This research report has been funded by Button Labs. By providing this disclosure, we aim to ensure that the research reported in this document is conducted with objectivity and transparency. Blockworks Research makes the following disclosures: 1) Research Funding: The research reported in this document has been funded by Button Labs. The sponsor may have input on the content of the report, but Blockworks Research maintains editorial control over the final report to retain data accuracy and objectivity. All published reports by Blockworks Research are reviewed by internal independent parties to prevent bias. 2) Researchers submit financial conflict of interest (FCOI) disclosures on a monthly basis that are reviewed by appropriate internal parties. Readers are advised to conduct their own independent research and seek advice of qualified financial advisor before making investment decisions.

Button: Productizing the Synthesis Stack

Key Takeaways

- The edge has moved from access to synthesis. Data that was once a sell-side moat is now just a subscription, and the sharpest, most timely analysis increasingly shows up on X before a bank's note clears compliance. The advantage no longer goes to whoever holds the data, but to whoever turns a flood of cheap inputs into a decision fastest.

- Selection is being paid again. Index concentration sits near record highs while breadth returns and dispersion runs well above average, the conditions under which stock picking has historically worked, and the marginal dollar is already rotating from passive back into active.

- AI makes traders faster, not autonomous. Live competitions and controlled benchmarks both show models lose money making trades; what they do well is read and synthesize, so the durable use is augmenting a human decider rather than replacing one.

- Button productizes the synthesis stack. Every serious trader already hand-stitches a workflow of Codex and Claude tabs, scripts, and feeds. Button turns that into one workspace, a coding agent that writes Python against the trader's own data, persistent strategies and watchlists, scheduled morning briefs and risk scans, and a real-time portfolio view, leaving the trader more time to make the most informed decisions.

- What you feed the agent matters as much as the agent. Frontier models are a commodity everyone shares. Button's edge is the knowledge graph: a layer capturing how each trader sees the market, the sources they trust and the connections they believe matter, fed in at runtime so the same question runs through the user's own view of the world rather than a generic one.

The Trader Comes Back

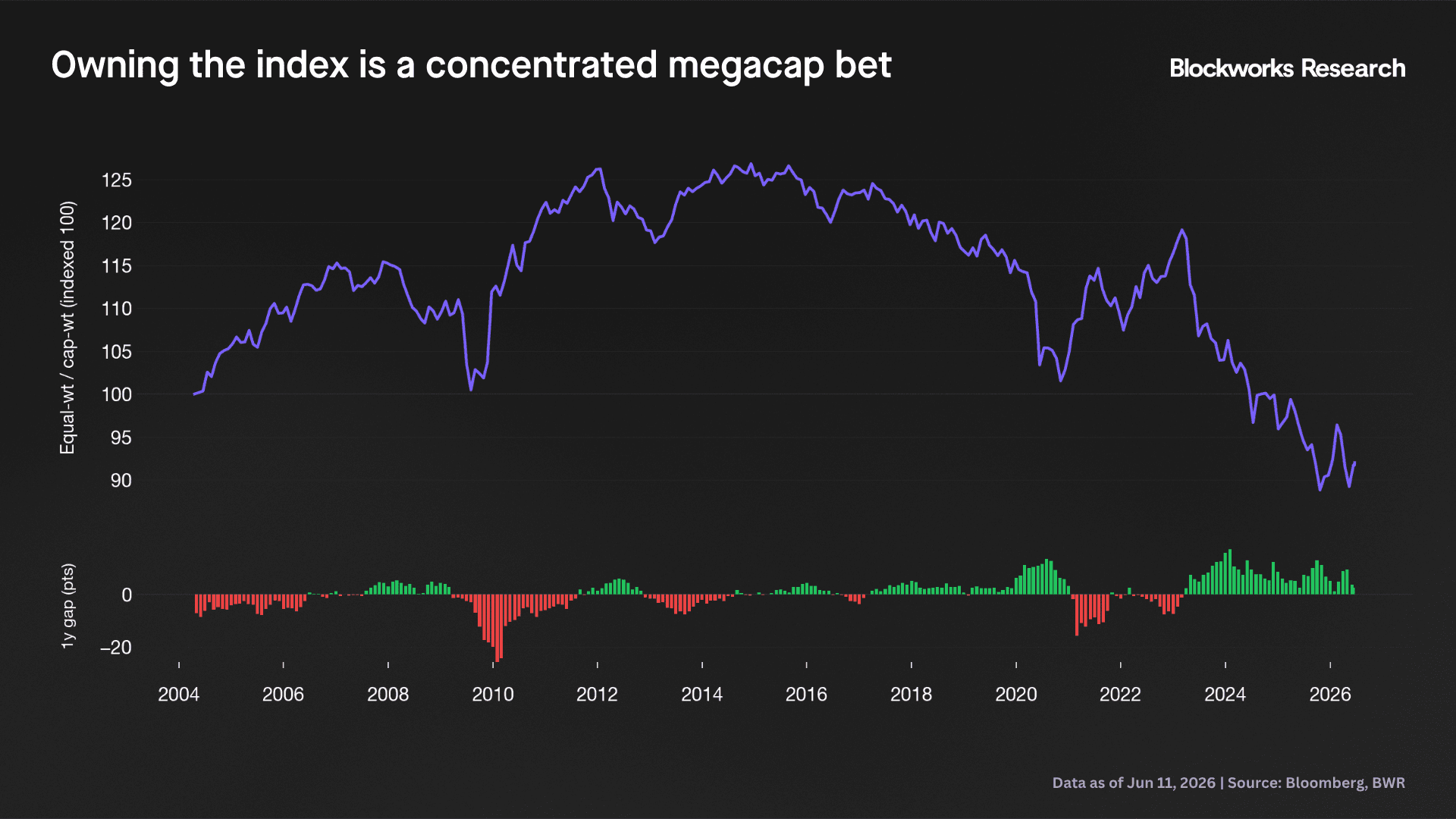

Buying the index is becoming a position in 10 stocks, not the diversification it advertises. The top names now sit around 40% of S&P 500 market cap, up from roughly 27% at the 2000 dot-com peak. And the supply pipeline points to more concentration rather than less: a generation of private giants led by SpaceX, OpenAI and Anthropic is headed for public listings at valuations that would land near the top of the index once eligible. Where past megacaps grew into their weight over years, the next generation arrives at full size.

The chart below tracks a dollar in the equal-weight S&P 500 against a dollar in the cap-weighted index: the average stock led for the first decade, then gave back the entire lead and kept falling. Each bar below is the gap between the two indexes’ trailing 12-month returns, and that gap has favored the megacap-weighted index every month since 2023, the longest unbroken stretch in the series.

That concentration inverts the logic of passive investing. When 2% of the constituents carry 40% of the weight, owning the index is an active wager on a handful of megacaps whether the holder means it or not. Security selection re-enters as the dominant variable, because the thing you are diversifying into is itself a directional position.

