Aave: Cracks in the Monolithic Thesis

Luke Leasure, Shaunda Devens and 1 others

Key Takeaways

-

The Kelp-Aave situation: On April 18, 2026, attackers exploited a vulnerability in KelpDAO’s LayerZero bridge to mint 116.5k unbacked rsETH on Ethereum, which was then posted as collateral on Aave V3 to borrow roughly $193M in ETH-correlated liquidity.

-

Hidden leverage in Aave’s looping trade: With 98.5% of WETH-borrow collateral ($5.43B of $5.52B) sourced from ETH LSTs, WETH lenders sat as the de facto third loss-bearing tranche. In the four days following the exploit, Aave experienced a bank run, with over 30% of its deposit base withdrawn.

-

Umbrella as the backstop: Resolution of the liabilities across Kelp, LayerZero, and Aave has yet to be finalized, and external or bespoke financing solutions may come into play. Aave faces $124M-$230M in bad debt depending on this resolution, with the $54M in Umbrella WETH facing the prospect of total loss of principal. Beyond this, WETH lenders and the Aave treasury may take a material haircut.

-

The monolithic vs. modular debate: The Kelp exploit exposed structural risks in monolithic lending pools, where unified liquidity can socialize losses across depositors and underprice risk for certain collateral. Modular lending offers a meaningful architectural improvement by isolating risk across markets and enabling specialized underwriting, though more vertically integrated “CeDeFi” models may also gain share by combining end-to-end underwriting, distribution, and legal enforceability.

-

Market share implications: Aave’s sharp loss in deposits may mark the first meaningful crack in its liquidity moat. If depositors increasingly view risk isolation as a feature worth paying for, recent events could accelerate a structural shift in where capital chooses to reside. That said, SparkLend’s inflows suggest capital is rewarding perceived risk management quality, not simply rotating toward one lending architecture.

Introduction

On April 18, 2026, attackers attributed to the Lazarus Group minted 116.5k unbacked rsETH by poisoning the downstream RPC infrastructure of LayerZero Labs’ Decentralized Verifier Network. KelpDAO’s bridge relied on a 1-of-1 DVN setup, making LayerZero Labs’ verifier the sole attester for cross-chain transactions; Kelp has stated this was the documented default for OFT deployments, while LayerZero maintains it explicitly recommended a hardened multi-DVN configuration.

The attackers compromised two independent RPC nodes, replaced their binaries with malicious versions that served forged data exclusively to the DVN while continuing to report accurate data to all other services, and DDoS’d the remaining nodes to force failover onto the poisoned infrastructure. With no independent verifier to cross-check the attestation, the DVN confirmed a forged message that rsETH had been burned on an L2, enabling the attacker to mint unbacked tokens directly on Ethereum mainnet.

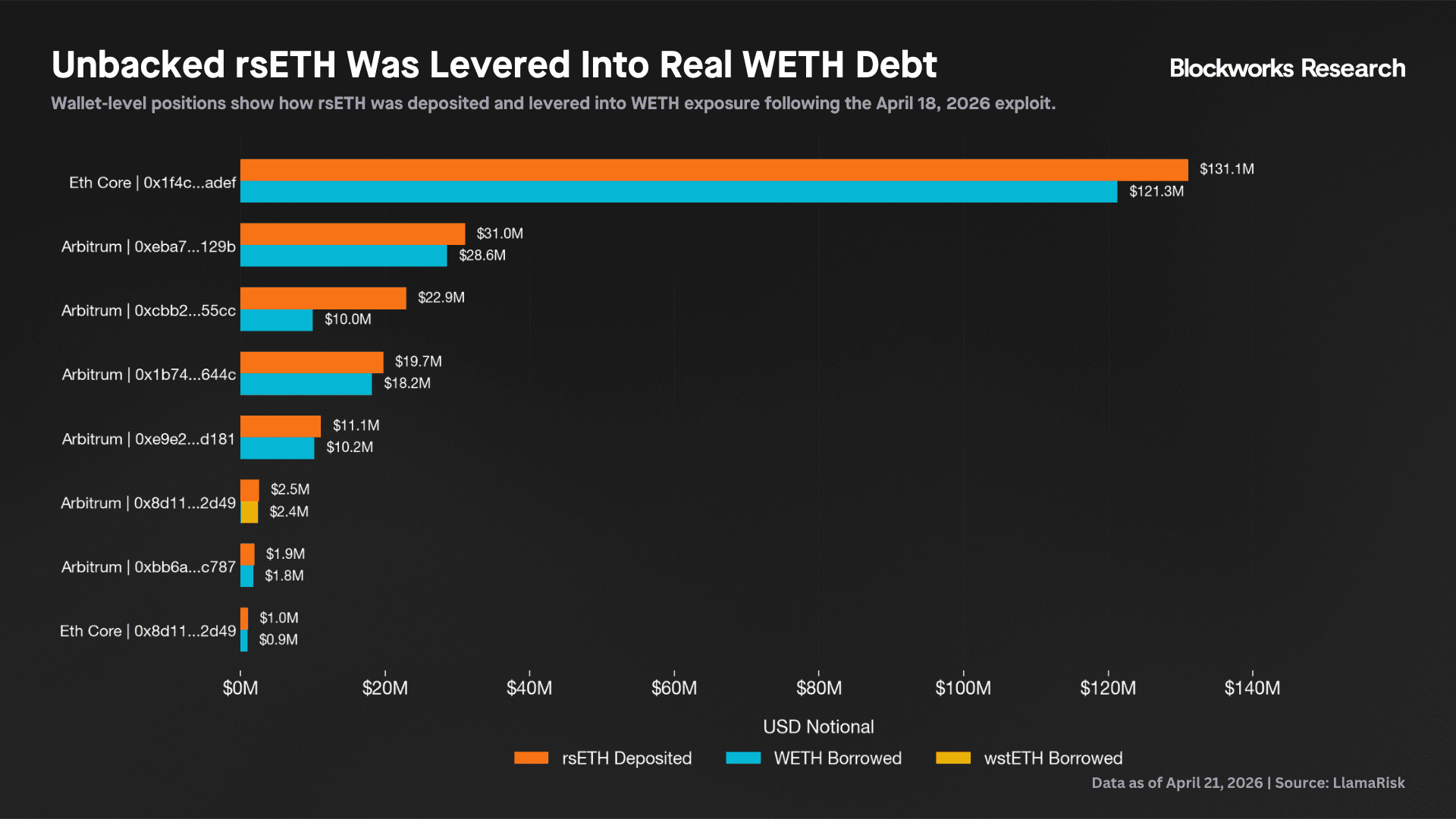

The attacker then split the proceeds across multiple branch addresses within minutes and deposited the bulk of the minted supply into Aave V3 as collateral. By exploiting Aave V3’s E-Mode framework, the attacker was able to borrow WETH at a 93% loan-to-value ratio against rsETH, and left the protocol with approximately $193M in ETH-correlated liquidity.

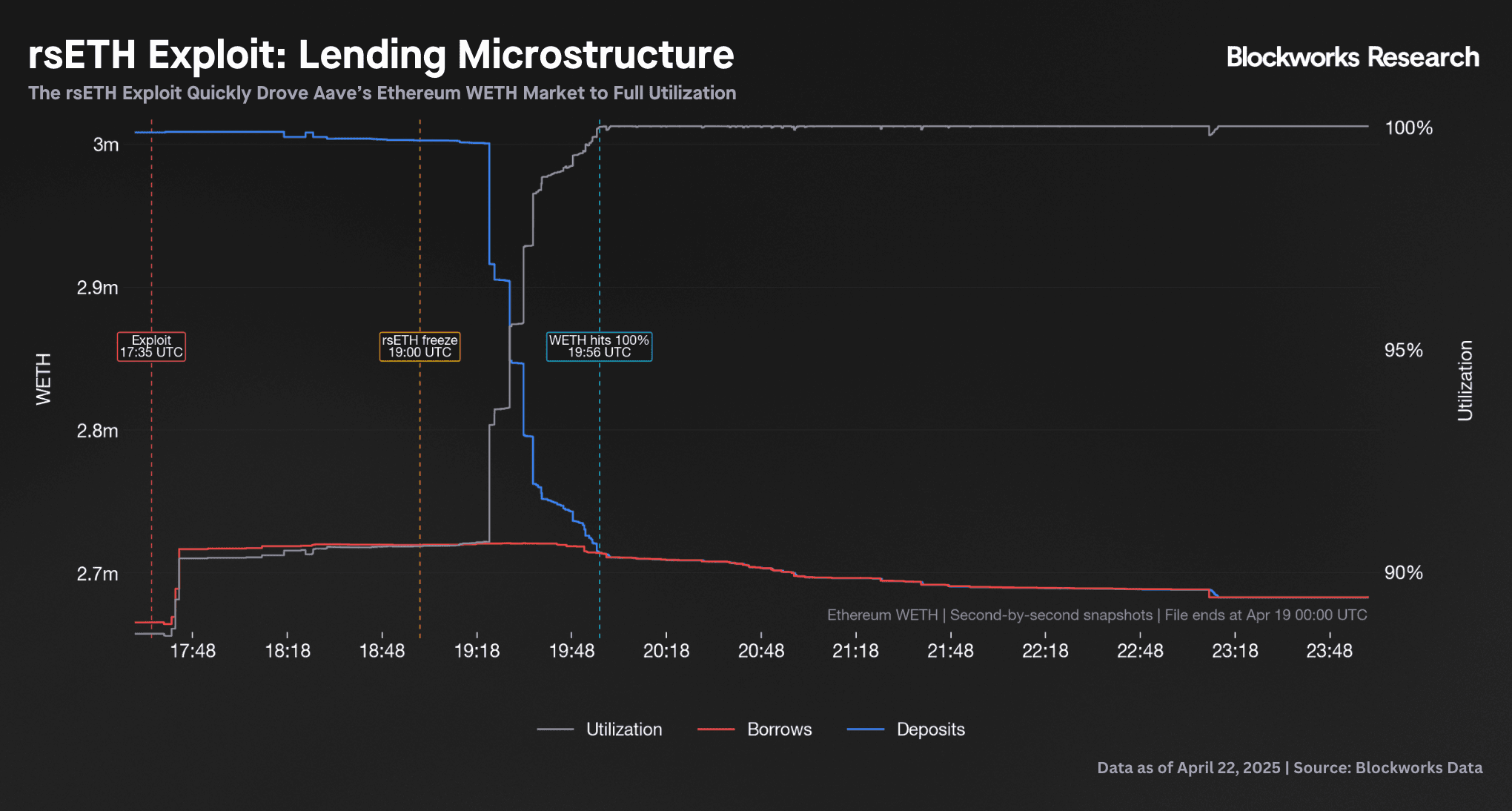

The chart below shows the market microstructure of the event. After the exploit at 17:35 UTC, the attacker borrowed WETH against unbacked rsETH, immediately tightening liquidity in Aave’s Ethereum WETH reserve. As news of the exploit and potential bad debt spread, other users began pulling liquidity as well. From 17:35 UTC to 19:56 UTC, WETH deposits fell by 294k WETH, pushing the market to 100% utilization, leaving no immediately available WETH liquidity in the pool.

