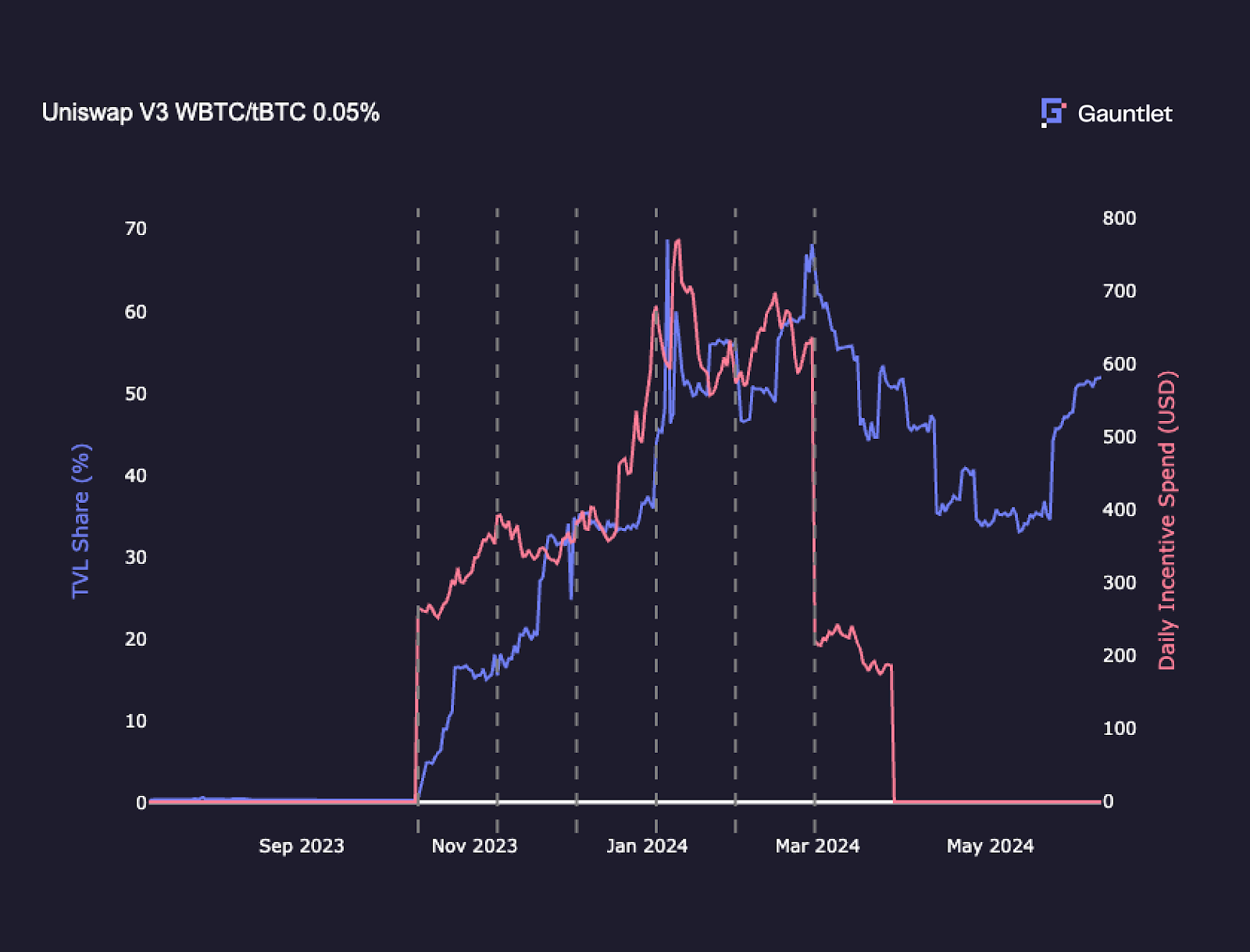

Higher trading volume, in turn, raises yields, encouraging additional liquidity providers to deposit. This creates a positive feedback loop, where higher volume attracts more liquidity, which further enhances trading efficiency and sustains growth. Even when incentive programs end, and some liquidity providers withdraw, the pool often remains a better trading venue due to improved execution. Consequently, a portion of the trading volume—and the liquidity it attracts—remains, preserving part of the program’s gains. The image below provides a concrete example of the described flywheel effect in action for a Uniswap pool.

Source: [5] Results and Analysis: Uniswap Arbitrum Liquidity Mining Program, July 2024, Gauntlet

This leads to two critical questions: How elastic are traders in the DEX ecosystem to price execution? How elastic are liquidity providers to trading returns?

Understanding these dynamics is essential for the industry to design effective and sustainable incentive programs for DEXs, and Gauntlet has played a notable role in advancing research and insights in this area.

In July 2023, Gauntlet’s trade mining analysis [2.1], conducted as part of the Uniswap Incentive Design Analysis [2], found that only about 1% of total DEX trading volume was routed sub-optimally. This indicates that the vast majority of trades are efficiently executed, flowing to the exchange offering the best results rather than remaining "sticky" to any particular platform. Further supporting this, 94% of trading volume was shown to come from whales or MEV activity, both of which are inherently non-sticky participants. These findings suggest that effective incentive mechanisms should focus on improving price execution rather than directly rewarding trading activity.

Gauntlet’s analysis of Uniswap’s liquidity mining program on Optimism [1] had previously also tested this volume bootstrapping mechanism and found it effective in two out of five pools—wstETH/WETH 0.05% and OP/USDC 0.3%—where sustained increases in TVL and trading volume persisted even after the incentives ended. However, for the remaining three pools—USDC/DAI 0.01%, WETH/DAI 0.3%, and OP/USDC 0.05%—the results were either inconclusive or showed no significant long-term impact.