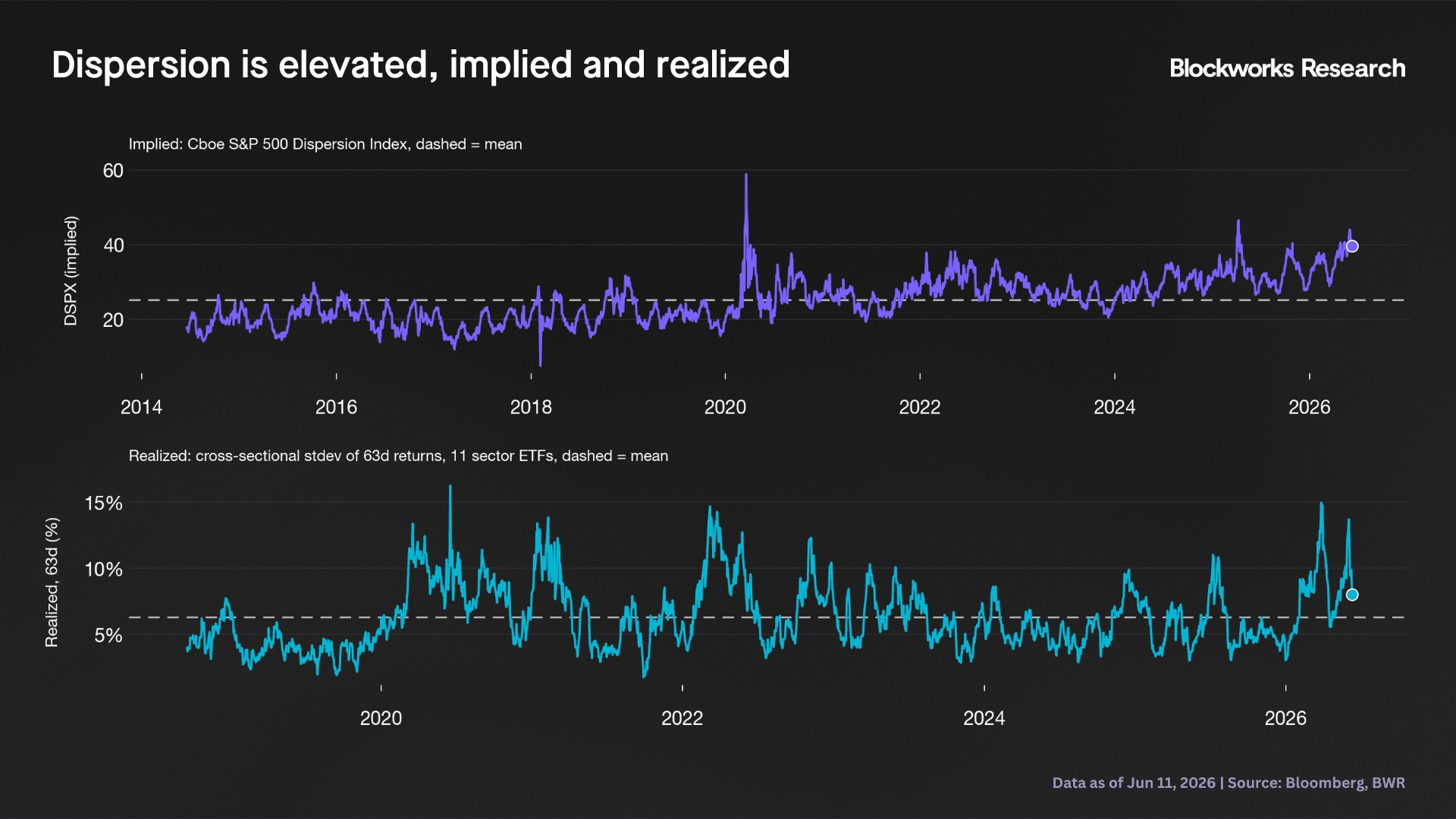

The chart below puts a number on that payoff: the top panel shows how big a gap between winners and losers options traders are pricing in for the month ahead, while the bottom shows the gap sectors have actually delivered. Both sit well above their long-run averages, meaning selection is being paid and the market expects it to keep being paid.

The odds of beating the index track concentration almost mechanically. Since 1960, roughly 30% of active funds beat the market in years when concentration was rising, against 47% when it was falling, because active portfolios sit closer to equal weight than their benchmark. Today sits on the favorable side of that split: concentration is at a peak and breadth is returning, with seven sectors beating the S&P 500 in early 2026 against three in all of 2025. That is the environment in which selection has historically paid.