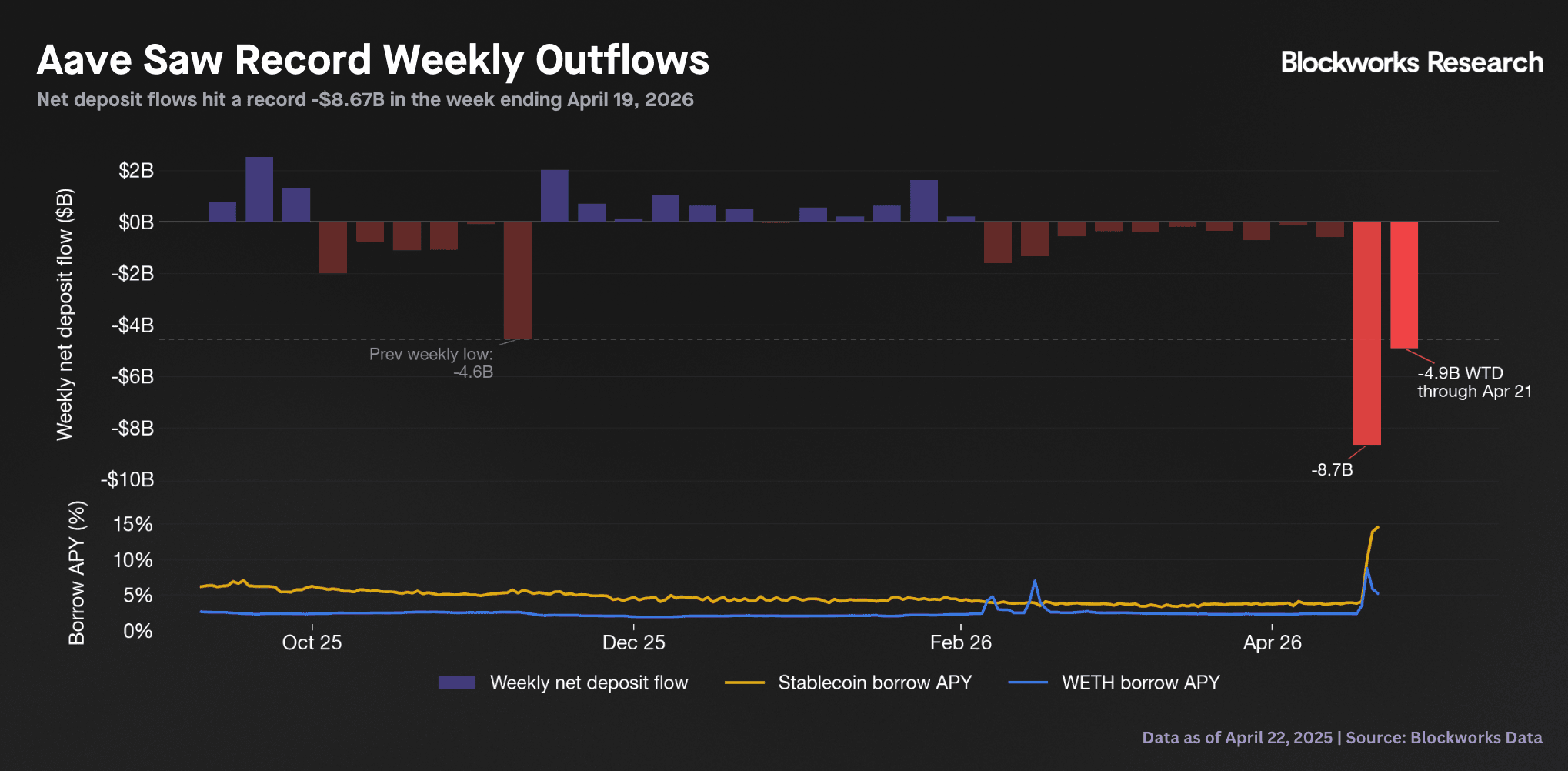

As reserve conditions tightened and users rushed to protect capital, protocol-wide flows deteriorated sharply, culminating in Aave's worst weekly outflow on record at -$8.67B. By April 20, major funding markets were effectively maxed out, with USDC, DAI, USDT, USDe, and WETH all pinned at 100% utilization.

With liquidity scarce, borrow rates rose sharply across key assets. But absent clarity on the recovery plan and how losses will be handled, Aave markets are now stuck in a standstill, with borrowers, depositors, and prospective lenders all waiting for greater certainty before re-engaging.

The Hidden Leverage in Aave’s Looping Trade

Before looking into the recovery plan, we believe this is an excellent example of the risks of Aave's looping strategies. For reference, we previously outlined the strategy via sUSDe looping and how it enables almost "risk-free” (relative to holding the underlying asset without looping) returns. The process works as follows:

- Loopers deposit high-yield-bearing assets (e.g., rsETH) on Aave.

- Loopers use E-Mode to borrow related assets (ETH) against rsETH and earn the difference between the staking yield and the borrow cost.

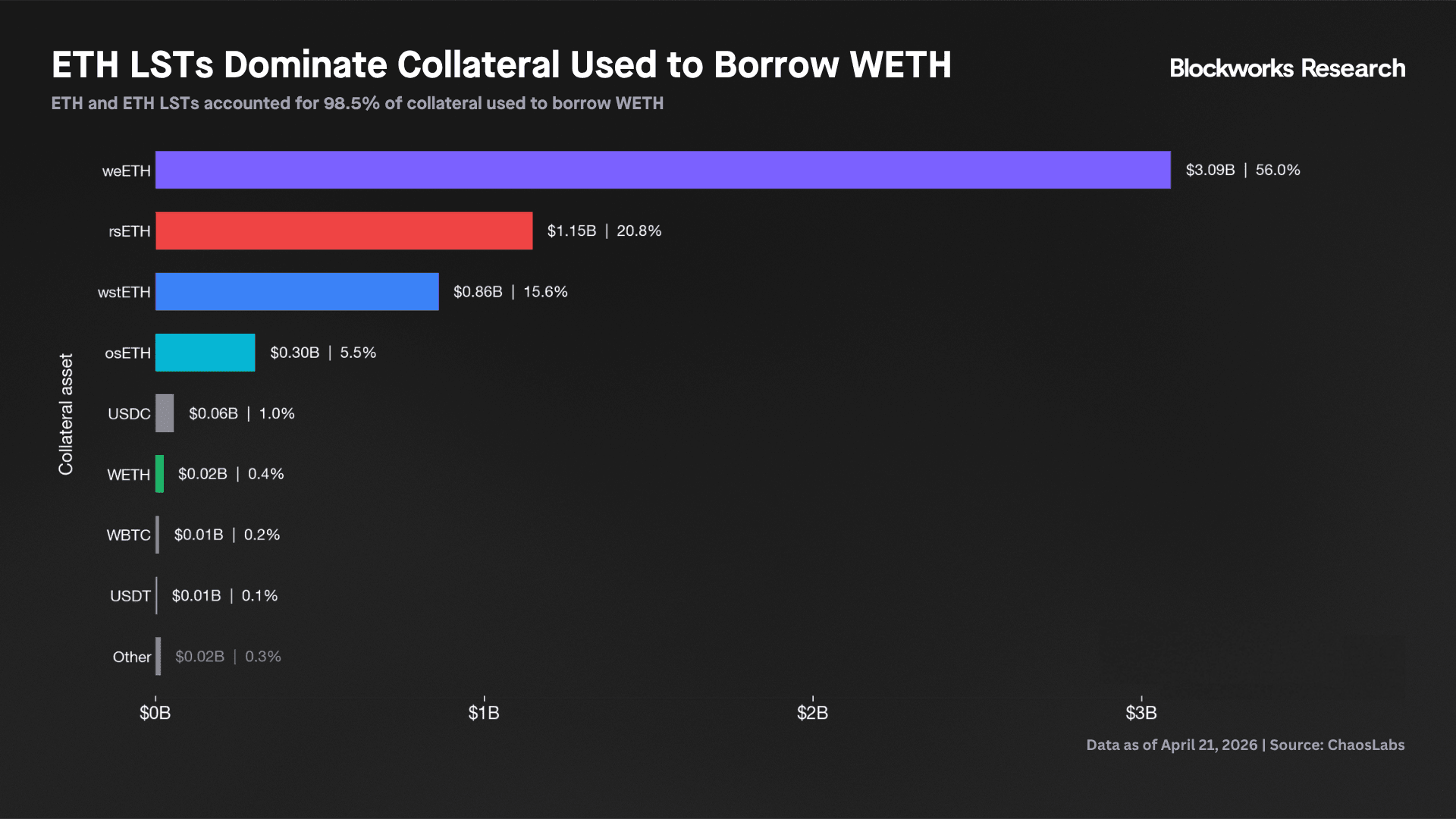

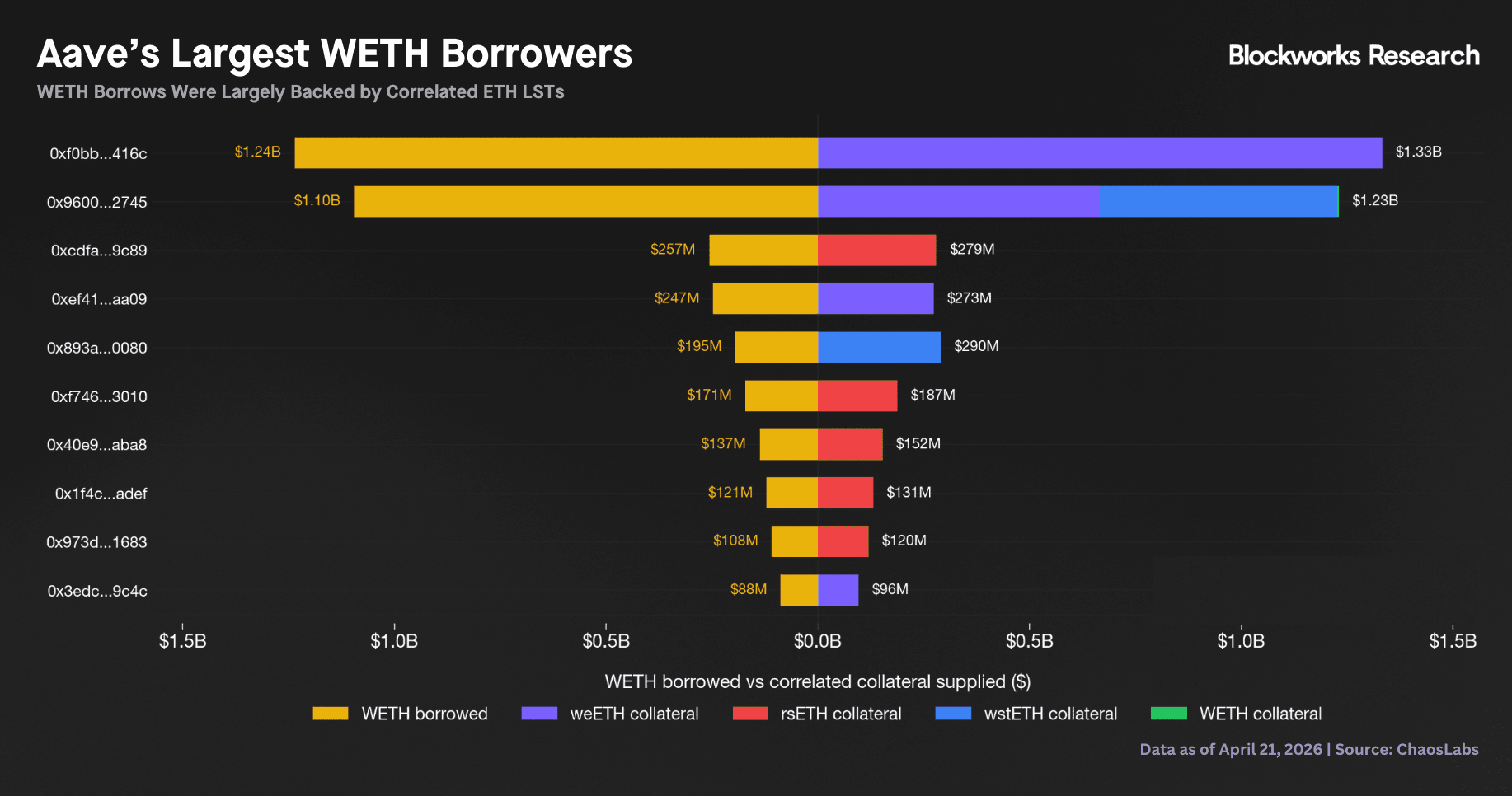

To highlight how prevalent this type of borrowing has become, we plot the collateral used to borrow WETH. On Aave, 98.5% of collateral backing WETH borrows came from ETH LSTs, totaling roughly $5.43B of the $5.52B collateral.