In the Uniswap Arbitrum Liquidity Mining Midpoint Retro [4], Gauntlet explored whether there is a soft limit at which increasing liquidity no longer improves price execution, and thus fails to attract additional trading volume. Using their fee simulation tools, they analyzed the percentage of trades routed efficiently and, among those, how many were directed to Uniswap. They also simulated scenarios to estimate how much volume could theoretically be re-routed from competitors if liquidity were improved, aiming to identify points of diminishing returns. In some cases, competition came from pools offering lower LP fees. This means that even under scenarios with extreme liquidity, the incentivized pool could not achieve superior price execution compared to these competitors. However, this approach represented a step forward in refining methodology for selecting pools to maximize incentive efficiency by identifying those with untapped potential for volume capture and determining the liquidity increases required for dominance in specific trading pairs.

Over the course of the program, culminating in the Results and Analysis report: Uniswap Arbitrum Liquidity Mining Program [5], the pool selection methodology shifted from being primarily market share-driven to a more advanced simulation-based approach, improving the precision and effectiveness of incentive allocation. A strong correlation (r = 0.93) was observed between TVL and liquidity within ±2% of the current tick, driven by Merkl's reward distribution, which prioritized fee-generating liquidity. Gains in volume-market share were moderately correlated (r = 0.58) with optimal-routing market share, validating the core premise of the pool selection methodology: increased liquidity enhances price execution, which draws additional trading volume. During the campaign, optimal-routing market share grew by +27.3%, adding approximately $570M in trading volume, and continued to grow by +24.8% post-campaign, contributing another $147M in trading volume.

The liquidity mining campaign demonstrated a strong ROI with sustained benefits and key to this success was the strategic shift to a scientific pool selection methodology and prompt optimizations, maintaining a tight feedback loop for adjusting pools and maximizing impact. Key results include an ROI for TVL of approximately $5.99 in additional TVL generated for every $1 spent on incentives ($1.7M total). Post-incentive TVL growth slowed compared to the during-incentive period but remained +9.8% higher than pre-incentive levels. Interestingly, the incentives effectively revived “dead pools” (pools with less than $10 in TVL), creating a lasting positive impact even after the incentives ended. However, not all pools responded to the incentives, leading to their early removal. This underscores the importance of improving pool selection criteria and actively managing incentive programs to maximize efficiency and returns.

OpenBlock’s STIP Incentive Efficacy Analysis ([8]) revealed that protocols supported by the STIP significantly outperformed non-STIP protocols on Arbitrum in terms of TVL growth, achieving an 82.6 percentage point advantage. These supported protocols were responsible for 75.8% of the nominal TVL growth on the network. To provide context, the STIP program allocated 50 million ARB tokens across 30 protocols, with distributions beginning on November 3, 2023. Under the program’s guidelines, projects were required to distribute their entire grant allocation by March 29, 2024, with any unused tokens returned to the Arbitrum Multisig. By the end of the STIP, approximately 736,000 ARB tokens were returned, reflecting unclaimed or unspent funds ([8]).

An analysis of the STIP program by StableLab also found it to be cost-effective in driving relative growth in top-line network metrics when compared to other large-scale initiatives, such as the ARB airdrop ([9]). However, user retention emerged as a significant challenge, with activity levels returning to pre-STIP figures. This highlights the need for further refinement and innovation in incentive program design to achieve sustained engagement. The STIP primarily attracted users categorized as “Traders” (94% of incentivized participants), underscoring the importance of adjusting program designs to engage a broader range of user segments. When comparing the STIP to the LTIPP, StableLab noted a key difference. In the STIP, community effort was heavily concentrated among a small subset of applicants. By contrast, LTIPP’s advisor role and council system improved the process by providing higher-quality feedback and reducing the burden on the broader community, leading to more effective outcomes.