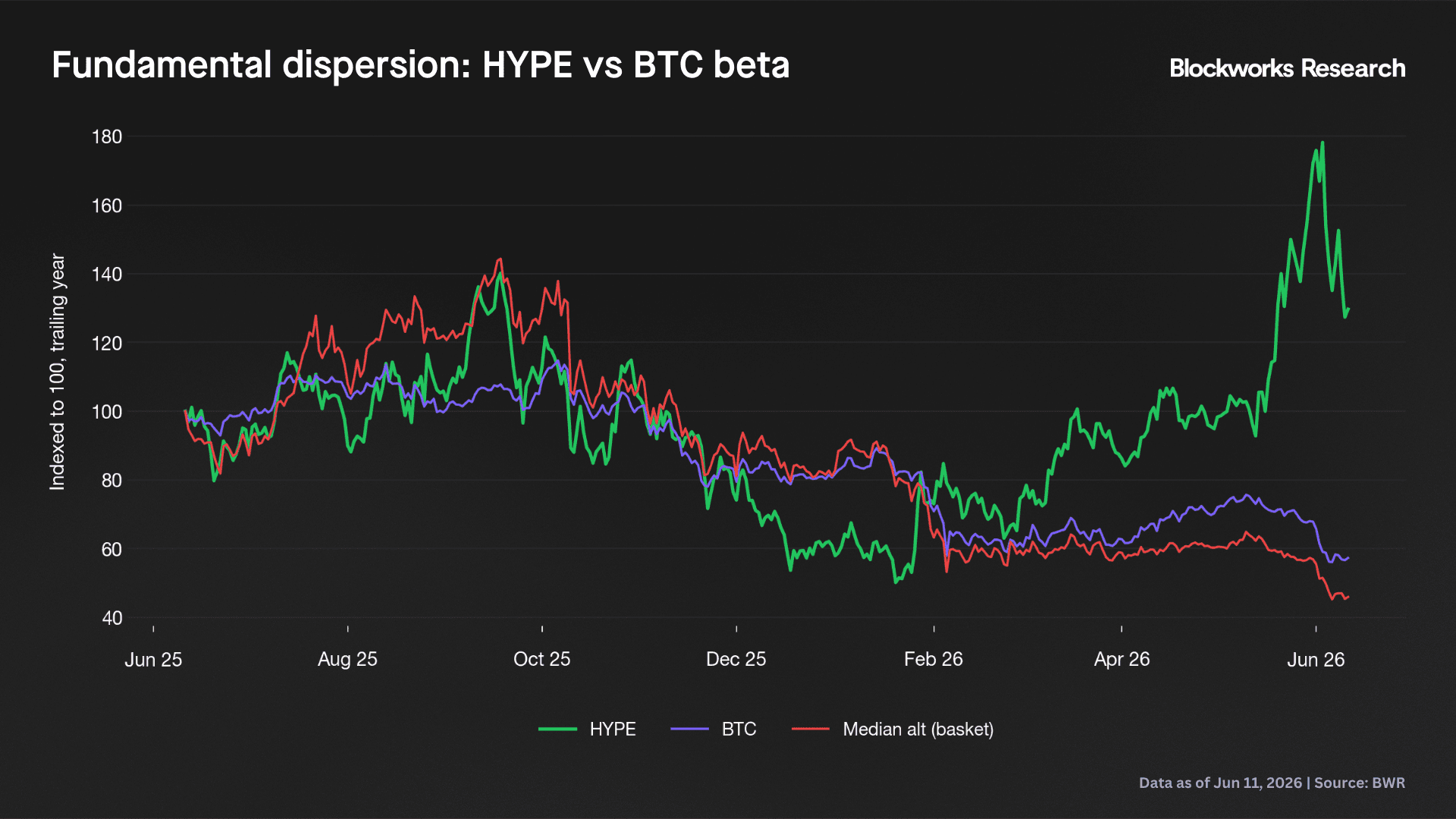

Crypto runs the same logic, just more cyclically. The 2024 to 2025 alt cycle produced enormous dispersion, but it was speculative and narrative-driven, and it collapsed as the market re-correlated: capital consolidated into bitcoin through mid-2025, with dominance peaking near 65%, and no broad alt season has followed. What is emerging instead is a more durable kind of dispersion. A handful of tokens with real cashflow, buybacks, and auditable financials are separating from a long tail that still trades as bitcoin beta.

HYPE is the clearest example. Hyperliquid is the dominant onchain perps venue, running around 60% of onchain derivatives open interest, and its revenue funds continuous buybacks of the token. The market has rewarded the model: HYPE is up over 100% in 2026 and entered the top 10 by market cap while bitcoin remains in drawdown.

The second shift is structural as the edge that used to come from privileged access has collapsed. Full price history for every US-listed security is a DataBento subscription away, the onchain record is open to anyone on Dune, and prediction-market feeds plug in for the cost of an API key.

The sell-side advantage of proprietary data and first look eroded with it. An independent researcher posting findings to X now moves information before a bank's note clears compliance, which leaves institutional research as the stale input more often than not.

AI compounds the collapse. What used to take a desk now takes one person. The datasets, traditional finance and onchain both, update continuously, and the analysis runs across them in real time.

I saw this firsthand. I spent years in sell-side research at a major investment bank, and toward the end the real edge increasingly came from X, where the work was often sharper and more timely than anything we produced in-house. Two structural drags explain why: banks restrict the AI models their analysts can use, and research clears compliance on a timeline that can run several days, by which point the alpha has already decayed.

When access is commoditized, the edge moves to synthesis: who can stitch the feeds together fastest and act on what they show. Both shifts point the same way. Dispersion gives a stock picker something to pick, cheap data gives everyone the same inputs, and what separates traders now is how quickly those inputs become a view. That is what makes a sharp discretionary trader valuable again, and the reason an AI-native trading interface has a market to serve.

Everyone Is Already Doing This

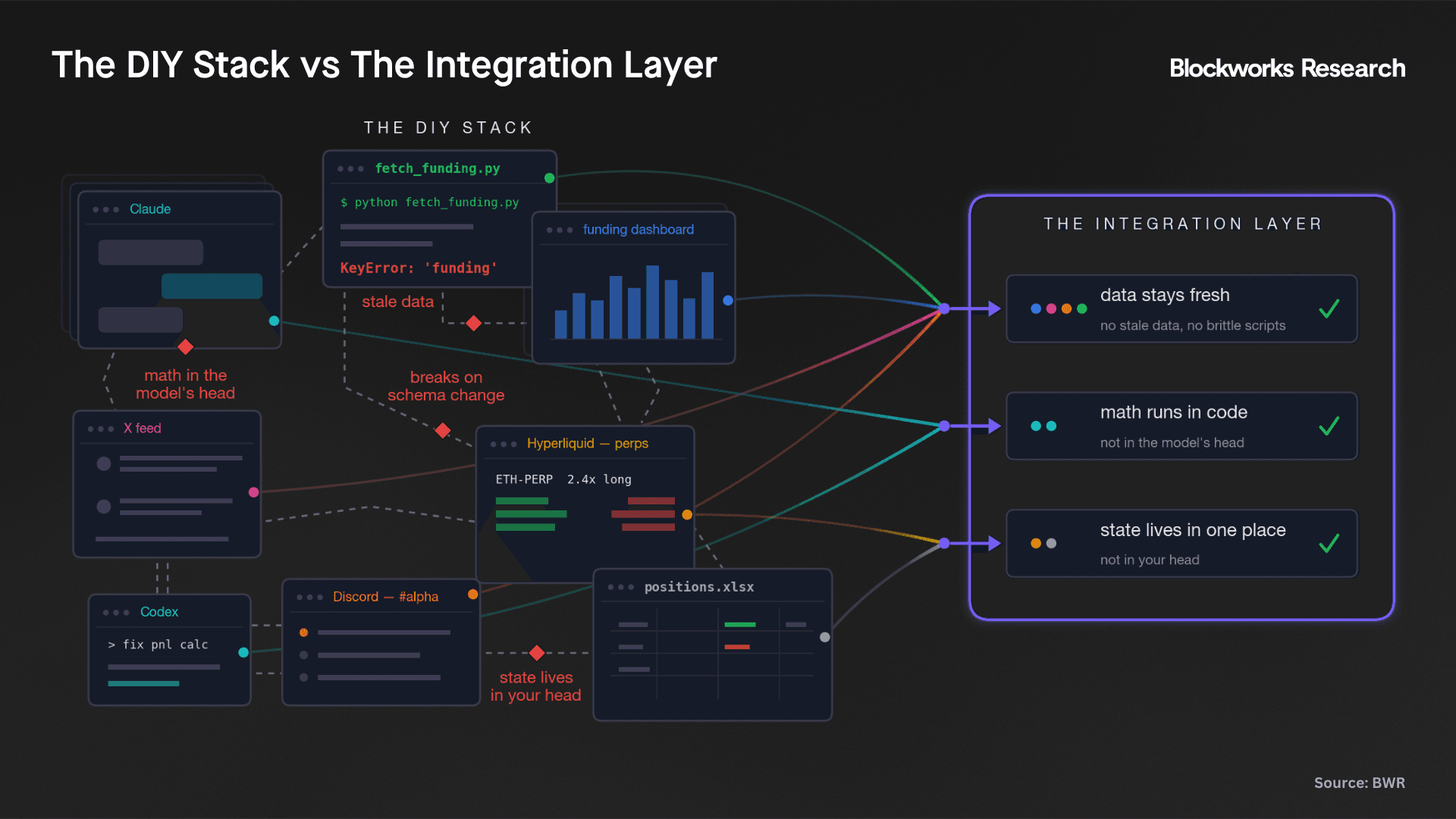

The workflow already exists; it is just messy, with every serious trader assembling their own pipeline by hand. That alone is the clearest sign the category is real.