Going deeper into individual wallets, tracking the largest borrowers of WETH we find that all of the top 10 accounts (accounting for $3.65B of WETH debt, or 65.4% of total borrows) were using that borrowed WETH to lever into higher-yielding ETH LSTs such as weETH, rsETH, and wstETH.

In theory, the relationship is symbiotic. Loopers access deep ETH liquidity to lever their carry trade, while ETH depositors benefit from the higher utilization this demand creates, with ETH supply APR elevated to 1.66% compared to a near-zero baseline for assets without this mechanic, such as WBTC at 0.01% APR.

In practice, however, the loss waterfall embedded in this trade is very different from what Aave’s pooled lending model suggests. With 98.5% of collateral backing WETH borrows sourced from ETH LSTs, Aave’s ETH reserve was not funding a diversified borrowing book. It was primarily funding levered LST carry.

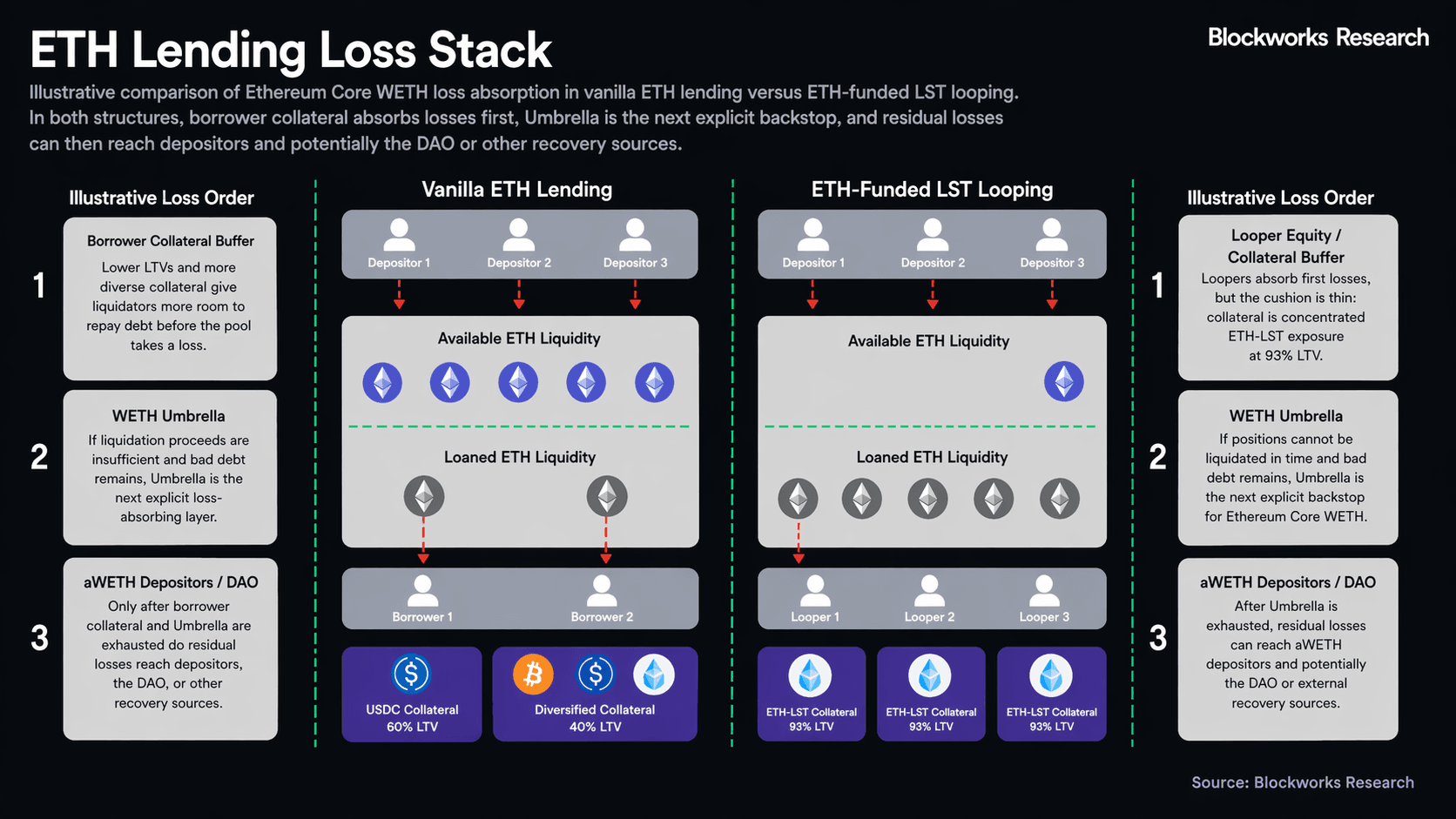

The first loss sits with the looper through the equity cushion in the overcollateralized position. If that cushion is exhausted and the position turns into bad debt, the next explicit loss-bearing layer is WETH Umbrella, which serves as Aave’s junior backstop. Only after Umbrella is depleted do residual losses reach aWETH depositors and, potentially, the DAO balance sheet or other recovery sources. In economic terms, ETH lenders are therefore not senior secured lenders to a broad pool of borrowers. They occupy a de facto third-loss position in a concentrated LST funding structure.

In traditional structured finance, that subordination would be disclosed explicitly and compensated accordingly. On Aave, by contrast, all ETH suppliers earn the same pool rate regardless of whether their ETH finances plain-vanilla borrowing or highly levered rsETH loops. The pooled architecture therefore compresses materially different risk profiles into a single APR, leaving ETH depositors undercompensated for the tail risk they are effectively underwriting.

The rsETH exploit made that structure visible. ETH depositors were impaired despite having no direct exposure to rsETH because their ETH had been lent against rsETH collateral at aggressive LTVs. That is the core weakness embedded in Aave’s pooled model. While modular lending is often criticized for enabling highly levered and potentially unsafe strategies, this is one of the areas where modularity offers a cleaner solution, as lenders can choose which collateral types they are willing to fund and demand compensation accordingly. That is also why Aave supported materially more looping than Morpho. On Morpho, lenders typically required higher APRs to fund these trades, which naturally limited their scale. On Aave, by contrast, the risk framework was set centrally by governance and its risk service providers, so ETH suppliers were effectively opted into financing the strategy whether or not they would have chosen that exposure themselves.

The obvious question, then, is who absorbs the loss when that pooled risk materializes. Aave’s answer is Umbrella, the safety module designed to backstop bad debt with staked junior capital.

Aave’s Immediate Response

85 minutes after the Kelp exploit, Aave froze all rsETH and wrsETH reserves across all deployments, setting LTVs to 0 and disabling new deposits and borrows, while repayment and liquidation remained active. As stress migrated to the WETH reserves and utilization hit 100%, borrow rates on WETH, the funding leg of these popular LST/LRT loops, rose to 10.5%, putting the billions in capital in these looping strategies into negative ROE. To contain the second order effects of this funding spike from leading to cratering health factors and liquidations on these loops, Aave updated the WETH Slope2 risk parameter to bring the interest rate at 100% utilization down to 3%. Subsequently, the WETH market was frozen, preventing new deposits and loans while still allowing for loan repayment, withdrawals, and liquidations, subject to available liquidity.

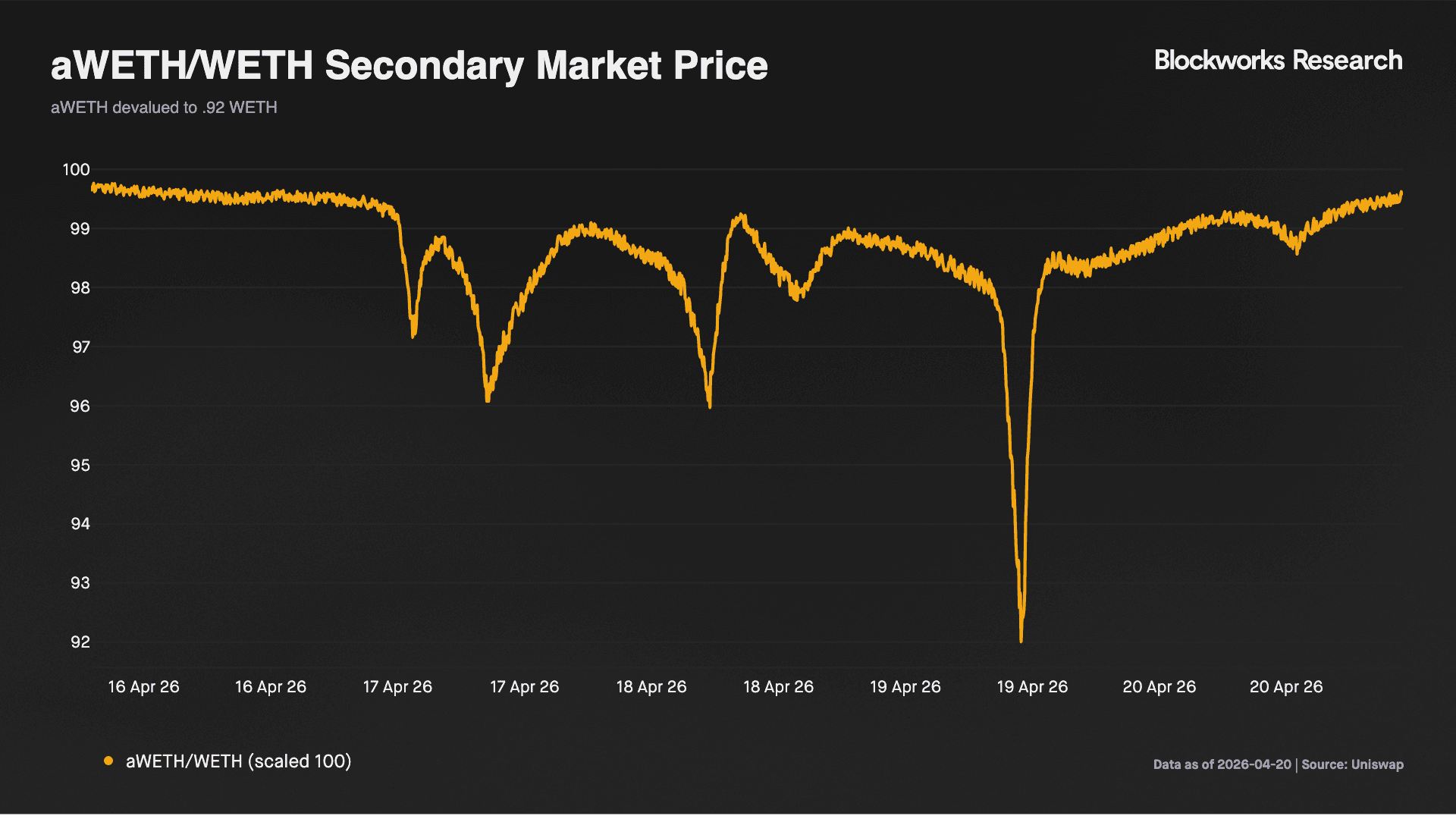

At 100% utilization, the aWETH position becomes illiquid, functionally converting what was a demand deposit into an illiquid loan with an indeterminate duration, elevated risk of impairment, and a reduced yield inadequate to compensate for this risk. The liquidation mechanism that is supposed to prevent bad debt from being realized also degrades in this regime. When a liquidator seizes collateral from an underwater position, the reserve has no available WETH to pay them in, so they receive aWETH instead, trapping liquidator capital in the same illiquid asset and weakening the incentive to liquidate at exactly the moment the protocol needs liquidation throughput most. The value of aWETH, which historically trades near a par value of WETH, traded down to an 8% discount and has since recovered.