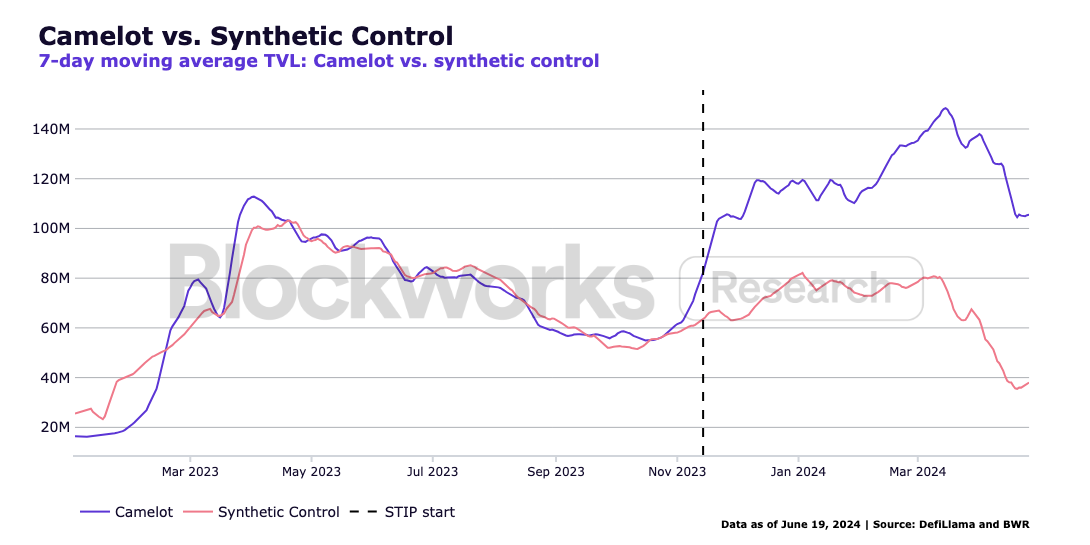

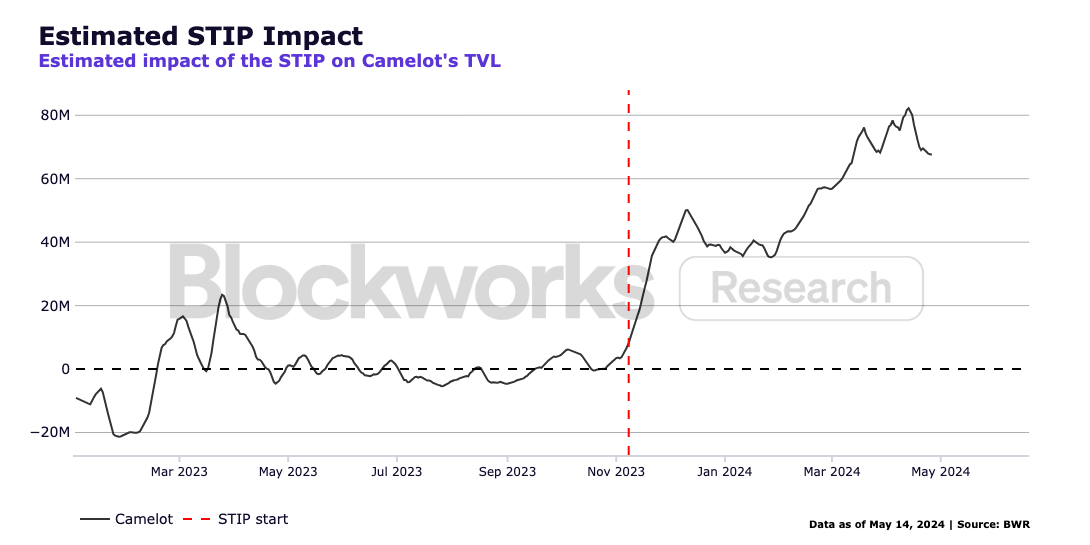

Blockworks Advisory’s analysis of the performance of the DEX vertical in the context of the STIP ([13]) yielded varied results: one protocol saw a significant 62.5% of its median TVL in the analyzed period attributed to STIP, while another saw 37.1%. Two other protocols also benefited, both with around 12% of their TVL linked to STIP incentives. During the STIP period and the two weeks following its conclusion, the added TVL per dollar spent on incentives was approximately $12 for two of the protocols, $7 for another, and $2 for the fourth one. Our analysis revealed that while different incentive distribution methods had a comparable impact on TVL across protocols, certain overarching differences still proved to be highly influential. These distinctions are explored in detail later in this report.

Source: [13] STIP Retroactive Analysis – Spot DEX TVL, July 2024, Blockworks Advisory (published under Blockworks Research)

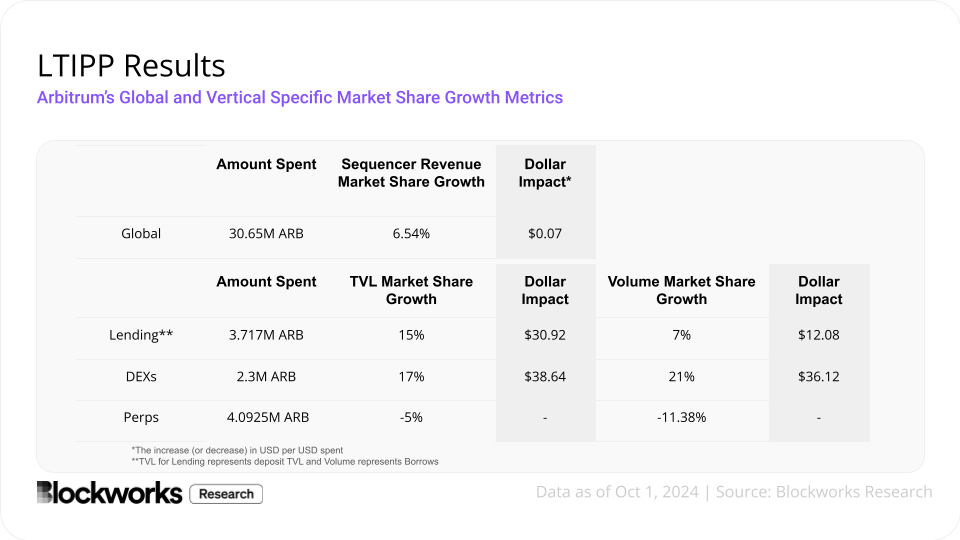

Blockworks Advisory’s analysis of the Long Term Incentives Pilot Program (LTIPP) [17] also found that incentives were effective in some cases. Arbitrum distributed approximately 30.65M ARB across various verticals, and we evaluated the program's strategy for protocols in the Lending, DEX, and Perps categories by analyzing key protocol-level metrics. The LTIPP had a notable impact on DEX and Lending activity, successfully mitigating a downward trend in sequencer revenues. The dollar cost of LTIPP for the lending category was $30.92 added TVL (normalized by market share) and $12.08 added borrows (normalized by market share) per dollar spent. For DEXs, TVL market share increased by 17%, reflecting $102.6M in added TVL (normalized by market share) during the program. This translates to $38.64 of TVL added per dollar spent on incentives. Besides this, Arbitrum’s global DEX volume market share grew significantly by 21%. When considering revenue, Arbitrum’s share of total L2 revenue increased from 6.04% to 12.58% during the program. However, the program revealed inefficiencies in sequencer revenue generation. For example, $0.07 in added sequencer revenue came at a cost of $1, highlighting significant opportunities for improvement in this area. These results suggest that while the LTIPP was effective in driving growth and activity in key areas, there is room to optimize its design for better cost-efficiency and broader impact.