The setup barely varies: a handful of Claude and Codex tabs, Python scripts piping in data, a couple of dashboards, an X feed open in the corner. What nobody has is a single place that pulls it all together, runs the right analysis, and spares them the stitching.

Button's user research bears this out. Across roughly 20 to 30 interviews weighted toward ex-institutional and crypto-native traders, the same behavior showed up at every level of sophistication:

- Crypto-natives want an agent that tracks smart wallets and decompiles unindexed contracts to work out what a new counterparty is actually doing.

- Traders want help making sense of their Discords and X feeds, turning scattered alpha into trades they can act on.

- And every interviewee, without exception, had wired AI into their workflow before anyone offered them a product.

And I am no exception. My version of the patchwork is a Python script piping in onchain and Hyperliquid data, Claude open to interrogate it, and X running alongside as the qualitative feed, all pieced together by hand before I can act. The hardest part is not pulling the data; it is keeping the state of everything straight: the wallets I follow, my own positions scattered across venues, and what has actually changed since I last looked.

The market still meets this demand in do-it-yourself mode. The guides that exist are build-it-yourself tutorials: spin up your own API keys, stand up a Claude or OpenAI framework, write your own strategy prompt, and monitor it yourself each week. The workaround proves the demand and exposes its cost. Every seam introduces errors: stale data, math done inside a model instead of in code, and brittle scripts that break on the next schema change. The opportunity is not inventing this workflow but productizing the one traders have already built for themselves.

The behavior is sticky because the building itself is the hook. The most addictive part of trading today is the vibe coding around it: wiring up your own data feeds, tweaking a backtest, getting a script to do exactly what you want. It is the same ownership and personalization that pulled people into DeFi in the first place, and it sets a hard bar for any product in the category. Hence, the winning product does not replace the tinkering, it gives it somewhere to live. That is the integration layer the DIY stack never had.

What Agentic Finance Actually Is

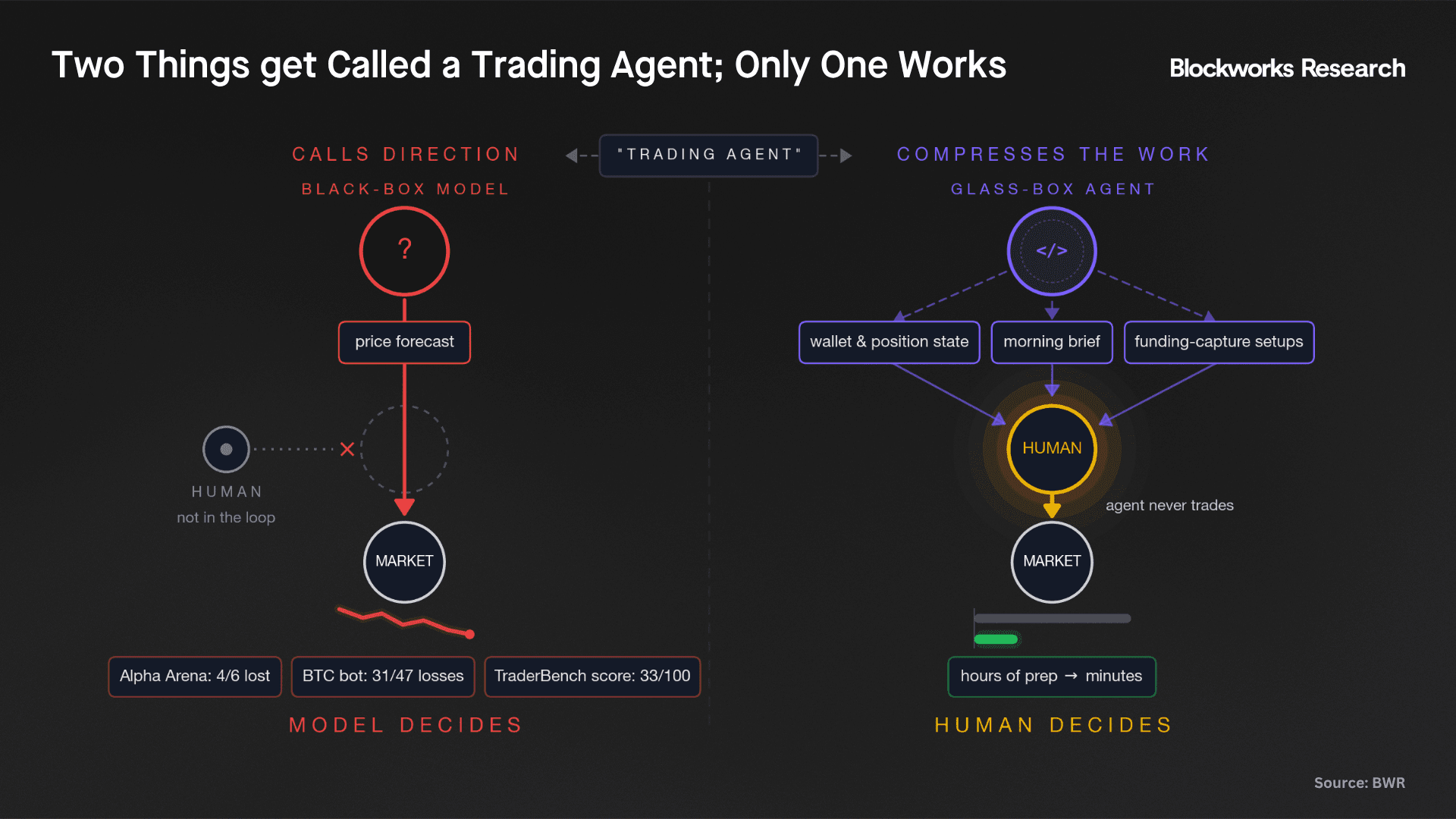

The durable use of AI in trading is synthesis and automation of mechanical work, not direction-calling. Two very different things get filed under "trading agent." One tries to forecast price and trade on it, the black box you throw money at. The other automates repeatable edges and compresses the manual work a discretionary trader already does. The first usually loses money. The second is where the value is.