As aWETH went illiquid and faced impairment risks, lenders increasingly borrowed stablecoins against their positions as an exit. This drove utilization in stablecoin markets towards 100% with interest rates spiking towards 15%. These positions now carry liquidation risk with respect to price depreciation on ETH, which was not the case for the ETH LST/LRT loops. While Aave’s emergency parameter updates may have reduced immediate bad debt risk in the WETH market, some of that risk was unintentionally displaced downstream into the stablecoin markets.

Umbrella as the Backstop

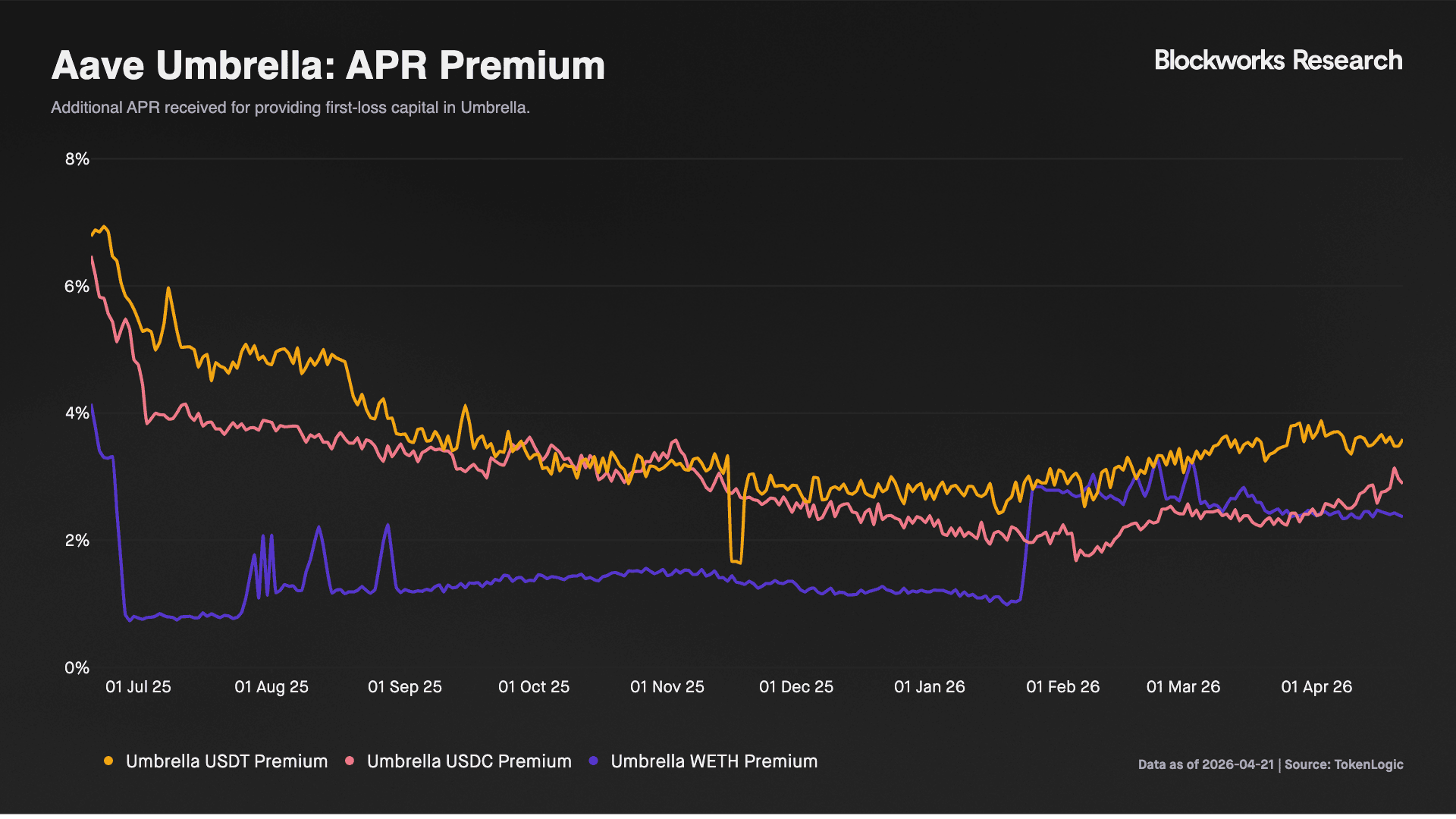

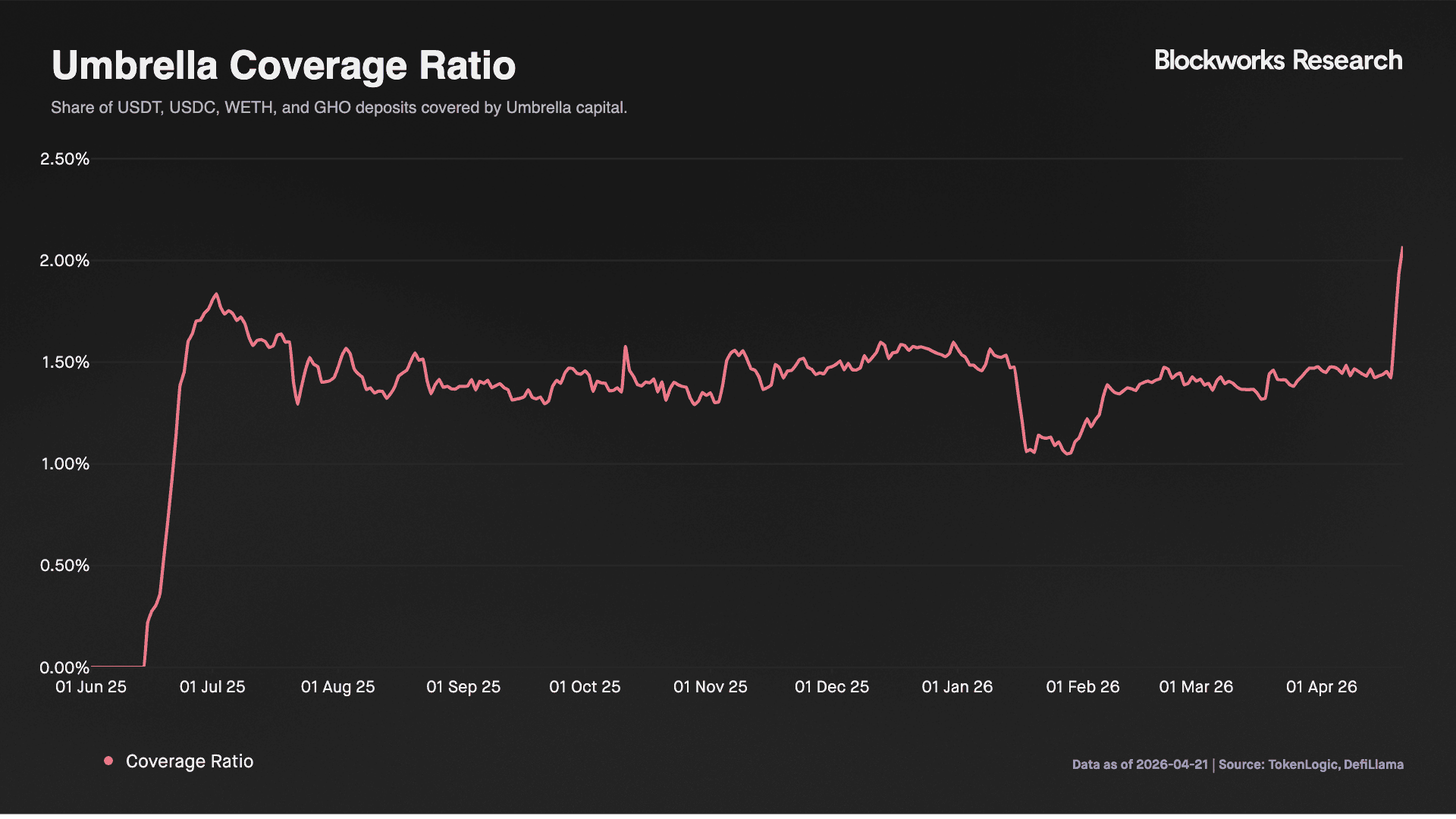

Aave’s Umbrella module now faces its first in-production stress test. The module allows asset depositors to stake their capital as first-loss protection in the event of bad debt in the underlying market. At construction and initial implementation, the mechanism seems elegant. The facility amassed over $370M in junior capital since its launch in June 2025 and was sitting at the target coverage level of $250M prior to the exploit. In the context of the historical realized bad debt, which was less than $5M, the Umbrella balance was sufficient. Lenders who staked in Umbrella received an additional 2-4% APR (shown below) and risked up to a 2% haircut on the principal should the historical levels of bad debt be realized in the future. Aave was financing the additional risk premium to Umbrella stakers with $8M per year from protocol revenues.

However, historical bad debt is an inaccurate forecast of the bad debt that may be realized in the future, and the future bad debt is precisely the left tail risk that Umbrella capital is liable to protect against. With USDT, USDC, and WETH offering the most common loan assets, Umbrella’s capital balance provided coverage on 1.5-2% of this deposit base.

Lending protocols like Aave price collateral risk primarily off the center of the distribution, incorporating expected volatility, liquidity depth, and correlation to borrowed assets under normal market conditions and where they may historically deviate. Liquidation thresholds, LTVs, and supply/borrow caps are configured so that if rsETH deviates modestly from peg, liquidators can profitably close positions before the book goes underwater.

What this framework cannot price, and what the Kelp incident made explicit, is the left-tail scenario where collateral value gaps lower because of an external, discrete failure arising from an exploit on a venue outside of Aave’s scope of risk management and opsec. Umbrella is the mechanism designed to absorb this residual. A reserve calibrated to ordinary liquidation slippage and asset variance is structurally undercapitalized for a regime where the dominant loss driver is an exploit event in adjacent protocols.