Source: [17] LTIPP Analysis, October 2024, Blockworks Advisory (published under Blockworks Research)

Methodologies Review

This section explores key methodologies used to evaluate and optimize incentive programs. It delves into approaches for accounting for market dynamics, selecting and normalizing metrics, and analyzing user behavior to design effective and sustainable programs. Through an assessment of these methodologies employed to date, we aim to present a comprehensive framework showcasing the current state of the art in incentive program analysis. This serves as a foundation for identifying areas of improvement and advancing strategies to better understand and optimize incentive programs.

Accounting for market dynamics

When evaluating growth metrics, it is essential to consider them in a relative context. A strong growth rate in a market where everything else is trending similarly offers little insight into the specific impact of a program. Conversely, stagnant growth in a declining market can indicate success, as the incentives may have helped maintain levels while others declined. The key is to normalize metrics to account for broader market trends.

This raises the question: what should one normalize against? Approaches to normalization can be viewed along a spectrum, ranging from simpler to more complex methodologies. While more complex methods theoretically provide greater precision by accounting for a wider range of variables, they are only effective when sufficient, reliable data is available and assumptions hold true. In cases where data is limited or assumptions are uncertain, simpler methods can be preferable. These approaches are not only easier to interpret but also reduce the risk of introducing bias through overly complex modeling.

Ultimately, the goal is to strike a balance, using a method that is both robust and well-suited to the available data, ensuring insights remain accurate and actionable. Different methods for normalizing metrics can be imagined as points along a spectrum, ranging from simpler approaches to more complex ones.

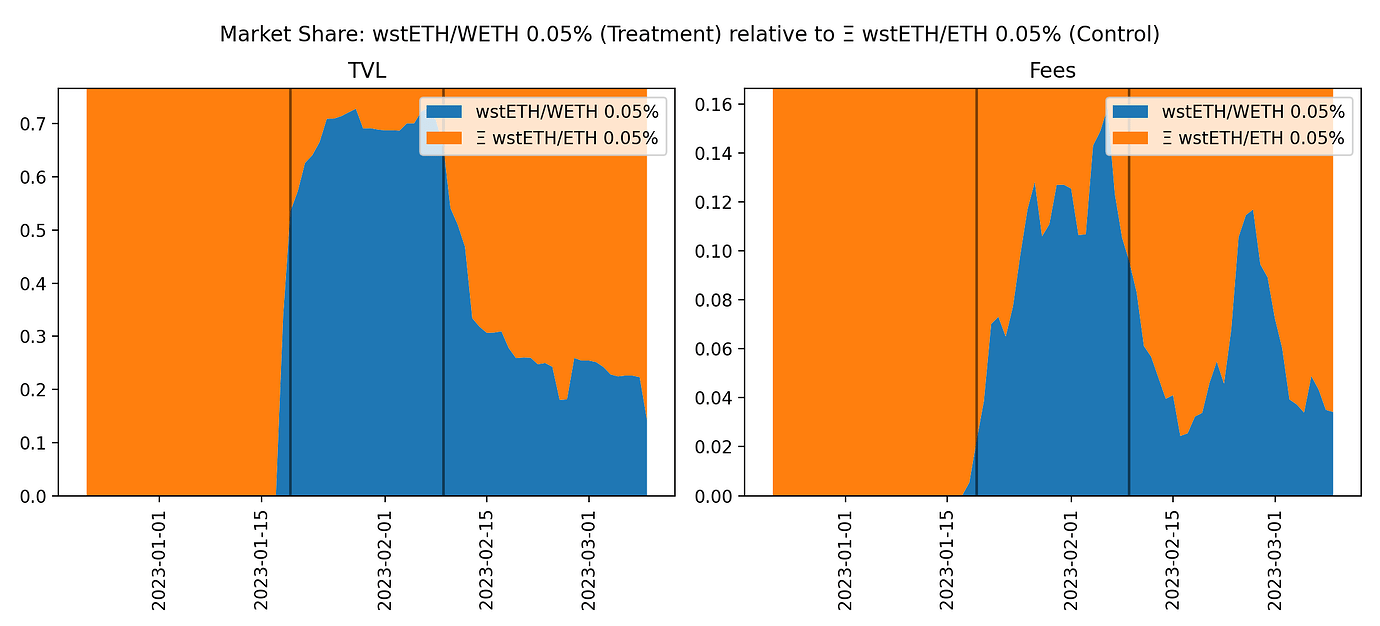

At the lower end of the spectrum, normalization can be achieved by selecting a control protocol or pool ([1]), depending on whether the analysis focuses on a protocol or a pool. For example, when evaluating the impact of an incentive program on a specific pool, this involves pairing incentivized pools with control pools to account for market trends. Statistical tests are then used to evaluate changes in metrics like TVL and volume before, during, and after the incentive period. The image below illustrates one instance of applying this method, analyzing market share growth in a pool by comparing it to a single, comparable control pool that did not receive any incentives ([1]).

Source: [1] Uniswap's liquidity mining on Optimism, June 2023, Gauntlet

This method provides a straightforward and effective comparison framework, but it comes with caveats:

- Poor selection of control pools can skew results.