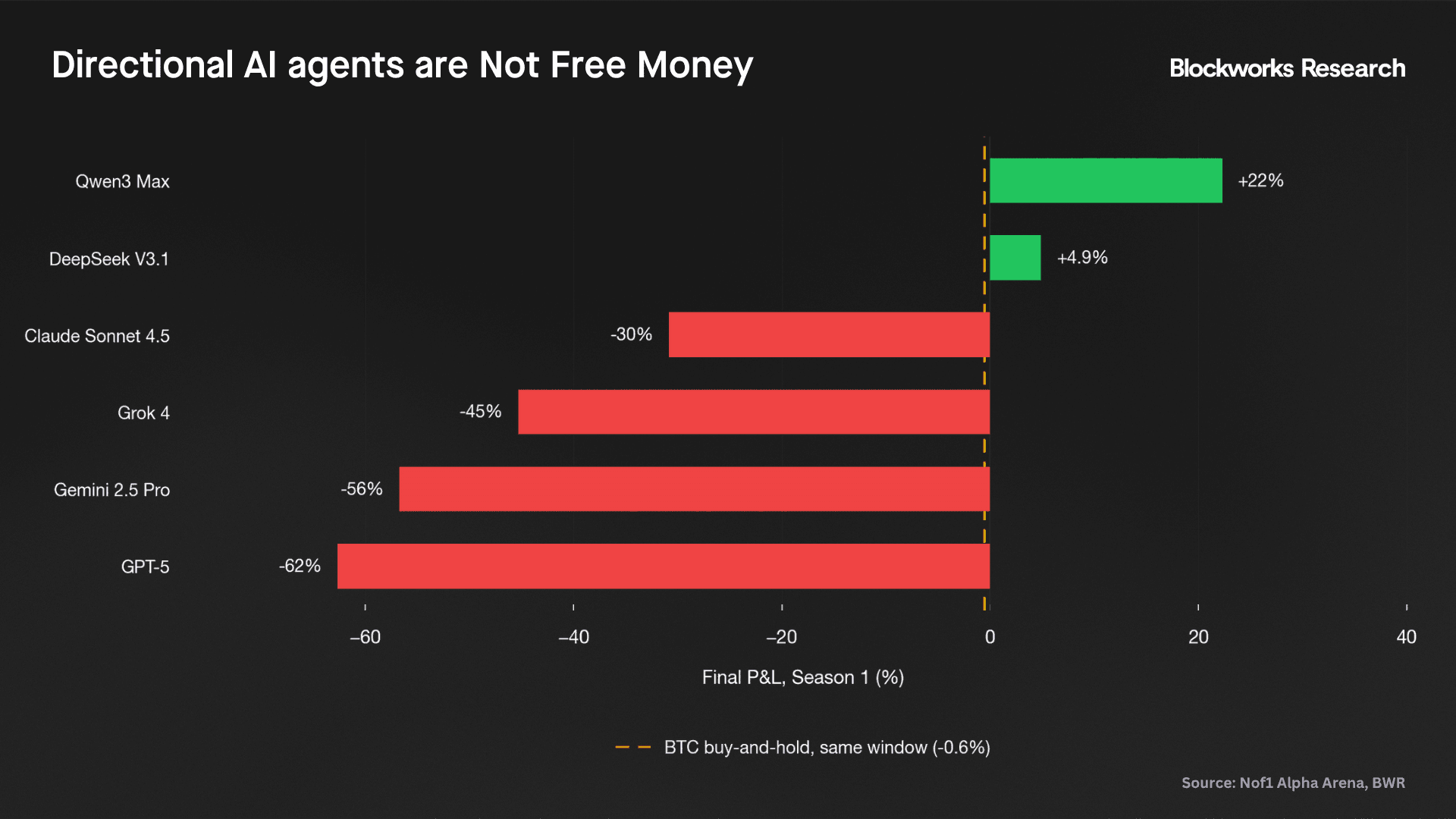

In Nof1's Alpha Arena (October to November 2025), six frontier LLMs were each given $10,000 to trade crypto perpetuals autonomously on Hyperliquid. Two finished positive: Qwen3-Max up roughly 22% and DeepSeek modestly green. The other four lost money, and the two worst, GPT-5 and Gemini, gave back well over half their capital. This was real money on a live exchange, and most of the models still lost. Hence, handing an AI the keys to the market is not free money.