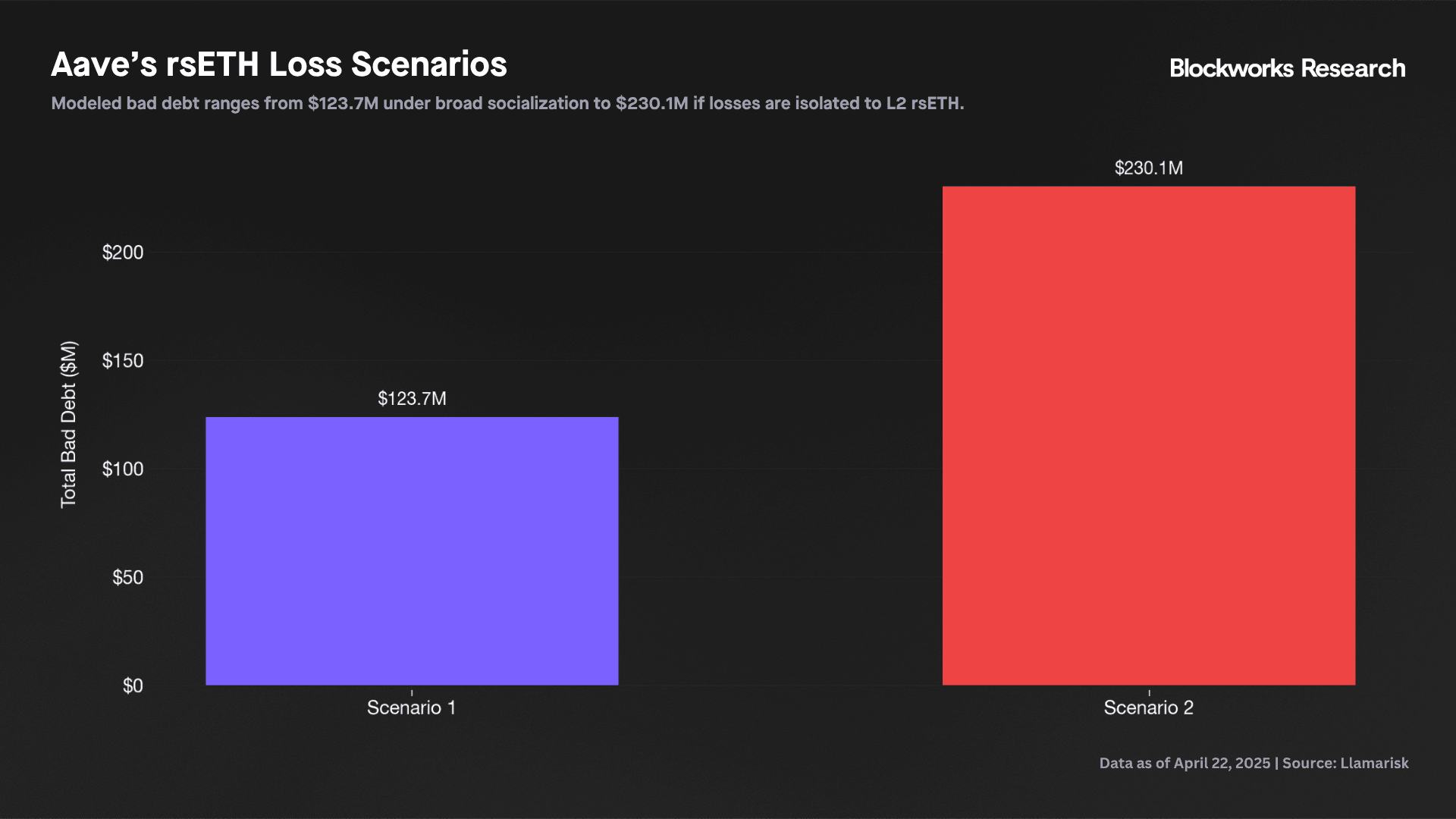

Aave service providers modeled two likely paths, with the outcome dependent on how Kelp allocates the loss. While resolution of the liabilities across Kelp, LayerZero, and Aave has yet to be finalized, and external or bespoke financing solutions may come into play, WETH Umbrella stakers currently face the prospect of a total loss of principal.

Scenario 1 (uniform socialization of losses by Kelp) spreads a 15.12% haircut across all rsETH holders on every chain, producing ~$124M in total bad debt, $91.8M of which lands on Ethereum Core WETH, with the remainder distributed thinly across L2s. Under this scenario, Umbrella’s 23,507 aWETH (~$54M) reserve is the primary first-loss layer for the $91.8M Ethereum Core shortfall, wiping out the Umbrella WETH balance. This is only large enough to offset roughly 59% of that loss, leaving ~$38M to be absorbed by the DAO treasury, external recovery, or aWETH depositors on Ethereum Core taking a ~0.60% haircut.

Scenario 2, where Kelp isolates losses to L2s, treats Ethereum mainnet rsETH as fully backed, and concentrates the entire loss on L2 rsETH via a 73.54% haircut, producing ~$230M in bad debt entirely on L2s. The Mantle instance alone faces a 71% WETH shortfall. Counterintuitively, the larger per-token haircut in Scenario 1 produces less total bad debt because spreading the shock across 119 positions lets each position's LTV buffer absorb part of the loss, whereas Scenario 2 blows through the L2 buffers entirely.

Under Scenario 2, Umbrella does not trigger at all, as the coverage does not apply to L2 markets, and mainnet is unaffected. In either scenario, the Umbrella module covers only a fraction of the potential loss, making the coverage gap the central balance-sheet question for the DAO. 80% of the $54M in Umbrella’s WETH balance has already entered the 20-day cooldown period, as depositors flee in an attempt to avoid the slashing. LlamaRisk proposed freezing the module to prevent capital flight prior to resolution from Kelp on the above scenarios and the corresponding implications for the Umbrella balance.

Aave’s balance sheet stands at $150M. Absent the recovery of stolen funds or an external financing solution, either Aave lenders, particularly those on L2s, or the DAO treasury will face a material haircut.

Zooming Out: Monolithic Lending Pools Underprice Risk

In 2022, a common framing during the CeFi blowups was that centralized institutions failed, while DeFi largely worked as designed. But recent events raise harder questions. How can users justify depositing into money markets when rates are often not even competitive with Treasury yields, yet principal could go to zero overnight? What protocols can users trust if even the largest lending venue has shown poor risk underwriting?

In just the past two weeks, more than $500M has been lost across the Drift and Kelp exploits, with contagion now spilling into other protocols, Aave most notably. Now that we have described the hack and its implications for Aave, it is worth stepping back to consider what these events may reveal about risk management and lending architecture more broadly.