- The selection process is subjective, making this a highly opinionated methodology.

Despite these drawbacks, this approach can be efficient when suitable control analogues are readily available.

In the context of ecosystem-wide incentive programs like the STIP, one could normalize by comparing growth in recipient protocols against non-recipient protocols during the same period ([8]). However, caution is warranted:

- It’s crucial to ensure the allocation between participants and non-participants is unbiased or random.

- For the STIP, protocols self-selected by applying for incentives, and allocation was based on proposal merit. This introduces potential bias, as participating protocols were likely more proactive in pursuing growth even without STIP.

As a result, performance differences may not fully reflect the program's impact.

For Uniswap Arbitrum Liquidity Mining, Gauntlet compared pool-level metrics (e.g., liquidity, volume, and fees) against Uniswap’s total metrics on Arbitrum ([4]). This approach helped assess whether incentivized pools outperformed. However, the methodology’s effectiveness depends heavily on pool selection. If pool selection is not random (which is most likely the case), the results may lack informativeness.

A more comprehensive approach involves measuring market share growth for key metrics ([5], [17]). This entails analyzing pre-incentive, during-incentive, and post-incentive periods, with each period defined by, for example, a 30-day window. Incremental changes in TVL, volume, and LP revenue are calculated by multiplying the change in market share by total market values, including both incentivized and competing pools. This method normalizes aggregate market effects, such as price fluctuations and demand shifts, and focuses on market share—a metric closely aligned with the goals of most incentive programs. It’s less subjective, as it reduces reliance on selecting a single control pool, and is particularly informative for assessing competitive positioning.

Source: [17] LTIPP Analysis, October 2024, Blockworks Advisory (published under Blockworks Research)

Another effective method is incorporating market dynamics into ROI calculations. For instance, Gauntlet’s analysis of Jito’s incentive program used a composite ROI formula that adjusted for changes in both Jito’s TVL and recipient pool TVL ([6]). This method accounts for broader market movements and enables direct comparison across incentive programs by producing a single, reproducible ROI value.

Causal Impact Analysis is an advanced method used to assess the effects of incentives on top-line network metrics ([9], [12]-[16]). This approach divides data into pre-event and post-event periods, using statistical models to predict the expected trend if the event (incentive) had not occurred. The difference between actual and predicted values represents the event’s impact. While dynamic market conditions may introduce unaccounted variance, this method offers a solid baseline for evaluating causality.

The Synthetic Control (SC) method, a specialized form of Causal Impact Analysis, was employed by Blockworks Advisory for retroactive analyses of STIP across multiple verticals ([12]-[16]). The SC method is a statistical technique utilized to estimate causal effects resulting from binary treatments within observational panel data. Regarded as a groundbreaking innovation in policy evaluation, this method has garnered significant attention in multiple fields. At its core, the SC method creates an artificial control group by aggregating untreated units in a manner that replicates the characteristics of the treated units before the intervention (treatment). This synthetic control serves as the counterfactual for a treatment unit, with the treatment effect estimate being the disparity between the observed outcome in the post-treatment period and that of the synthetic control. In the context of our analysis, this model incorporates market dynamics by leveraging data from other protocols as the untreated units. Thus, changes in market conditions are expected to manifest in the metrics of other protocols, thereby inherently accounting for these external trends and allowing us to explore whether the reactions of the protocols in the analysis differ post-STIP implementation.

Source: [13] STIP Retroactive Analysis – Spot DEX TVL, July 2024, Blockworks Advisory (published under Blockworks Research)

This approach provides several advantages:

- Reduced bias: The model itself selects relevant data points for trend estimation, reducing issues with subjective control selection.

- Significance testing: Robust statistical tests are available to validate the reliability of the results.

Among these methods, the Synthetic Control method stands out for its ability to account for market trends while minimizing analyst bias. By leveraging diverse data points and allowing the model to determine useful trends, this approach enhances reliability and interpretability. However, it requires substantial historical data to produce trustworthy results, which may limit its applicability in all cases.

In conclusion, the choice of normalization method should balance data availability, methodological rigor, and the specific goals of the analysis. Simpler methods may suffice in straightforward scenarios, while other techniques like market share analysis, ROI embedding, and Synthetic Control offer greater precision when sufficient data and resources are available.

Choosing the right metrics

Metrics commonly used to measure the impact and ROI of an incentive program in the context of DEXs include:

- TVL added,

- Volume added, and

- Fees added

As discussed earlier, these metrics can be normalized by market share or analyzed using other methods to isolate the program's specific effects. Beyond these basic metrics, additional insights can be gained by incorporating more nuanced measures, such as:

- Added LP revenue: evaluating the direct revenue earned by liquidity providers,

- Projected future LP revenue (normalized by market share): estimating long-term revenue potential based on current trends ([5]),

- Overall ROI: calculating ROI by dividing projected future LP revenue by incentive spend ([5]). This approach, or any general normalization by the amount of incentives received, is particularly important for comparing the performance of multiple protocols in deploying incentives effectively. For instance, this methodology proved insightful in analyses of programs like STIP or LTIPP ([8], [12]-[17]).

These additional metrics provide a deeper understanding of the effectiveness of incentive programs, allowing for more accurate comparisons and insights into their long-term impact.

Analyzing these metrics in isolation does not always lead to accurate or actionable conclusions. As demonstrated in prior studies ([1]-[3]), the dynamic between TVL and trading volume is key to driving sustainable growth in DEXs. While TVL is an informative metric, it often fails to provide a complete picture on its own. Instead, the focus should shift to productive metrics—those tied to revenue-generating activities and reflective of protocol quality and usability.