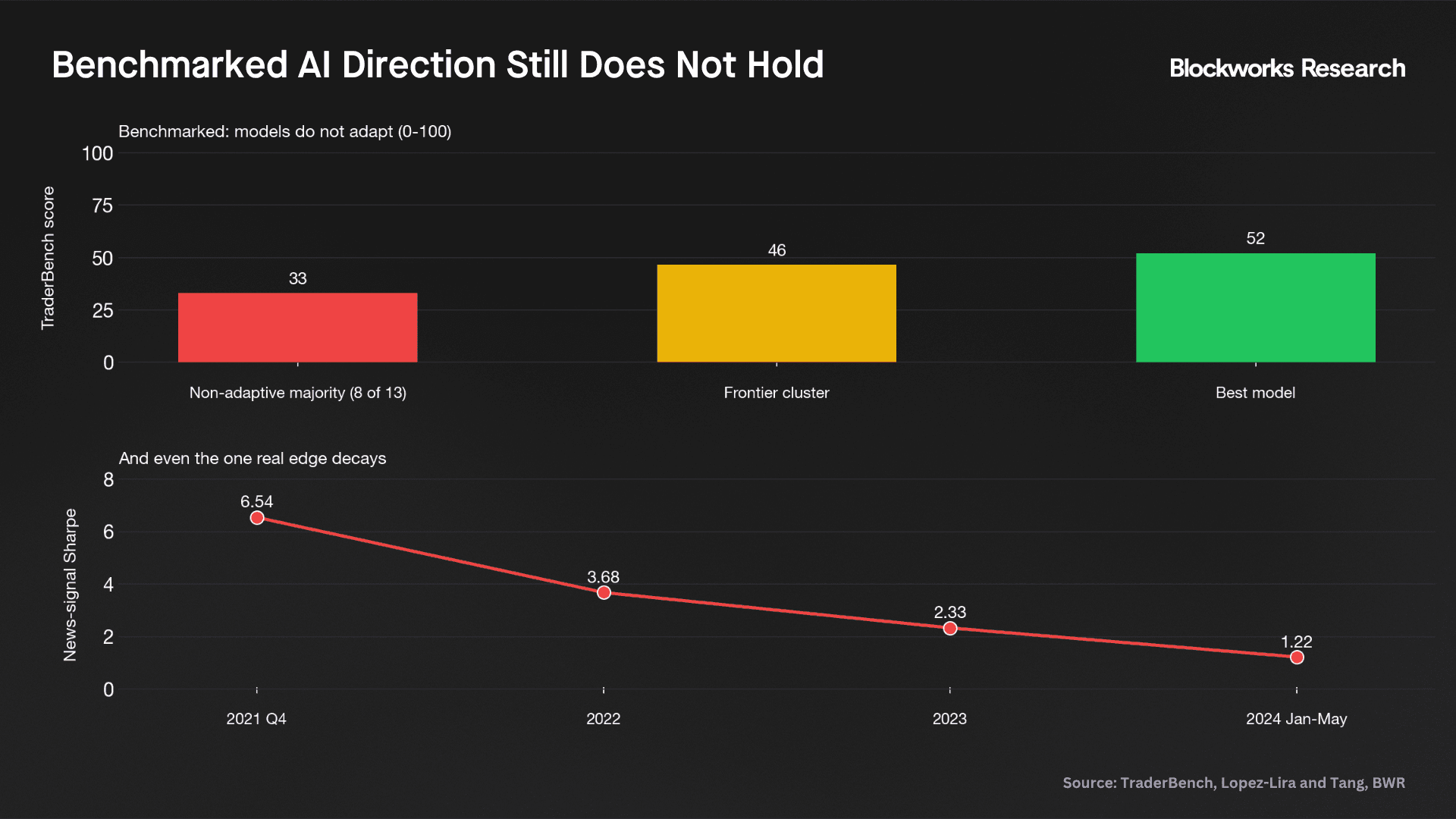

What Alpha Arena showed with real money, a controlled benchmark confirms in simulation. TraderBench ran 12 models through a simulated crypto market four times, from clean to deliberately manipulated, scoring 0 to 100. Seven of the 12 never left the do-nothing floor of 33, moving less than a point even when the market was gamed against them. And extended reasoning lifted one model's financial-knowledge score by 26 points but its trading by just 0.3. Hence, more thinking makes a model better at looking things up, not better at trading.

The one skill that survives all this testing is synthesis. In a well-known 2023 study, Lopez-Lira and Tang had GPT-4 grade news headlines as good or bad for a stock, and a fixed rule that traded every grade, long the good news, short the bad, made money across thousands of stocks: a Sharpe of 6.5 at its late-2021 peak, decaying to 1.2 by mid-2024 as the market matured (note all numbers are pre-trading costs). But the model never made a trading decision; it only read and graded the news. A pre-written rule did all the buying and selling, harvesting thousands of those slightly-right grades. Nothing in that says a model can pick a trade, size it, and manage it, and Alpha Arena shows what happens when one tries.

The defensible line is that agents process information well but bet on direction poorly.

The product landscape says the same. Autonomous bots are sold on dashboards and "risk-adjusted returns," yet on a venue where every account is publicly auditable, almost none publish a live P&L, win rate, or drawdown. A 2023 test cited on Button's blog shows why: an LLM bot trading BTC direction for 30 days finished 47 trades with 31 losses, the median loss 8% against a 2% median win, losing twice as often as it won and four times more when it did.

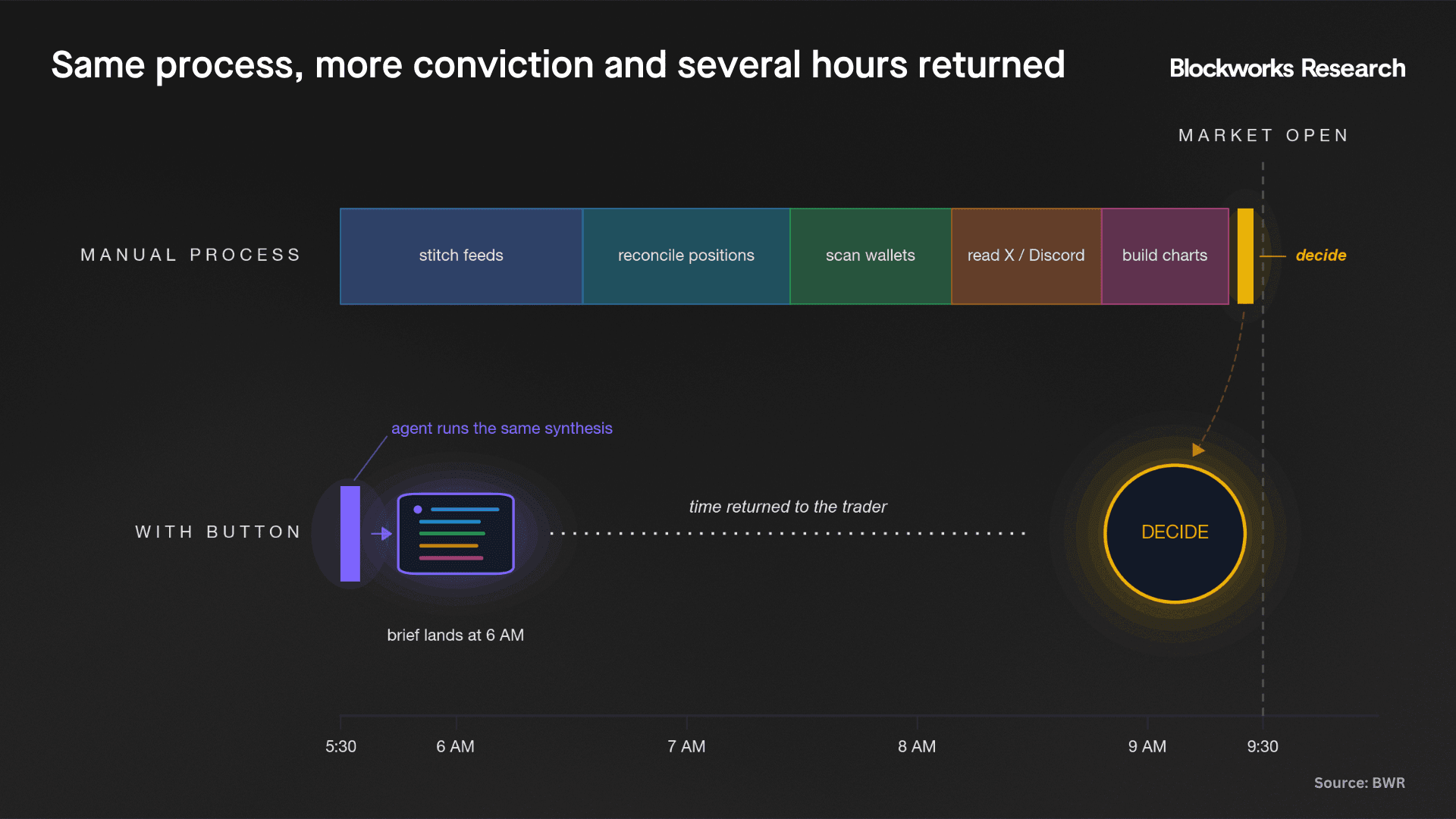

The durable use of AI in trading is synthesis: the four hours a trader burns every morning stitching feeds and reconciling positions become just minutes, done better, with the decision staying human. An agent does not make you a better bettor. It makes you a faster, better-informed decider.