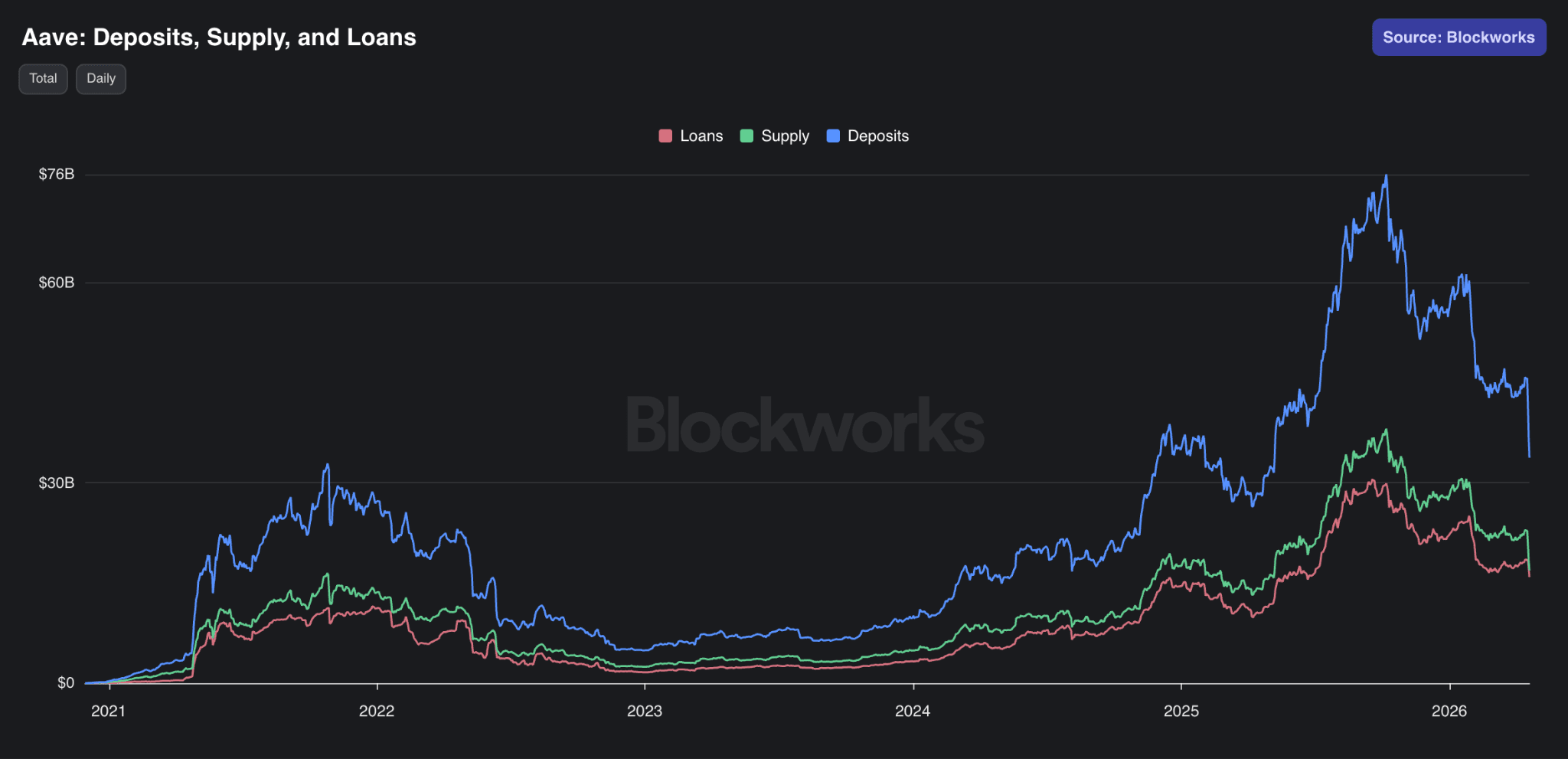

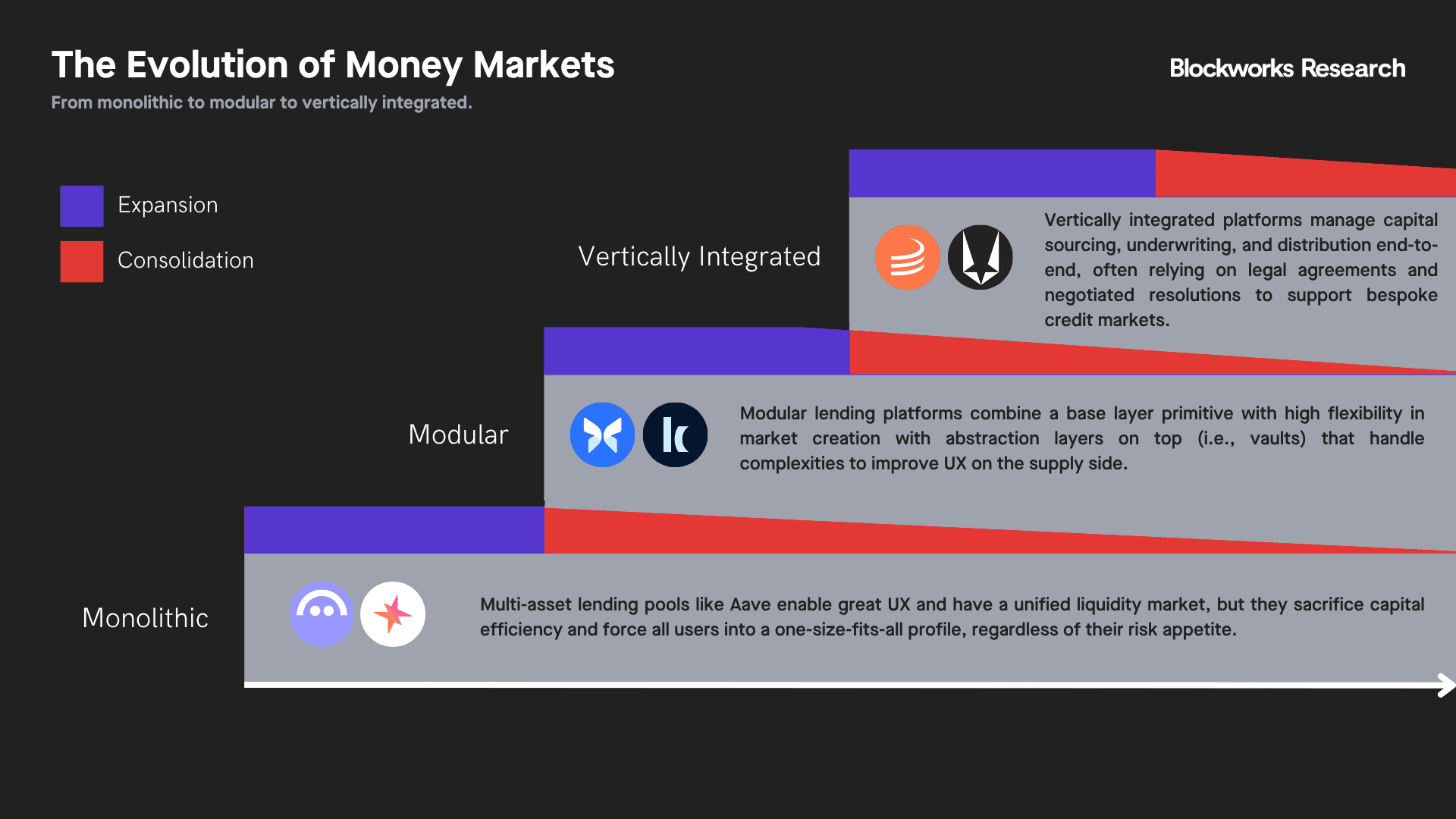

Despite scaling to over $75B in deposits and $35B in outstanding loans at its peak, Aave has remained architecturally anchored to the unified pool-based model popularized by Compound back in 2018.

That model has been enormously successful. It bootstrapped liquidity, enabled permissionless borrowing at scale, and works well when the collateral set is restricted to a minimal set of high-quality assets. But it also comes with tradeoffs, particularly as collateral moves down the risk curve.

The biggest is that pooled money markets socialize risk by default.

Because Aave forces all users into a one-size-fits-all framework, it can underprice the risk of certain collateral while overpricing others. For instance, one USDC borrowed against sUSDe should not carry the same rate as one USDC borrowed against USDT. In Aave v3, however, it does, which means USDC depositors effectively subsidize participants in the PT-sUSDe looping trade while bearing risks they may never have chosen to underwrite.

Of note, Aave v4 is designed to address this limitation. Aave v4 introduces Risk Premiums, which make borrow rates partially user-specific and dependent on the collateral backing the loan. Combined with a hub-and-spoke architecture and more isolated markets, Aave is moving toward more granular risk pricing and better segmentation.

The Monolithic vs. Modular Debate

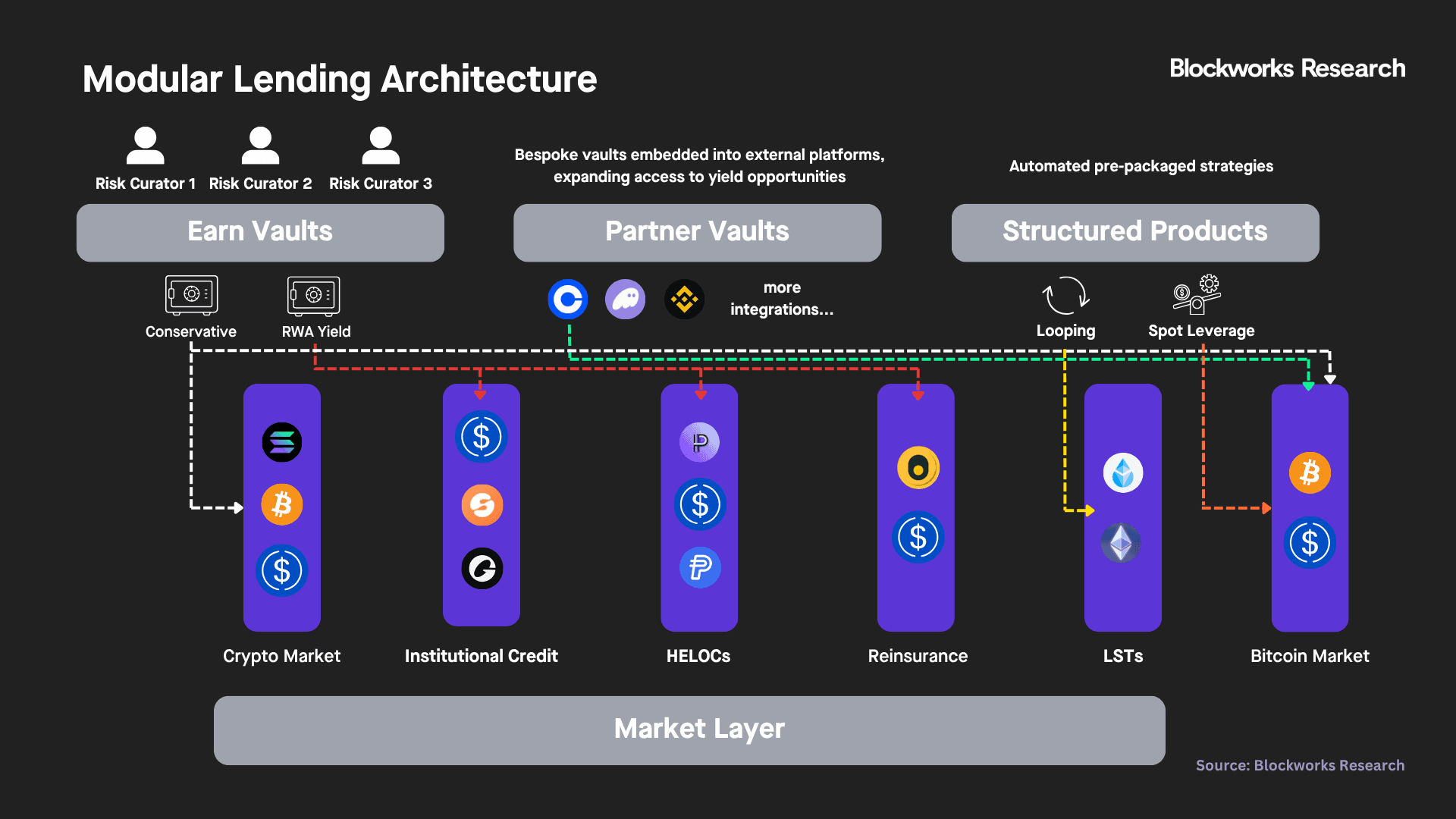

Protocols like Morpho, Kamino V2, and Euler V2 introduce modularity through permissionless market creation and abstraction layers on top, such as vaults, which aggregate liquidity and improve the user experience, primarily on the supply side. Modular lending represents a meaningful improvement by isolating risk across markets.

At the foundation sits the market layer, where a diverse set of markets can be created to serve different users, use cases, and risk profiles. Rather than forcing all assets into a unified pool, modular architectures allow markets to be tailored around specific collateral types and underwriting assumptions. An RWA market, for instance, could be deployed that only accepts pre-approved assets as collateral, while other markets may be optimized for crypto spot leverage, institutional credit, reinsurance, or LST-backed strategies.

Just as important, the protocol’s role is not simply to support market creation, but to onboard competent risk curators who can package these opportunities into differentiated vault strategies.

This architecture also enables partner vaults, where external platforms can embed bespoke vaults directly into their own products, as seen in integrations like Morpho’s partnership with Coinbase, which has helped drive over $2.5B in BTC inflows into Morpho. Finally, modular designs make it easier to build structured products on top, automating strategies like looping in isolated, capital-efficient markets.

That is not to say modular lending comes without tradeoffs. Protocols like Morpho and Kamino can better isolate and cap losses at the vault or market level, though the burden of trust shifts more toward protocols carefully whitelisting curators and users deciding who they trust.

Importantly, modularity may prevent loss socialization, but it does not prevent loss propagation through correlated exposures. Last month, roughly 15 Morpho vaults with non-negligible exposure (>$10k) were affected following the Resolv USR exploit. While the loss ceiling was bounded per vault, the simultaneous impact across multiple vaults highlights a broader contagion footprint. At the same time, curators like Steakhouse showcased strong risk management, underscoring the value of isolating risk while giving users a choice.

Unfortunately, the advantages of modular architecture may only be fully appreciated by the market after an event like the Kelp exploit. Since late 2024, we have viewed modular money markets as the natural evolution of monolithic lending. That said, modularity may not be the final form of onchain credit. A renewed shift toward more vertically integrated “CeDeFi” models such as Maple, Pareto, and Wildcat may be another outcome.

Unlike unified pools or curator-led modular systems, these platforms more closely resemble traditional credit markets, combining onchain capital formation with centralized underwriting, legal agreements, and more bespoke liquidation processes. In some cases, non-atomic liquidations and negotiated restructurings can make markets safer when collateral values are uncertain or difficult to realize instantly.

More importantly, vertically integrated models offer clearer attribution of responsibility and legal recourse, which may become increasingly valuable after incidents like Kelp, where accountability is fragmented across protocols, bridges, and infrastructure providers. As DeFi scales, trust may increasingly accrue not just to architecture, but to platforms that can underwrite, distribute, and enforce credit risk end-to-end.