Incentives should aim to enhance the protocol itself, attracting a user base that remains engaged even after the incentives are withdrawn. For DEXs, this means prioritizing trading volume in addition to TVL, as higher trading volume correlates with better price execution and a superior user experience. A DEX with robust trading volume offers more compelling value to users and liquidity providers, creating a stronger foundation for long-term growth.

In Blockworks Advisory’s most recent analysis of the Arbitrum LTIPP ([17]), we developed a new metric, Volume-Adjusted TVL Growth, to capture this dynamic. For each protocol, we collected trading volume and TVL data from before and throughout the duration of LTIPP, calculated the growth in both metrics from the 30-day median before LTIPP to the median throughout LTIPP, derived a volume-adjusted TVL metric, and normalized this metric by total ARB claimed. The equations applied in this analysis are detailed below.

This volume-adjusted TVL growth metric effectively penalizes TVL growth when the volume-to-TVL ratio decreases and amplifies growth when the ratio increases.

Another key insight from our analysis of past incentive research concerning the choice of performance metrics, is the use of averages over a given period. Averages can be problematic because they are highly sensitive to outliers, potentially distorting the true impact of an incentive program. A more robust alternative is to use the median, which provides a clearer representation of central tendencies, minimizing the influence of extreme values. For a more nuanced analysis, time series methods could also be employed to examine effects over time, offering richer insights into trends and dynamics. However, these methods are not always feasible or practical in real-time scenarios. As such, we believe that using the median represents a significant improvement for comparing periods, regardless of the metric in question.

Another critical consideration is the common use of daily active users (DAU) as a growth metric. While frequently cited, DAU is inherently flawed—especially in the context of incentive programs, where sybil activity is pervasive. For instance, during the STIP, Arbitrum reportedly added over 94,000 daily active users ([8]), but this figure alone provides little insight into the program's effectiveness in attracting genuine, engaged users.

Lastly, the time window selected for comparison plays a critical role in shaping the outcomes of an analysis. Depending on what is the thesis being studied, the most suitable time window can vary. For example, in one study ([5]), Gauntlet employed a short time window to assess statistically significant changes in pools, comparing 15 days before incentives to 15 days during incentives. This approach is based on the rationale that LPs typically respond swiftly to attractive incentives, making any changes in liquidity detectable almost immediately. Gauntlet then further distinguished between before, during, and after periods in their most recent analysis ([5]). This methodology offers greater insight into the dynamics of growth—capturing both the immediate impact of the program while it was active and the persistence of that growth shortly after the program ended.

In contrast, simpler approaches ([7]), calculate growth as the percentage difference between the starting and ending dates of the program. While straightforward, this method risks overlooking important persistence dynamics that occur after incentives conclude. Moreover, it is particularly vulnerable to outliers at the start or end dates, which can distort the results. To account for persistence dynamics in our analysis of the STIP ([12]-[16]), Blockworks Advisory utilized the median data from the two weeks following the conclusion of the incentive program. This approach allowed us to evaluate the lasting effects of the incentives while minimizing the influence of outliers and short-term fluctuations.

Understanding the users

To design an effective incentive program, it is essential to first understand the users—both those of the protocol being analyzed and those of the competition. This requires a purposeful and intentional approach, beginning with a clear definition of who we aim to attract and how their behavior will impact the protocol.

A comparative user behavior analysis provides valuable insights into:

- Who the main users are on the platform;

- What features are used by specific user segments;

- How user behavior compares to similar platforms;

This information informs key decisions, such as targeting specific user groups in future incentive programs, identifying areas for improvement (e.g., features, parameterization) to attract users from competing platforms, and understanding how to retain existing users.

By categorizing users into cohorts, we can better understand their behaviors, determine which cohorts are most relevant to the protocol, and compare these patterns with competitors. This enables deeper questions, such as why these behavioral differences exist and how incentives can address them—ensuring current users are retained and new users are attracted.

An example of this in practice is Gauntlet’s User Behavior Study for Jito ([6]), which compared Jito’s user base to competitors like Marinade, BlazeStake, and Marginfi (LST). The study categorized users based on stake size and status, revealing trends that informed Jito’s incentive strategies. Key findings included:

- Jito effectively attracted whale users, leading to sustained staking growth.

- Smaller-to-medium-sized users were less responsive to incentives, suggesting a need for tailored approaches.

- Jito users had a higher average number of withdrawal operations but a low 17% withdrawal rate, indicating strong holder retention.

- Jito wallets showed the highest net worth among competitors but had one of the lowest LST DeFi utilization rates, indicating a more risk-averse user base.

- Many wallets held at least two types of LSTs, reflecting a preference for diversification.

Resulting recommendations were:

- Redesign incentives to target distinct user cohorts, such as medium-to-large stakers.

- Leverage high-net-worth users through specialized strategies.

- Explore cross-platform partnerships and features catering to diversified stakers.

Tracking user behavior after incentives are deployed is also important, particularly through user churn analysis. StableLab’s analysis of incentive programs during STIP ([9]) sought to identify the types of users attracted by the program, assign a cost per engaged user, and measure user permanence on the network to evaluate retention and calculate metrics like churn rates and active users. To conduct this user segmentation analysis, they analyzed all active addresses and grouped them into profiles based on their interaction patterns. Each profile was defined by specific criteria, such as a transaction ratio and absolute thresholds. For example, a "gamer" profile had a game-to-total transaction ratio of 0.1 and an absolute threshold of 10 transactions.