Productizing the Paradigm

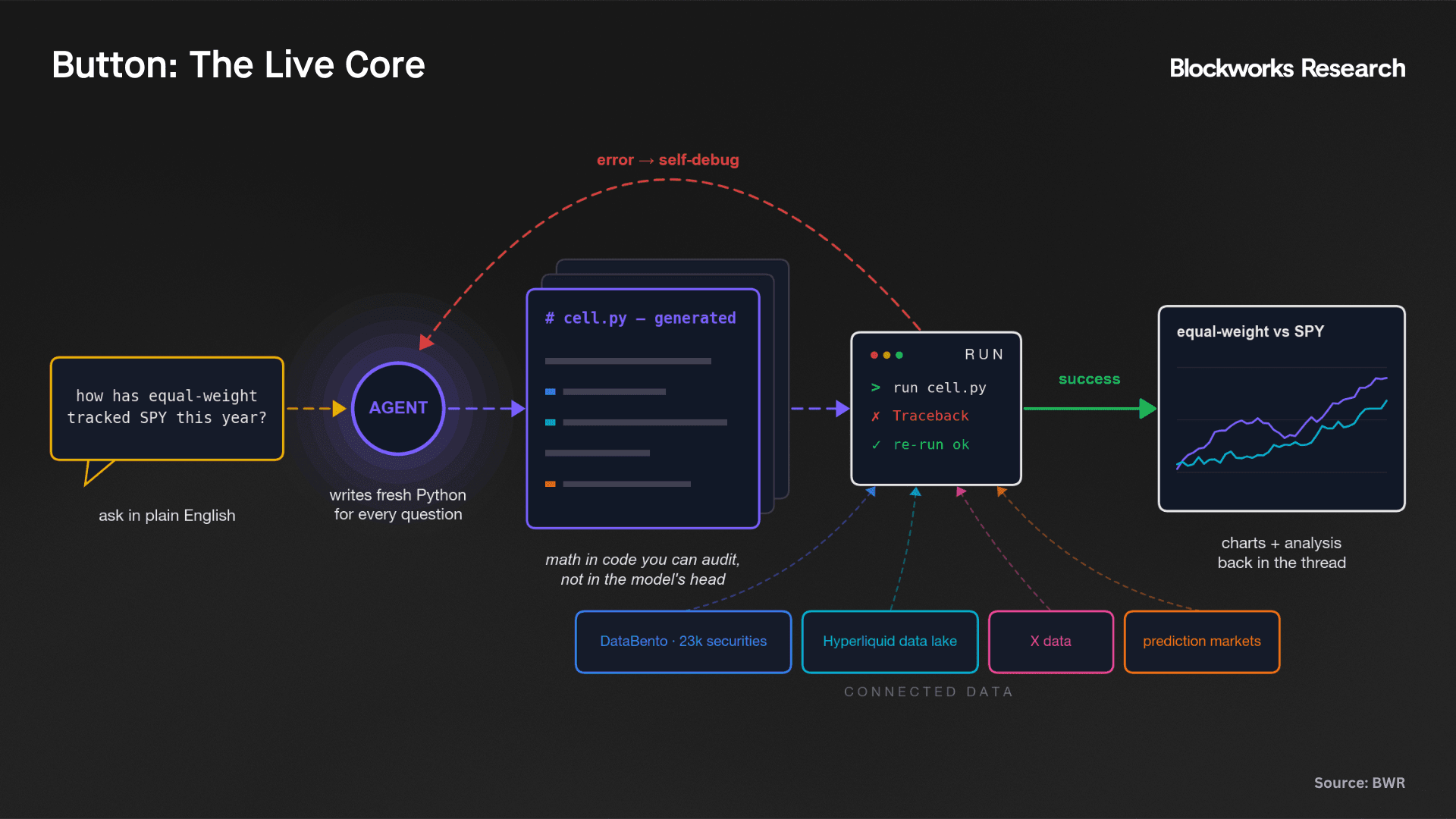

Button is building the integration layer as a workspace, not a bot: a coding harness that writes Python at runtime, sitting on connected data, with a forward-deployed team embedding alongside traders. It positions itself as the productization of the agentic stack.

The architecture has three primitives, in Button's framing: an agentic runtime, stored artifacts, and datasets. The bet is that an integrated workspace beats a black-box bot, because the value is in synthesis, not in an AI price signal.

The workflow is a chat thread backed by a code interpreter. A user asks a question or describes a trade idea in plain English, and the agent writes real Python, runs it, and returns the chart and the analysis. "Compare equal weight against SPY" produces a live comparison; "buy bitcoin on days it falls 5%" comes back as a built strategy, backtested across full market history, with variations on request. Connectors determine what the agent can see, an X feed, Hyperliquid, DataBento data, and now the user's own accounts, so the analysis runs on the data the trader actually wants.

Button's credibility on execution is not theoretical. The team has deep, hands-on expertise in data ingestion, regime detection, and trade execution, and that is what today's product is built on.

What is shipped today:

- The core workspace is live. The agent harness, the threads UI, and a connector page cover the full loop from question to analysis, with X, Hyperliquid, and DataBento among the sources a user can plug in.

- Market history runs deep. A DataBento integration surfaces around 23,000 securities, so a user can backtest a full-history Apple strategy even though Hyperliquid's Apple market is only months old.

- Hyperliquid is indexed. A data lake of the venue's historical data sits under the agent's backtests and analysis.

- Artifacts persist. Strategies, theses, and watchlists the agent builds are saved to the workspace and referred back to in later sessions, the primitive that turns ad hoc chat into a durable workflow.

- Work runs on a schedule. Automations regenerate briefs and scans on their own; the morning brief is a recurring artifact, not a one-off ask.

- And the surface keeps widening. Watchlists, traditional-finance assets, brokerage connections, and a real-time view of the user's onchain positions are now live.

The roadmap from here:

- The morning brief leaves the app. It already regenerates on a schedule inside Button; delivery to email before the open takes it to where a trader's day actually starts.

- More of the trader's stack plugs in. Button frames itself as a neutral aggregation layer, so the sources a user already relies on, Dune, DefiLlama, prediction-market data, get wired into the agent.

- The knowledge graph is the deepest build, the layer that will teach the agent how the trader sees the market (more on it below).

- Execution through the agent comes last. Wiring the agent to place orders follows once it has proven it can find ideas worth placing.