Market Share Implications

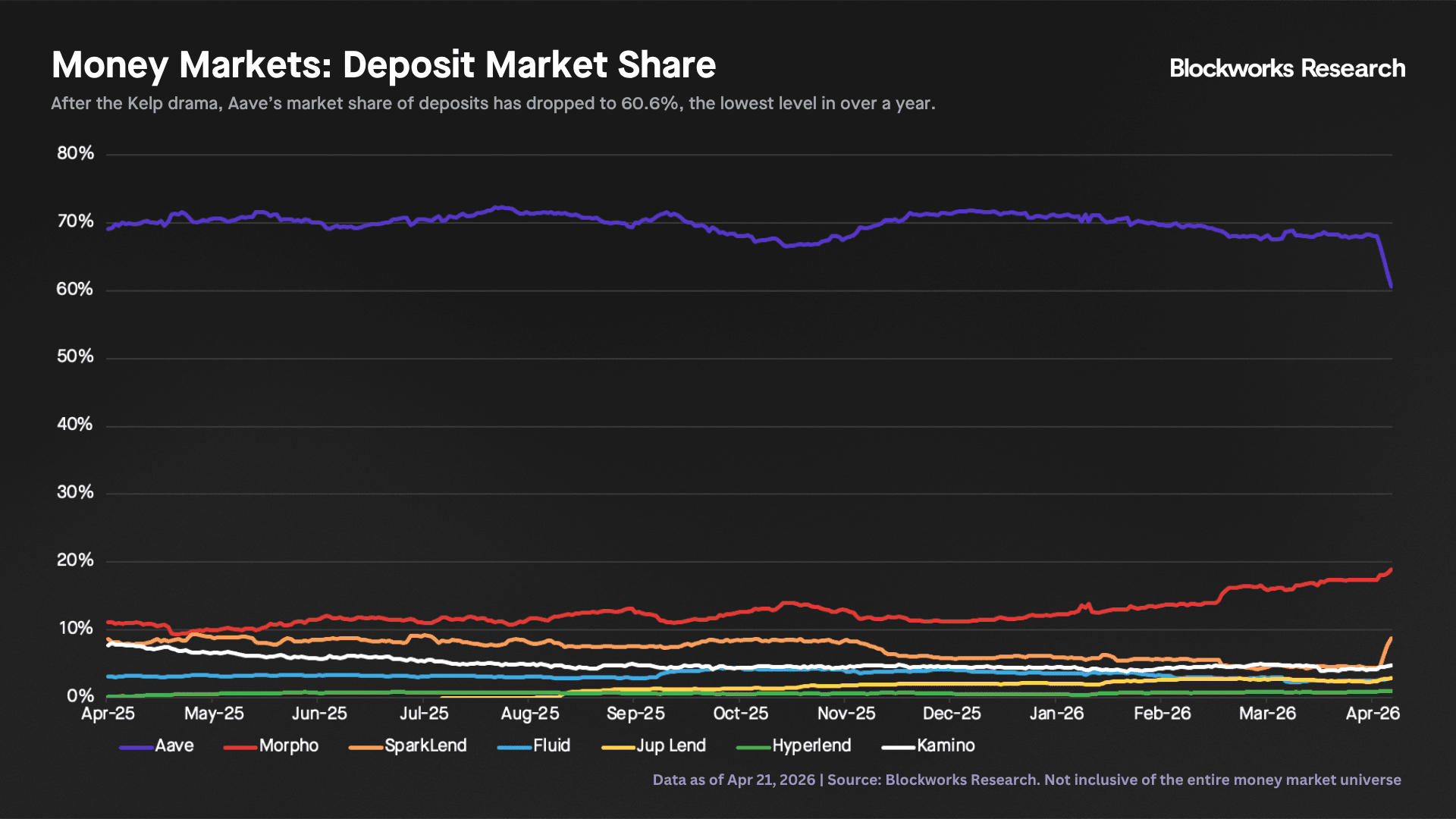

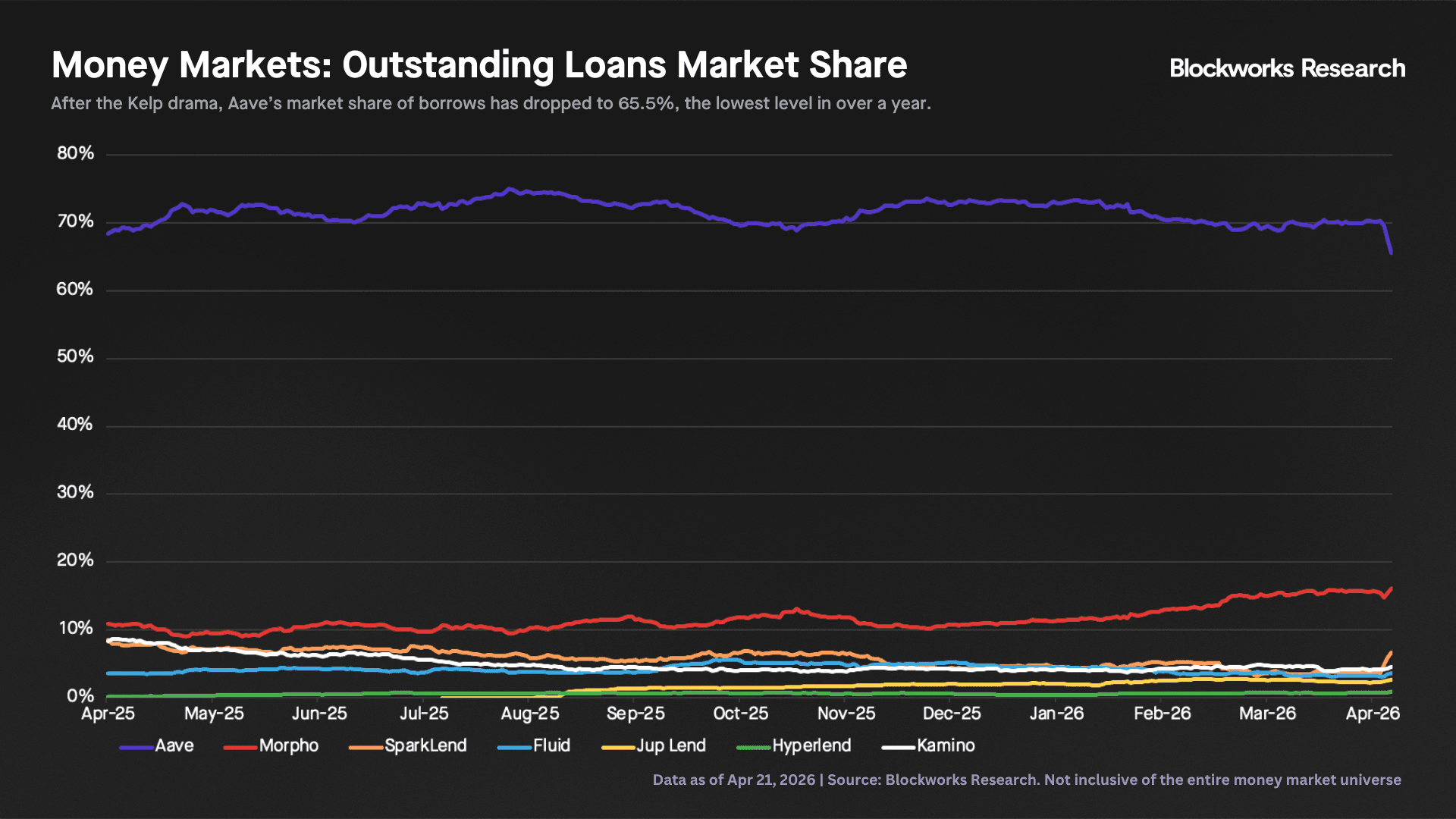

In practice, however, Aave built a defensible liquidity moat in lending, compounding its lead over every other protocol. It has historically dominated nearly every major asset vertical, from stables and LSTs to ETH and PTs, and at its peak commanded nearly 70% market share in deposits and outstanding loans.