Source: [9] StableLab: Analyzing STIP’s Efficacy and LTIPP Comparison, June 2024, StableLab

What Works and What Doesn’t

The success of incentive programs hinges on careful design, execution, and the ability to adapt to real-world dynamics. Several factors can undermine their impact, such as external incentive programs, cannibalization of liquidity or volume, and a lack of organic trading activity. These challenges, while difficult to quantify, underline the importance of understanding overarching principles and patterns across analyses. By examining all mentioned research, we can distill what works and what doesn’t in the context of incentive programs in DEXs.

Trade Mining and Payment for Order Flow: Ineffective Approaches

Trade mining, which involves directly incentivizing trading activity, has consistently shown poor results ([2.1], [12]). While the goal is to onboard new traders by subsidizing execution costs, the assumptions it relies on—sybil resistance and user stickiness—are unrealistic in practice. Gauntlet's analysis found that suboptimally routed trades accounted for only 1% of DEX trading volume on Ethereum, demonstrating the limited scope for improvement through these programs. Furthermore, users rarely continue trading after incentives are removed, rendering such programs ineffective in the long term.

Similarly, Payment for Order Flow (PFOF), which incentivizes aggregators to preferentially route trades, proved inefficient ([2.2]). While it can theoretically enhance liquidity by increasing order flow, its high costs and inability to target specific LPs make it a suboptimal strategy. With most DEX trades already routed optimally, PFOF provides minimal incremental benefit and struggles to create long-term integrations or significant volume increases.

The Importance of Pool Selection

Liquidity mining remains one of the most promising strategies for driving growth, but its success heavily depends on selecting the right pools ([2.3], [4], [5]). Targeting pools with high market-wide trading volume but low protocol market share has shown potential, as has focusing on bootstrapping inactive pools. However, several challenges emerged:

- LP Awareness: Some LPs were unaware of the incentives or found them too small to justify action.

- Liquidity-Volume Disconnect: Increasing liquidity does not always result in proportional volume gains, undermining the assumption that market share of volume follows market share of liquidity.

- Market Volatility: Incentivizing assets during volatile periods complicated assessments of program impact.

Despite these hurdles, liquidity mining has proven effective for kickstarting activity in dormant pools and supporting protocols that enhance the LP experience. Future programs should focus on gradual reward reductions, optimized allocations, and tailored strategies for specific liquidity provisioning needs ([5]).

Flexibility and Iteration

A recurring theme across all successful programs is the need for flexibility and experimentation ([6], [10], [13], [17]). Incentive programs could be approached like paid marketing campaigns in Web2, requiring constant monitoring, iteration and data-driven adjustments. Shorter incentive periods often fail to generate sustained results, highlighting the importance of maintaining program duration flexibility to adapt to market conditions and user behavior.

Protocols that succeeded also emphasized the importance of effective marketing, frequent communication, and responsiveness to user feedback. These efforts helped ensure participants were aware of the incentives and understood how to engage with them optimally. Programs with insufficient marketing or overly complex structures often failed to gain traction, as seen in cases where LPs were unaware of available rewards or didn’t find the effort worth it.

Community and Ecosystem Engagement

Engaging the broader community and ecosystem amplifies the effectiveness of incentive programs. Community-driven mechanisms, such as point systems, can boost participation and foster loyalty ([6]). Incentives tied to new features or announcements have also proven impactful, drawing attention to innovations and bootstrapping new markets ([10]). Additionally, incentivizing composability and integrations fosters ecosystem growth, as seen with protocols leveraging end-use cases to drive adoption ([10]).

Protocols that formed partnerships during incentive programs, such as LTIPP, generally achieved better results ([17]). Protocols with differentiated products also outperformed, often reaching higher "steady states" after the program concluded ([14]). Furthermore, incentives can attract new builders and protocols to the ecosystem, as demonstrated by Kwenta and Curve Lending migrating to Arbitrum with onboarding incentives.

Incentivizing Revenue-Generating Behavior

Sustainable growth depends on aligning incentives with revenue-generating activities. Programs should avoid rewarding mercenary behaviors, such as sybils and wash trading, which unravel once incentives are withdrawn ([2], [5], [7], [10]). Ensuring that rewards are sybil-resistant and minimizing friction in incentive distribution mechanisms are critical. OpenBlock Labs’ analysis ([7]) highlighted the prevalence of sybil exploitation in some programs, underlining the need for better reward mechanisms.

Another key consideration is to avoid disrupting the natural equilibrium between supply and demand. Over-incentivizing one side of the market can lead to inefficiencies that self-correct once the program ends, rendering the resources spent suboptimal ([10]).

Application Process for Ecosystem Incentives

The application process itself can influence the success of ecosystem-wide incentive programs ([9], [14]). StableLab’s analysis of LTIPP revealed that changes like introducing an advisor role and a council system improved the quality of feedback while reducing community effort. However, smaller teams often find these processes overly complex, deterring participation and limiting the reach of the program. Simplifying application criteria could help attract a broader range of participants.

Simplicity and Clarity in Incentive Design

Overly complex incentive structures often hinder user engagement. Programs that require additional steps, such as purchasing vesting tokens, add friction and reduce participation ([10], [12], [15], [17]). Incentive criteria should be kept clear and simple, allowing users to easily understand how to engage. Protocols that streamlined reward mechanisms generally achieved better results.

Final Thoughts

This report aims to distill Blockworks Advisory’s extensive internal research on incentive programs and their analysis, providing a solid foundation for designing future programs while fostering the establishment of industry-wide standards. By promoting standardized evaluation methods, benchmarks, and robust monitoring frameworks, the goal is to enable unbiased, comparative assessments that drive maturity and innovation across the industry.