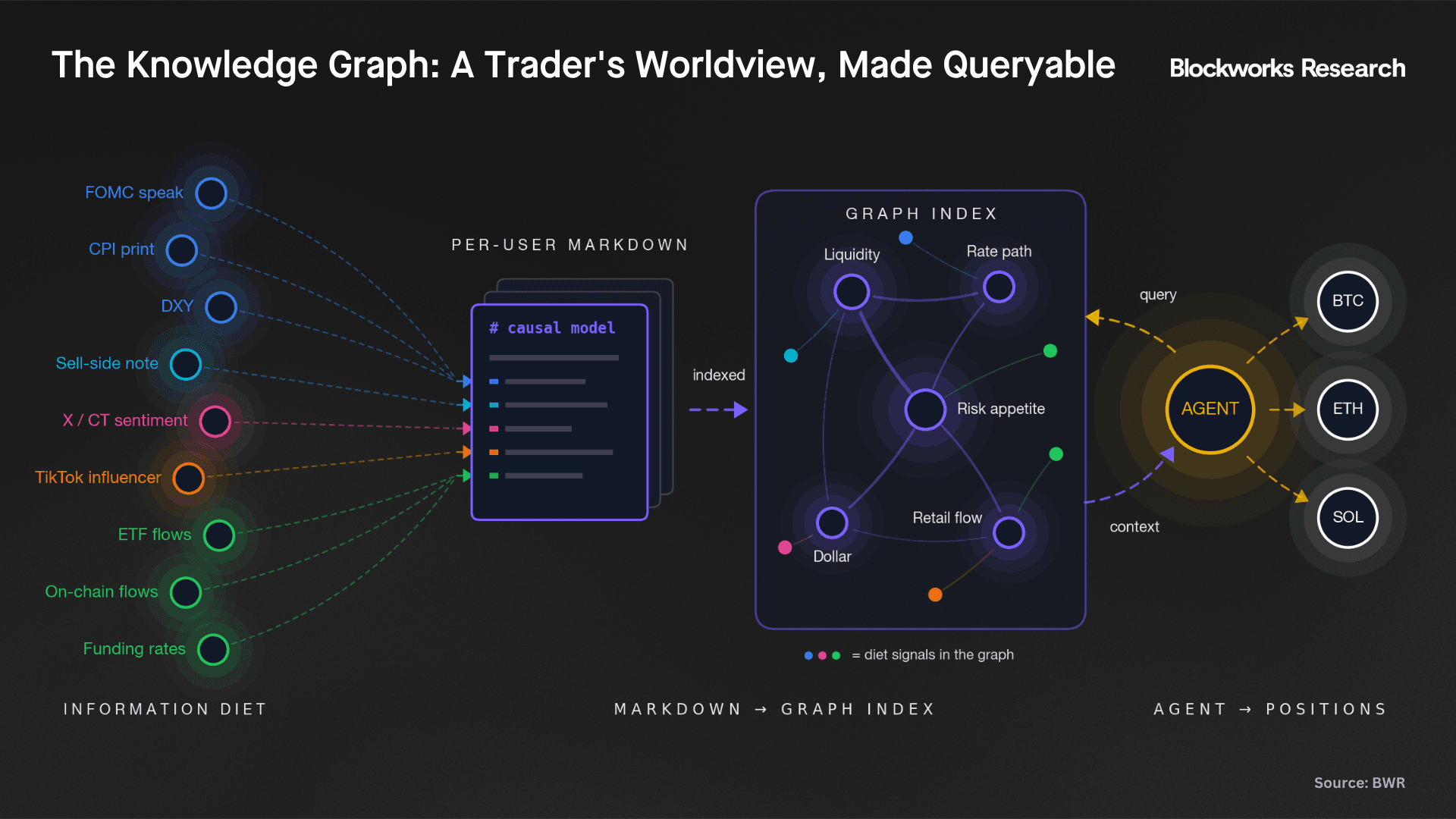

The most differentiated piece is the knowledge graph. A trading agent is only as good as what it knows, and the knowledge graph is where a trader's context lives: the qualitative influences that move a book but never surface in a price feed, from a sell-side research piece to the handful of X accounts worth trusting. Connectors carry the data; the graph encodes what the trader believes drives what, and the agent queries it at runtime, so two users with identical feeds get different answers, each grounded in their own information diet rather than the model's generic priors.

Mechanically, each user gets a set of markdown files encoding a causal model of how they think the world fits together, indexed behind the scenes into graph databases for fast runtime lookup. It is the sharpest bet in the product: the edge is not the model, it is what gets fed into it. Garbage in, garbage out, and the knowledge graph is how the trader controls what goes in.

The edge is still the trader's view; the agent just digests the world faster, and the knowledge graph makes sure it is digesting the trader's world.

The Traders Already Using It

The honest measure of agentic finance is not P&L from a bot. It is whether the tool makes a good trader meaningfully better. Button's first goal is deliberately mundane: deliver the best morning brief ever. Not a black box, but the daily synthesis ritual compressed into something that arrives before the open.

Button’s early power users describe it not as a replacement for judgment, but as a research layer that sharpens the judgment of already sophisticated traders:

“I’ve tried a lot of finance tools and most of them just dump data on you and call it a day. Button is different. Tailor does my research every morning before I'm even thinking about it, then hands me real trade opportunities, not a wall of charts to decode. Everything lives in one place, so I'm not juggling through different platforms or piecing things together. I open it, see what matters, and make my call. It actually saves me time, which is more than I can say for most of what's out there.” Jason Waters, sophisticated day trader

"I heavily rely on Button's Threads feature as a sophisticated sounding board to validate my investment theses and analyze complex market setups. The AI-driven insights provide high-quality analysis that helps me form a solid investment foundation, effectively bridging the gap between deep market research and execution. It essentially serves as an intelligent research partner, allowing me to stress-test ideas before translating them into active market positions." Ali Bajwa, former VP at Jefferies Group

“I'm using the Button harness for different pockets of assets. I have one for robotics. One for entertainment, and one for ancillary AI calls. I plan on patching Button into my trading agent once it can connect Coinbase agent and Robinhood agent. I want a trading agent that can help me see the calls I've missed and why without missing out on money in the process.” Jonah Blake, LiveFrame

Video example: https://x.com/JonahBlake/status/2064716880116388195?s=20

There is a second-order bet underneath all of this. Button's wager is that AI gives sophisticated traders their time back, and that the population able to trade discretionarily grows as the cost of synthesis falls. If that holds, the addressable market expands rather than merely consolidating, a more durable foundation than competing for a fixed pool of existing traders.

The pessimism around agentic finance is aimed at the wrong target. The fear is an autonomous bot that replaces the trader, yet the evidence so far runs the other way. The version that works is more realistic: an interface that lets a sharp discretionary trader synthesize faster and act with more conviction.

So when owning the index is a concentrated bet and the edge is synthesis rather than access, the scarce skill is now turning a flood of cheap data into a decision. Agentic finance does not make the decision. It makes the decider faster and better informed. That is the market Button is building for, and on the current evidence, it is the right one.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.