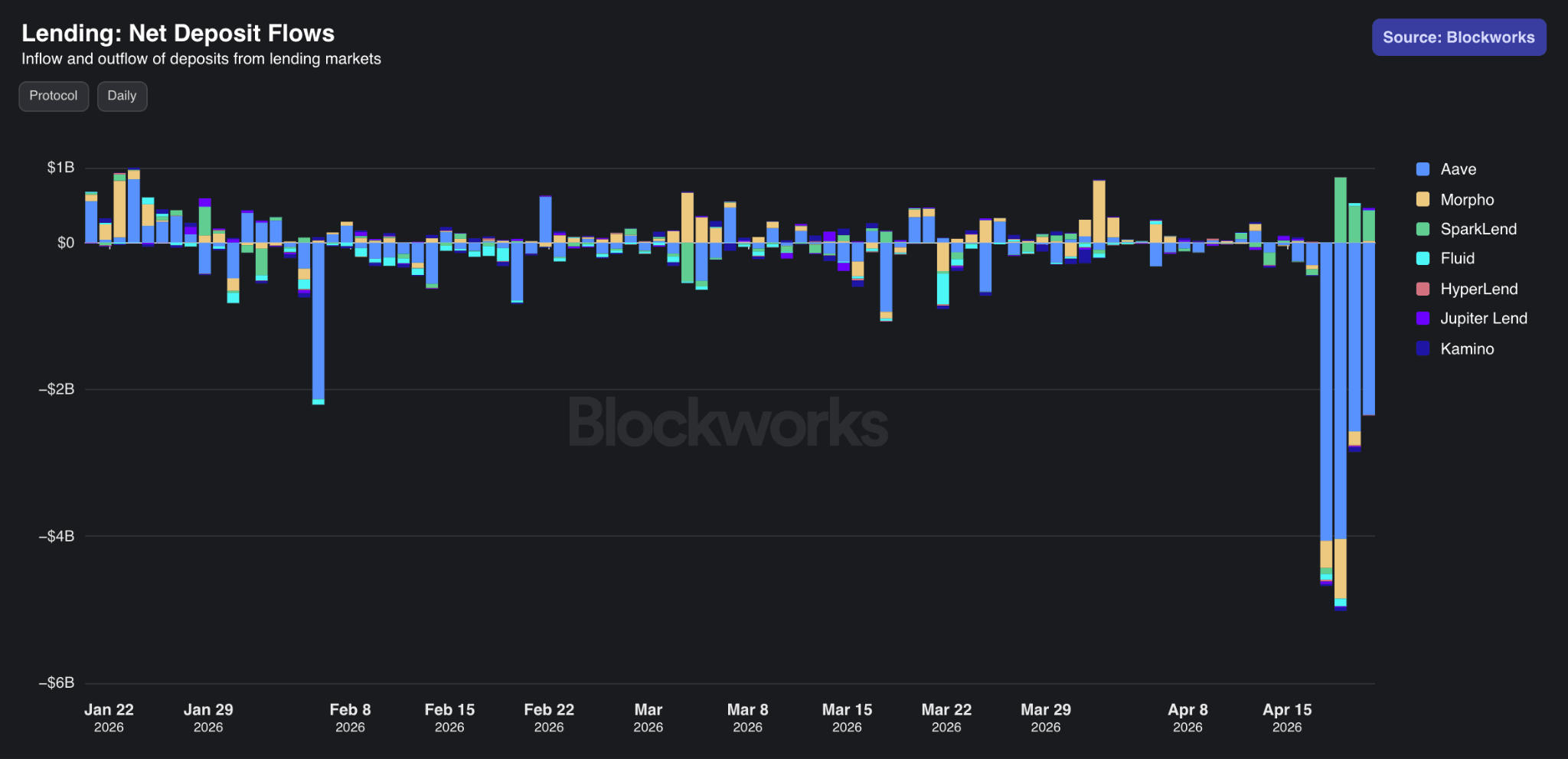

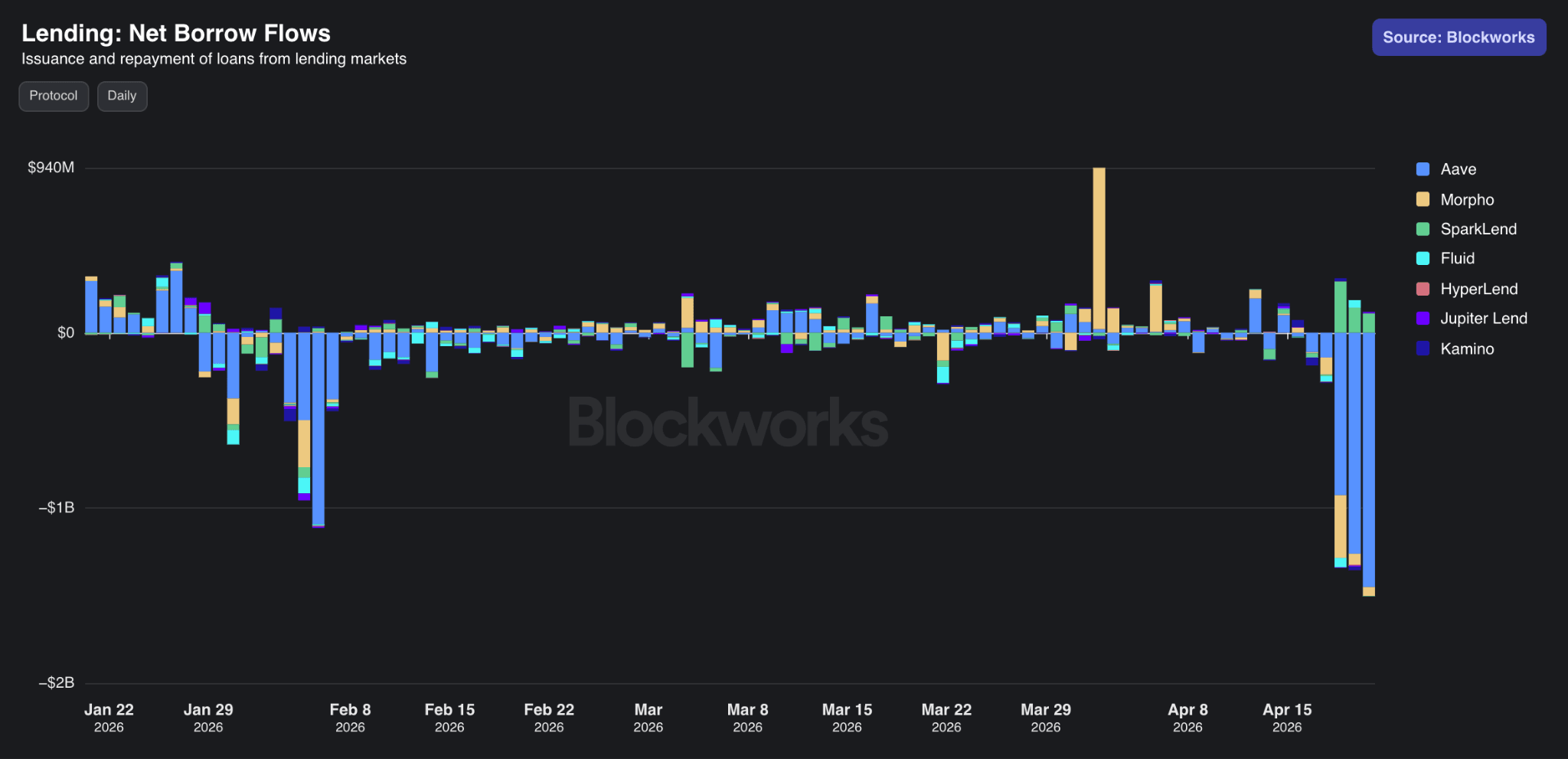

The Kelp-Aave situation may prove to be a catalyst for modular and CeDeFi platforms to accelerate market share gains. In the four days following the exploit, Aave experienced a bank run, with over 30% of its deposit base withdrawn. As shown below, Aave’s share of deposits relative to other money markets like Morpho, SparkLend, and Kamino fell from roughly 68% to under 61% in just four days, the lowest level in well over a year.

That move is notable not simply because of the magnitude of withdrawals, but because it may mark the first meaningful crack in Aave’s long-standing liquidity moat. If depositors increasingly view risk isolation as a feature worth paying for, recent events could accelerate a structural shift in where capital chooses to reside.

Interestingly, however, the largest beneficiary of inflows challenges a simplistic “modular lending will win” thesis: SparkLend.

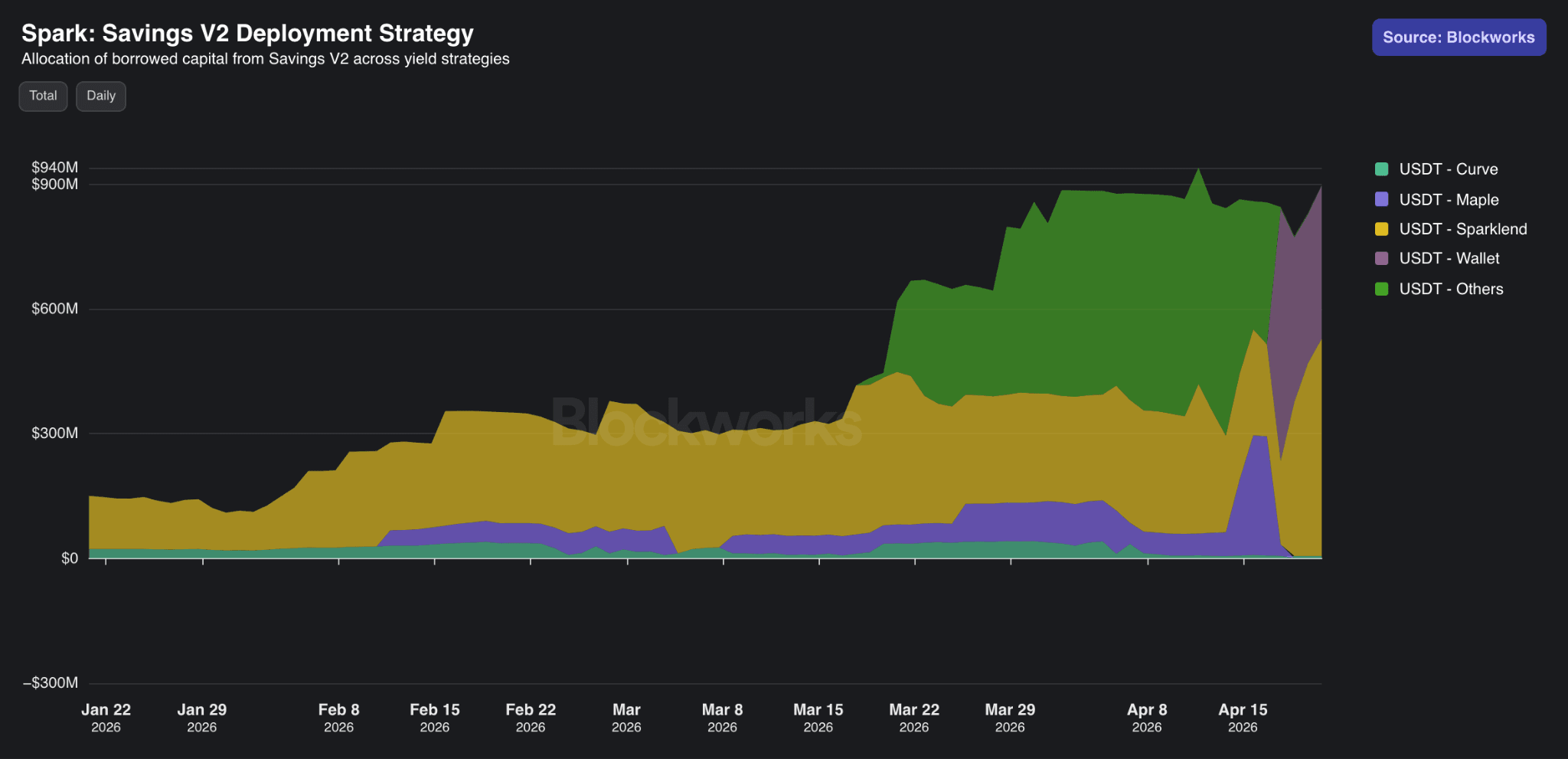

Despite its unified pool architecture, SparkLend saw roughly $1.8B in inflows over April 19-21, appearing to be viewed as a safe haven. This suggests capital may not simply be rotating toward modular architectures, but toward protocols perceived to have superior risk management.

SparkLend had no exposure to rsETH, having deprecated the asset alongside other low-usage markets back in January. Even if rsETH had remained listed, Spark’s more conservative design likely would have limited losses of the same magnitude through rate-limited supply and borrow caps that constrain how quickly exposure can scale.

Just as importantly, SparkLend demonstrated stronger liquidity management during the crisis. At a time when Aave’s USDT market and several Morpho vaults are at 100% utilization, Spark has maintained the most robust liquidity position, having over $350M in instantly available liquidity in spUSDT.

While the exodus has been concentrated on the depositor side, market share in outstanding loans has been somewhat more stable, suggesting borrowers have not unwound positions at the same pace, partly due to Aave freezing the WETH market. Still, Aave’s share of outstanding loans has also fallen to 65.5%, likewise the lowest level in over a year.

SparkLend, once again, has benefited the most in net borrow flows, seeing over $540M in net borrow flows over Apr. 19-21, with most outstanding loans USDT-denominated, again reflecting its position as the only major money market with sufficient USDT liquidity during the crisis.

SparkLend may be less a rebuttal to the modular thesis than a reminder that architecture alone does not determine trust. Ultimately, risk management matters more than protocol design. Even modular systems are only as strong as their curators, and poor underwriting can still lead to user losses despite isolated markets.

Whether this proves temporary or marks the start of a more durable re-rating in lending market structure remains an open question. Recent flows suggest the deeper re-rating may be occurring not just across architectures, but across perceptions of who underwrites risk most credibly.

For the first time in years, Aave’s dominance appears meaningfully contestable.

Looking Forward: A New Market Structure for Lending

Credit always has an implicit element of trust. Even in an overcollateralized model, users must trust that a protocol is underwriting onboarded collateral diligently and understand the risks they are taking. Any money market, regardless of architecture, relies on someone underwriting risk.

Recent flows suggest this may not simply be an architectural debate, but the beginning of a segmentation in lending markets.

On one side, unified pool markets may continue to work well for a narrow set of assets whose risk is primarily continuous and estimable, think BTC, ETH, USDT, and USDC, where the dominant risks are price volatility and liquidity, both of which can be reasonably modeled through LTVs and liquidation thresholds. Shared liquidity remains highly valuable in these markets. In that world, protocols with battle-tested risk management and strong liquidity operations may continue to thrive, as exemplified by Spark.

By contrast, assets with hybrid or discrete risk profiles, such as LSTs or bridged assets, introduce jump risks from protocol, bridge, or smart contract failures that unified pools are structurally less equipped to price without tightly capping exposure.

Modular lending platforms may be better suited to scale these assets, as well as long-tail and net-new assets in DeFi. Permissionless market creation, isolated risk, and specialized curators can support a broader set of opportunities without forcing those risks into a unified pool, giving lenders discretion over which assets they are willing to underwrite and the return they require for doing so.

At the same time, more vertically integrated “CeDeFi” models may continue to gain share in bespoke or institutional credit markets, where underwriting, legal enforceability, and negotiated resolutions matter more than atomic liquidations or permissionless access. These models may be better positioned to support undercollateralized credit, structured products, and other markets that more closely resemble traditional finance.

Rather than one model displacing the others, the market may be moving toward a new market structure, where different lending architectures serve different parts of the risk spectrum. Unified pools may remain dominant for highly liquid, continuously priced collateral; modular platforms may expand the frontier of long-tail and hybrid-risk assets; and vertically integrated CeDeFi models may gain share in bespoke and institutional credit markets. If so, the future of DeFi lending may be less about a single winning architecture and more about matching the right structure to the risks being underwritten.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.