Incentive programs have shown varying levels of effectiveness in driving growth and engagement across DEXs. Well-designed incentives can trigger a self-sustaining flywheel effect, where liquidity attracts trading volume, and trading volume draws more liquidity, leading to long-term gains in TVL and market share even after incentives end. However, success depends heavily on precise pool selection, efficient resource allocation, and the ability to adapt to diminishing returns. Analyses of initiatives like Uniswap's liquidity mining and Arbitrum's STIP and LTIPP programs reveal the importance of improving price execution, engaging diverse user segments, and refining methodologies for better cost-efficiency and sustained impact.

An appropriate methodology plays a critical role in accurately analyzing and optimizing incentive programs. Effective methods account for market dynamics, normalize metrics to reflect true impact, and align performance measures with protocol goals. By balancing simplicity and complexity, methodologies can reduce bias and ensure actionable insights. Advanced techniques, such as Synthetic Control, highlight the importance of leveraging robust data to isolate program effects and evaluate causal impacts. Ultimately, thoughtful methodological design provides a foundation for identifying strengths, addressing inefficiencies, and driving long-term success in incentive programs.

Our analysis highlights that successful incentive programs require a balance of careful design, active management, and adaptability. Incentives are most effective when they target sustainable behaviors, such as improving price execution or bootstrapping underutilized pools, rather than mercenary activities like trade mining. Pool selection is critical, and programs benefit from dynamic, data-driven adjustments to maximize efficiency and returns. Flexibility in structure and duration, alongside robust community engagement, ensures better alignment with user needs and market conditions. However, the challenge of retaining user activity after incentives remains a key area for improvement. Ultimately, the most valuable takeaway is the importance of a continuous feedback loop—monitoring, analyzing, and iterating incentive strategies to foster long-term protocol growth.

Analyses Included

[1] Uniswap's liquidity mining on Optimism, June 2023, Gauntlet: https://gov.uniswap.org/t/uniswap-liquidity-mining-analysis/21416

[2] Uniswap Incentive Design Analysis, July 2023, Gauntlet: https://gov.uniswap.org/t/uniswap-incentive-design-analysis/21662

[2.1] Uniswap Incentive Design Analysis - Trade Mining, July 2023, Gauntlet: https://gov.uniswap.org/t/uniswap-incentive-design-analysis/21662

[2.2] Uniswap Incentive Design Analysis - Payment for Order Flow, July 2023, Gauntlet: https://gov.uniswap.org/t/uniswap-incentive-design-analysis/21662

[2.3] Uniswap Incentive Design Analysis - Liquidity Mining, July 2023, Gauntlet: https://gov.uniswap.org/t/uniswap-incentive-design-analysis/21662

[3] Uniswap Liquidity Mining Retro, August 2023, Gauntlet: https://gov.uniswap.org/t/uniswap-incentive-design-analysis/21662/8

[4] Uniswap Arbitrum Liquidity Mining Midpoint Retro, January 2024, Gauntlet: https://www.gauntlet.xyz/resources/uniswap-arbitrum-rewards-midpoint-retro

[5] Results and Analysis: Uniswap Arbitrum Liquidity Mining Program, July 2024, Gauntlet: https://www.gauntlet.xyz/resources/results-and-analysis-arbitrum-liquidity-mining-program

[6] JIP 2: Incentive Budget and Framework for Strategic Growth, May 2024, Gauntlet: https://forum.jito.network/t/jip-2-incentive-budget-and-framework-for-strategic-growth/294

[7] OpenBlock Labs STIP Efficacy + Sybil Analysis, February 2024, OpenBlock Labs: https://forum.arbitrum.foundation/t/openblock-labs-stip-efficacy-sybil-analysis-2-24/21441/1

[8] OpenBlock’s STIP Incentive Efficacy Analysis, May 2024, OpenBlock Labs: https://forum.arbitrum.foundation/t/openblocks-stip-incentive-efficacy-analysis/23687

[9] StableLab: Analyzing STIP’s Efficacy and LTIPP Comparison, June 2024, StableLab: https://forum.arbitrum.foundation/t/stablelab-analyzing-stip-s-efficacy-and-ltipp-comparison/24777

[10] Arbitrum STIP Risk Analysis | Insights & Key Findings, July 2024, Chaos Labs: https://chaoslabs.xyz/posts/arbitrum-stip-analysis-summary

[11] The Blur blitzkrieg, March 2023, Spindl: https://blog.spindl.xyz/p/the-blur-blitzkrieg#footnote-1-105093208

[12] STIP Retroactive Analysis – Perp DEX Volume, June 2024, Blockworks Advisory: https://forum.arbitrum.foundation/t/ardc-research-deliverables/23438/4

[13] STIP Retroactive Analysis – Spot DEX TVL, July 2024, Blockworks Advisory: https://forum.arbitrum.foundation/t/ardc-research-deliverables/23438/6

[14] STIP Analysis of Operations and Incentive Mechanisms, July 2024, Blockworks Advisory: https://forum.arbitrum.foundation/t/ardc-research-deliverables/23438/7

[15] STIP Retroactive Analysis – Yield Aggregators TVL, July 2024, Blockworks Advisory: https://forum.arbitrum.foundation/t/ardc-research-deliverables/23438/8

[16] STIP Retroactive Analysis – Sequencer Revenue, July 2024, Blockworks Advisory: https://forum.arbitrum.foundation/t/ardc-research-deliverables/23438/9

[17] LTIPP Analysis, October 2024, Blockworks Advisory: https://forum.arbitrum.foundation/t/ardc-research-deliverables/23438/14